The most gifted runners not only go faster and with a smoother gait. They also need less recovery time. The phase of the current bull market that pushed off the blocks six months ago is proving elite at refreshing itself with the briefest of respites before continuing forward to the next mile marker. The S & P 500 fell a maximum of 2.98% using intraday prices, nearly all of that in one day on Oct. 10, after President Donald Trump rhetorically re-escalated the U.S-China trade confrontation. The index then spent the next nine trading days inside that single-day range until it broke to a fresh high this past Friday, briefly surpassing 6,800, after an unthreatening CPI report removed one possible impediment to the two more Federal Reserve rate cuts expected by year’s end. The main reason the CPI report released the indexes higher is that it simply passed, making Big Tech earnings next week the next known swing factor and allowing the old favorites of the AI trade to reassert leadership. .SPX 3M mountain S & P 500, 3 months This column last week suggested that “an ideal scenario for the remainder of the year would have the recent choppiness last a bit longer to qualify as a proper scare, skimming the froth off the speculative stuff and resetting expectations in a way that rebuilds investors’ capacity to be surprised to the upside.” As of now, it appears no genuine scare was needed, unless we count the couple of days last week when gold, crowded momentum plays and unserious meme stocks were liquidated in a slightly sloppy but ultimately benign rotation. Evercore ISI equity strategist Julian Emanuel makes the case that the manic surge-and-swoon act in gold and connected high-velocity speculative stuff need not dictate the broader market path: “As was the case in early 2021 when the peak in meme stocks, SPACs and profitless tech created brief instability in markets generally, gold’s selloff has been accompanied by selloffs in other speculative themes from quantum computing to lithium to uranium. Yet as it was in 2021, where the S & P 500 rallied an additional 23% from the meme-stock fizzle to the capital markets fueled peak a year later, rumors of speculation’s demise in 2025 are greatly exaggerated.” This is well-observed, though the obliteration of the frothiest market themes from their early 2021 peak was far more damaging than anything seen so far this month. Tireless retail buying And anything resembling the demise of the speculative fervor is hard to locate. Citadel Securities equity trading-flow guru Scott Rubner on Friday extolled the persistent aggression in somewhat valuation-insensitive small-investor activity, noting that 22% of trading volume now comes from retail accounts – the most since (yup) February 2021 – and retail has been a net buyer of stocks 23 of the past 27 weeks. And, truly, what would deter such excitable, tireless buying among non-professionals when AI hype is being invoked by so many adjacent industries and marginal companies, when Robinhood is blurring the line between investing and gambling with sports-prediction contracts in their app, when whole subsectors (rare minerals, quantum computing) get pumped to the stratosphere on the mere hint of the Trump administration possibly taking a stake, in a dynamic I call “too rigged to fail?” Yet for all the fun and games, the genuine fundament of corporate value – real profits – are coming through nicely to substantiate generally elevated valuations. Companies so far are beating forecasts at around an 80% rate, better than the norm. Stocks aren’t universally being rewarded for it, but it moves the chains on forward earnings-growth forecasts. Of course, total S & P 500 earnings for 2025 are now looking as if they’ll come in below where consensus pegged them at the start of the year. On Dec. 31, the full-year estimate was $274, which fell to $264 by July and is now up to $268. That’s a 2% decline over a ten-month stretch in which the S & P 500 index is up 15.5%. So, yes, the market is more expensive now, but there’s always next year. Consensus for 2026 is tracking above $304, which is now becoming the denominator for all investor valuation assumptions and return projections. This is what bull markets do, they roll forward their optimism until forced to rethink it. Was the little wobble in popular momentum stocks enough to soften up expectations to receive good news on tech results with