Beverly Hills, CA, Oct. 20, 2025 (GLOBE NEWSWIRE) — ThrIVe Health is proud to announce a comprehensive Thyroid Eye Disease (TED) Patient Support & Educational Seminar scheduled for Saturday, November 1st, 2025, from 11:00 AM to 12:30 PM at…

Blog

-

Apple Reimagines the Blank Page in ‘Great Ideas Start on a Mac’

Apple has unveiled a new global brand platform for Mac that celebrates the power of possibility — and the idea that every great creation begins with a blank page. The campaign is a tribute to inspiration, curiosity, and the Mac as the tool…

Continue Reading

-

How to Watch the 2025 Hanwha LIFEPLUS International Crown – LPGA

- How to Watch the 2025 Hanwha LIFEPLUS International Crown LPGA

- How Does the International Crown 2025 Work? Format, Teams & Other Details Explained EssentiallySports

- Who is playing in the Hanwha LIFEPLUS International Crown 2025? Full Field…

Continue Reading

-

Players who signed rookie extensions before 2025-26 deadline

OKC made sure to lock up young stars Chet Holmgren (left) and Jalen Williams in the offseason.

For players drafted in the 2022 NBA Draft, the deadline to sign rookie-scale contract extensions is 6 p.m. ET on Oct. 20.

Here’s a quick look at the…

Continue Reading

-

Health Minister reviews ongoing Human Papillomavirus (HPV) vaccination campaign

– Advertisement –

– Advertisement –

– Advertisement –

KARACHI, Oct 20 (APP): Sindh Minister for Health and Population Welfare, Dr. Azra Fazal Pechuho on Monday chaired a high-level meeting on the ongoing Human Papillomavirus (HPV) vaccination…

Continue Reading

-

Just a moment…

Just a moment… This request seems a bit unusual, so we need to confirm that you’re human. Please press and hold the button until it turns completely green. Thank you for your cooperation!

Continue Reading

-

A high dose of uncertainty: Navigating pharmaceutical tariffs

The information contained in this post is believed to be reliable as of October 20, 2025.

Because of sourcing, production environment, and transportation sensitivities, tariff uncertainties can present complex financial and operational challenges to pharmaceutical companies. Reported tariffs of 100% on brand-name or patented pharmaceutical products imported into the United States have been paused pending ongoing negotiations to secure pricing agreements. While details are unclear, any policy shift could disrupt the global pharmaceutical supply chain, which has historically prioritized efficiency and accessibility.

The stated aim of the new tariff is to bring pharmaceutical prices down through encouraging domestic production. However, unintended consequences may include rising costs, increased complexity, and heightened regulatory risks for pharmaceutical companies and others involved in the testing, manufacturing, packaging, and distribution of products.

Overview of recent changes to global pharmaceutical trade

Historically, countries including the US, the UK, the EU, Canada, and China have adhered to the World Trade Organization’s (WTO’s) Pharma Agreement, which imposes no tariffs on pharmaceutical products to promote the affordability and accessibility of medicines.

However, in April 2025, the US implemented a 10% global tariff on nearly all imported goods, impacting pharmaceutical and healthcare sectors by increasing costs for critical inputs such as active pharmaceutical ingredients (APIs), specialized reagents, manufacturing equipment, and medical devices. Concurrently, a Section 232 investigation was launched to assess whether pharmaceutical imports and their ingredients pose a national security risk, especially as the US imports APIs from producers in China and India.

Affected medications may include widely used asthma treatments, cancer therapies, and weight loss drugs, as well as select vaccines. Pharmaceutical products from the EU and Japan are believed to be limited to 15% tariffs given their specific trade agreements, which is still significant but much lower than the proposed global 100%.

A potential sign of ongoing deal-making is the launch of TrumpRx, a direct-to-consumer website offering drugs at government-negotiated prices. Pfizer was the first pharmaceutical company to participate, reducing drug costs and committing US$70 billion to US manufacturing, in exchange for a three-year tariff waiver on its products. A deal with a British-based drugmaker will also see it sell some medicines at a discounted price in exchange for tariff relief. However, the impact of all these developments on pricing for future drug releases, both overseas and in the US, remains uncertain.

