Kiss founding member Ace Frehley, the rock band’s original lead guitarist, has died aged 74.

He passed away peacefully, surrounded by his family, in Morristown, New Jersey, his agent said.

He had suffered a recent fall.

A statement…

Kiss founding member Ace Frehley, the rock band’s original lead guitarist, has died aged 74.

He passed away peacefully, surrounded by his family, in Morristown, New Jersey, his agent said.

He had suffered a recent fall.

A statement…

You don’t have permission to access “http://www.undp.org/press-releases/new-global-multidimensional-poverty-index-report-reveals-nearly-80-worlds-poor-live-regions-exposed-climate-hazards” on this server.

Reference…

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Venture Global is seeking to quell accusations from major energy clients that it plans to sell liquefied natural gas cargoes on spot markets rather than honouring supply contracts from its new export terminal in Louisiana.

The US LNG supplier wrote to clients on Thursday affirming its commitment to deliver on contractual obligations, after selling more than 100 cargoes from its Plaquemines facility before having declared it operational. Such a declaration triggers legal obligations to begin delivering on contracts.

The customers are fearing a repeat of Venture Global’s conduct when it launched its first facility, Calcasieu Pass, from which it sold more than 400 cargoes on spot markets before fulfilling deliveries to customers. The move has led to growing legal and financial pressure on the group after an international arbitration panel ruled last week that the company breached its obligations.

In a filing to US regulators last month, Venture Global requested a delay of its in-service date for Plaquemines by several months to the end of 2027, raising concerns among customers that the company could delay supplying cargoes to them as it did at its Calcasieu Pass facility.

In that case, the company declared force majeure on its contractual commitments in March 2023 on the grounds that the Calcasieu Pass facility’s power supply equipment needed repair, even though it was able to supply cargoes to the spot market amid a price surge following Russia’s invasion of Ukraine.

Spot markets are again priced far higher than long-term supply contracts would fetch.

Saul Kavonic, head of energy research at MST Marquee, said: “Venture Global stands to make over double the revenue by selling cargoes on the spot market compared to selling under their long-term contracts.”

The clients are so-called foundational customers, whose long-term contracts enable Venture Global to raise the money to build its LNG terminals.

Last week the International Chamber of Commerce found Venture Global breached its obligations to BP by failing to deliver cargoes from Calcasieu Pass. It now faces damages claims worth more than $1bn from the UK oil major, as well as four additional arbitration cases filed by customers that could lead to similar judgments.

Rating agency Fitch on Thursday revised its outlook on the company to “negative”, from “stable”, saying “any significant damages are likely to further pressure the company’s financial position in a period of elevated leverage”.

Venture Global’s request for an extension of its in-service date for Plaquemines, which the Federal Energy Regulatory Commission approved on Thursday, prompted two customers, Chevron and Orlen, a Poland-based energy company, to ask the regulators to intervene in the case.

Orlen, which is one of Plaquemines largest customers with a contract to buy 4mn tonnes of LNG a year, said it had “concerns regarding the intentions of Plaquemines parent company” in its submission to US energy regulators.

Shell, also a foundation customer, told the Financial Times it was “closely monitoring activities at the Plaquemines facility to ensure adherence to our contracted commercial operation date”.

When contacted for comment about its letter to customers, Venture Global said its recent filing to US regulators requesting a delay of its in-service date for Plaquemines to the end of 2027 would not change the date it would begin shipping cargos to long-term customers.

“Our request for an extension is a case of aligning our permits with our actual construction schedule,” it said. “To be clear, this request will have no impact on our expected commercial operations date, which remains unchanged from what has been communicated and agreed upon with our customers.”

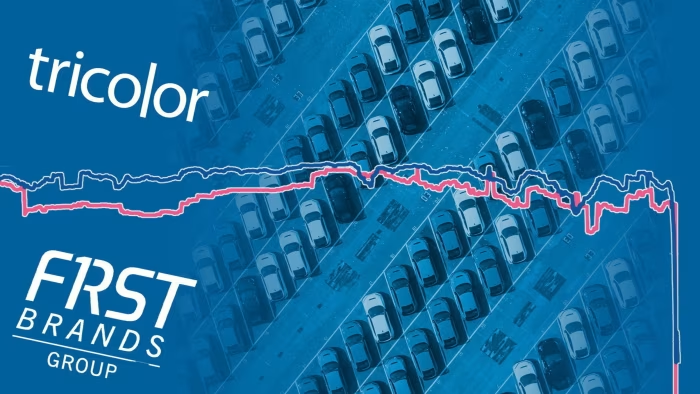

Investors in the $2tn leveraged loan market have warned that the abrupt collapse of First Brands Group is an early sign of trouble for a market where hasty deals and hurried due diligence have become commonplace.

First Brands was among the largest issuers of loans bought by collateralised loan obligations, investment vehicles that buy up small slices of hundreds of individual corporate loans.

