Published as part of the Financial Stability Review, November 2025.

Hedge funds represent a relatively small segment of the euro area investment fund sector and comprise both AIF and UCITS hedge funds. The total assets of euro area hedge funds stood at around €660 billion in the third quarter of 2025, equivalent to roughly 3% of the investment fund sector’s total assets. In the EU, hedge funds may fall either under the Alternative Investment Fund Managers Directive (AIFMD)[1] or the Undertakings for Collective Investment in Transferable Securities (UCITS) Directive.[2] AIF hedge funds are usually marketed to wealthy investors and are predominantly held by euro area investment funds. They offer limited liquidity, by allowing redemptions only quarterly or even annually (often with advance notice), for example, and by imposing lock-up periods on initial investments. By contrast, UCITS hedge funds are more accessible to retail investors and other non-bank sectors – with euro area households and insurance corporations each holding around 15% of the shares in such funds. As these funds often allow investors to redeem shares on a high-frequency basis, the sector is more exposed to fund share redemptions during market turmoil. UCITS hedge funds account for about 30% of the overall hedge fund sector in terms of shares issued (Chart A, panel a) as well as total assets.

Chart A

UCITS hedge funds exhibit higher retail participation and use derivatives more intensively than do AIF hedge funds

|

a) Investor base and shares issued by euro area hedge funds, by fund type |

b) Euro area hedge funds’ financial leverage and gross derivatives exposure, by fund type |

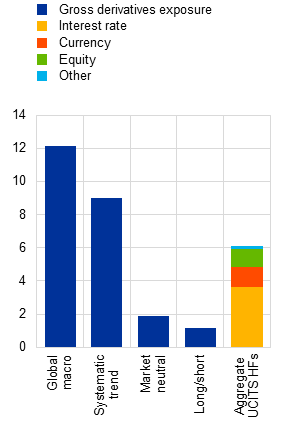

c) Gross derivatives exposures of euro area UCITS hedge funds and derivative type distribution |

|---|---|---|

|

(Q3 2025; percentages, € billions) |

(Q3 2025; total assets divided by shares issued, derivative gross notional divided by shares issued) |

(Q3 2025, derivative gross notional divided by shares issued) |

|

|

Sources: ECB (EMIR, IVF, SHS), Morningstar Direct[3] and ECB calculations.

Notes: the sample of euro area UCITS and AIF hedge funds is derived from the ECB’s investment fund list classification. AIF stands for alternative investment fund. Panel a: the investor base is proxied by information available for traded securities. The latest available information on the investor base refers to Q2 2025. For a discussion of different measures of leverage for hedge funds, see the article entitled “Leveraged investment funds: A framework for assessing risks and designing policies”, Macroprudential Bulletin, Issue 26, ECB, 2025. Panel c: hedge fund strategies follow the Morningstar Direct classification. HFs stands for hedge funds.

As UCITS hedge funds have relatively high derivatives exposure and leverage, they warrant attention from a financial stability perspective. Both UCITS and AIF hedge funds employ a wide range of investment strategies, including leveraged trades, to achieve positive absolute returns. Because of regulatory constraints on borrowings,[4] UCITS hedge funds make less use of financial leverage than AIF hedge funds do, with a total assets/equity ratio of 1.3 for UCITS hedge funds versus 1.7 for AIF hedge funds. However, synthetic leverage through derivatives is more pronounced in UCITS hedge funds, with gross notional derivatives exposure reaching up to 12 times equity for fund categories such as global macro strategies (Chart A, panels b and c).[5] In addition, UCITS hedge funds hold a lower proportion of highly liquid assets (e.g. cash and sovereign bonds) than AIF hedge funds do.[6] This leaves them more vulnerable to liquidity risk from redemption shocks or margin calls. Although some research has been carried out on the performance of UCITS hedge funds, this box sheds light on their liquidity and leverage-related risks, given their importance for financial stability.[7]

