Mount Fuji and the Shinjuku skyline in Tokyo, Japan, on Friday, Feb. 14, 2025. Photographer: Kiyoshi Ota/Bloomberg via Getty Images

Bloomberg | Bloomberg | Getty Images

Asia-Pacific markets fell Wednesday as investors assessed trade data from Japan and its new government.

Japanese exports in September snapped four months of declines, climbing 4.2% year on year, as shipments to Asia saw robust growth, partially offsetting the drop in exports to the U.S.

Exports, however, missed analysts’ expectations of a 4.6% rise, according to median estimates in a Reuters poll of economists.

Prime Minister Sanae Takaichi and her new cabinet were sworn in on Tuesday, with her former rival in the ruling Liberal Democratic Party’s leadership race, Shinjiro Koizumi, named defense minister and Satsuki Katayama becoming Japan’s first female finance minister.

Japan’s Nikkei 225 was down 1.26%, leading losses in Asia, while the Topix index lost 0.18%. Shares of SoftBank plunged over 10%, building on their 0.26% drop on Tuesday. Shares had gained 8.5% on Monday.

On Tuesday, the Nikkei briefly set a new intraday record of 49,945.95, before retreating after Takaichi won the parliamentary vote to become Prime Minister.

South Korea’s Kospi index was down 0.26%, while the small-cap Kosdaq fell 0.25%. Shares of LG Chem soared as much as 10% after Palliser Capital urged the chemicals company to revamp its board and buy back shares, according to a Reuters report.

Australia’s S&P/ASX 200 started the day down 0.73%, pulling back from earlier gains on Tuesday after rare earth stocks briefly rallied on news of a U.S.-Australia critical minerals agreement.

Hong Kong Hang Seng index futures were at 25,919, lower than the last close of 26,027.55.

Indian markets are closed for a holiday.

Overnight in the U.S., the Dow Jones Industrial Average set a new closing record, boosted by strong earnings reports from companies such as Coca-Cola and 3M, while the S&P 500 was relatively unchanged.

The 30-stock index gained 0.47% to close at 46,924.74, and briefly topped 47,000 during the session.

The broad market S&P 500 closed just above the flatline at 6,735.35, while the tech-heavy Nasdaq Composite lagged, falling 0.16% to 22,953.67.

—CNBC’s Sean Conlon and Pia Singh contributed to this report.

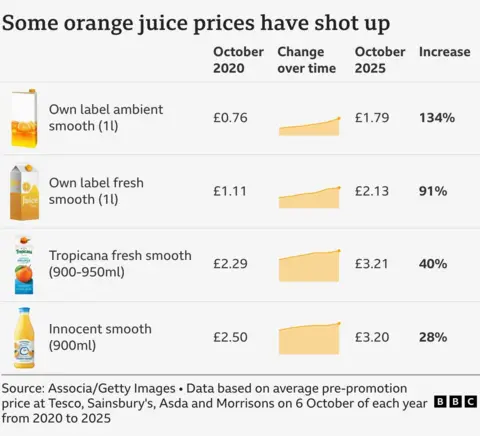

There has been more than a bitter twang in the glasses at British breakfast tables. Only five years ago, a typical supermarket own-label carton of orange juice could be bought for 76p for 1 litre. It now costs £1.79.

That’s a rise of 134% since 2020, and it’s up 29% just in the past year.

In cafes and restaurants it’s a similar story – with £3.50 to £4 now a standard price point for a glass of basic OJ.

One colleague was outraged to be sent a bill for £9 for a glass of hangover-busting orange juice and lemonade at an unassuming little restaurant in Kent. Asked why so much, she was told that the orange juice – albeit freshly squeezed – accounted for £5.30 of the price.

Yet as costs have surged, the taste is changing too, with certain manufacturers substituting oranges for mandarins to cut costs.

The public is, if you like, being freshly squeezed.

There are all sorts of reasons for this: disease among crops, extreme weather, over-reliance on supply from a single nation, new rules for packaging and complexities around trade wars and Brexit.

All of this is compounded by grocery price inflation which, after hitting 17.5% in 2023, came down (to around 5.7% in August) but is rising once again. New figures for overall inflation will be released later today.

It is a perfect storm.

Yet the problem is not isolated to orange juice – track the prices of all sorts of other groceries in supermarket aisles and you’ll see a similar pattern. And so understanding what has happened to orange juice offers a glimpse into how our overall grocery bills suddenly seem so expensive.