Adding to a complex landscape, another Section 232 investigation was launched in September 2025 to assess the national security implications of imports of personal protective equipment (PPE), medical consumables, and medical devices. Given that 75% of US medical devices are manufactured abroad — primarily China, Mexico, and Canada — further tariffs risk increasing costs and causing shortages of critical equipment. Additionally, tariffs on steel and aluminum could disrupt the production of hospital tools and equipment, further straining supply chains.

Tariffs’ side effects on pharmaceutical supply chains

Tariffs have created a more complex, restrictive, unpredictable, and evolving trade environment for pharmaceutical organizations operating globally. Like many other industries, the stability and security of trade and supply chains for pharmaceuticals are increasingly being challenged.

Generally, trade disruptions can raise the risk of supply interruptions, manufacturing delays, and cost volatility. For the pharmaceutical sector, the effects can potentially extend beyond operational inefficiencies, potentially delaying patient access to critical medicines. In the longer term, while tariffs may incentivize local investment, they also risk hindering innovation and research, as companies might reduce their research efforts and budgets to offset any additional expenses.

Even before the tariff announcements, US imports of pharmaceutical products surged in the first quarter of 2025. As companies anticipated tariffs, there was a 70% increase in medicine imports and a 493% increase in basic pharmaceutical product imports.

However, several large manufacturers have said that their future exposure to tariffs may be limited. Many are already manufacturing drugs or constructing facilities in the US over the coming years, thereby qualifying for tariff exemptions. This includes European companies GlaxoSmithKline and Roche, who signalled their intent to expand US research and production. Nonetheless, given that global pharmaceutical companies operate across multiple countries, the additional tariffs could disrupt various parts of their complex supply chains.

Four prescriptions to strategically mitigate pharmaceutical tariff risks

Given the growing complexity of tariff impacts, pharmaceutical developers and manufacturers should evaluate their operations with the aim of protecting continuity, controlling costs, and maintaining patient access.

To more effectively navigate the challenges posed by pharmaceutical tariffs, businesses should consider:

- Implementing cost-reduction strategies: Tariffs may increase drug development costs both directly, such as raising the cost of inputs, as well as indirectly by adding hidden costs such as higher customs fees, increased administrative burdens, and more complex import logistics. Conducting comprehensive reviews of your operations can help identify where costs can be reduced. Actions could include optimizing production processes, shifting toward domestically focused supply models, or investing in US-based manufacturing capabilities to reduce reliance on international suppliers. Bear in mind that any trade-offs could affect sustainability initiatives, product quality, skills availability, supplier concentration risks, and overall sourcing strategies.

- Diversifying supply chains: For some products, where specific raw materials, components, and technologies may have only a limited number of global sources, geographic concentration can create critical vulnerabilities. Reducing reliance on specific countries or suppliers subject to higher tariffs can help mitigate risks associated with geopolitical tensions and supply chain disruptions. Diversifying your supply chains may include adopting a multi-region supply strategy, partnering with suppliers in different geographies, and nearshoring or reshoring production to reduce dependence on single sources or regions.

- Assessing risks: Given the unpredictability of global trade policy, tariff-related disruptions could be considered as part of a trend of persistent disruption. For pharmaceutical companies, operational risks are particularly acute due to their supply chain complexity, often limited sourcing flexibility, specialized handling needs, long processes, and regulatory requirements. With the help of our specialists and using insights from Marsh McLennan’s Sentrisk supply chain visibility platform, pharmaceutical companies can analyze their exposure to tariff impacts and identify critical vulnerabilities. Furthermore, scenario modeling with our Tariff Simulator enables companies to quantify potential impacts on inventory, lead times, and production schedules, facilitating better-informed decision-making.

- Implementing risk management solutions: Pursuing insurance solutions — for example, ones that include coverage for forms of business interruption risk resulting from physical loss or damage — can potentially mitigate the associated impacts of trade- and tariff-related risks. Using a risk management framework can also help organizations better anticipate, prepare for, and respond to changes.

Immunizing your business

Tariffs pose a complex and evolving challenge for the pharmaceutical and healthcare industries, with significant potential implications for costs, supply chains, and patient health. Successfully navigating this landscape requires strategic foresight, collaboration, and resilience.