CLOs have become popular with insurers and other big investors who bet that by spreading their lending across many different companies they are protected from the pain of defaults in one or two businesses.

But the rapid bankruptcy of First Brands, a maker of antifreeze, windshield wipers and brake pads, has raised concerns over the rapid growth of the CLO market, which has provided almost unquenchable demand for the leveraged loans that private equity firms often use to finance their acquisition sprees. Some fund managers worry that a spate of CLO losses could cause Wall Street’s securitisation machine to sputter.

“Inside credit markets for more than a year, there has been a grudging recognition that there was and is a series of credit problems that could be substantial and could be dangerous to the overall economy,” said Andrew Milgram, chief investment officer of Marblegate Asset Management, a distressed-debt investor.

First Brands’ downfall, just weeks after subprime auto lender Tricolor filed for bankruptcy amid allegations of fraud, has stoked concerns that the failures are unlikely to be isolated incidents.

“You’re not paid to do due diligence in this market,” an executive at a former lender to First Brands said.

First Brands had issued more than $5bn of senior and junior loans, which were bought up and held in dozens of CLOs issued by asset managers including PGIM, Franklin Templeton, Blackstone, CIFC, Oaktree and Wellington, according to a Morgan Stanley analysis.

Most of those vehicles have already realised their losses, selling out of the loans as First Brands’ problems came to light over the past two weeks. The loans are now changing hands at just cents on the dollar, with an implied loss of more than $4bn.

Those losses will principally hit the returns of CLO equity holders, which includes the managers of the structured credit vehicles themselves. CLOs are often 10 times leveraged, with $50mn of equity supporting a $500mn loan portfolio, for example. Defaults such as First Brands’ cut into that equity cushion, which exists to take the first loss and protect higher-rated investment grade tranches of the CLO.

Trading of those equity tranches is opaque, but investors said they had not yet seen money managers dumping those positions in secondary trades.

The sell-off in First Brands debt has started to weigh on the broader market, with PitchBook LCD data showing the US leveraged loan market is on pace for its biggest monthly loss since 2022.

“The two successive defaults of [First Brands] and Tricolor Auto brought into highlight potential irregularities and underwriting challenges in the credit market,” Bank of America strategist Pratik Gupta said. “The market has started to take a dim view of credit fundamentals.”

Despite the troubles at First Brands and Tricolor and pockets of weakness starting to appear in the US economy, the strong demand for higher-yielding investments such as leveraged loans has kept spreads on risky corporate debt at near-record low levels.

Leveraged loan issuance hit a record in the third quarter at $404bn, according to PitchBook LCD. However, investors say this feverish pace of issuance has meant deals — which a few years ago may have taken weeks or more to line up — are now often raced through.

When First Brands raised more than $750mn in March 2024 to fund an acquisition, it announced it was in the market for the debt financing on a Monday morning. Investors were allocated the loans before lunch on Friday of the same week. In total, more than 80 CLOs were exposed to First Brands, bankruptcy filings showed.

Demand has persisted despite some of the worst investor protections on record, according to Covenant Review. Lawyers for the industry say they have little power to push back against weak protections when willing buyers are so numerous.

First Brands debt offered attractive rates, with an interest rate 5 percentage points over the floating rate benchmark for the US dollar loans it issued in March 2024. When accounting for discounts investors received at the time of the capital raise, the loans yielded roughly 11 per cent.

Investors who have suffered losses on the loans say due diligence was not made a priority, with some investors taking comfort from the fact that larger managers with bigger teams of credit analysts had bought in.

But others saw red flags they said steered them away from the debt. The company was perpetually buying up smaller businesses and raising more debt to fund those takeovers. Investors said that made it difficult to assess how the underlying business was faring. Others pointed to the difference between the cash flows that First Brands generated and the profits it reported it was earning.

“Everything was adjusted,” one investor who decided against investing in First Brands debt said, referring to its profit statement. “Nothing tied to cash so it was virtually impossible” to analyse.

Josh Easterly, the chief investment officer of investment group Sixth Street, pointed to the fact that many CLO investment firms have just a handful of analysts covering their entire credit portfolios, which can include hundreds of different investments. Moody’s estimates roughly 2,000 companies issue debt that is bought by CLOs in the US.

“When the tide goes out . . . things are going to come out,” Easterly said, noting that investors would see “who has done their work and who hasn’t.”

While defaults in the leveraged loan market have picked up this year from 2024, the pace remains low by historical standards, according to PitchBook LCD data. But concerns about the lack of due diligence in a frothy market are starting to mount.

“With [Tricolor] and First Brands, the problems of the credit market are starting to percolate into the general Wall Street psyche,” Milgram said. “Are we entering a period where those [CLO market’s] assumptions will be tested?”

The top-rated AAA tranches in CLOs have proven their mettle during prior market sell-offs and economic downturns, given how diversified the vehicles are. Investors said defaults would need to rise dramatically to begin to impair investors in even the lower-rated portions of the vehicles.