It all prompts the question: is this storm a passing one, or are prices set to remain stubbornly high – and should brace for them staying that way permanently?

The Bing Crosby effect

Where else to start but in the orange groves of Florida where the industrialisation of OJ began as an initiative of the US Army during World War Two.

The US government was seeking a source of transportable Vitamin C for troops that didn’t taste like turpentine.

Hulton Archive/Getty Images

Orange juice from concentrate was commercialised by Minute Maid

Orange juice is nearly 90% water. So gently evaporating the water off the juice and freezing the concentrate, allowed for transportability of a much better tasting product when water was later re-added.

WW2 ended before the troops got to try it, but it ended up being commercialised by what became the American soft drink giant, Minute Maid.

It was popularised by Bing Crosby, who, as a significant shareholder, would sing in ads and radio show jingles about frozen orange juice being “better for your health”.

Western consumption of orange juice surged.

TV Times/ Getty Images/ Screen Archives

Minute Maid orange juice was popularised by Bing Crosby

Flash forward to today and an estimated 2.5 billion gallons of orange juice are drunk each year – with about a tenth of that in the UK, where the market is still growing.

Drought, disease and flooding

At an industrial unit in the Essex town of Basildon, green steel drums of frozen orange concentrate arrive from Brazil, overseen by Maxim McDonald.

His firm Gerald McDonald and Co is named after his grandfather, a pioneer who was importing orange concentrate as far back as the 1940s from what was then British-mandate Palestine.

Today it produces juices and blends them, then sells them to supermarkets and restaurant suppliers.

But prices reached extraordinary heights in global markets, rising from $1(75p) to $1.50 (£1.12) per lb over the last decade, to a record $5.30 per lb by the end of last year.

This followed five years of poor crops, owing to severe drought and a disease called citrus greening (caused by a bacteria spread by insects). Brazil had its worst crop since 1988. In some parts of its citrus belt, two thirds of orange trees are affected.

“Around September of last year the price shot up to crazy levels,” Maxim tells me. “At the worst time I was being offered $7 a kilo.

“For such a major commodity to go from $2 to $7 is insane, but it took a while to filter through to consumers.”

Until 2023 the rise in orange juice prices was disguised among food inflation in general, explains Philip Coverdale, an industry expert at consultancy firm GlobalData.

Producers have tried to look beyond South America but it’s not easy – the supply of oranges has been sown up by Brazil, even more so than, say, the Saudis have cornered the market for crude oil.

Morocco, Egypt and South Africa grow oranges too but their supplies are more limited. Spain also grows them, but Valencia and Seville oranges are mostly exported as fruit, rather than concentrate. (Plus Spain too suffered from weather-related production slumps, including the floods in Valencia last October.)

AFP via Getty Images

Spain has suffered from weather-related production slumps

Even within Brazil the market is concentrated in the hands of huge industrialised conglomerates.

In a truly competitive market the price would settle again – but it hasn’t, nor does the industry expect it to. This is a phenomenon that is common to many other ordinary groceries too whose prices have risen.

Oranges becoming less sweet

Florida is the other traditional exporter of oranges, but output from the Sunshine State over the past year has been the lowest since the Great Depression, amid a high number of hurricanes and long-term problems caused by citrus greening.

One problem with greening is that it reduces sugar content, making oranges less sweet.

“Not many are buying Florida oranges any more unless it is a requirement to label the juice ‘Florida Orange’,” says Maxim McDonald.

“It’s very difficult to get oranges out of Florida [because of the shortages] and it’s too expensive.”

VW Pics/Universal Images Group via Getty Images

Spain also grows oranges – but Valencia and Seville oranges are mostly exported as fruit, rather than concentrate

One of the leading suppliers to Tropicana sold off some of its land earlier this year to build homes.

Tropicana itself, the marquee US brand for orange juice, had to restructure its debts this year. Pepsi has also sold most of its stake in it.

One of Tropicana’s recent product innovations in the US has been to launch an “essentials” brand of orange juice “blends” – combining orange, apple and pear juice – at a lower price.

Similar trends can be seen on British shelves. Orange is being mixed with mango, mandarins and clementine juice. Mango purée is especially cheap right now, driven by a good harvest in India. Mandarin concentrate, meanwhile, is cheaper than its orange equivalent because there is less demand for it.