Marsh is ready to support pharmaceutical companies in understanding and mitigating tariff risks through advanced analytics, specialized risk advisory, and tailored insurance solutions. By understanding the risks and implementing proactive mitigation strategies, stakeholders can better help safeguard the integrity and safety of healthcare in an uncertain global environment.

Continue Reading

-

Cut carbon with SIG Terra: download LCA summary

Cut carbon. Not performance.

No aluminium. Full product safety and shelf life. Get the data behind SIG Terra Alu-free + Full barrier.

Highlights from the independent lifecycle assessment:

• Up to 61% lower carbon footprint compared to standard…

Continue Reading

-

Brazil Begins Planting with Expected Record Acreage Driven by High Demand but Low Margins

Farmers across Brazil have begun planting the 2025/26 crop season, with expectations for another record in corn and soybean acreage. The first outlook for the new cycle, released by the National Supply Company (Conab), Brazil’s food supply and statistics agency, projects an increase in planted area. The expansion is driven by growing domestic demand for biofuels and strong export performance, which continues to push shipments to record levels. Despite the expected acreage growth, gross margins for both crops are likely to decline significantly due to rising production costs and lower prices. This article reviews the first official Brazilian government estimates for soybeans and corn, analyzes financial trends, and explores their implications for the global soybean and corn trade.