enthusiasm? John Flood, Head of Americas Equities Sales Trading at Goldman Sachs, says yes, in a trading-desk note: “This week’s painful drawdown in momentum…has only added to the already significant wall of worry out there. As a result, the sentiment/positioning setup into the heart of mega-cap tech earnings is the friendliest I have seen in quite some time. If no foot faults from MAGMA (Microsoft, Amazon, Google, Meta, Apple) next week (we are not expecting any) I am bracing for another leg higher at the index level led by super-cap tech.” Year-end upside again? Just a few reasons it’s tough for bears to find a meal in a year like this, especially as we get deeper into the fall. Everyone knows most years have an upward bias in the final two months of the year, even more so when the first ten months have been strong. Granted it’s hard to make a specific case for why this year will fall into the 20% of instances when year-end seasonality failed, yet it’s worth noting that the seasonal signals have been glitchy this year. We were supposed to be up handily into April, but the S & P had a 15% year-to-date drawdown by April 8. The chart below, from Renaissance Macro Research, plots the forward-three-month S & P 500 return for each date, based on decades of market history. Last week we hit what’s supposed to be the best entry point for three-month-forward gains. But note that almost exactly three months ago was meant to be the worst moment to buy (in late July) and since then the index is up 6%. Two weeks ago, the president’s social-media growling about higher China tariffs exposed a node of complacency among investors, who as a group had turned their focus away from the trade-policy flux. Rationally so, in a sense, given the incentives all around to be sure that things settle into a manageable arrangement. Alongside a few corporate-credit hiccups and overbought speculative sectors, the risk-off reaction briefly overwhelmed the market’s usual capacity to absorb shocks through rotation. If forced to identify another node of complacency it might be investors’ comfort level with the underlying sturdiness of the economy. The conventional wisdom sees meager job growth as largely a result of immigration restrictions and demographics, disconnected from still-healthy GDP-tracking models that capture urgent capex levels and free spending by the affluent. It’s a plausible and defensible stance. And it’s true that overall (unofficial) consumption data and corporate commentary are not raising any alarms. Still, the market is no longer sending as emphatic a message about the pace of growth as it was several weeks ago, even. Equal-weighted consumer discretionary stocks are no longer outperforming. Industrials are better but have stalled on a relative basis. Veteran strategist Jim Paulsen of Paulsen Perspectives says, “A good proxy for U.S. economic surprises may be the relative performance of S & P cyclical sectors. Cyclicals have continued underperforming badly since Oct 1!” Warren Pies, founder of 3Fourteen Research, points out, “During this October wobble, homebuilders and other key cyclical areas of the market have lagged. Simultaneously, the AI trade has powered higher. Against the backdrop of falling yields, these intra-market moves point to nascent growth concerns.” Accumulated anecdotes could include an uptick in corporate layoff news, weak S & P PMI manufacturing sentiment, mortgage-application volumes not responding much to lower rates. There’s a good chance the market is cushioned against a growth scare by AI, by the Fed’s dovish turn and by the projected stimulative effects of the new tax law fattening tax refunds early next year. And maybe no news can remain good news for now in the absence of government data, and then perhaps the Street will give the data a Mulligan once it comes given the shutdown distortions. This low-volatility ascent since April quite resembles the imperturbable rally through all of 2017. That run required a steep acceleration higher into January 2018 accompanied by euphoric investor expectations for policy-driven growth, reaching serious excesses well beyond present conditions before breaking hard into a flash correction. None of this is enough to withhold the benefit of the doubt from the bulls for now, of course. But such issues can serve as a study guide for when the tape goes in search of an excuse to administer its next test.

