Arts organisations and artists have said they are still in “funding limbo” with mounting bills and uncertain futures after this summer’s crash of Arts Council England’s grant processing platform.

ACE’s online portal, Grantium, was used…

Arts organisations and artists have said they are still in “funding limbo” with mounting bills and uncertain futures after this summer’s crash of Arts Council England’s grant processing platform.

ACE’s online portal, Grantium, was used…

30 October 2025

The Governing Council of the European Central Bank (ECB) has decided to move to the next phase of the digital euro project. This decision follows the successful completion of the preparation phase, launched by the Eurosystem in November 2023, which laid the foundations for issuing a digital euro.

The Governing Council’s decision aligns with European leaders’ request to accelerate progress on the digital euro, as recently stated at the October 2025 Euro Summit. A digital euro will preserve Europeans’ freedom of choice and privacy and protect Europe’s monetary sovereignty and economic security. It will foster innovation in payments and help make European payments competitive, resilient and inclusive. The Eurosystem will implement its preparations flexibly, in line with calls from euro area leaders for the Eurosystem to be ready for a potential digital euro issuance as soon as possible, while also recognising that the legislative process has not yet been completed.

The ECB Governing Council‘s final decision on whether to issue a digital euro, and on what date, will only be taken once the legislation has been adopted. Under the assumption that European co-legislators will adopt the Regulation on the establishment of the digital euro in the course of 2026, a pilot exercise and initial transactions could take place as of mid-2027. The whole Eurosystem should then be ready for a potential first issuance of the digital euro during 2029.

“The euro, our shared money, is a trusted sign of European unity,” said ECB President Christine Lagarde. “We are working to make its most tangible form – euro cash – fit for the future, redesigning and modernising our banknotes and preparing for the issuance of digital cash.”

As payment habits evolve, and cash payments decline compared with digital transactions, the need for a public digital means of payment – complementary to cash – has become increasingly urgent. The digital euro will complement cash and bring its benefits – simplicity, privacy, reliability, availability across the whole euro area – to digital payments. Along with the Regulation on the establishment of the digital euro, the ECB is also supporting the European Commission’s proposal to reinforce the right to pay with cash.

The Eurosystem will focus on three main areas:

“This is not just a technical project but a collective effort to future-proof Europe’s monetary system,” said ECB Executive Board member Piero Cipollone, who chairs the High-Level Task Force on a digital euro. “A digital euro will ensure that people enjoy the benefits of cash also in the digital era. In doing so, it will enhance the resilience of Europe’s payment landscape, lower costs for merchants, and create a platform for private companies to innovate, scale up and compete.”

Transparency and close cooperation with stakeholders have been – and will continue to be – fundamental to the project. The Eurosystem has benefited greatly from feedback from European decision-makers, market participants and potential users, and will continue to engage actively with a wide range of stakeholders.

The Eurosystem’s continued preparation for a digital euro will be implemented flexibly, ensuring alignment with the legislative process. To this end, work will be structured in modules to enable gradual scaling and limit financial commitments.

The final cost of a digital euro – for both its development and operation – will depend on its final design, including components and related services that need to be developed. As a result of the work done in the preparation phase, the total development costs, comprising both externally[1] and internally developed components, are estimated at around €1.3 billion until the first issuance, which is currently expected during 2029. Subsequent annual operating costs are projected to be approximately €320 million per year from 2029. The Eurosystem would bear these costs, as it does for producing and issuing euro banknotes – which, like the digital euro, are a public good. As in the case of banknotes, these costs are expected to be compensated by the generated seigniorage – even if digital euro holdings were small compared with banknotes in circulation.

The conclusion of the preparation phase marks an important transition in the digital euro project. Building on the insights gained during the investigation phase conducted from 2020 to 2023, we moved towards refining its practical design. Key achievements include (i) the development of the draft digital euro scheme rulebook, (ii) the selection of providers for digital euro components and related services, (iii) the successful running of an innovation platform for experimentation with market participants, as well as (iv) the investigation by a technical workstream into the fit of the digital euro in the payment ecosystem. The latter, conducted by the ECB and market participants via the Euro Retail Payments Board, concluded that a digital euro could foster further competition in the European payments market. Besides directly benefiting from distributing the digital euro, banks and other payment service providers could leverage its open standards to expand their reach across the euro area without needing their own acceptance networks. They would also be able to co-badge the digital euro with existing payment solutions.

The ECB provided technical input to co-legislators on request, thereby supporting the legislative process. This input demonstrated that the costs of the digital euro for banks will be contained – these costs will be close to the European Commission’s initial estimates and similar to those incurred for the implementation of the Payment Services Directive. It also showed that safeguards built into the design of the digital euro (such as holding limits) would ensure that it does not create financial stability risks.

To ensure that the digital euro is designed to meet the needs of European citizens and merchants, the Eurosystem conducted extensive user research targeting vulnerable consumers and small merchants. The findings – available in a separate report published today – show the need for a simple, reliable and secure payment experience.

These results reaffirm the ECB’s commitment to developing a digital euro that works for everyone and advances Europe’s financial evolution – designed to empower citizens, support innovation and strengthen the resilience of our monetary system.

For media queries, please contact Georgina Garriga Sánchez, tel.: +49 69 1344 95368.

“A digital euro will ensure that people enjoy the benefits of cash also in the digital era. In doing so, it will enhance the resilience of Europe’s payment landscape, lower costs for merchants, and create a platform for private companies to innovate, scale up and compete”.

Piero Cipollone, ECB Executive Board member

The Eurosystem’s digital euro project aims to adapt central bank money to the digital age, addressing the current challenges of the European payments ecosystem. As payment habits evolve, the use of cash declines and digital transactions become the norm, the need for a public digital means of payment – complementary to cash – has become increasingly urgent. As digital cash, the digital euro is designed to complement physical cash, ensuring that everyone in the euro area can keep using a public, trusted and universally accepted means of payment –now and in the future. Therefore, it will preserve freedom of choice and Europe’s monetary sovereignty across the euro area. In addition, it will foster innovation in payments and help make European payments competitive, resilient and inclusive.

In 2021 the Eurosystem embarked on the investigation phase (2021-23), which focused mainly on the design of the digital euro. In November 2023 the Eurosystem decided to launch a two-year preparation phase to lay the groundwork for the potential issuance of a digital euro. The main objectives of this phase included providing a draft digital euro scheme rulebook, selecting potential providers for the digital euro platform and infrastructure, learning through experimentation and user research, conducting more in-depth technical analyses, and interacting with stakeholders to ensure a digital euro would meet the highest standards of quality, security, privacy and usability. All these objectives have been achieved.

One important area of work in the preparation phase was the further development of the draft digital euro scheme rulebook. The rulebook provides a single set of rules, standards and procedures for the provision of basic digital euro payments services for payment service providers (PSPs) participating in the scheme. It draws as far as possible on existing industry standards and market practices. While the rulebook will ensure a standardised digital euro payment experience across the euro area, it distinguishes between provisions that are mandatory for all scheme participants and provisions that are only optional, illustrative and intended to further support participating PSPs in their implementation efforts. Through this approach, the rulebook standardises requirements and limits them to what is necessary, while providing the basis for the development of further innovative services and supporting interoperability. At the time of closing this report, a new and comprehensive draft version of the rulebook had been shared and commented on by the digital euro scheme’s Rulebook Development Group (RDG) and its constituents. This new draft version covers the functional requirements (such as requirements for the digital euro services related to access, liquidity and transaction management) and non-functional requirements (such as requirements for availability, latency and maintenance). The draft also covers requirements for minimum user experience, dispute management and the application of the digital euro brand, along with detailed implementation specifications. While the draft rulebook will cover all basic digital euro services for the use cases considered, a roll-out plan for the digital euro’s functionality will need to be developed to inform and facilitate its implementation by scheme participants.[1] The process that led to the current draft began in the investigation phase, supported by the RDG.[2] It has been collaborative and iterative, and brings together representatives of consumers, merchants, PSPs and third-party service providers from across the European retail payments market, as well as observers from the Eurosystem national central banks (NCBs) and EU institutions.

The selection of providers for the digital euro service platform (DESP) was another key milestone achieved. The sourcing process covered both externally procured and internally sourced components. Externally, the European Central Bank (ECB) launched tenders for five components of the DESP; core settlement and issuance components were sourced within the Eurosystem. Five external providers were selected, and they all signed framework agreements.[3] These do not entail financial commitments at this stage; any development or operational work will be initiated through subsequent specific agreements.