Soybean Acreage Expected to Hit Historical Highs

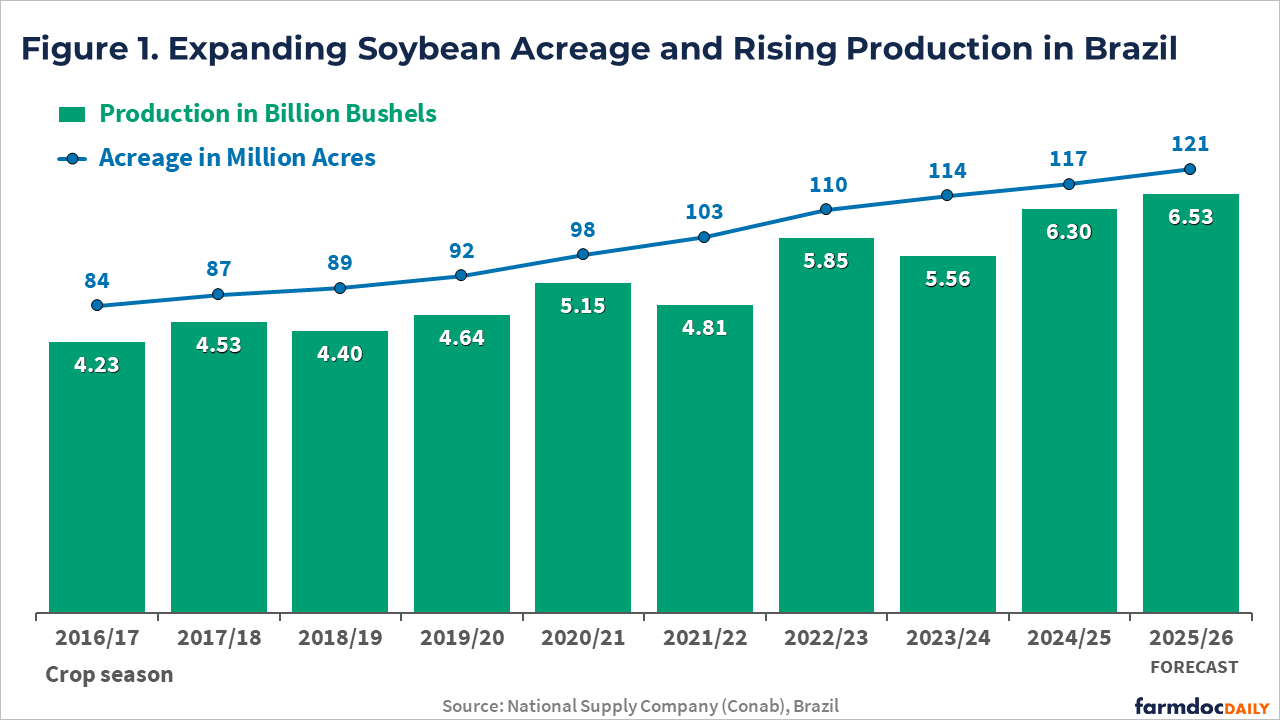

In its preliminary estimate released on October 14, Conab projected that Brazil’s soybean acreage will increase by 3.5%, reaching 121 million acres – the largest area on record. For comparison, U.S. farmers planted 81 million acres of soybeans in the current crop season. If weather conditions cooperate, Brazilian production is expected to reach a new record of 6.5 billion bushels, up 3.6% from last season (see Figure 1). As of October 11, approximately 11% of the soybean area had been planted, below the five-year average of 17%, according to Conab.

The expansion in soybean acreage is being driven by strong domestic and international demand. On the domestic side, growth is supported by Brazil’s biodiesel mandate, with soybean oil being the main raw ingredient. As of August 1, 2025, the country raised its required biodiesel blend from B14 to B15. Basically, diesel fuel must now contain 15% biodiesel, up from 14%, which represents about a 7% increase in total biodiesel use, given Brazil’s large diesel market. The change is part of the government’s Fuel of the Future program, aimed at boosting domestic biofuel production, creating jobs, and reducing dependence on imported fossil fuels.