Blog

-

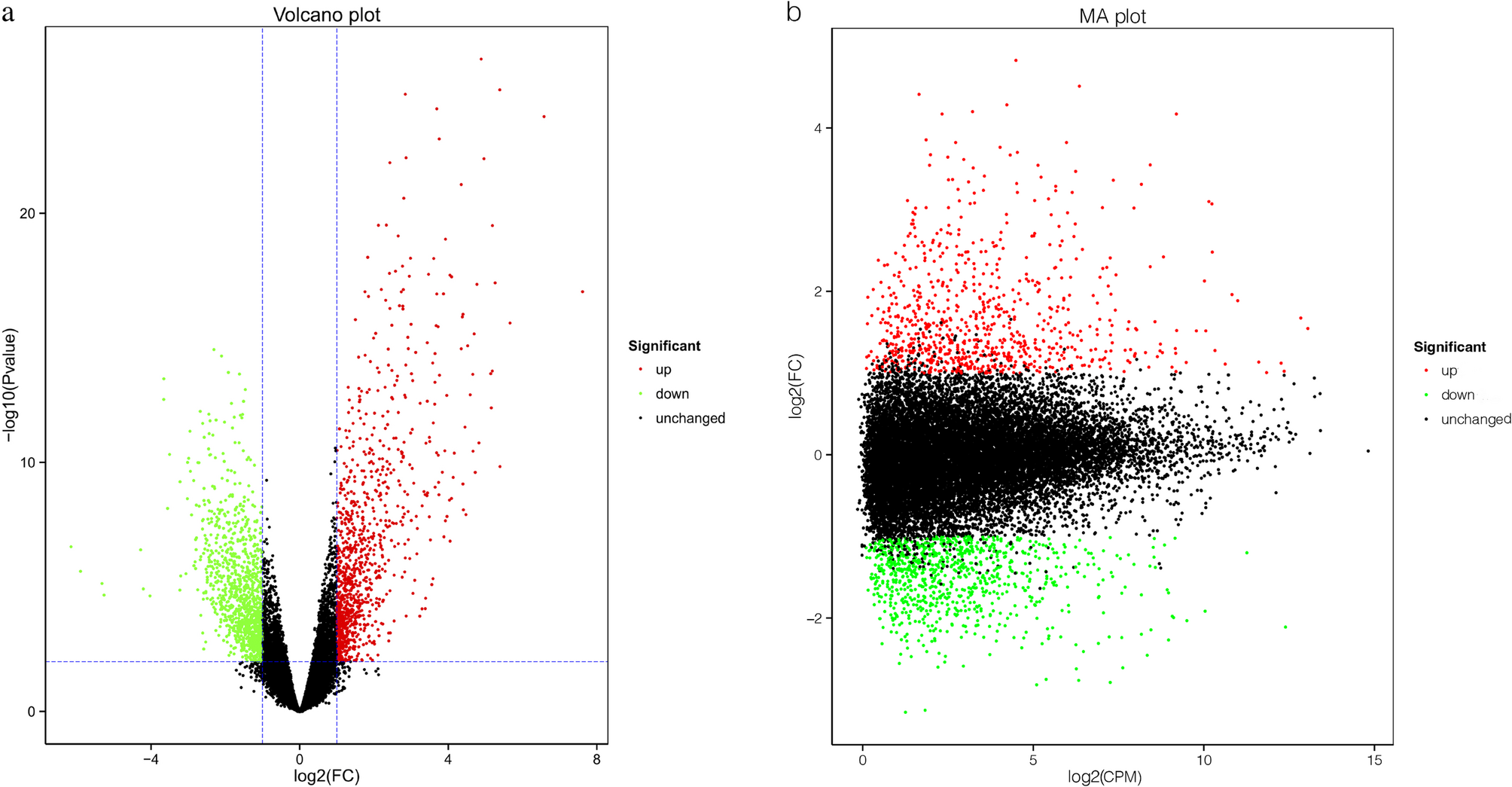

Full-length transcriptome analysis of papillary thyroid carcinoma reveals correlation between LAMB3 expression and clinical features | BMC Cancer

Patients

Each study participant voluntarily provided informed consent. The criteria for inclusion were as follows: (i) 18 to 80 years of age with positive diagnosis of PTC using paraffin-embedded biopsy samples; (ii) no prior thyroidectomy; (iii)…

Continue Reading

-

Retinal Biomarkers Track Multiple Sclerosis Severity

A recent large-scale study has revealed new insights into the structural changes of the retina in multiple sclerosis (MS) patients, highlighting potential biomarkers for disease monitoring and severity assessment. Researchers analyzed optical…

Continue Reading

-

Scientists Invented an Entirely New Way to Refrigerate : ScienceAlert

Say hello to ionocaloric cooling. It’s a new way to lower temperatures with the potential to replace existing methods of chilling things with a process that is safer and better for the planet.