These developments save money, but also maintain the traditional sweetness of the taste.

Tariffs: War on the orange

Then there is the added impact of the recent spike in trade tensions with the US since President Trump introduced new tariffs.

Oranges, it transpires, have been at the centre of it.

US exports of orange juice to Canada have slumped to a 20-year low after Canada put counter-tariffs on US exports. The former PM Justin Trudeau warned that Canadians might have to “forgo Florida orange juice”.

The Trump administration has also settled on a 10% tariff on orange juice coming from Brazil, which will feed into US supermarket prices.

In 2024, the UK eliminated tariffs on some imports produced from fruit grown outside Britain. But tariffs on certain sweeter, cheaper varieties and blends were not part of this.

And while the tariff cuts might have helped, they were vastly outweighed by the increase in the underlying price.

Getty Images

The Trump administration has put a 10% tariff on orange juice coming from Brazil

Then there are new regulations around packaging, further adding to the pressures.

The rules, known as Extended Producer Responsibility, are aimed at improving recycling rates, with a weight-based fee. All juice producers will be impacted, especially those still using glass bottles.

In August a Bank of England report said that high food price inflation is driven partly – and among other things – by these regulations.

Did the West fall out of love with OJ?

In Brazil, the orange harvest has recovered somewhat – this is the greatest hope for a return to normal prices. Yet it coincides with sinking demand: global consumption of orange juice is now down 30% from a peak two decades ago.

Though this may be partly down to the high prices, in certain parts of the world there has also been a shift in perception about the sugar content and health benefits or otherwise of fruit juice.

“When young children are not regularly given juice from an early age, they are less likely to be regular juice drinkers in later years,” suggests Philip Coverdale at GlobalData.

Demand is increasing in countries with growing middle classes, such as China, South Africa, and India. But elsewhere other more exotic fruit juices such as mango, pear and pomegranate are growing in popularity.

AFP via Getty Images

South Africa grows oranges but its supplies are small

Ultimately, however, orange juice is a staple that supermarkets have long been used to selling at low prices. And the price spikes to £2 a carton could, with for example better weather, simply reverse.

“The volatility in the harvest appears to have reduced,” says Giles Hurley, UK CEO of Aldi, “Our buying team are doing everything they can to ensure that that saving is passed on to consumers.”

Others in the supply chain are less convinced, given that much of the frozen concentrate was bought at last year’s high prices. Plus, the stranglehold of the small number of giant producers who control the market remains.

As for the citrus greening, some major commercial producers, including Coca-Cola, which owns Minute Maid and Innocent, have contributed to a project to Save the Orange, using artificial intelligence to find a way to combat it.

It’s a long-term project – and even if fruitful, it may be some time before the effect – if at all – filters through to grocery bills.

But the story of orange prices does also show how an upward price shock gets transmitted around the world far more quickly than a downward one.

Chocolate, coffee, butter and beef

Oranges are not the only food that has seen a price spike, of course. The price of beef and veal is up almost 25% in a year. Butter is up almost 19%, and chocolate and coffee 15% and milk over 12%, all according to the Office for National Statistics.

This all suggests that, more generally, there may be something else at play. And that for all the food and drink spikes, the consumer was actually protected from the worst of it for a period – and now it is pay back time.

“It might be the retailers didn’t full pass through the cost increase in the first place and therefore it’s a way of recouping some of the margin they would otherwise have got,” says Steve McCorriston, Professor of Agricultural Economics at the University of Exeter.

EPA – EFE/REX/ Shutterstock

Do consumers need to simply accept the fact that the UK will be increasingly exposed to food price shocks?

Ultimately, though, trying to unpick the precise reason for why our food and drink costs what it does is very difficult – other factors that influence price can go undetected.

“What we don’t know much about is how these supply chains tend to work in practice. It’s difficult to uncover relationships between retailers and manufacturers or farmers and the use of contracts.”

There is also a broader question that goes well beyond orange juice: do consumers in the UK need to simply accept the fact that as a densely populated small country with limited agriculture, a changing climate means the UK will be increasingly exposed to food price shocks?

A 2024 government report on food security noted: “The UK continues to be highly dependent on imports to meet consumer demand for fruit, vegetables and seafood…

“Many of the countries the UK imports these foods from are subject to their own climate-related challenges and sustainability risks.”

And so it could be that this is only the start of a wild ride on what we pay for our food and drink.