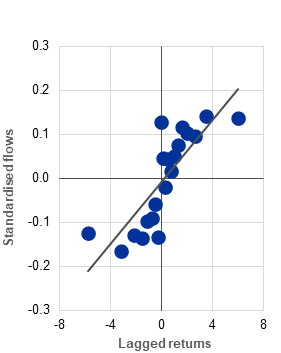

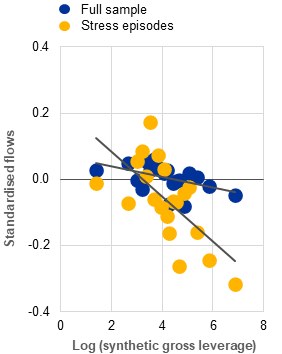

Procyclical flows and larger redemptions from leveraged funds in times of stress can lead to asset sales and mounting liquidity pressures during periods of high market volatility. Evidence from a panel of 457 UCITS hedge funds shows that their flows are procyclical, positively correlated with past returns (Chart B, panel a) and in line with the findings for other fund categories.[8] Although the analysis does not indicate that leverage generally amplifies the flow procyclicality of UCITS hedge funds, it does show larger outflows from leveraged UCITS hedge funds in periods of market stress (Chart B, panel b). Since fund share redemptions may force funds to sell assets when markets are under pressure, leveraged funds could be required to close larger positions, thereby amplifying stress.

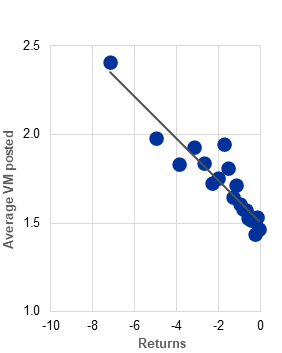

The use of derivatives by UCITS hedge funds can intensify liquidity pressures via margin calls. Derivatives positions, which can be used for hedging or for leverage, are subject to margin requirements. During periods of elevated price volatility and significantly negative returns, margin calls on these derivatives positions tend to increase (Chart B, panel c), further straining a fund’s liquidity.[9] This exacerbates the challenges faced by leveraged UCITS hedge funds, as they have to manage liquidity to meet both margin calls and redemption requests simultaneously. Interaction between these factors can heighten liquidity strains and contribute to broader market stress under adverse market conditions.[10]

Chart B

Flows into UCITS hedge funds tend to be procyclical, while margin calls may intensify liquidity risk

|

a) Average fund-level flows into euro area UCITS hedge funds, by lagged return level |

b) Average fund-level flows into euro area UCITS hedge funds, by synthetic gross leverage level |

c) Average fund-level daily posted variation margin of euro area UCITS hedge funds, by negative return level |

|---|---|---|

|

(Jan. 2019-Oct. 2025; standardised values, percentages) |

(Jan. 2019-Oct. 2025; standardised values, log of derivative gross notional as a percentage of TNA) |

(Jan. 2020-Oct. 2025; percentages of TNA, percentages) |

|

|

|

Sources: ECB (EMIR), EPFR Global, Morningstar Direct[11] and ECB calculations.

Notes: Panel a: the sample is based on funds that have been classified as UCITS hedge funds in the ECB’s investment fund list since 2009, to limit survivorship bias. The analysis is restricted to funds pursuing major hedge fund-like strategies, as classified by Morningstar Direct, and which have substantial representation in the sample. These strategies include global macro, systematic trend, options trading, market neutral and long/short strategies. Fund-level returns are calculated by aggregating the returns for each fund’s share classes, weighted by the total net assets (TNA) of each share class. Fund-level flows and TNA are obtained by aggregating the corresponding values across all the share classes within each fund. Flows are expressed as percentages of TNA and standardised to remove trends from the data. Panel b: stress episodes are defined as months in which the VIX exceeds the 90th percentile of our sample. Synthetic leverage is proxied by the gross notional value of derivatives excluding interest rate and FX contracts, which are extensively used for hedging, as a share of fund-level TNA. Panel c: average posted variation margin (VM) is calculated as the mean of fund-level daily margin amounts posted as percentages of fund TNA.

A robust stress-testing framework for leveraged UCITS hedge funds is essential to ensure their resilience and limit the risks to financial stability in turbulent market conditions. The combination of outflows and margin calls on derivatives positions can intensify liquidity pressures for UCITS hedge funds during periods of stress. This raises concerns about the ability of such funds to manage the challenges and contributes to broader financial instability. These dynamics highlight the need for strengthened risk management and comprehensive stress-testing practices to safeguard financial stability during episodes of market turmoil.

Finally, authorities should be equipped with suitable tools to limit excessive leverage in UCITS hedge funds and mitigate the build-up of risks during periods of market stress. While authorities have tools that enable them to contain excessive leverage in AIFMD-compliant funds, they do not have such tools for UCITS hedge funds. The Eurosystem suggests introducing discretionary powers that would allow authorities to impose stricter leverage limits on these funds when they pose risks to financial stability.[12] It also recommends that all UCITS hedge funds should be required to report their leverage using the commitment approach.