In parallel, the ECB launched an innovation platform[4] to explore how the digital euro could support innovation in payments and address new market needs. Structured into two workstreams – pioneers and visionaries – the initiative involved around 70 market participants, including banks, fintechs, merchants and PSPs. The pioneers tested features such as conditional payments[5] in a simulated environment, while the visionaries proposed forward-looking new ways to integrate the digital euro into Europe’s financial ecosystem. The work demonstrated that market participants see strong innovative potential in the digital euro, in terms of both technical capabilities and its role in improving financial inclusion, while enabling market participants to develop new business opportunities.

Ensuring accessibility and inclusion has been a guiding principle in the design of the digital euro. In designing the digital euro app, a particular focus was placed on accessibility to ensure the app would be usable by everyone, including people with physical disabilities, low digital skills or learning impairments. The design is informed by user research and feedback from civil society organisations, confirming the importance of multiple onboarding options and payment flows that feel familiar and reassuring. These efforts aim to make the digital euro usable and relatable for everyone – particularly vulnerable groups – and will continue to evolve in the next phase to ensure no one is left behind.

On the technical front, the ECB advanced its analysis to ensure the digital euro remains operational and resilient in a wide range of scenarios, including in emergencies such as power or network outages. Key areas of work included the design of the offline functionality – a crucial innovation allowing payments to be made even when internet connectivity is lost, thus making the European payment landscape even more resilient and providing a cash-like level of privacy. These efforts are aimed at supporting the resilience, usability and inclusiveness of the digital euro and ensuring continuity of payments in critical situations.

To ensure the digital euro’s design is inclusive and meets the needs of European citizens and merchants, the ECB conducted user research throughout the preparation phase, focusing on payment preferences and behaviours. The ECB commissioned both quantitative and qualitative research to gather insights from a broad spectrum of potential users across the euro area. The ECB engaged small merchants and vulnerable consumers through focus groups and interviews. [6] When considering the adoption of a new payment method, vulnerable consumers emphasised the importance of a universally accepted solution with simple, intuitive design and access to in-person support. They also expressed a preference for new payment methods to be distributed by trusted banks and/or public bodies and showed greater willingness to try them if offered by a European provider. Small merchants supported the value proposition of the digital euro and emphasised the importance of increased bargaining power to negotiate lower transaction fees and of seamless integration with their existing systems. The backing of the digital euro by the ECB was also viewed as a further positive factor and perceived as a guarantee of strong payment security, which could increase consumer trust and potential adoption. The Eurosystem also conducted a survey among a large and representative panel of EU citizens to explore payment attitudes and preferences and explore the usability aspects of the digital euro. A majority of respondents (66%) showed interest in trying the digital euro – which is broadly consistent with findings from other surveys conducted by the ECB and NCBs.

Stakeholder engagement was a cornerstone of advancing technical work on the design of the digital euro in the preparation phase. The ECB further intensified its outreach to banks and non-bank PSPs, merchants and consumers through technical sessions, workshops and bilateral meetings at expert and strategic level. Special attention was given to how the digital euro would fit into the existing European payments ecosystem, with dedicated Euro Retail Payments Board (ERPB) technical sessions to assess value drivers across the themes of competition, synergies and business model. The outcome of this work[7] showed there was consensus among market stakeholders across several topics, while on other topics there were diverging views. Key benefits identified by the ECB and all stakeholders included the following: (i) the digital euro would enhance competitiveness in the European payment landscape by strengthening the negotiating position of European PSPs and merchants; (ii) by making use of open digital euro standards, European PSPs and account-to-account (A2A) schemes can voluntarily integrate the digital euro into their payment solutions and/ or co-badge it on physical cards; (iii) the digital euro would establish a “common acceptance layer” for A2A payments, facilitating seamless transactions across point-of-sale (POS) and e-commerce platforms for European players; and (iv) a staggered roll-out approach could be considered for the introduction of the digital euro, striking an optimal balance between market relevance, the Eurosystem’s policy objectives, and technical and implementation costs. A phased roll-out of functionalities would thus enable both costs and resources to be spread over time, while focusing on essential use cases first, ensuring broad adoption and resilience.

The ECB also continued regularly engaging with EU institutions throughout the preparation phase, providing technical input to support the legislative process and keeping the Eurogroup and the European Parliament informed on project developments. This phase has been underpinned by ongoing legislative efforts at European level, with EU leaders emphasising the strategic importance of a digital euro and calling both at their March[8] and October[9] 2025 meetings for swift progress on its adoption to meet the evolving needs of citizens and businesses. In their meeting on 19 September 2025, finance ministers in the Eurogroup agreed on the governance framework around the issuance of the digital euro and on the process of setting a holding limit.[10] This further facilitates the legislative progress in the Council. In parallel, the ECB responded to co-legislators’ requests that emerged during the legislative negotiations with two technical analyses: one assessing the potential financial stability effects of a range of hypothetical digital euro holding limits[11], and another evaluating investment costs for the banking sector[12]. The first analysis confirmed that using the digital euro for day-to-day payments would not harm financial stability and that – given the different hypothetical holding limits of up to €3,000 per person that the co-legislators asked to be tested – the impact of the digital euro would not harm financial stability within the euro area, even under a highly unlikely and extremely conservative crisis scenario. The second analysis found that investment costs for the banking sector could range between €4 billion and €5.8 billion. This would be broadly in line with the estimates given by the European Commission in its draft Regulation impact assessment in 2023 and would be comparable to cost estimates for initiatives such as the Payment Services Directive (PSD2). Public information and engagement activities were stepped up, with ECB representatives participating in numerous public events and seminars to promote awareness and dialogue around the digital euro’s benefits and design.

On 23 October 2025, European leaders called for accelerated progress on the development of a digital euro. On 29 October 2025, the Governing Council of the ECB decided that the Eurosystem will continue its preparations and move to the next phase of the digital euro project. In this phase, the Eurosystem will build the necessary technical capacity ahead of a possible decision to issue, while maintaining flexibility and alignment with the legislative process.

The ECB aims to be ready for a potential first issuance of the digital euro during 2029. This is based on the working assumption that European co-legislators will adopt the Regulation on the establishment of the digital euro in the course of 2026. A pilot exercise and initial transactions could take place earlier, potentially starting as soon as mid-2027, to prepare for a potential issuance.

To deliver on this shared ambition, the Eurosystem will focus on three main workstreams: advancing technical readiness, deepening market engagement and supporting the legislative process. This will include starting to develop the digital euro’s technical foundations and validating core functionalities by means of piloting; working closely with PSPs, merchants and consumer representatives to progressively test and prepare for a first issuance; and maintaining close engagement with EU co-legislators, institutions and authorities on the digital euro project to continue to provide technical input throughout the legislative process.

The Eurosystem’s continued preparation for a digital euro will follow a flexible implementation approach, ensuring alignment with the legislative process. This approach responds to calls from euro area leaders for the Eurosystem to be ready for potential issuance as soon as possible, while also recognising that the legislation has not yet been adopted. Work will be structured in modules to allow gradual scaling and limited financial commitments. The final cost of a digital euro – both for its development and operation – will depend on its final design, components and related services that need to be developed. Total development costs, comprising both externally and internally developed components, are estimated at around €1.3 billion until the first issuance, which is currently expected during 2029.Subsequent annual operating costs are projected to be approximately €320 million per year from 2029.

The ECB Governing Council’s possible decision on whether to issue a digital euro, and on what date, will only be taken once the legislative act is adopted. The ECB will continue to follow the legislative debate closely and implement any appropriate adjustments to the development of the digital euro that may result from legislative deliberations. The Eurosystem aims to ensure that, when the time comes, the digital euro can be made available as a secure, inclusive and innovative complement to cash across the euro area.

The digital euro project is a strategic initiative by the Eurosystem to safeguard the role of central bank money in a rapidly digitalising economy. As payment habits evolve and digital transactions become the norm, the need for a public digital means of payment – complementary to cash – has become increasingly urgent. As a digital form of cash, the digital euro is designed to preserve people’s freedom of choice in how to pay, thereby enhancing financial inclusion and reinforcing Europe’s monetary sovereignty across the euro area.