Top image credits: Daniel Grizelj/ Tetra Images/ Getty Images

BBC InDepth is the home on the website and app for the best analysis, with fresh perspectives that challenge assumptions and deep reporting on the biggest issues of the day. You can now sign up for notifications that will alert you whenever an InDepth story is published – click here to find out how.

Shoppers have yet to see the full impact of price increases on store shelves, one analyst says

Mattel reported quarterly results on Tuesday.

Mattel Inc. on Tuesday said it expects a decent holiday season, but shares still dropped after the toymaker’s third-quarter earnings report missed Wall Street’s expectations.

The results arrived as toymakers and retailers gear up for the key holiday-shopping stretch – and as they both try to cushion the impact of tariffs, which have made imports more expensive and threatened to push prices higher for inflation-weary consumers.

For the third quarter, Mattel reported sales of $1.74 billion. That was down 6% year over year, led by a drop in North America, and below FactSet analyst estimates for $1.83 billion. The company’s adjusted earnings per share came in at 89 cents, below forecasts for $1.06.

Mattel shares (MAT) dropped around 6% in after-hours trading Tuesday.

Chief Executive Ynon Kreiz said that since the start of the fourth quarter, orders from U.S. retailers had grown as stores try to stock up for the holiday season. So had point-of-sale trends and consumer demand overall.

“Looking into the balance of the year, we expect a good holiday season for Mattel and strong top-line growth in the fourth quarter,” he said.

Against that backdrop, Mattel said it was sticking with its full-year outlook. The company expects adjusted earnings per share of $1.54 to $1.66 for the full year.

Mattel’s results also landed as it tries to become more of a gaming and entertainment company, along with one that sells classic toys like Hot Wheels, Barbie dolls and action figures.

Netflix Inc. (NFLX) on Tuesday said it was partnering with Mattel and rival Hasbro Inc. (HAS) to roll out toys for “KPop Demon Hunters,” the streaming service’s megahit film. On Monday, Mattel said it had renewed a multiyear licensing agreement to make Disney’s (DIS) Princess and “Frozen” toys.

Some analysts expect holiday spending to cool slightly this season, as consumers stay selective on purchases and wrestle with tariff-related anxieties. In May, Mattel said it planned to raise prices in the U.S. “where necessary” as it grappled with the Trump administration’s trade wars.

During Mattel’s earnings call Tuesday, Kreiz said Mattel’s U.S. business during the third quarter was “challenged” by changes in the way retailers are ordering toys that shifted orders to the fourth quarter. More retailers, management said during the call, were opting to let Mattel handle imports and warehousing before taking in items – a more “just-in-time” approach to shipping, as retailers look for more flexibility in committing to orders.

UBS analyst Arpine Kocharyan said in a research note Monday that Mattel and Hasbro, as larger players in the toy industry, were in better shape than their rivals heading into the holidays. But she noted that the toy companies have largely acknowledged that shoppers have yet to see the full impact of price increases on store shelves.

Kocharyan said the industry was also running up against issues trying to move production out of China, a country that it has relied on for manufacturing and which the U.S. has targeted in its global trade war.

“The process of taking production out of China has been bumpier than anticipated for the industry,” she said.

“Buyers note supply-chain problems and issues with uninterrupted supply, while suppliers highlight disappointing production processes due to a lack of infrastructure in markets such as Vietnam and India and others,” she added.

-Bill Peters

This content was created by MarketWatch, which is operated by Dow Jones & Co. MarketWatch is published independently from Dow Jones Newswires and The Wall Street Journal.

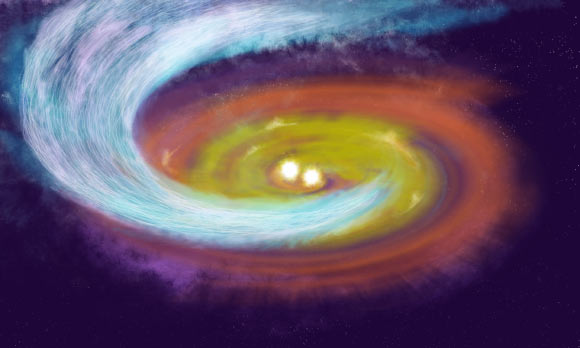

This streamer of gas is channeling matter from the surrounding cloud of a star-forming region in Perseus directly onto a newborn binary star system called SVS 13A.