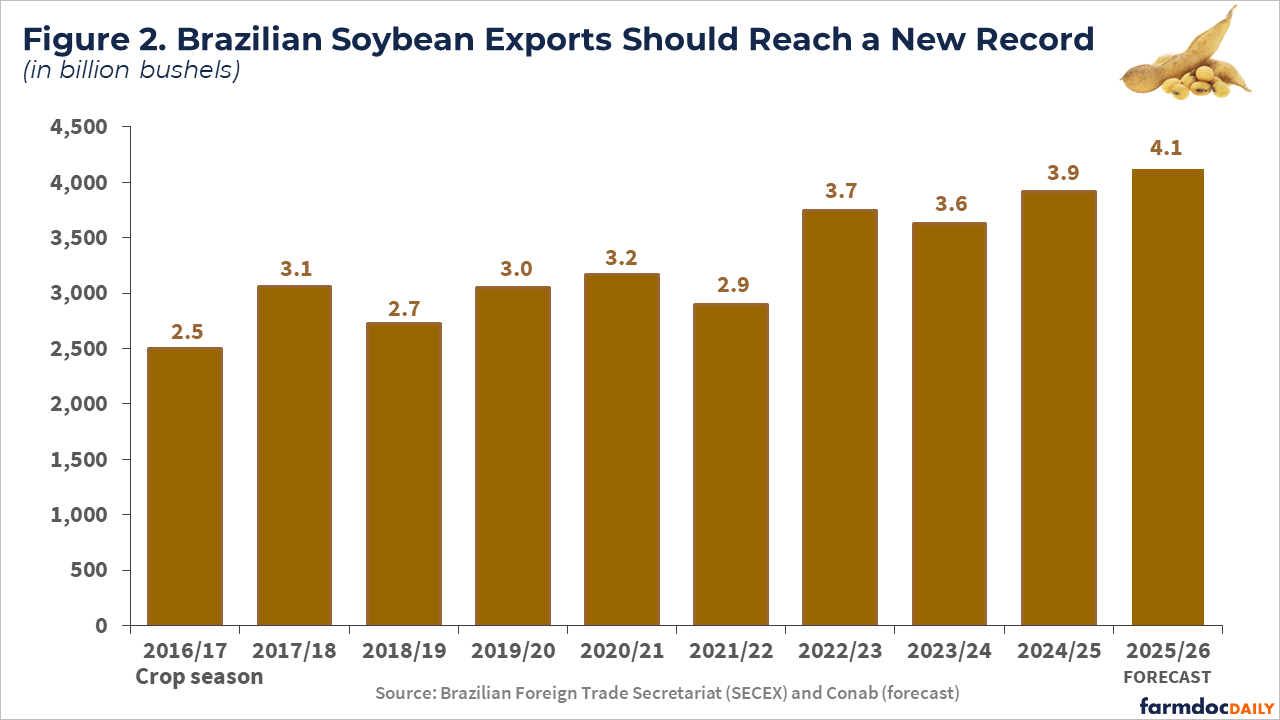

On the international side, demand remains strong, particularly from China. From January through September this year, Brazil exported 3.45 billion bushels of soybeans, with 77% of that volume shipped to China, according to the Foreign Trade Secretariat (Secex/Brazil). The total is 5% higher than in the same period last year. Brazil is projected to reach a record 3.9 billion bushels in soybean exports by the end of 2025, with shipments expected to surpass 4 billion bushels next year (see Figure 2).

A significant share of Brazil’s export growth to China reflects the gap left by the United States, as Chinese buyers have largely suspended purchases of U.S. soybeans since May following the imposition of U.S. tariffs. Historically, China has been the top buyer of U.S. soybeans by a large margin. In 2024, the United States shipped nearly 985 million bushels to China, accounting for 51% of the nation’s total soybean exports that year (Colussi & Langemeier, 2025). China’s current share of Brazil’s soybean exports is historically high – comparable only to 2018, when President Trump launched the first trade war with China (see farmdoc daily, May 15, 2025).

Despite the optimistic outlook for exports, Brazilian farmers are planting a soybean crop that is expected to be financially challenging, with 4% higher production costs and lower international prices. Projections from the Center for Advanced Studies on Applied Economics (Cepea) at the University of São Paulo (USP) indicate a decline in producers’ gross margins for the upcoming season. Compared with last year, average gross margins (gross revenue minus direct production costs) are estimated to fall from $165 per acre to $105 per acre. However, when interest rates, land rent, and depreciation are considered, margins are projected to turn negative (i.e., -$90 per acre).

