Cognizant Technology Solutions recently announced the launch of its Enterprise Vibe Coding Blueprint, a suite of services and reusable intellectual property that enables large enterprises to securely and efficiently operationalize AI-assisted coding across both technical and non-technical teams.

This move builds on the company’s record-setting Vibe Coding Week and highlights a shift toward fostering broad-based AI literacy and practical application within client organizations, reaching beyond traditional developer roles.

We’ll explore how the introduction of the Enterprise Vibe Coding Blueprint could reshape Cognizant’s investment case and growth outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

To be a Cognizant Technology Solutions shareholder, one must believe in the company’s ability to lead enterprise adoption of AI-driven services, leveraging its proprietary platforms and deep consulting expertise to accelerate clients’ digital transformation. While the launch of Enterprise Vibe Coding Blueprint amplifies Cognizant’s differentiation in enterprise AI, it does not materially shift the immediate catalyst, clients scaling GenAI/automation projects, nor does it reduce the key risk of margin pressure from heightened competition and evolving client demands.

Among recent developments, Cognizant’s July rollout of Agent Foundry stands out as it directly relates to the company’s focus on proprietary AI offerings, further supporting the current catalyst of large-scale AI implementation deals. Both the Blueprint and Agent Foundry signal Cognizant’s commitment to capturing new automation-led revenue streams, but risks remain if the company cannot continue scaling these platforms to offset potential headwinds from traditional outsourcing erosion.

However, investors should also be aware that if technological progress outpaces demand for Cognizant’s labor-intensive services…

Read the full narrative on Cognizant Technology Solutions (it’s free!)

Cognizant Technology Solutions’ latest forecasts project $23.5 billion in revenue and $2.9 billion in earnings by 2028. This outlook is based on analysts’ expectations for 4.7% annual revenue growth and a $0.5 billion increase in earnings from the current level of $2.4 billion.

Uncover how Cognizant Technology Solutions’ forecasts yield a $85.80 fair value, a 30% upside to its current price.

CTSH Community Fair Values as at Oct 2025

Eight community-generated fair value estimates for Cognizant range from US$66.06 to US$117.06 per share, reflecting wide variation in expectations. While many see upside, ongoing competition from established technology vendors could impact future earnings and project wins, consider multiple viewpoints to make a more informed decision.

Explore 8 other fair value estimates on Cognizant Technology Solutions – why the stock might be worth just $66.06!

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Right now could be the best entry point. These picks are fresh from our daily scans. Don’t delay:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CTSH.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

If you are eyeing CME Group stock and wondering whether now is the right time to buy, hold, or maybe wait on the sidelines, you are not alone. Over the past few years, CME has treated its long-term shareholders to a remarkable journey, boasting a 100.4% return over the past five years. Even zooming in, the ride has stayed exciting, with a 15.1% return so far this year and 22.6% over the last twelve months. Some investors might notice the dip of 1.3% in the past week, raising questions about whether new developments such as the company’s plan to launch sports contracts by the end of the year are already baked into the price or are hinting at shifting risk perceptions in the market.

Of course, price action is only half the story. Analysts have recently adjusted their expectations; UBS even trimmed its price target slightly, despite raising estimates, reflecting a bit more caution about future outlook. Meanwhile, CME’s latest venture into sports contracts could open fresh revenue streams, especially as it wades deeper into prediction markets alongside big names in the industry. With competitors watching closely and industry partnerships evolving, the question is not just whether CME Group’s stock can keep climbing, but whether its current valuation really stacks up against its prospects.

When we run CME Group through our 6-factor valuation check, it scores a 1 out of 6 for being undervalued, so not a screaming bargain at first glance. But before jumping to conclusions, let’s break down what those valuation measures really mean and see if there is a more insightful way to judge what CME is worth in today’s market.

CME Group scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

The Excess Returns valuation approach examines how well a company generates returns above its cost of equity. Instead of focusing simply on earnings or cash flows, it measures the value created over and above what shareholders expect as a return for their capital. For CME Group, recent analyst estimates suggest its book value stands at $77.13 per share, while its expected stable earnings per share are $12.28, based on a weighted average of future Return on Equity projections from eight analysts.