Typical refrigeration systems transport heat away…

Continue Reading

-

Trump says open to making concessions to China to calm trade war – POLITICO

“We’re at 157 percent tariff for them. I don’t think that’s sustainable for them,” Trump said.

“They want to get that down, and we want certain things from them,” he added.

Trump is set to meet with Chinese leader Xi Jinping at the…

Continue Reading

-

Life’s Ingredients Found Frozen Beyond The Milky Way For First Time : ScienceAlert

For the first time, astronomers have seen life’s building blocks in ice beyond the borders of our galaxy.

Among a mix of complex organic molecules trapped in ice circling a newborn star in the Large Magellanic Cloud, researchers found ethanol,…

Continue Reading

-

Here’s where the James Webb Space Telescope and 4 other legendary spacecraft are in October’s night sky

Humanity’s understanding of the solar system has evolved dramatically following the advent of spaceflight. Over the past seven decades, thousands of sophisticated spacecraft have been launched on ambitious missions to look down on our planet,…

Continue Reading

-

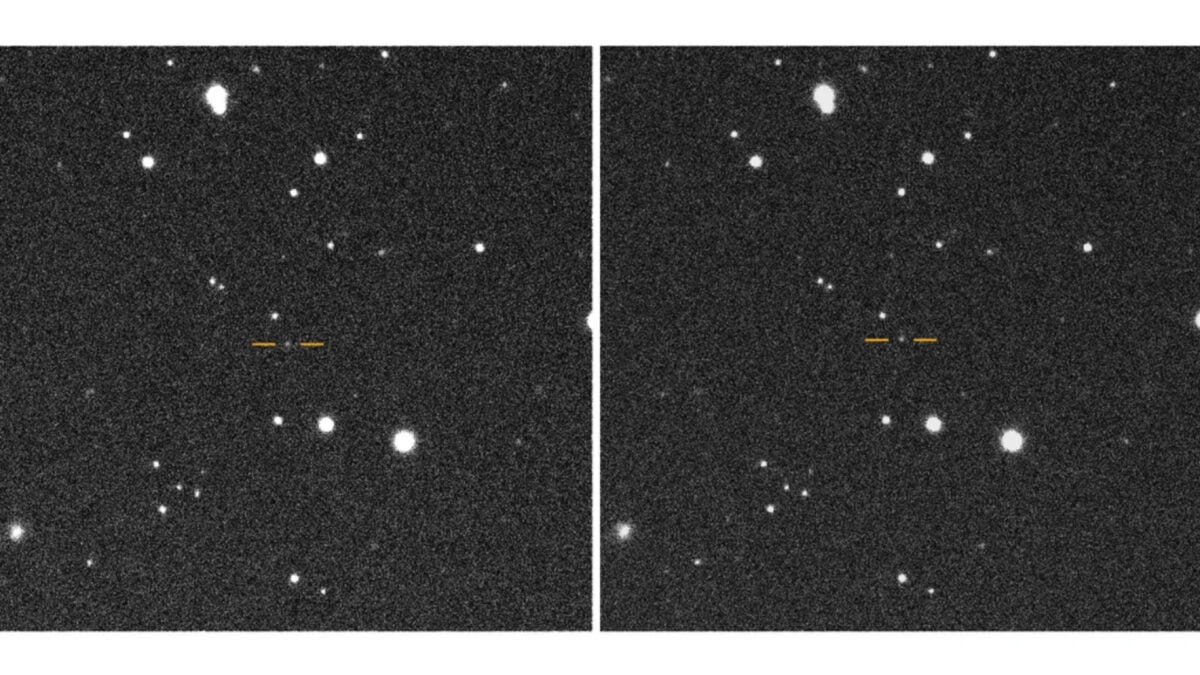

Astronomers Just Found a Sneaky Asteroid Near the Sun—and It Highlights a Dangerous Blind Spot

Millions of asteroids are currently zipping through our solar system. These rocky remnants of the early solar system receive extra attention when their itinerary brings them too close to Earth—which, fortunately, astronomers can…

Continue Reading

-

AI spending is boosting the economy, many businesses in survival mode

Cameron Pappas, owner of Norton’s Florist

Norton’s

For Cameron Pappas, owner of Norton’s Florist in Birmingham, Alabama, the artificial intelligence boom is a world away.