Corn Acreage to Expand Despite Lower Output

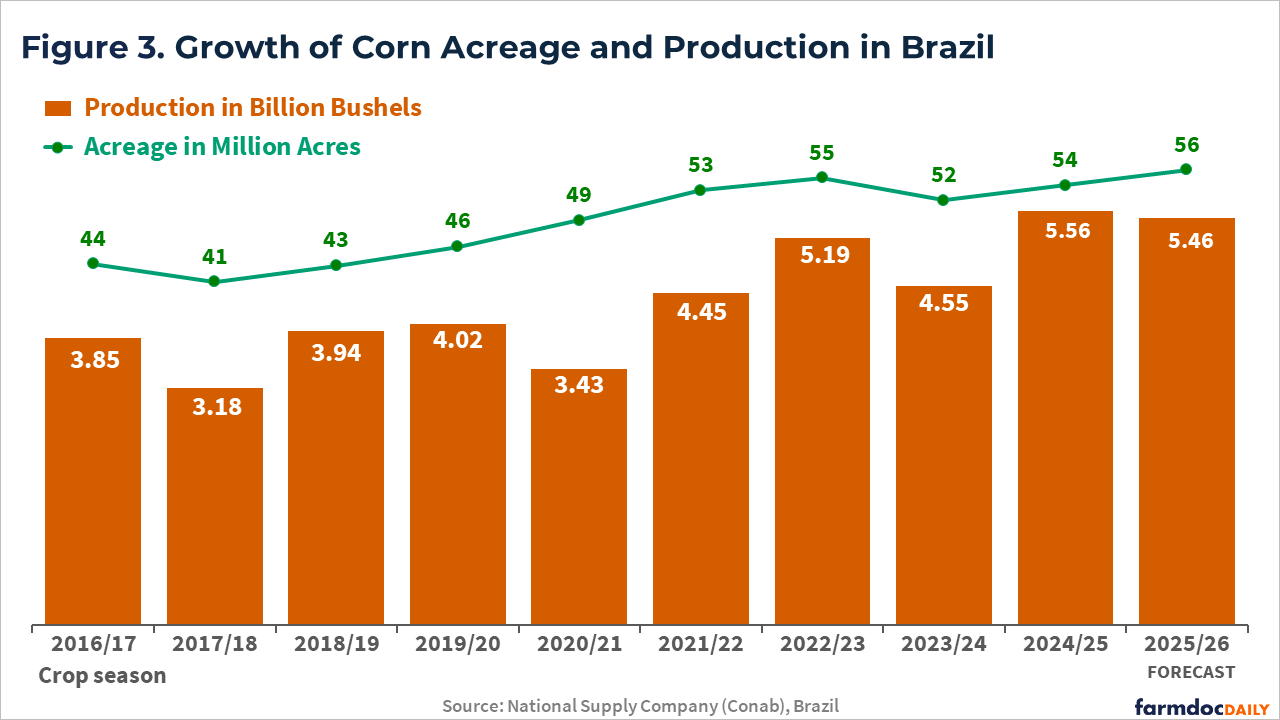

Like soybeans, Brazilian corn acreage is also expected to expand by 4% in the 2025/26 season, reaching 56 million acres, according to Conab’s initial estimates. For comparison, U.S. farmers planted 99 million acres this season. Brazil’s total corn production is projected at 5.46 billion bushels across the country’s three crop cycles – 2% lower than last year and roughly one-third of total U.S. production (see Figure 3). The projected decline reflects an expected reduction in yields, following last season’s record-high production and productivity.

The first corn crop – planted beginning in September across southern Brazil and some irrigated areas of the Southeast – is expected to expand by 6% compared with last year. The second crop, planted right after the soybean harvest in January and February across the Center-West region and now accounting for nearly 80% of Brazil’s total corn production, is projected to see a 4% increase in acreage from last season. The expansion is driven mainly by rising domestic corn consumption, which Conab projects will grow from 3.58 billion bushels to 3.74 billion bushels – supported by stronger demand from the livestock feed and corn ethanol industries. Historically known for its sugarcane-based ethanol, Brazil has been rapidly expanding corn-based ethanol production, which today represents about 20% of the country’s total biofuel output (see farmdoc daily, April 14, 2025).