Europe’s payments landscape remains fragmented, with many countries relying heavily on non-European providers for digital transactions. Nearly two-thirds of euro area card-based transactions are processed by non-European companies, while 13 euro area countries depend entirely on international card schemes or mobile solutions for in-store payments. These private solutions may not always be accessible to everyone or guaranteed to function in all circumstances, such as in times of crisis.

Market leadership and relevant domestic payment options across euro area countries

Notes: World icon stands for “international, non-European solutions”. European flag stands for “European solution”. “P2P” refers to alias-based P2P payments which are not available everywhere. The table does not explicitly highlight the P2G channel that would also be served by the digital euro; however, it is encompassed within the “e-commerce” or “POS” channels. A relevant domestic option is defined as a solution holding an estimated market share exceeding 10% within the respective use case, though other domestic options may also be technically present.

Sources: ECB elaboration based on ECB SPACE report; Euromonitor; Global Payments Report (FIS Worldpay); Key players in the EU payments landscape (The Payments Association EU); Roland Berger.

In addition, there is no European electronic payment option that covers the entire euro area. Current European digital payment solutions, such as cards issued by European payment schemes, mainly cater to national markets and specific use cases. The lack of European payment solutions available on a European scale and the difficulty faced by European PSPs in keeping pace with technological advances mean that Europe is not competitive within its own market.

At the same time, the use of cash continues to decline[13]: in 2024, cash accounted for only 24% of day-to-day payments, and the share of companies not accepting cash has tripled to 12% over the past three years. Over the period from 2019 to 2024, the value of goods purchased in e-commerce doubled, from 18% to 36%.[14] These trends, which are likely to continue owing to the digitalisation of the economy in line with what has been observed in many advanced economies, expose Europe’s payment infrastructure to external risks and limit its strategic autonomy.

The digital euro is designed to address these challenges by providing a public, pan-European digital payment solution that covers all use cases and allows people to pay everywhere in Europe, while being resilient, inclusive and future-proof. The digital euro is designed to complement physical cash. It would offer a digital form of cash backed by the ECB that is universally accepted and free to use, and could be used for person-to-person and retail transactions in both physical and digital environments. Consequently, it would preserve freedom of choice for all individuals and businesses in the euro area, support competition and innovation in the payments market and strengthen the strategic autonomy of the European financial system.

The digital euro is being designed to ensure payments remain possible under all circumstances, with inclusion as its guiding principle. From accessible design features to local support, we are working to ensure that everyone – regardless of income, digital skills or accessibility needs – can benefit from secure and easy-to-use digital payments.

In 2021, the Eurosystem embarked on the investigation phase (2021-2023) in which it developed a high-level product design and the related functional and non-functional user requirements for a digital euro[15]. To lay the foundations for the potential future issuance of a digital euro, the Eurosystem then launched a two-year preparation phase on 1 November 2023. This aimed to achieve the following.

In this phase the Eurosystem has also carried out more in-depth technical analysis on key design features. Engaging with various stakeholders – such as EU policymakers, market participants and civil society – helped in defining rules and safeguards to make a digital euro work in real life for everyone: people, merchants and PSPs.

Collaboration with stakeholders was central throughout, reinforcing the project’s commitment to inclusivity, usability and transparency. EU institutions and policymakers play a critical role in shaping the legal and regulatory framework that would underpin the digital euro, and their work will continue to be vital in the next phase of the project. The legislative process is currently progressing in parallel with the technical preparations. The ECB provided technical input to support both the Council and the Parliament during this process. European heads of state or government have been calling for swift progress on the legislation,[16] and the Danish Presidency of the Council aims to find agreement on a general approach by the end of its term, in December 2025. The ECB is cooperating closely with the Commission as well. The President of the European Commission, Ursula von der Leyen, highlighted in her 2025 State of the Union address that “a digital euro will make it easier for companies and consumers alike”.[17]

This report provides an overview of the work carried out in the preparation phase between November 2023 and October 2025. It consolidates the key deliverables and outcomes of this phase and outlines the next steps. The ECB Governing Council’s possible decision on whether to issue a digital euro, and on what date, will only be taken once the Regulation on the establishment of the digital euro[18] has been adopted.

A key focus during the two-year preparation phase of the digital euro project was the further development of the draft digital euro scheme rulebook. The rulebook aims to define a single set of rules, standards and procedures for the provision of digital euro payments throughout the euro area. It would ensure that PSPs deliver consistent basic digital euro services, enabling a uniform user experience regardless of the country or PSP involved. The rulebook would thus provide the basis for the development of further innovative services, supporting interoperability.

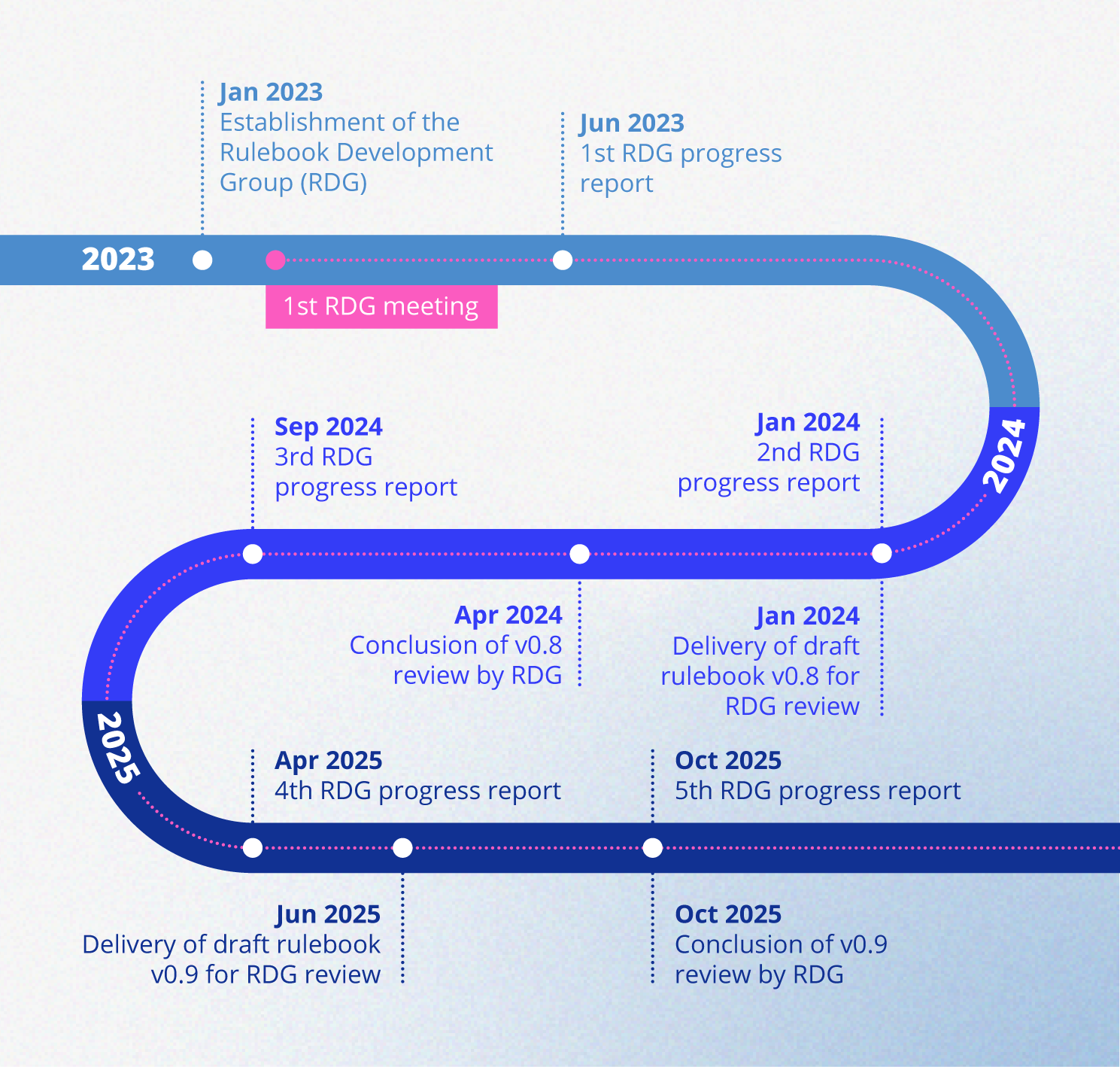

The rulebook is being developed in a collaborative and iterative process with the support of the digital euro scheme’s Rulebook Development Group (RDG). The RDG includes representatives from consumers, merchants, banks and non-bank PSPs, as well as third-party service providers from the European retail payments market, alongside observers from Eurosystem NCBs and EU institutions. Regular updates on the work of the RDG were published in January 2024, September 2024, April 2025 and October 2025.