An artist’s impression of the SVS 13A system. Image credit: NSF / AUI /…

In an age of fierce geopolitical tension, it’s easy to lump all Chinese exports into the same category: state-subsidised oversupply flooding western markets.

However, nothing could be further from the truth when it comes to matcha. As your Big Read shows (“Can Japan satisfy the world’s thirst for matcha?”, October 10), the enormous surge in demand for matcha in the UK and the rest of the world is causing some serious global shortages.

This trend compelled me to turn to China as a source of supply.

As a business owner, I found Chinese matcha to be a great commercial delight. I discovered matcha of comparable grade to Japan’s, for half the price, sometimes even less.

And as a certified tea sommelier, I found Chinese matcha intriguing. Though there was a fair share of pretty rubbish matcha, if one looks there are certainly gems that rival what Japan has to offer. Perhaps not the grand cru of matcha, but premier cru it certainly is.

So perhaps China turning its hand to this rediscovered agricultural export may end up bringing good to the world — or at least to Gen Z and yuppy millennials, who will no longer have to pay £5 for a cup of matcha.

Raphael Chow Managing Director & Co-founder, Brut Tea, London W1, UK

The U.S. Cybersecurity and Infrastructure Agency has issued a warning relating to an actively targeted Microsoft Windows vulnerability that can be found in unpatched versions of Windows 10, Windows 11 and Windows Server.

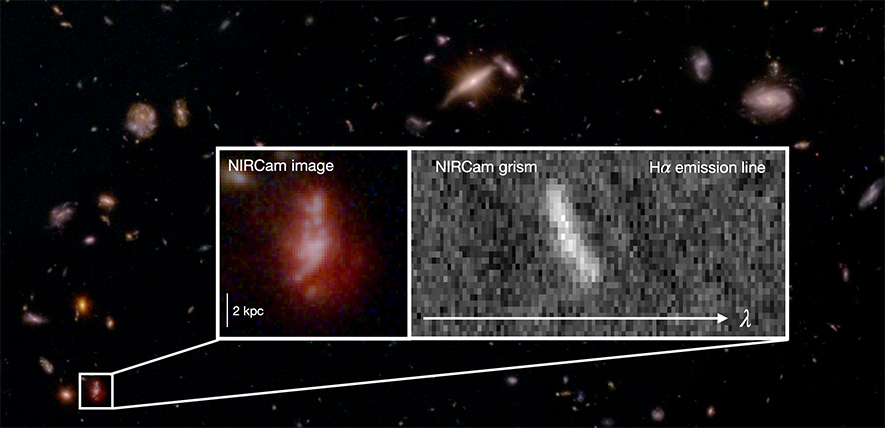

The team, led by researchers at the University of Cambridge, analysed more than 250 young galaxies that existed when the universe was between 800 million and 1.5 billion years old. By studying the movement of gas within these galaxies, the…