With a cost of equity set at $6.41 per share, CME achieves an excess return of $5.87 per share. This translates to an impressive average Return on Equity of 15.56%. The model also references a stable book value projection of $78.88 per share, built from assessments by five different analysts. These figures together inform a valuation model designed to capture the company’s ability to unlock value well into the future, rather than reflecting just short-term profits.

Taking these key indicators into account, the Excess Returns model calculates an intrinsic value for CME Group that is 37.1% below the current share price. This suggests the stock is substantially overvalued by this measure.

Result: OVERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for CME Group.

CME Discounted Cash Flow as at Oct 2025

Our Excess Returns analysis suggests CME Group may be overvalued by 37.1%. Find undervalued stocks or create your own screener to find better value opportunities.

For established, profitable companies like CME Group, the Price-to-Earnings (PE) ratio is widely considered one of the most reliable valuation methods. It captures how much investors are willing to pay for each dollar of current earnings, offering a straightforward gauge of market sentiment around profitability and future growth prospects.

The appropriate or “fair” PE ratio is not a one-size-fits-all number. It shifts based on factors such as expected earnings growth, perceived risks, and broader industry trends. Higher growth and stability often warrant a higher PE, while risk and competitive pressures can bring it lower.

Currently, CME Group trades at a PE ratio of 25.9x. That places it exactly in line with the broader capital markets industry average of 25.9x, but well below the average of its peer group, which sits at 33.8x. On the surface, this might suggest a reasonable or even conservative valuation compared to peers.

However, Simply Wall St’s “Fair Ratio” offers a deeper perspective by factoring in CME’s unique attributes, including its earnings quality, growth forecast, profit margins, its market cap, and the risks specific to this business. Unlike a simple industry or peer comparison, the Fair Ratio captures a more nuanced base case for what multiple a business should trade at in light of all these realities. For CME, the Fair Ratio currently stands at 17.7x, meaning its market price is well above what these fundamentals suggest is justified.

Comparing the Fair Ratio of 17.7x to the current PE of 25.9x, CME Group’s stock is trading at a significant premium, indicating it is overvalued on this basis.

Result: OVERVALUED

NasdaqGS:CME PE Ratio as at Oct 2025

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is simply your story behind the numbers—your personal perspective about where CME Group is headed, expressed through your own fair value and estimates for future revenue, earnings, and profit margins.

Rather than just relying on historic figures or generic multiples, Narratives link your outlook on the company and its industry to an actual financial forecast. From there, you arrive at a Fair Value that reflects your unique view. Narratives are easy to create and explore on Simply Wall St’s platform within the Community page, where millions of investors together bring diverse insights and evolving perspectives.

By setting your own Narrative, you can instantly see how your fair value compares to the current price, helping you decide if it is time to buy, sell, or hold. Narratives refresh dynamically as new news or results come in, so you are always working with up-to-date information.

For example, some investors using Narratives see CME Group fairly valued as high as $313, citing strong international expansion and retail growth. Others set targets as low as $212, factoring in competition and technology risks.

Do you think there’s more to the story for CME Group? Create your own Narrative to let the Community know!

NasdaqGS:CME Community Fair Values as at Oct 2025

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CME.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Yuki Tsunoda has hit out at Liam Lawson for “always doing something on purpose” after complaining of being blocked by the Racing Bulls driver in Qualifying for the United States Grand Prix.