Developing the digital euro rulebook – Milestones

In January 2024, a first interim draft of the rulebook, which included core chapters on the scope, key actors, functional and operational model, and technical requirements of the digital euro scheme, was produced with the support of the RDG. This version subsequently underwent an interim review, completed in April 2024, during which RDG members and their constituencies submitted around 2,000 unique comments. These were assessed and followed up with draft updates, clarifications or further technical work.

In parallel, several dedicated RDG workstreams were launched to develop and expand on specific areas such as minimum user experience standards, certification and approval frameworks, risk management, and implementation specifications. These workstreams, composed of around 50 market participants from over 30 organisations across the euro area, have since delivered proposals on topics including user journeys, fraud and operational risk mitigation, and implementation specifications covering the technical interactions between end users, PSPs and the DESP. The ECB also hosted expert sessions to inform the rulebook’s technical specifications and ensure robust end-user interactions. These included sessions covering issues such as latency and dispute management as well as PSPs’ liquidity management.

In June 2025, a revised interim draft of the digital euro scheme rulebook was delivered to the RDG and its constituencies. This version reflected the extensive market feedback that was offered during the previous review process in 2024. Additionally, it covered new key areas such as requirements to establish minimum user experience standards, rules providing guidance on the consistent roll-out and application of the digital euro brand, and detailed implementation specifications to eventually support PSPs in the technical implementation of the digital euro. Other areas incorporated into the rulebook included the dispute management framework[19], the onboarding process for scheme participants and, in the same connection, the testing and certification framework for devices and applications used in digital euro transactions, such as payment terminals, ATMs and mobile applications. These various provisions of the draft rulebook are aimed at ensuring a standardised digital euro payment experience across the euro area. At the same time, the rulebook distinguishes between provisions that are mandatory for all scheme participants and provisions that are only optional, illustrative and intended to support participating PSPs in their implementation efforts. Through this approach, the rulebook standardises requirements and limits them to what is necessary, while providing the basis for the development of further innovative services and supporting interoperability.

The delivery of the draft digital euro scheme rulebook in June 2025 marked the beginning of a four-month market consultation with market participants, which was finalised at the end of October 2025. RDG members gathered feedback from their constituents, including consumers, merchants, credit institutions, different types of payment institutions, corporate treasurers and third-party providers. To support this process, the ECB hosted an information session with over 250 selected market experts. These activities were aimed at promoting a shared understanding of the draft rulebook and allowing all relevant actors to provide meaningful input.

Looking ahead, assessing and reviewing the draft rulebook in the light of the feedback from RDG members and their constituents will be essential for its further development. At the same time, additional areas and implementation specifications will be elaborated, in particular those that are dependent on the selection of service providers. With the support of the RDG and the RDG workstreams, work continues on further developing relevant areas of the rulebook, including the technical implementation of specifications for payment initiation methods, the annex on risk matters, further specification of the adherence framework, certification and testing processes, and iteratively expanding the minimum user experience requirements for all basic digital euro services. While the draft rulebook will cover all basic digital euro services for the use cases considered, a roll-out plan for the digital euro’s functionality will need to be developed to inform and facilitate its implementation by scheme participants. The draft rulebook is being designed with sufficient flexibility so that discussions on the digital euro can be taken into consideration.

One key objective of the preparation phase was to select providers for digital euro components and related services. This work focused on both external procurement and internal Eurosystem sourcing to ensure operational readiness for the next project phase. The Eurosystem has been following rigorous procurement processes to guarantee transparency, fairness and the best value for money.

As part of the external procurement process, the ECB launched five public tender procedures covering:

With the publication of the contract notices on 2 October 2025, the Eurosystem completed the selection of providers for each of the five components. Framework agreements were signed with the top two ranked tenderers in each procedure to ensure contingency. The framework agreements were signed with the following providers.

All providers are EU nationals controlled by EU nationals[20], which helps ensure the European autonomy of the digital euro. These contracts do not entail financial commitments at this stage, as any development or operational work will be subject to a specific agreement following the ECB procurement decision. For components sourced from external providers, service requests will initially be directed to the first-ranked provider; the second-ranked provider will be approached only if required.

In parallel with the procurement of external components, the ECB conducted a call for offer among all Eurosystem NCBs to deliver core components such as clearing and settlement and issuance. As a result, a group of six NCBs (Banca d’Italia, Banco de España, Banque de France, Deutsche Bundesbank, Lietuvos Bankas and Oesterreichische Nationalbank) was selected by the Governing Council on 23 July 2025[21] as the provider for the core components.

The final cost of a digital euro – for both its development and operation – will depend on its final design, components and related services that need to be developed. The total development costs, comprising both externally[22] and internally developed components, are estimated at around €1.3 billion until the first issuance, which is currently expected during 2029. Subsequent annual operating costs are projected to be approximately €320 million per year from 2029. The Eurosystem would not charge or benefit from any digital euro transaction fees. Instead, it would bear the costs of the establishment of the digital euro scheme and infrastructure, just as it does for the production and issuance of euro banknotes – which, like the digital euro, are a public good. As with banknotes, these costs would be covered by “seigniorage” – the income the ECB earns from issuing money – even if digital euro holdings were small compared with banknotes in circulation.

To complement these efforts, and in preparation of the next project phase, the ECB published a call for applications for digital euro network service provider connectivity. This procedure covers the provision of connectivity services between the distributed components of external actors (mostly PSPs and NCBs) and the DESP, as well as between DESP components hosted in different sites/data centres belonging to the different providers. Like the other sourcing activities, this procurement includes safeguards to ensure the European autonomy of the digital euro.

Experimentation was one of the core pillars of the digital euro preparation phase. It plays a central role in refining both the technical design and the user experience of the digital euro based on real-world needs, ensuring the digital euro meets the requirements of consumers, merchants and the market and is adapted to emerging innovations.

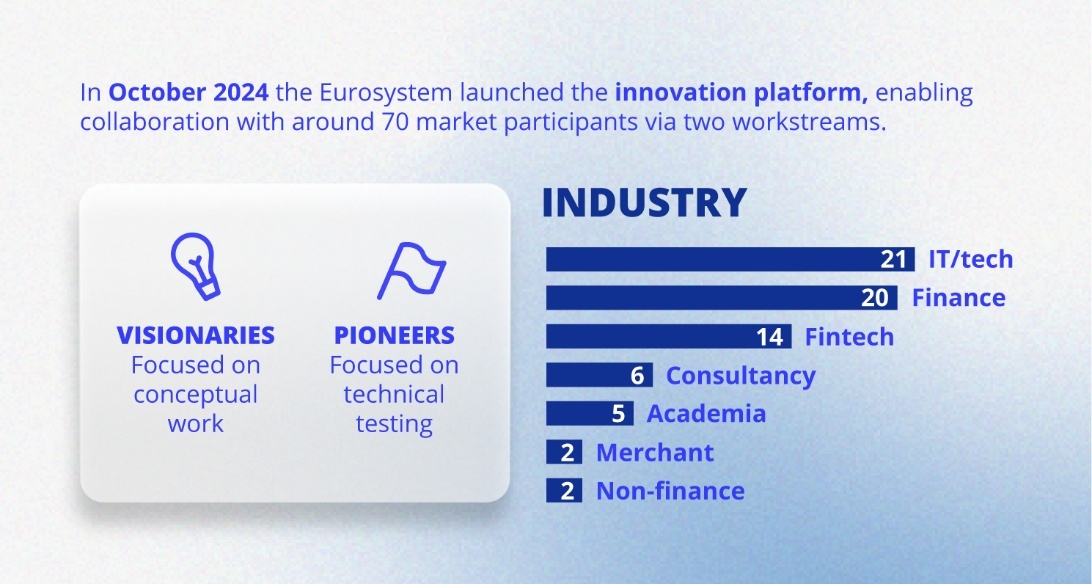

Building on the findings of the investigation phase, the ECB launched its experimentation activities to shape the long-term vision for the digital euro and to engage with the market on innovative use cases. In October 2024, the ECB hosted a workshop on the future of business-to-business (B2B) payments, which attracted over 150 applications from industry and payment experts. Six speakers from sectors including retail, banking, academia and travel were selected to present their perspectives on B2B payment challenges and opportunities. This workshop complemented the ECB’s broader experimentation efforts by identifying potential new use cases beyond the current retail focus. Also in October 2024, the ECB issued a call for expressions of interest[23] to join its innovation platform, which received over 100 applications. From these, around 70 market participants – including banks, fintechs, merchants and non-bank PSPs – were selected to explore technical and conceptual aspects of the digital euro.