While companies like Nvidia, Alphabet and Broadcom are lifting the stock market to fresh highs and bolstering GDP, Pappas is experiencing what’s happening in the real economy, one that’s far removed from Wall Street and Silicon Valley.

Small businesses like Norton’s, and companies of all sizes in retail, construction and hospitality, are struggling from higher costs brought by the Trump administration’s sweeping tariffs, and as downbeat consumers reduce their spending.

“We’ve just got an eagle eye on all of our costs,” Pappas, 36, told CNBC in an interview.

Norton’s generated $4 million in revenue last year, selling flowers, plants and gifts to locals. To avoid raising prices, which could cause customers to flee, Pappas has been forced to get creative, reworking some of his designs.

“If a bouquet has 25 stems in it, if you reduce that by three to four stems, then you’re able to keep the price the same,” Pappas said. “It’s really forced us to focus on that and to make sure that we’re pricing things the best that we possibly can.”

Pappas’ story and many like it are being masked in the macro data by the power of AI. In the first half of the year, AI-related capital expenditures contributed to 1.1% of GDP growth, according to a September report from JPMorgan Chase. That spending outpaced the U.S. consumer “as an engine of expansion,” the report said.

Total U.S. GDP increased at an annual rate of 3.8% during the second quarter of 2025 after falling 0.5% in the first quarter, the Commerce Department said.

U.S. manufacturing spending has contracted for seven straight months, according to the Institute for Supply Management. And construction spending has been flat to down, due to high interest rates and rising costs. Cushman & Wakefield said in a report this month that total project costs for construction in the fourth quarter will be up 4.6% from a year earlier because of tariffs on building materials.

The stock market shows a similar disconnect between AI and everybody else.