Tsunoda and Lawson have been involved in a number of…

FRISCO, Texas — Donovan Ezeiruaku never went more than two games last year at Boston College without a sack. He is six games into his Dallas Cowboys career, and the second-round defensive end is still looking for his first sack as a…

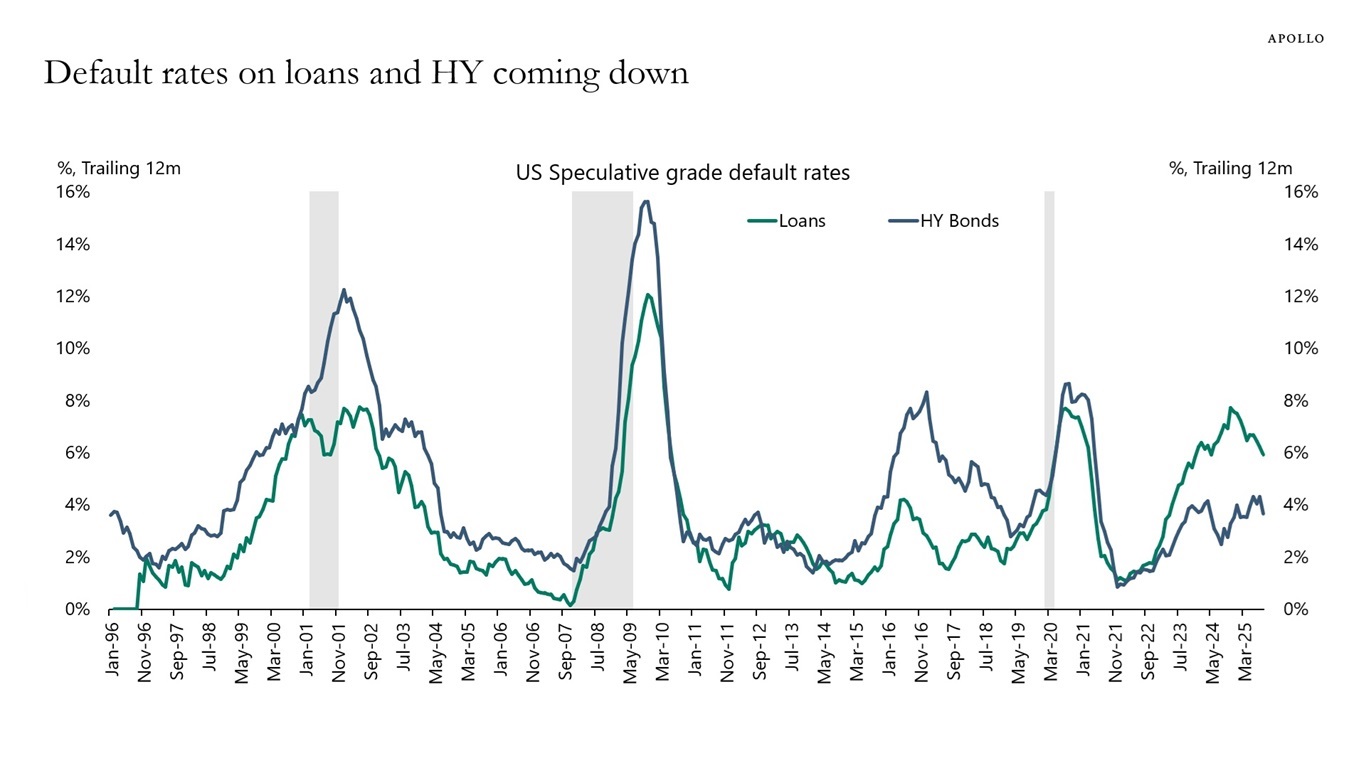

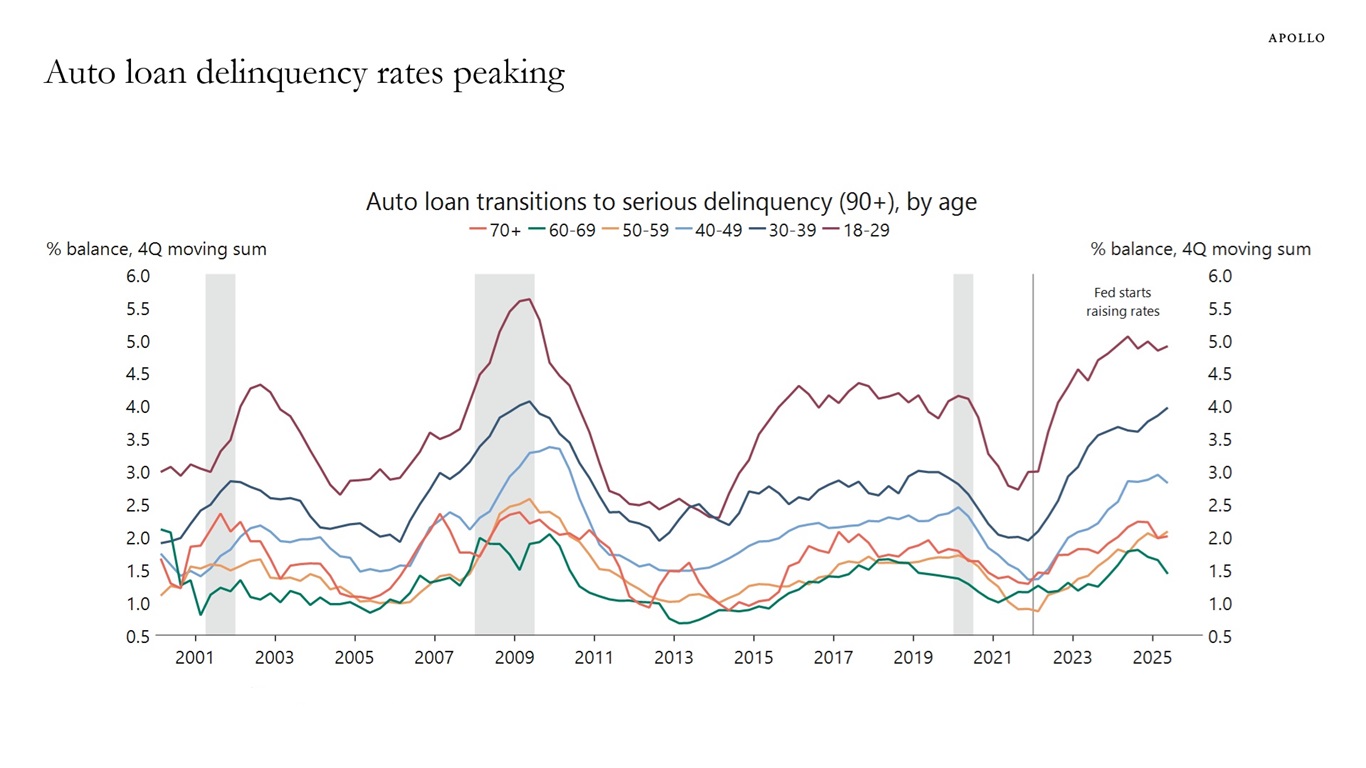

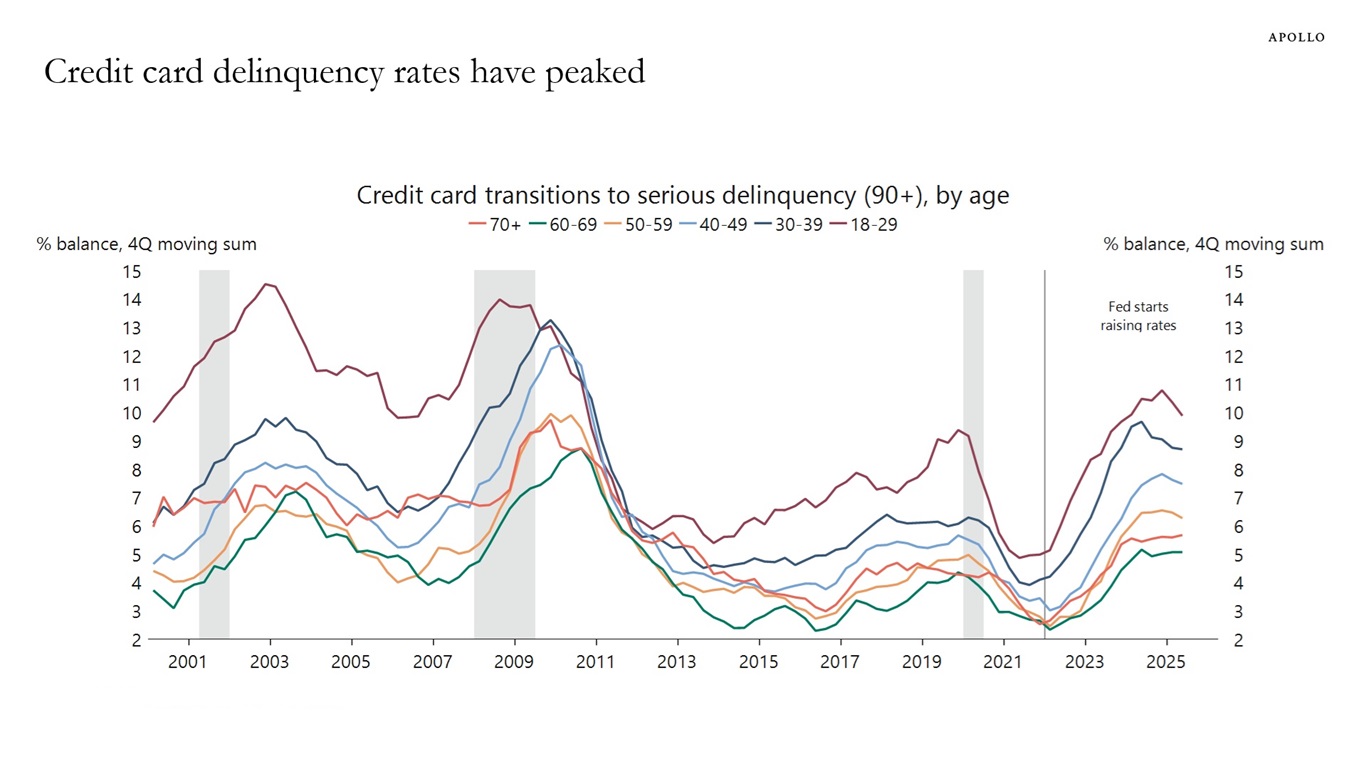

Contrary to widespread fears about the economic outlook, key credit indicators are turning more bullish. Default rates for high yield debt and loans have peaked, along with delinquency rates for auto loans and credit cards, see charts below.

Three factors explain why corporate default and consumer delinquency rates are moving lower:

1) Uncertainty related to the trade war is significantly lower than its peak during Liberation Day.

2) The ongoing AI boom is boosting the buildout of data centers and related energy infrastructure. Simultaneously, higher stock prices are supporting consumer spending.

3) Investors are increasingly recognizing that we are in the early stages of an industrial renaissance across sectors like aerospace, defense, manufacturing, biotech and technology/automation.