The innovation platform was structured into two workstreams: “pioneers” and “visionaries.” Between February and May 2025, the pioneers focused on hands-on technical testing of conditional payments in a simulated digital euro environment. Participants tested functionalities such as reservation of funds, waterfall mechanisms and various payment flows (P2P, P2B and B2P refunds), confirming that the current design could support conditional payments while preserving privacy and scalability. In parallel, the visionaries explored scenarios focusing on how the digital euro could support and foster innovation within the broader financial ecosystem. Proposals covered a wide variety of sectors such as mobility, financial inclusion and e-commerce. This dual-track approach encouraged collaboration with market participants and helped identify both practical implementation challenges and forward-looking opportunities.

Innovation platform workstreams

The outcomes of the innovation platform highlighted:

Both workstreams underscored the digital euro’s potential to reduce the fragmentation of the payment ecosystem, unlock new business models for market participants and support pan-European interoperability. A detailed summary of the outcomes is available in the innovation platform outcome report, published on 26 September 2025. The ECB will use the findings to inform future digital euro developments.

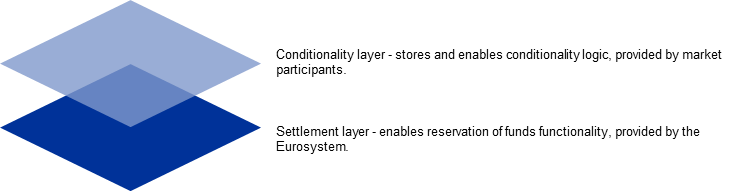

Two-layer set-up to enable conditional payments

The preparation phase included targeted technical work on the design features of a potential digital euro. The work focused on key design areas such as offline functionality, accessibility and inclusion, holding limit calibration methodology, and system architecture. The analysis was informed by user research, expert input and collaboration with market participants. It aimed to explore practical implementation aspects and support the refinement of technical specifications. These efforts have helped ensure that the digital euro is being developed with a framework that supports resilience, usability and inclusiveness across the euro area.

The offline functionality of the digital euro is being developed to enhance the accessibility and resilience of digital payments, supporting a broad spectrum of payment scenarios. It would allow users to make payments between two devices close to each other without an internet connection – for example, in areas with limited coverage, during power outages and in emergency situations. Payments would be settled directly between two devices (such as mobile phones or smart cards) by the near-instantaneous transfer of cryptographically secure tokens. The transfer would not involve any online system – a key innovation that does not yet exist in the market – and tokens would remain securely on the device. The approach taken preserves user privacy, as transaction details (e.g. what goods were bought, where and from whom) remain on the devices and are not shared with PSPs or the Eurosystem during (or after) the payment process.

Technical work has focused on enabling offline payments via card or phone through secure environments[24] (such as embedded secure elements[25] and eSIMs[26]). The ECB has explored deployment options with device manufacturers and service providers, focusing on how to enable easy and seamless user onboarding. Metrics and associated standards have been analysed to determine which secure element form factors are most likely to gain widespread adoption in consumers’ mobile devices in the future. The focus is centred on three primary options: embedded secure elements (eSEs), integrated secure elements (tamper-resistant secure enclaves, excluding Trusted Execution Environments) and embedded SIMs (eSIMs). Each of these form factors has the potential to deliver the robust security needed to meet the demanding requirements of the offline digital euro.[27]

Among these options, eSIMs are expected to gain the most traction in consumer devices thanks to their increasing adoption across a wide range of smartphones and wearables. Their ability to combine connectivity and advanced security in a compact, software-updatable form factor positions them as a leading candidate for future offline digital euro implementations. However, eSIMs must be supported by appropriate standards to ensure that offline wallets and their associated funds remain independent of the consumer’s currently selected mobile network operator subscription. All three technologies remain viable pathways to achieving the high security standards required to protect sensitive information and critical payment operations for the offline digital euro. In addition to analysing secure element availability, design challenges have been addressed such as supporting multiple front-end applications from PSPs, while ensuring offline funds remain accessible and correctly linked to the distributing PSP. Alternative form factors, such as battery-powered smart cards and bridge devices, are also being researched to see if and how they could facilitate inclusive access for users without smartphones.

Analytical findings on offline functionality have been regularly shared with European co-legislators and market stakeholders, including through technical seminars and ERPB sessions (see also Section 6. Engagement with external stakeholders).

As part of the broader technical analysis, the Eurosystem explored how the online digital euro could be supported by a resilient and privacy-preserving system architecture. A key focus was to ensure that the architecture could protect user data, maintain continuity in adverse scenarios and support reliable performance across the euro area. Strong cyber resilience is enabled by the establishment of “state-of-the-art” cybersecurity controls addressing organisational and technical areas. Special focus is placed on the areas of secure development practices, cryptographic agile implementation in response to new developments in the cryptographic domain, such as quantum computing, reduction of the attack surface, regular planned testing against simulated cyberattacks and the inclusion of strong governance structures. The design of the cybersecurity controls builds on existing proven Eurosystem practices for other market infrastructures and industry best practices.

From a privacy standpoint, the digital euro is being designed as an ecosystem with minimised data and segregated information, and with distributed and segregated processing across the individual DESP components, in which end-user identities are not visible to the Eurosystem. The digital euro end user is onboarded through a PSP which is required to adhere to existing regulations on anti-money laundering (AML) and know-your-customer (KYC) procedures, ensuring that only the necessary personal data are captured, in line with the General Data Protection Regulation (GDPR)[28]. The PSP will then send these transactions to the DESP for settlement using pseudonymous identifiers, ensuring that the ECB will not be able to connect any transaction with a private individual. Such privacy safeguards reinforce the Eurosystem’s commitment to data protection and minimisation and build on earlier design principles from a technical standpoint. The offline solution for the digital euro is designed to uphold even stricter privacy standards than the online solution, which already offers an unparalleled level of data protection. Offline payments provide enhanced user anonymity and ensure that sensitive payment information (i) remains on the device in a secure element, and (ii) is inaccessible to both the Eurosystem and PSPs.

To ensure continued functionality in adverse conditions such as digital disruptions, the architecture would include safeguards for emergency scenarios. For example, if under extreme circumstances a PSP were to lose access to the mapping[29] between its users and their respective holdings – owing to a cyberattack or technical failure – upon user request, and by providing proof of identity and passkey, a new PSP could re-establish users’ access to their holdings, without the Eurosystem knowing their identities. This would ensure that users could reclaim their funds securely and highlights the value of a public digital payment infrastructure in supporting financial resilience.

To ensure uninterrupted service, the Eurosystem would operate a central ledger in a multi-region set-up, hosted across three different regions, each equipped with multiple servers in different locations. This approach goes beyond standard redundancy models and is designed to maintain continuity even if data centres in a whole region of Europe become unavailable. In the event of a regional disaster, payments could be automatically rerouted to other regions, ensuring uninterrupted operations. As holding a digital euro would mean holding a direct liability of the central bank – as is the case with banknotes today – the Eurosystem would need to be able to correctly record (and hence also to verify) all settlements of its own liabilities. Therefore, the decision has been taken to have a centralised ledger. Unlike systems which rely on technical tools, such as resource-intensive consensus algorithms to establish trust among unknown parties, there is no need for such a set-up and the Eurosystem will leverage geographical distribution of the digital euro operations in an efficient way. Nevertheless, the technical architecture of the digital euro builds on key design principles from distributed ledger technologies (DLTs) to enhance resilience and efficiency, and to improve the system’s overall performance and reliability. This relates mainly to the geographical distribution across multiple independent sites, the decentralised execution of settlement transactions, the atomicity and immutability of transactions, and the use of a sophisticated distributed consensus mechanism. Additionally, the digital euro would benefit from state-of-the-art technologies such as sophisticated AI models with responsible frameworks. These technologies would ensure (i) explainability of the generated output to manage risk and detect fraud based on pseudonymised transaction data only, thus providing an additional layer of end-user protection to the anti-fraud measures pursued by the PSP, (ii) highly scalable distributed systems to enable the lowest possible latency, (iii) real-time processing, and (iv) advanced cryptographic protocols to ensure top-tier security and trust, and to safeguard against future threats.