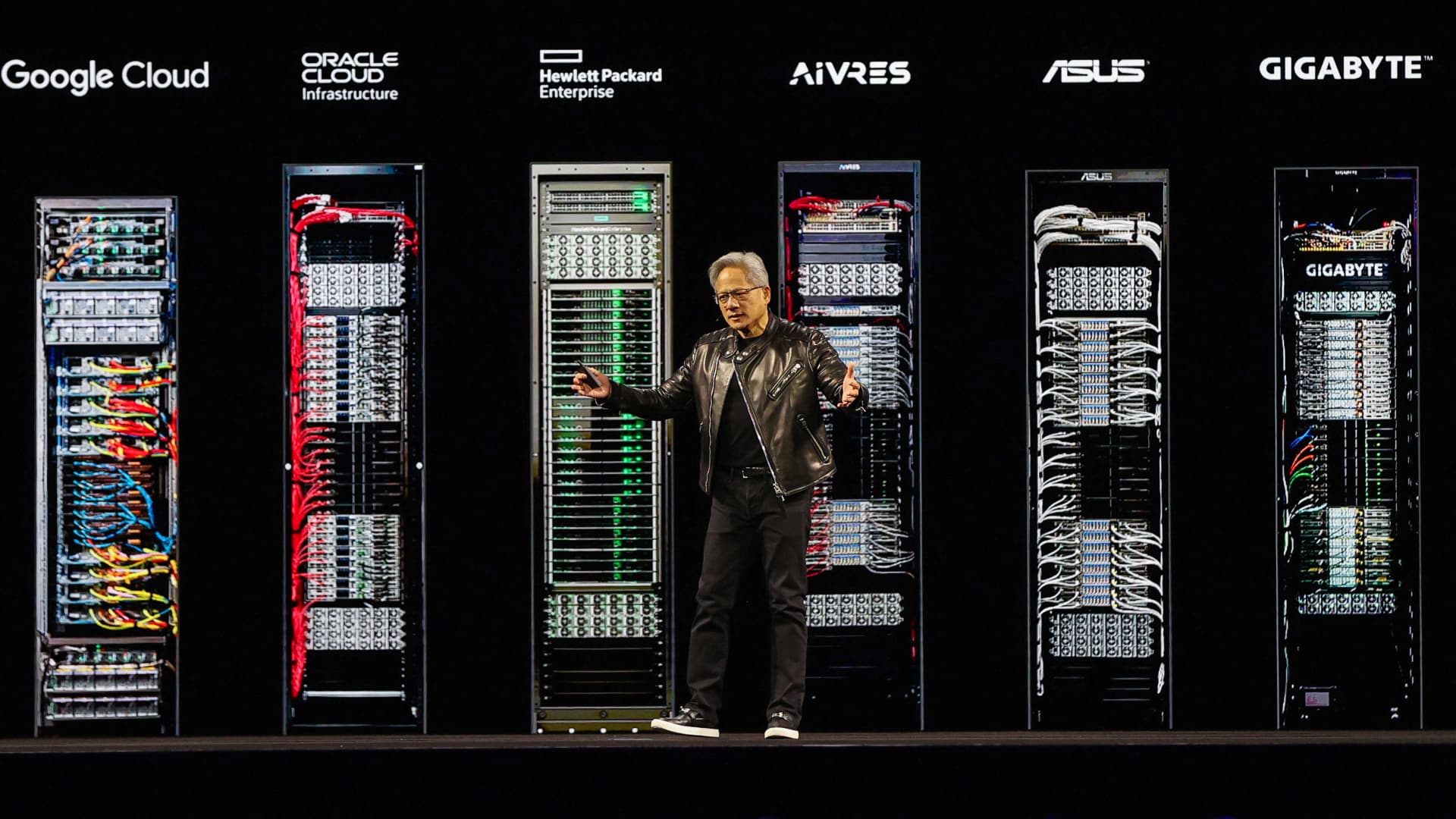

Nvidia CEO Jensen Huang delivers the keynote for the Nvidia GPU Technology Conference (GTC) at the SAP Center in San Jose, California, U.S. March 18, 2025.

Brittany Hosea-Small | Reuters

Eight tech companies are valued at $1 trillion or more and, to varying degrees, are all tied to AI. Those companies — Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta, Tesla and Broadcom — make up about 37% of the S&P 500. Nvidia, with a $4.5 trillion market cap, accounts for over 7% of the benchmark’s value by itself.

Investors are giddy about the massive investments they’re seeing in AI infrastructure. Broadcom shares are up more than 50% this year after more than doubling in each of the prior two years, while Nvidia and Alphabet have jumped almost 40% in 2025.

That explains why the S&P 500 and Nasdaq are up 15% and 20%, respectively, reaching record highs on Friday, even as the government shutdown continues to cause economic angst.

Meanwhile, the S&P 500 subgroups that include consumer discretionary and consumer staples companies have increased by less than 5% year to date.

The latest troubling sign in the consumer market came on Thursday, when Target said it’s cutting 1,800 corporate jobs — the retailer’s first major round of layoffs in a decade. Target shares have plunged 30% this year.

“I think the message that the AI economy is sort of driving up the GDP numbers is a correct one,” Arun Sundararajan, a professor at New York University’s Stern School of Business, told CNBC in an interview. “There may be weakness in the rest of the economy, or not weakness, but there may be more modest growth.”

Investors will hear all about AI in the coming days, the busiest stretch of the quarter for tech earnings, and will be listening closely for additional guidance on capital expenditures. Meta, Microsoft and Alphabet report on Wednesday, followed by Apple and Amazon on Thursday.

Nvidia’s stock over the last year.

Last month, Nvidia announced a $100 billion investment in OpenAI, a startup valued at $500 billion. The capital will help OpenAI deploy at least 10 gigawatts of Nvidia systems, which is roughly equivalent to the annual power consumption of 8 million U.S. households.