In summary, while the trade war remains a mild drag on growth, its impact is being more than offset by the tailwinds from the AI boom and the industrial renaissance. Consequently, there is a growing upside risk that economic growth will reaccelerate over the coming quarters.

Sources: Moody’s Analytics, Apollo Chief EconomistSources: Federal Reserve Bank of New York, Macrobond, Apollo Chief EconomistSources: Federal Reserve Bank of New York, Macrobond, Apollo Chief Economist

Download high-res charts

This presentation may not be distributed, transmitted or otherwise communicated to others in whole or in part without the express consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

Apollo makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made during this presentation, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of the speaker as of the date indicated. They do not necessarily reflect the views and opinions of Apollo and are subject to change at any time without notice. Apollo does not have any responsibility to update this presentation to account for such changes. There can be no assurance that any trends discussed during this presentation will continue.

Statements made throughout this presentation are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed during this presentation, including consulting their tax, legal, accounting or other advisors about such information. Apollo does not act for you and is not responsible for providing you with the protections afforded to its clients. This presentation does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by Apollo.

Certain statements made throughout this presentation may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

Max Verstappen secured pole position for the United States Grand Prix, backing up his lights-to-flag victory in the Sprint, despite a timing error from Red Bull denying him a second timed effort in Q3.

With age comes a natural decline in cognitive function, even among otherwise healthy adults without dementia. A new study finds that a cognitive training program may boost production of a brain chemical that plays a role in memory and attention.