To ensure cost-efficient implementation and seamless integration with existing systems, the digital euro is designed to make use of market standards for interaction between PSPs and the DESP, while employing state-of-the-art technology. Specifically, we have chosen to use a synchronous REST interface for the connection between PSPs and the back-end infrastructure. Developed with the involvement of representatives from the financial industry, it builds on standards familiar from the implementation of the revised Payment Services Directive (PSD2), with existing payment infrastructures. The REST interface enables low-latency transactions, speeds up innovation and supports the seamless settlement of transactions via balance-based data interfaces already known to PSPs, which facilitates compliance checks while allowing PSPs to maintain and further enhance smooth and intuitive user experiences. These design choices reflect a careful balance between innovation and stability, ensuring that the digital euro is both future-proof and grounded in a proven, reliable infrastructure.

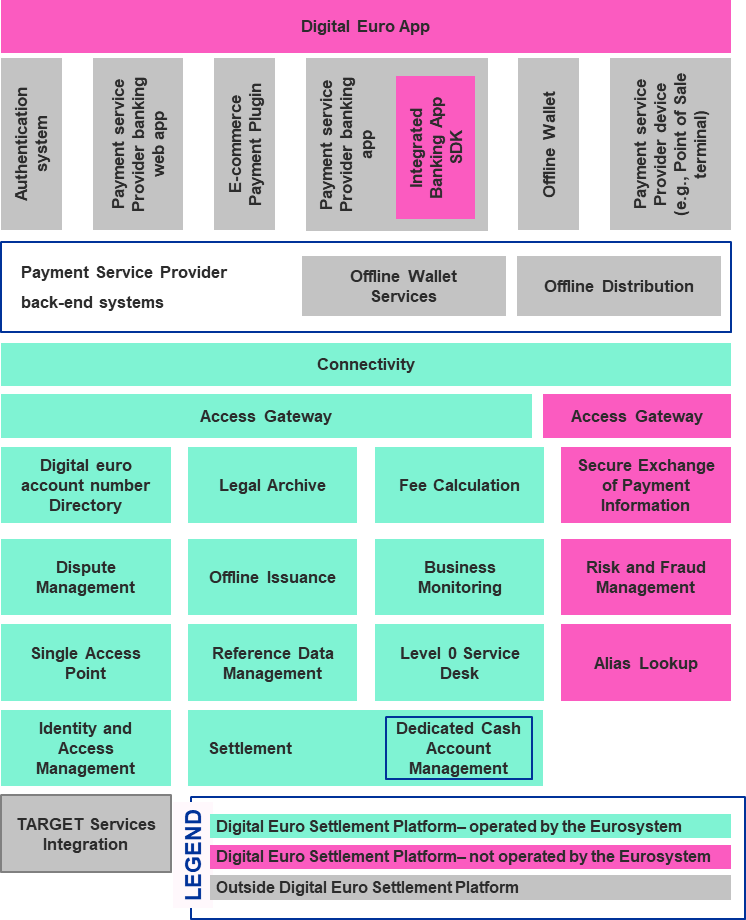

Preliminary architecture overview

The envisaged design incorporates advanced capabilities, including a state-of-the-art funds reservation functionality[30] which supports a diverse range of innovative features,[31] including conditional payments.[32] A clearly separated settlement layer in the back-end infrastructure, provided by the Eurosystem, and a conditionality layer, provided by market participants, would ensure a secure environment that preserves the privacy of end users and the integrity of the payment process, while also allowing the flexibility for external monitoring that can trigger conditions. In practice, conditional payments would allow end users to initiate payments by temporarily reserving the specified amount in their account. While the reserved amount reduces the user’s available balance, the funds are not transferred immediately. Thereby, sufficient funds remain available to complete the payment when required, enhancing reliability and efficiency in transaction processing.

In addition, specific conditions governing the release of reserved funds could be set out within a dedicated conditionality layer developed by market participants[33]. Once the applicable condition is verified, such as the confirmation of a train arrival, the reserved amount is transferred to the recipient. If the condition is not met, for instance should the train not arrive or should it arrive only with significant delay, the reservation is cancelled or allowed to expire, and the funds are returned to the payer’s available balance for future use.

Recent work by the Eurosystem, conducted in close collaboration with market participants, has confirmed that the current design of the digital euro can effectively support conditional payments. Market participants underscored the significant potential of these features to enable advanced services and drive further innovation.

The digital euro would be legal tender. Therefore, ensuring that it is accessible to all citizens and is highly usable – regardless of age, ability, or digital literacy – was a guiding principle throughout the preparation phase. The ECB has taken a comprehensive approach to inclusion, combining technical design considerations with extensive user research. An overarching accessibility strategy has been designed to underpin the development of the digital euro app. The digital euro app would comply with the European Accessibility Act.[34] Moreover, in addition to the development of a physically accessible design, a specific focus would be placed on cognitive accessibility to ensure everyone can use the digital euro app and can quickly learn how to use it.

User research (see also Section 6.1 User research) has reinforced the importance of inclusive and user-friendly design. Focus groups with vulnerable consumers highlighted the need for multiple onboarding options, including in-person support at local branches, and payment flows which resemble familiar experiences. Participants emphasised the value of reassurance, simplicity and control over personal finances, particularly for those less confident with digital tools.

In parallel, the ECB has engaged with civil society organisations (see also Section 6.5 Engaging with the public) and consumer advocacy groups to gather feedback on how the digital euro can promote financial inclusion. These dialogues will inform both the technical design and the Eurosystem’s outreach strategy, ensuring that the digital euro is not only highly usable but also understandable and relatable to all segments of society.

In September 2025, the ECB hosted a workshop with the NCB expert group on digital financial inclusion, which brings together experts from 12 NCBs. The group reviewed best practices for implementing the public approach and discussed priorities for the next phase, including defining clear use cases for inclusion, refining the value proposition and usability of the digital euro app – especially its offline mode – and exploring features such as guided tutorials and support tools for users. The workshop also emphasised the importance of communications that help people understand how to use the digital euro, with a focus on empowering those who support vulnerable groups, such as associations and public institutions. These insights will inform the next phase of work on inclusion and accessibility.

Work on accessibility and inclusion will continue in the next phase, with further developments on the app interface, the process that users would follow to start using digital euro services (onboarding flows) and the support mechanisms to help users in case of issues or need. These efforts aim to ensure that the digital euro is a truly European means of payment – one that leaves no one behind.

The Eurosystem is fully committed to ensuring that the introduction of the digital euro is consistent with a resilient financial environment that allows its monetary policy to be transmitted effectively. Individuals’ digital euro holdings would not be remunerated and would be subject to holding limits, as provided for in the Commission’s legislative proposal. These holding limits are intended not to prevent the digital euro from being a store of value altogether but rather to moderate its use in this capacity, and therefore preserve the role of banks in ensuring the efficient provision of credit to the real economy.[35]

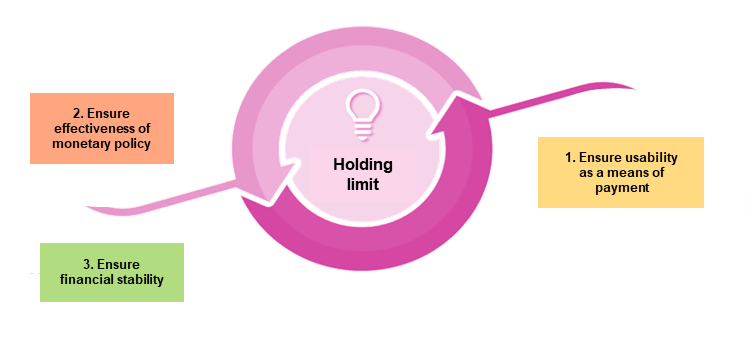

The development of the methodology for calibrating an appropriate holding limit for the digital euro has therefore been a central focus throughout the preparation phase. The approach to calibration seeks to ensure that the introduction of the digital euro aligns with a seamless payment experience for users, while ensuring that a resilient financial environment is maintained and allowing for continued effective monetary policy implementation and transmission, in accordance with Article 15(1) of the draft Regulation (Figure 5).[36]

Framework for the calibration of the digital euro holding limit based on the objectives set out in Article 15.1 of the draft Regulation on the establishment of the digital euro

Source: ECB elaboration.