Capital One shares rose on Tuesday evening after the credit card issuer reported a sizeable quarterly beat, driven by improved credit quality performance. Revenue in the third quarter ended Sept. 30 increased 53% year over year to $15.36 billion, beating the LSEG-complied consensus estimate of $15.08 billion. Adjusted earnings per share increased 32% year over year to $5.95, exceeding the $4.37 estimate, LSEG data showed. This adjusted figure excludes a $1.12 after-tax diluted EPS impact tied to integration expenses, intangible amortization expense, and loan and deposit fair value market amortization related to the Discover acquisition. COF YTD mountain Capital One YTD Shares were trading up about 4% in extended trading Tuesday night to around $226 per share. The stock’s record close is $229.74 set on Sept. 18. Bottom line The biggest takeaway from the quarter was better-than-expected credit performance. Credit has become a hot topic in the market lately due to the notable collapses of auto parts manufacturer First Brands Group and the subprime auto lender Tricolor Holdings. A few regional banks also recently flagged bad loans tied to possible fraud. Since Capital One has a large exposure to the subprime market, some investors weren’t quite sure how its loans were holding up. The subprime market is usually the first to feel the pain of an economic slowdown. That’s why it was so important to see Capital One once again report strong credit metrics, with better-than-expected net charge-offs and provisions for credit losses, resulting in an allowance release of $760 million and a boost to earnings per share by almost $1. Provisions for credit losses are funds that Capital One sets aside to cover potential loan defaults – the higher the provisions, the worse the sign of credit quality. The $760 million reflected continued favorable credit performance but was partially offset by what the company called “emerging economic uncertainties.” Why we own it Capital One’s acquisition of Discover is a transformative deal with significant strategic advantages and financial benefits. There are also several billion dollars worth of expenses and network synergies that should make this deal highly accretive to earnings per share. Lastly, the acquisition strengthens Capital One’s balance sheet, allowing for aggressive share repurchases in the future. Competitors : American Express , MasterCard , Visa Most recent buy : July 31, 2025 Initiated : March 6, 2025 Beyond the scrutiny of credit metrics, the other focus of Tuesday night’s post-earnings conference call was $35 billion acquisition of Discover and its integration. The company is still in its early stages, but the initial results are encouraging, with all synergies on track. “As a result of years of strategic preparation, we have a wealth of opportunities today that put us in an advantageous position to grow and win in the marketplace as it continues to change dramatically,” CEO Richard Fairbank said on the earnings call. “To capitalize on these opportunities at this special moment, we need to make significant and sustained investments.” He added, “Our acquisition of Discover enhances and accelerates some of these opportunities, and, of course, brings new opportunities as well.” Our thesis remains that the Discover acquisition will improve Capital One’s earnings power and help re-rate its price-to-earnings multiple as the business model evolves to more closely resemble American Express. By the way, we can check one box off our thesis after the company revealed a huge new share repurchase authorization. We’re reiterating our buy-equivalent 1 rating and price target of $250. Deal outlook On the earnings call, Capital One provided a positive update on the progress of the Discover integration. Consistent with what we learned last quarter, the company expects integration costs to be “somewhat higher” than its previously announced target of $2.8 billion. On the synergy side, Capital One said it’s on track to hit its target of $2.5 billion of net synergies, which is made up of cost savings and revenue synergies generated by moving its debit business and some of its credit business onto the Discover network. Fairbank said the process of moving its Capital One debit business off external networks like Mastercard’s and onto the Discover network is “going well” and will largely be completed in early 2026. Revenue synergies are expected to ramp up in the fourth quarter and in early 2026. From an operating expense standpoint, Fairbank said they are making “good progress.” In terms of long-term strategy, Fairbank wants to win at the top of the credit card market and pursue heavy spenders. He understands that winning in this market requires a lot of sustained investment to create a great product and give customers access to great experiences and exclusive investments. In a nod to JPMorgan’s Chase Reserve and American Express’ Platinum card, Fairbank noted that its biggest competitors in the premium space have “hugely stepped up their levels of investment,” and he wants to do the same. Commentary Capital One’s domestic card portfolio saw its net charge-off rate decline 64 basis points year over year to 3.89%. Net charge-offs refer to the amount of debt a bank has written off as uncollectible, minus any recoveries – a decline is a good thing. “Our charge-off rate has been improving on a seasonally adjusted basis throughout 2025 following the trend of improving delinquencies that started in late 2024 and supported by strong recoveries,” Fairbank explained. Within its consumer banking business, auto net charge-offs were 4.99%, down 62 basis points from the prior year. The auto results should ease fears around Capital One, considering the First Brands and Tricolor bankruptcies. “There’s been a lot of noise in the subprime auto space pointing to rising delinquency rates. Our own performance in subprime auto has remained stable through this time,” Fairbank said. Capital One’s subprime auto exposure is holding up better than peers thanks to a decision it made a few years ago to scale back its auto lending. Fairbank said the company anticipated inflated credit scores, normalizing credit, and declining vehicle values. As for buybacks, we learned during conference season that management stepped up the repurchase program, and they did not disappoint. The company repurchased 4.6 million shares for $1 billion in the third quarter, a sizeable increase from the $150 million worth of stock repurchased in the second quarter. The company also announced a new authorization of up to $16 billion, representing nearly 12% of the company’s current market cap. The company didn’t provide explicit guidance on how quickly it will move through this program, but CFO Andrew Young said that it’s “reasonable to assume that we’ll be picking up the pace of share repurchases from here.” Capital One also boosted the quarterly dividend by 20 cents per share to 80 cents. This bump increases the dividend yield to about 1.5% from $1.11%. (Jim Cramer’s Charitable Trust is long COF. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Chinese scientists studying a 2-gram lunar soil sample from the Chang’e 6 mission have identified rare CI chondrite impact residues, providing new insights into mass transfer in the inner solar system and offering new…