Shares of Advanced Micro Devices have doubled this year and soared more than 20% earlier this month after the chipmaker announced a deal with OpenAI, while Oracle has been on a tear of late due to its ties to OpenAI and the broader infrastructure buildouts.

“Are we sort of inflating the economy now, thereby setting ourselves up for a crash in the future?” Sundararajan said. He added that he’s not seeing signs that demand for AI infrastructure will slow anytime soon.

‘Tariff price management’

When it comes to local businesses, most only know about the AI gold rush from the news headlines. One in four small business owners are stuck in “survival mode” as they contend with challenges like rising costs and tariffs, according to a September KeyBank Survey. It’s a segment of the economy that routinely accounts for about 40% of the nation’s GDP.

Pappas’ flower shop was founded in 1921, and purchased by his dad in 2002. The business has survived the Great Depression, World War II and the Covid pandemic. Pappas said his father, who died in 2022, reminded him that these periods were “just another season” for Norton’s, and that such challenges come with the territory.

But Trump’s tariffs have created a whole new set of constraints, as roughly 80% of all cut flowers in the U.S. are imported from countries like Colombia and Ecuador, according to the U.S. Department of Agriculture.

There’s no way for Norton’s to avoid higher import costs, but Pappas said he’s started buying some flowers directly from South American growers, which saves him money versus going through distributors that charge extra.

Pappas said it’s part of his “tariff price management” effort.

Trump’s tariffs will cost global businesses more than $1.2 trillion this year, and most of those costs are being passed onto consumers, according to S&P Global.

With the holiday season rapidly approaching, consumer sentiment is of particular importance. The picture is bleak.

The majority of U.S. consumers, 57%, that responded to a Deloitte survey published this month said they expect the economy to weaken in the year ahead, up from 30% a year ago. It’s the most negative outlook since the consulting firm began tracking sentiment in 1997.

Gen Z consumers, which the survey defined as ages 18 to 28, said they plan to spend an average of 34% less this holiday season compared to last year. Millennials, those between 29 and 44, said they expect to spend an average of 13% less this holiday season.

Additionally, seasonal hiring in the retail industry is poised to fall to its lowest level since the 2009 recession, according to a September report from job placement firm Challenger, Gray & Christmas.

The firm released another report earlier this month that showed new hiring in the U.S. has totaled just under 205,000 so far this year, off 58% from the same period last year.

The Starbucks logo is displayed in the window of a Starbucks Coffee shop on Sept. 25, 2025 in San Francisco, California.

Justin Sullivan | Getty Images

Starbucks announced a $1 billion restructuring plan in September that involves closing several stores in North America. Around 900 nonretail employees were laid off as part of the plan, and the company let go of another 1,100 corporate workers earlier this year.

Starbucks shares are down about 6% this year.

Shares of Wyndham Hotels & Resorts slumped on Thursday after the hotel chain issued disappointing third-quarter results. CEO Geoff Ballotti cited a “challenging macro backdrop” in the company’s earnings release. The stock is down roughly 25% year to date.

Even in parts of the tech industry that have benefited the most from the AI boom, companies have been conducting layoffs. Microsoft announced plans to cut around 9,000 jobs in July, which the company partly attributed to reducing layers of management. Salesforce is one of a number of tech companies that have announced layoffs, saying that AI can now handle the work.

But Hatim Rahman, an associate professor specializing in AI at Northwestern University’s Kellogg School of Management, said that most businesses using AI for efficiencies won’t find them right away. So companies can’t count on the technology to counter declining revenue and, Rahman said, “the road to the future is going to be bumpy.”

“AI is not a plug-and-play solution,” Rahman said. “For many organizations, it’s going to involve engagement with people, processes, culture, tools to be able to reap the benefits. And in the aggregate, it’s going to take time.”

WATCH: The AI boom is lifting the stock market, but it may be masking a weaker economy

The AI boom is lifting the stock market, but it may be masking a weaker economy

The AI boom is lifting the stock market, but it may be masking a weaker economyContinue Reading