During this phase, the ECB made significant progress in developing the methodology for calibrating the digital euro holding limit. Together with experts from NCBs and national competent authorities (NCAs), the ECB worked to develop a methodology for the calibration of the digital euro holding limit and engaged with market stakeholders throughout to consider a wide range of feedback.[37] Input received was directly incorporated into the methodology. The testing drew on data on retail deposits collected in collaboration with European banking supervision, as well as results from ECB research on user behaviour with respect to holding digital euro. The methodology considers the increasing digitalisation of money and payments[38], combined with a granular assessment of digital euro user preferences and bank deposit outflows.

In the context of the preparation of the methodology, the ECB commissioned a survey on user behaviour to shed light on users’ attitudes towards holding digital euro. This was carried out among a diverse and representative sample of EU citizens aged 18 and older, aiming to examine their payment attitudes and preferences[39]. A majority of respondents (66%) showed interest in trying the digital euro.[40] This information – which is broadly consistent with findings from other surveys run by the ECB and NCBs[41] – can be used to gain a better understanding of the expected take-up rate in normal times (the “business-as-usual” scenario). The survey was also used to shed light on preferences for pre-funding versus activating and using the reverse waterfall feature. Around two-thirds of respondents would prefer to pre-fund or use a combination of both options to fund their account.[42] In addition, a large majority of respondents (75%) stated that monthly expenses are an important benchmark for referencing their digital euro holdings[43], and more important than income, bank account balances or cash holdings.

In response to a formal request from co-legislators, the ECB prepared a technical analysis estimating the potential financial stability effects of different hypothetical digital euro holding limits in a range identified in the request, namely from €500 to €3,000 per individual.[44] This technical analysis involved assessing potential digital euro demand and its consequences for deposit outflows and banks’ balance sheets under two scenarios: (i) a business-as-usual scenario, expected to prevail; and (ii) a highly unlikely and extremely conservative flight-to-safety scenario, which has never occurred in the 25 years since the first issuance of the euro.[45] This analysis should be read solely as a technical response to the specific request from the co-legislators[46] (see also Section 6.3 Engaging with co-legislators), and not as the outcome of the ECB’s full methodological process nor as the ECB’s position on an appropriate level for holding limits.

The findings of the technical analysis confirmed that using the digital euro for day-to-day payments would not harm financial stability. Considering that the gradual decline in the use of banknotes for payments due to digitalisation corresponds with an increased use of deposit-based instruments, the analysis showed that no aggregate bank deposit outflows would be recorded. Even under a highly unlikely and extremely conservative scenario, given different hypothetical holding limits in the range from €500 to €3,000 per person, the impact of potential digital euro demand on banks’ deposit outflows would be manageable, and there would be no significant impact on financial stability.[47]

Overall, the analysis confirmed that holding limits can effectively restrict deposit outflows from the banking sector, safeguarding financial stability and supporting the effective formulation and implementation of monetary policy. This analysis and the numerical results presented should be read solely as a technical response to the specific request from the co-legislators, and not as the outcome of the ECB’s full methodological process nor as the ECB’s position on an appropriate level for holding limits. The estimates outlined in this analysis are illustrative and reflect an initial and partial application of the methodology being developed by the ECB, rather than an exhaustive assessment. The complete methodology encompasses three pillars (Figure 5) with additional aspects that extend beyond the scope of this analysis. Moreover, the hypothetical holding limits assessed in this analysis are based on the co-legislators’ specific requests to test a defined range. Consequently, the results presented should not, under any circumstances, be interpreted as representing the official final position of the ECB on the appropriate level of holding limits.

Throughout the preparation phase, the ECB maintained structured and continuous engagement with a broad range of external stakeholders, including market participants, EU policymakers, other central banks, civil society organisations, consumer advocacy groups and the public. By engaging with a broad range of stakeholders and conducting extensive user research, the ECB has gathered valuable feedback in shaping the design of the digital euro, ensuring that it meets stakeholders’ needs while also fostering transparency and trust in the project. The engagement activities included technical sessions, bilateral meetings, workshops and public-facing events.

To ensure the digital euro meets the needs of citizens and merchants across the euro area, the ECB conducted user research throughout the preparation phase. This work focused on understanding people’s payment preferences and behaviours to inform the design and value proposition of the digital euro. From autumn 2024 onwards, the ECB commissioned a series of quantitative and qualitative studies in all euro area countries. These activities were aimed at identifying the challenges and needs of diverse user groups in relation to payment methods and learning how a digital euro could respond to their preferences, with particular attention to vulnerable consumers[48] and small merchants[49].

In one research stream, when considering the adoption of a new payment method, vulnerable consumers highlighted the need for a universally accepted solution with an inclusive and intuitive design, as well as in-person support at local branches. Moreover, they frequently valued offline access, especially among those who personally experienced a lack of internet connectivity during travel, in rural areas or in emergency scenarios. Most vulnerable consumers expressed a preference for any new payment method to be introduced by a trusted and established bank and/or public body and indicated that they would be more likely to adopt a new payment method if it were offered by a European provider.

In another research stream, small merchants highlighted low costs, seamless integration in the existing checkout process and consumer preference as very important factors to consider in the adoption of new payment methods. Small merchants were introduced to the digital euro and were cautiously optimistic overall about its value proposition. They particularly favoured offline functionality, instant settlement and its potential to serve as a tool for negotiating better terms with their payment service providers, possibly reducing fees. The digital euro’s backing by the ECB was also spontaneously mentioned as an additional supporting factor. It was perceived as a guarantee of strong security for payments, which could increase consumer trust and potential adoption.

Vulnerable consumers and small merchants both stressed the need for a simple, reliable, and secure payment experience. Overall, the insights gained from user research will inform the ongoing design of the digital euro and how the Eurosystem can best engage with different user groups. A detailed summary of the findings is available in the Digital euro user research report, published on 30 October 2025.

During the preparation phase, the ECB actively engaged with a broad range of market stakeholders, including banks and non-bank PSPs, merchants and consumers. This engagement featured high-level meetings with merchants, attended by President Christine Lagarde and Executive Board member Piero Cipollone, as well as a technical workshop addressing merchant and consumer-specific topics. Meetings between ECB Board members and the leadership of banks and non-bank PSPs took place throughout the phase, alongside ongoing technical exchanges at expert level and meetings with consumer organisations at senior management level.

The ECB has engaged continuously with the Euro Retail Payments Board (ERPB) since the start of the investigation phase to ensure that the digital euro reflects the needs and expectations of key market stakeholders. By leveraging the expertise of all actors involved in the digital euro ecosystem, both on the supply side (such as merchants and PSPs) and on the demand side (for instance consumers), and by gathering valuable input from consumer associations, the ECB can design a digital euro that addresses the needs and preferences of its stakeholders. To this end, the ECB organised technical sessions and workshops with ERPB associations, providing a structured forum for dialogue with representatives of consumers, merchants and PSPs. These engagements covered a range of topics, including acceptance standards[50] and the calibration of the holding limit[51]. The ECB also used these sessions to present updates on experimentation activities and to gather feedback on how the digital euro could be integrated into the broader European payments landscape. A dedicated stream of ERPB technical sessions was organised to discuss market views on the digital euro’s fit in the payment ecosystem.

The digital euro aims to foster innovation and competitiveness within the European retail payments market. This objective makes the digital euro’s “fit in the payment ecosystem” a key topic for policymakers and market stakeholders alike.

Between November 2024 and April 2025, dedicated ERPB technical sessions involving PSPs, merchants and consumers were conducted around three key thematic pillars: competition, synergies and business model. Across these sessions, 29 suggested value drivers were discussed.[52] Participants’ written feedback was published on the ECB’s website, and an outcome session was conducted for each theme.

Engagement with market stakeholders on fit of the digital euro in the payment ecosystem

Notes: 1) Competition and Synergies outcome sessions were held on the same day.

2) Merchants and Consumers sessions were held on the same day.

The outcomes were consolidated in the Fit of the digital euro in the payment ecosystem report, which summarises the overall engagement, identifies potential benefits, and recommends areas for further public-private technical collaboration to maximise benefits and mitigate risks. These areas may lie fully in the remit of either the Eurosystem or the co-legislators, to which the Eurosystem will continue to provide its technical input[53].