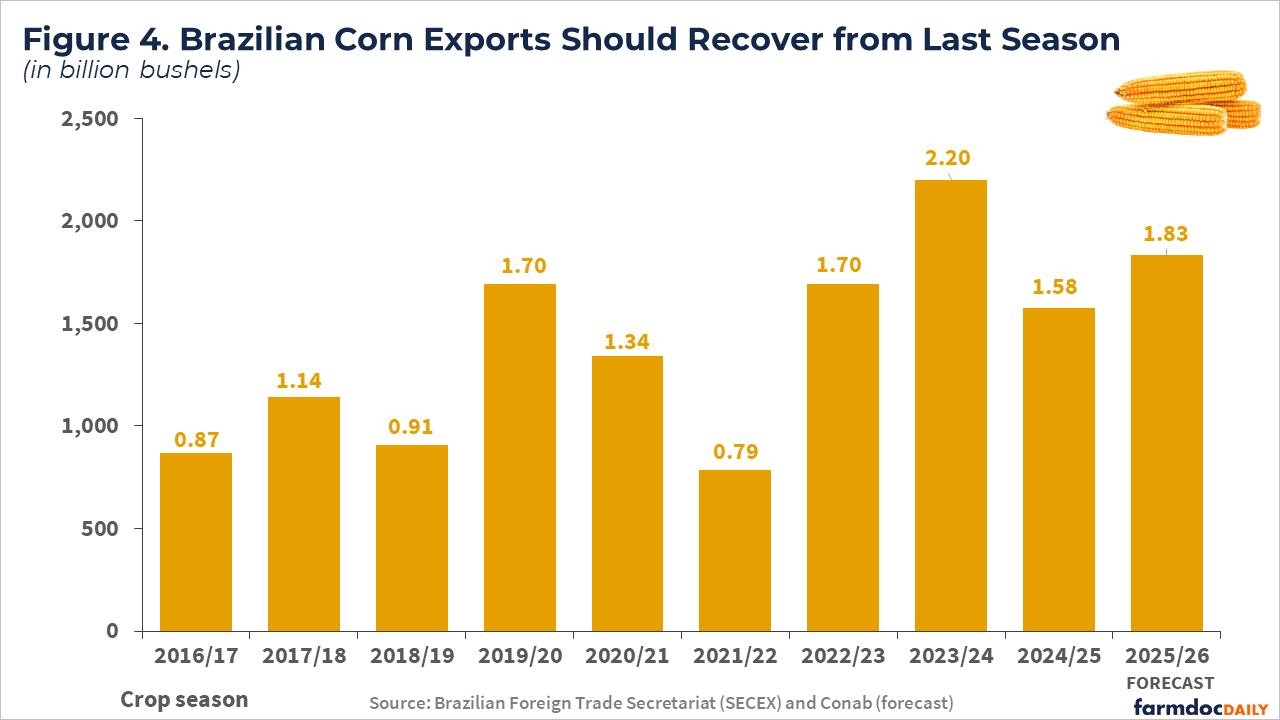

In addition to stronger domestic demand, corn production is also expected to benefit from higher export projections for next year. While exports for the 2024/25 season are estimated at 1.58 billion bushels, the Brazilian government forecasts shipments of 1.83 billion bushels for the upcoming season – a 16% increase compared with the previous year, though still below the record set in 2022 when China opened its market to Brazilian corn (see Figure 4).

In terms of production costs, Brazilian corn farmers are expected to see a 6% decrease in the next season, according to data from Cepea/USP. Even so, the projected gross margin (gross revenue minus direct production costs) is expected to fall from $75 per acre in the last crop season to just $6 per acre in the 2025/26 cycle. When other expenses, such as land rent and interest, are included, profits turn into losses, estimated at $135 per acre. The projected reduction is based mainly on the historical average yield of 90 bushels per acre, compared with 109 bushels per acre in last season’s record crop.

Final Considerations

Brazil is beginning its summer crop season with expectations of record planted area for both soybeans and corn, driven primarily by rising domestic demand for biofuels and favorable conditions in international markets. In the case of soybeans, higher exports to China – following the suspension of Chinese purchases of U.S. soybeans – have kept prices firm in Brazil, even after a record harvest. For corn, which also reached record output last season, the expansion in planted area is largely supported by the rapid growth of the corn ethanol industry in the Center-West states, a new and quickly expanding sector in Brazil.

However, shrinking profit margins and higher financial costs could slow the pace of expansion ahead. While Brazil’s farmers continue to gain ground in global markets, their profitability is being squeezed by rising input costs, lower commodity prices, and high interest rates – a scenario similar to that faced by U.S. agriculture (see Langemeier et al., 2025), though with some regional differences. If margins remain tight, Brazilian future production growth should rely more on efficiency gains – such as higher yields and investments in logistics and storage – than on further area expansion.

Data and References

Colussi, J., M. Langemeier. “U.S. Soybean Harvest Starts with No Sign of Chinese Buying as Brazil Sets Export Record.” Center for Commercial Agriculture, Purdue University, September 22, 2025.

Colussi, J., J. Coppess, N. Paulson and G. Schnitkey. “Trade Conflicts and Long-Term Consequences: Are Soybeans Doomed to Repeat History?” farmdoc daily (15):90, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, May 15, 2025.

Colussi, J., G. Schnitkey and N. Paulson. “Ethanol Boom Drives Sharp Rise in Brazil’s Corn Consumption.” farmdoc daily (15):69, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, April 14, 2025.

Conab, National Supply Company. Crops Time Series. Soybean and Corn Production. Brasília, Brasil. October 2025.

Langemeier, M., M. Boehlje, and J. Colussi. “Financial Stress on Crop Farms: Who Is Most at Risk in the 2024–26 Downturn?” Center for Commercial Agriculture, Purdue University, September 3, 2024.

Secex, Brazilian Secretariat of Foreign Trade. Brazil’s Ministry of Development, Industry, and Trade. Exports Report. October 2025. http://comexstat.mdic.gov.br/en/geral

Continue Reading

-

Timberwolves Run It Back with Prince-Inspired Nike City Edition Uniforms in Partnership with Prince’s Paisley Park Enterprises – NBA

- Timberwolves Run It Back with Prince-Inspired Nike City Edition Uniforms in Partnership with Prince’s Paisley Park Enterprises NBA

- Timberwolves announce return of Prince uniforms, new court to match Sports Illustrated

- Timberwolves unveil…

Continue Reading