Money managers are nonetheless keenly aware of the problem that First Brands might cause the broader market.

Asset manager Silver Point this month began the marketing of its first euro CLO by highlighting one point in investor materials seen by the FT.

It said: “Silver Point has zero First Brands exposure.”

Additional reporting by Robert Smith

My personal style signifier is sports- and swimwear – particularly my Youswim two-piece sets. I live in them; I have them in every single colour. It’s like Hunza G [in crinkle-stretch fabric] but I find the Youswim ones more elasticated….

Unlock the White House Watch newsletter for free

Your guide to what Trump’s second term means for Washington, business and the world

Saudi Arabia is discussing a defence deal with the Trump administration similar to a US-Qatar pact last month…

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is a managing partner and head of research at Axiom Alternative Investments

The AT1 bond market does not have many friends. When Swiss authorities controversially wiped out $17bn of the Additional Tier 1 bonds issued by Credit Suisse, many claimed that the market was dead. As the argument went: “Surely no one would be foolish enough to read the terms and conditions and still buy bonds that can be worth zero overnight?”

Lots of people were, it turned out: since lows hit in the wake of the failure of Credit Suisse, a Bloomberg index of the price of the bonds is up 50 per cent. And 2024 still saw a near 60 per cent increase in issuance to €46bn, according to Barclays. This year issuance has reached €34bn.

AT1s were introduced as a form of supplementary bank capital, designed to be wiped out in a crisis to cover losses. They are crucial to reduce banks cost of equity and increase their capacity to lend. The issue with the Credit Suisse AT1s is whether the bonds were wiped out fairly. The Swiss Federal Court ruled on Tuesday that the treatment of the bonds was unlawful — a decision my investment firm supports as we own some bonds affected and are taking separate legal action. Now we are hearing a similar argument to the one made at the time of the Credit Suisse failure, only in reverse: if you cannot wipe out AT1 capital when an entity is a “gone concern”, the asset class is dead.

But the circumstances of the Credit Suisse saga are idiosyncratic. To simplify, Swiss regulator Finma argued that it had basically three grounds to wipe out the bonds: two contractual grounds based on the terms of the bonds, and one general legal right, as an authority overseeing the bank’s resolution. The court dismissed the contractual grounds with a reasoning that is strictly limited to the specifics of this case. The terms and conditions allowed the wipeout in two situations: i) a notification by Finma of the non-viability of the bank and request by it for the wipeout of both AT1 and Tier 2 bonds or ii) necessary state aid improving the capital of the bank. On the first point, the court noted that Finma issued no such notification and, incomprehensibly, did not wipe out Tier 2 bonds. It could have done so. On the second point, the court says that Credit Suisse only received liquidity, and liquidity does not improve capital.

The last nail in the coffin? Finma argued that, as AT1 eligible bonds, the terms were maybe unclear but should have allowed the wipeout. The court answered that Finma should not have authorised the bonds if they did not meet AT1 requirements.

The discussion on the “general legal right” is also very intriguing. There were many ways for the Swiss authorities to zero the bonds. Swiss banking law gives huge discretion to Finma as a resolution authority and the court points that it explicitly refused to declare a resolution event and wipe out the bonds, presumably to protect the shareholders who received $3.2bn from UBS in the takeover of Credit Suisse and would have been left with nothing in a resolution. Under the Swiss constitution, an infringement on property rights requires a law and emergency ordinances can only be used as a substitute if no law is readily available.

None of this has direct implications for the rest of Europe. European authorities have already proved that swift and strict application of resolution laws can be done with little litigation risk. Sberbank Europe was wound down in 2022 and even the fall of Banco Popular in 2017 did not leave many pathways for AT1 bondholders to pursue redress in court.

Where does this leave UBS? Our firm has an interest in the outcome as we own UBS bonds but hold short positions on the stock. It’s the big unknown, and the Swiss court was very careful to point out that it was not answering that question — yet. This is why it calls its own decision “partial”. But the full text of the ruling hints at three possibilities.

Ruling that the ordinance wiping out the bonds is null could simply mean that the bonds are reinstated and reintroduced in UBS’s balance sheet. Whether UBS could receive indemnification from the Swiss government, in the middle of the current tense discussion on massive new capital requirements for the bank is another story. But the court could also rule that the AT1s remain void and that its decision only opens the right to seek indemnification from Finma or from the now combined Credit Suisse-UBS.

Who pays what in that scenario remains highly speculative — not to mention that this complex decision is not final and Finma will appealed against it. The Credit Suisse AT1 saga is far from over.

Eighty years since the first of a beloved fleet of trains was introduced to the world, a national blue plaque is being unveiled at the redbrick house in Gloucestershire where the Rev W Awdry worked on his railway stories.

Train stations in city centres are urban areas often associated with dirt and pollution. However, in the heart of Melbourne, a railway station is quietly cleaning the air around it. The Arden Station façade actively fights pollution, kills…