Amongst others, several key benefits were identified by the ECB and all stakeholders. While merchants and consumers generally perceive significant advantages, provided certain requirements are met, the banking sector raised more questions regarding the benefits.

Lastly, the recommended areas for further collaboration include: (i) detailing how European schemes and the digital euro propositions will coexist and, where possible, make use of existing infrastructure and processes; (ii) launching collaborative work to ensure that the potential issuance of the digital euro is as cost-efficient as possible; and (iii) further exploring fraud risk management and offline functionality.

Throughout this project phase, the ECB has provided technical input to the co-legislators as they advanced in their discussions concerning the draft Regulation on the establishment of the digital euro. In this light, the ECB welcomes the ambition of the Economic and Financial Affairs Council (ECOFIN) to reach a Council agreement on the Single Currency Package[54]by the end of 2025 within the Danish Council Presidency. This ambition has received broad support from the EU finance ministers, as expressed during the ECOFIN meeting on 8 July 2025.[55] Such high-level political backing underscores the shared commitment across Member States to advance the legislative process and ensure the timely adoption of the digital euro, in line with Europe’s strategic priorities.

On 19 September 2025, finance ministers in the Eurogroup agreed on the governance framework around the issuance of the digital euro and the process of setting a holding limit. The President of the Eurogroup explained: “The agreement […] signals the collective determination that we have to advance this important project. Ensuring a digital future for our currency is essential for the euro.”[56] The political agreement reached among ministers facilitates further legislative process in the Council.

The ECB also maintains its support to the legislative debate in the Council at the technical level. Together with the Commission, the ECB is an observer at meetings of the Council Working Party (CWP), which discusses the digital euro legislative proposal, providing expert technical input, in accordance with the Opinion adopted by the Governing Council. Since the start of the digital euro preparation phase, the ECB has participated in 19 CWP meetings and provided four technical seminars as well as multiple presentations. Below are examples of input recently provided to the CWP.

The ECB has engaged in discussions within EU forums regarding the strategic significance of the digital euro, which was also acknowledged by the euro area heads of state or government. In parallel, the ECB also provided regular updates on the digital euro project to the euro area finance ministers at the Eurogroup.

The ECB has updated the European Parliament regarding the developments in the project throughout the preparation phase. Executive Board member Piero Cipollone took part in five public exchanges of views on the digital euro at the European Parliament’s Committee of Economic and Monetary Affairs.[57] The ECB also provided technical input to the rapporteur and shadow rapporteurs on the file, both in bilateral contacts with MEPs and, at the invitation of the rapporteur, in sessions that were open to all MEPs of the negotiating team and covered the following topics.

The ECB provided technical input to co-legislators upon their request, including a view on recent assessments of digital euro investment costs for the euro area banking sector[58], and a technical analysis on the impacts of alternative digital euro holding limits[59], based on its work on a methodology for determining the limits.

On costs, the ECB’s assessment estimates that the euro area banking sector would need to invest €4 billion to €5.8 billion in total or €1 billion to €1.44 billion annually over four years (i.e. 3.4% of significant banks’ annual IT upgrade budgets and around 0.7% of the euro area banking universe’s net income of approximately €197 billion in 2023). This range is consistent with the estimates given in the 2023 European Commission impact assessment.[60] It is comparable to the costs for initiatives such as PSD2 and below the level of investments for SEPA harmonisation. The difference reflects the ECB’s use of synergies and cost mutualisation, corrections to design and legislative assumptions, and a more realistic and efficient implementation model. The impact assessment was conducted using banking sector studies as a foundational base. On 17 July 2025, the ECB presented the ongoing work on the development of the methodology for calibrating the digital euro holding limits in a dedicated technical seminar on financial stability and the digital euro holding limits, organised by the European Parliament rapporteur for the draft Regulation on the establishment of the digital euro. Following this seminar, the ECB received a formal request from the co-legislators for technical data on the potential financial stability effects of alternative digital euro holding limits asking to quantify the potential impact of each limit on certain key indicators.[61] In response, the ECB produced a technical analysis estimating these impacts across the specified hypothetical limits (see also Section 5.4 Holding limit calibration).

The ECB has stepped up its engagement with the academic community to foster dialogue on the digital euro with those studying its potential economic, legal and technological implications. The ECB has maintained a structured dialogue with universities, research institutes and policy think tanks. It has done so by means of bilateral engagements, participation in conferences, targeted workshops at universities and dedicated research initiatives in which scholars have been invited to present their research and contribute valuable insights to the design process of the digital euro.

To further strengthen this dialogue, a call for proposals[62] on topics related to central bank digital currencies (CBDCs), digital assets, payment systems and digital capital markets was issued. Selected contributions were presented and discussed at a conference in Milan on 25 and 26 September, organised together with the Centre for Economic Policy Research (CEPR), Review of Finance and Bocconi University. The conference included a speech by Executive Board member Piero Cipollone on research and innovation. Through these efforts, the ECB aims to continue promoting transparency and informing debates within the wider research community.

Public communication activities have been a cornerstone of the digital euro preparation phase, aimed at raising awareness, addressing misinformation and building trust among European citizens and stakeholders. These efforts have focused on delivering clear, accessible, accurate and consistent information across the Eurosystem, highlighting the digital euro’s role in preserving freedom of choice, enhancing financial inclusion and strengthening Europe’s strategic autonomy. By leveraging a range of communication activities through various channels, the ECB has worked to engage diverse audiences and address their needs.

The ECB has maintained a robust public presence through high-profile speaking engagements and events. Executive Board Member Piero Cipollone and other senior ECB representatives have participated in over 60 public events each year, explaining how the digital euro complements cash, boosts innovation and strengthens resilience.

In addition to these high-level engagements, the ECB has organised online seminars targeted at specific audiences. Civil society organisations representing consumers, minorities and vulnerable groups participated in three seminars to discuss how the digital euro could improve usability, ensure access to offline payments and enhance privacy.[63] In September 2024, the ECB engaged with over 1,000 market participants in a focus session to address questions related to the design of the digital euro and its impact on the payments market. Broader outreach efforts included participation in public events such as Europe Day and Europa Open Air 2025, where the ECB engaged directly with citizens.

Digital platforms – such as the ECB website and social media – have played a vital role in disseminating updates and insights. Communications have been crafted to be clear, factual and relatable, fostering understanding across diverse audiences. The ECB actively engages with media outlets to address inaccuracies in reporting on the digital euro, ensuring that the information shared is both factual and accurate. The ECB has ensured transparency throughout the preparation phase by regularly publishing key documents and progress reports, keeping stakeholders and the public informed about the digital euro’s development and next steps.

On 23 October 2025, European leaders called for accelerated progress on the development of a digital euro. On 29 October 2025, the Governing Council of the ECB decided that the Eurosystem will continue its preparations and move to the next phase of the digital euro project. In this phase, the Eurosystem will build the necessary technical capacity ahead of a possible decision to issue, while maintaining flexibility and alignment with the legislative process.

With the next phase of the digital euro project, the ECB aims to be ready for a potential first issuance of the digital euro during 2029. This is based on a working assumption that the European co-legislators will adopt the Regulation on the establishment of the digital euro in the course of 2026. A pilot exercise and initial transactions could take place earlier, potentially starting as soon as mid-2027, to prepare for a potential issuance.

To deliver on this shared ambition, the Eurosystem will focus on three main workstreams.

Looking ahead, the Eurosystem’s preparation for a digital euro will follow a flexible and modular approach. This approach responds to calls from euro area leaders for the Eurosystem to be ready for potential issuance as soon as possible, while also recognising that the legislation has not yet been adopted. This approach allows gradual scaling and limited financial commitments while ensuring continued alignment with the legislative process. A possible decision by the Governing Council of the ECB on whether to issue a digital euro, and on what date, would only be considered after the legislative act is adopted.

The effective issuance date and the ECB Governing Council’s possible decision on whether to issue a digital euro remain subject to decision-making by EU co-legislators. The ECB will continue to closely follow the legislative debate and implement any appropriate adjustments to the development of the digital euro that may result from legislative deliberations, ensuring compliance with the legal framework in force at the time of possible issuance. The technical and legislative processes must therefore advance in parallel: the Eurosystem prepares the technical groundwork, while co-legislators lead the legislative process. Both processes are essential to ensure that, if and when the time comes, the digital euro can be made widely available as an additional option to pay digitally, complementing cash across the euro area.

© European Central Bank, 2025

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.