Gold prices rallied hard amid the chaos of the reciprocal tariff roll-out in early April. Once that episode was over, they went into a holding pattern and stayed there until Chair Powell’s dovish speech at Jackson Hole on August 22, which unleashed a true frenzy of precious metals buying. The IMF/WB annual meetings burst that bubble and precious metals prices have gone back into the same holding pattern they went into once the April tariff shock had worn off. However, my sense is that the underlying drivers of the “debasement trade” are only getting stronger, so that will keep going.

In today’s post, I lay out how markets might evolve now that the “gold rush” of recent months has ended. Needless to say, forecasting is a dangerous business and I’ll likely be wrong on many fronts. But I feel strongly that the “debasement trade” is here to stay and will only build over the medium term. If that is true, the question then becomes where this trade will pop up next. Will it again be in precious metals, in longer-term yields, in equities or in currencies? I discuss all this in today’s post.

-

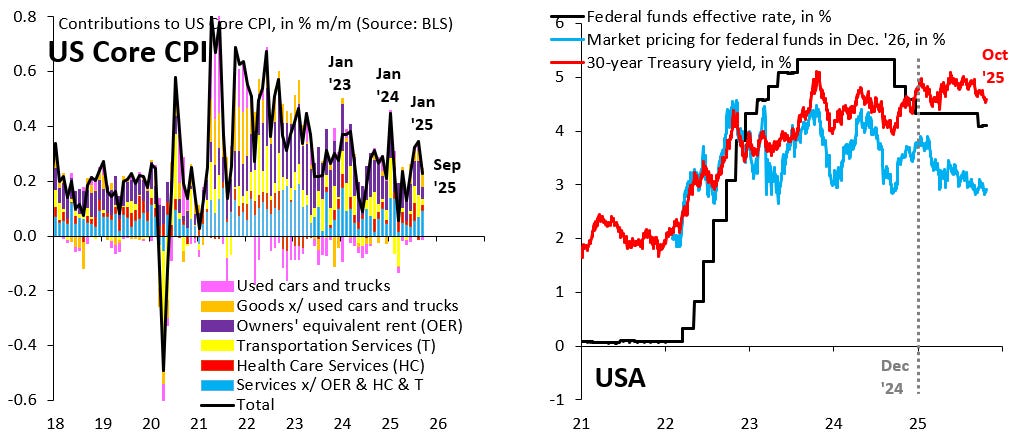

Why the “debasement trade” will build: the Fed is cutting as underlying inflation rises. The “debasement trade” is about the fear that central banks will bend to the will of politicians and monetize unsustainable government debt levels. Some of this “fiscal dominance” is already playing out in the US. The left chart below shows the drivers of monthly core CPI inflation (black line). My preferred measure of underlying inflation – what inflation is after you filter out all the noise – is the blue bars, which have trended up for half a year. That just isn’t an environment where the Fed should be cutting, let alone be in a substantial easing cycle. The blue line in the right chart below shows that markets price almost five 25 basis point rate cuts between now and the end of 2026. The fact that the Fed isn’t pushing back on this market pricing understandably raises questions about its credibility and is one reason why longer-term Treasury yields (the red line in the right chart below) remain high even as more and more Fed cuts get priced.

-

Why the “debasement trade” will build: fewer safe haven assets. I’ve been banging on about how safe haven countries like Japan or Germany are losing that status. Indeed, there are many places across the G10 where fiscal policy is unsustainable, not just in the US. This is why the Dollar was stable in the course of the precious metals rally in recent months, as the blue line in the left chart below shows. The debasement trade isn’t about the US, it’s about a much broader loss of confidence in fiat currencies. The Japanese Yen would have been a key place to hide in the past, but the blue line in the right chart below shows that’s tumbling against the Dollar. The safe havens of today are Switzerland (black line), Sweden (red line) and Norway (orange line). Unsurprisingly, these are places where government debt is low because fiscal policy hasn’t become unmoored.

-

Where will the “debasement trade” pop up next? Precious metals are back in the same holding pattern they were in after the April tariff shock wore off. Longer-term bond yields are in a similar holding pattern as markets price more and more rate cuts for G10 central banks, which is pulling long-end yields down for now. Perhaps the best “debasement trade” currently is the S&P 500, which is up over 15 percent so far this year. President Trump frequently looks to the stock market as validation of his policies. The S&P 500 won’t be allowed to fall. What will also not fall is the Dollar, which – as the left chart below shows – has been stable since its sharp fall in April. So much “bad news” is priced into rate differentials, which have moved massively against the Dollar, that the only way for the greenback is up. Indeed, over the past few weeks, I’ve heard more and more talk of a return of “US exceptionalism.” Sentiment on the Dollar is changing for the better.