AHDB released its full season (2024/25) usage data for animal feed production across GB last week. Overall, feed production across the industry was down (-1.4%). However, feed demand across the UK’s cattle sector rose notably (+5%) in the 2024/25 season compared to the five-year average.

Both dairy and beef systems have seen increased feed use, albeit for slightly different reasons. Market prices, supply pressures, weather conditions, and cost structures have all contributed to this upward shift.

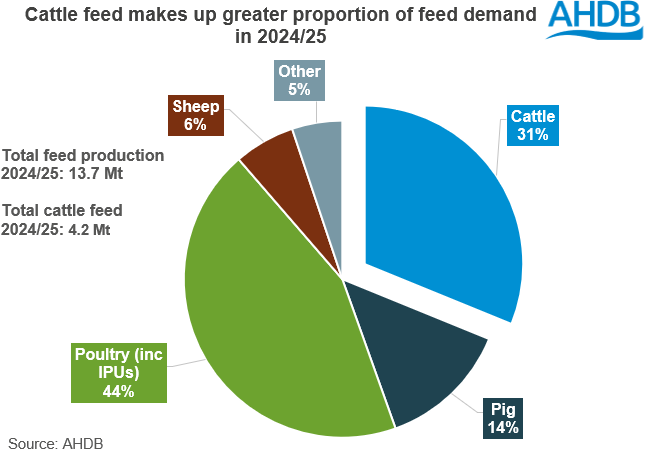

Cattle feed production made up 31% of total feed production in 2024/25. As such, looking at the key factors driving demand is important for the cereals and oilseeds sector moving into this new marketing year.

Dairy feed demand

Usage of blends for dairy cows were up 8.2% against the five-year average at 864.1 Kt for 2024/25. While compound feeds grew at 1.6% over the same period.

The milk-to-feed price ratio can be used to show how profitable it is to feed more concentrates by comparing milk value to feed cost. From July 2024 to May 2025, the milk-to-feed price ratio rose from 1.33, peaking at 1.53 in November 2024 before steadying at 1.46 in May 2025.

Compared with the five-year average of around 1.22–1.26, this shows that in the 2024/25 season, stronger margins consistently favoured higher concentrate use to drive milk output.

A persistently wet summer and autumn in 2024 for parts of the country, undermined grass growth and silage production across many UK regions, leading to earlier housing and increased supplementation between October and March; this was compounded by a historically dry spring in 2025, severely limiting grass development, further pushing feed usage higher.

Beef feed demand

Between July 2024 and June 2025, UK beef feed production increased on the year and above the five-year average, with the sharpest gains in all other cattle blends (+22%) and solid growth in all other cattle compounds (+4.8%).

AHDB’s beef market outlook forecasts UK beef production in 2025 to fall by around 4%, driven by lower prime cattle and cow slaughter. Tighter supply this season has pushed deadweight prices to record levels, peaking above 700 p/kg in May, incentivising producers to feed intensively and aim for heavier carcass weights.

The beef sector did not escape the weather either, the wet summer/autumn 2024 cut grazing and forage quality, prompting earlier housing, while a dry spring in 2025 kept feed demand high into summer.

Higher-than-expected slaughter in 2024, along with increased dairy cow retention, have reduced cattle availability. Tight supplies, strong deadweight prices and cheaper feed have driven beef finishers to feed more and maximise weight gain, explaining some of the increase in feed production we have seen.

Feed Prices

AHDB data shows the average dairy concentrate cost in May 2025 was £296/t, £12 lower than a year earlier and slightly below the five-year average of about £304/t. Together, strong margins and moderated feed costs helped sustain elevated feed usage.

At the same time, feed input costs eased, with UK November 2025 feed wheat futures falling to around £172/t (12 August 2025), compared with roughly £200/t at the same point last season, marking the lowest level for this stage in the harvest cycle in four years. Globally, cereal and oilseed futures have also declined sharply in 2024/25, driven by ample supplies and softer demand.

What next?

Overall, favourable margins, lower feed costs, and challenging weather pushed cattle feed demand well above recent norms in 2024/25. Looking ahead, if grain prices remain subdued and dairy and cattle prices stay firm, feed usage in both dairy and beef systems is likely to stay elevated. Mixed conditions in the forage season have left supplies tighter for some, which could keep reliance on purchased feed high into the next period.