Stuart Morrison, Research Manager, British chambers of Commerce

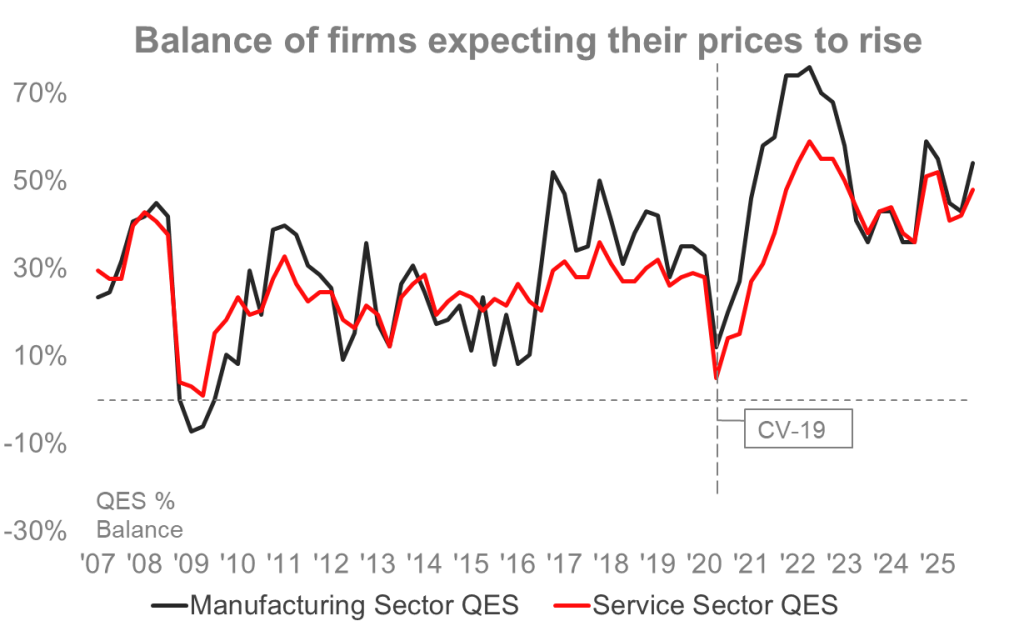

The latest Quarterly Economic Survey (QES)[1] from the BCC’s Insights Unit once again highlights price pressures as a central concern for UK businesses. Just over half (52%) of firms report that they expect to raise prices over the coming months, reflecting ongoing cost challenges. While the QES is not designed as a formal inflation forecast, its price expectations measure has, over time, proved to be a useful barometer of inflationary pressure in the wider economy.

To understand what the Q4 2025 results are telling us, it helps to place them in a longer-run context.

What the QES price expectations measure captures

Each quarter, the QES asks firms whether they expect to increase, decrease, or hold prices over the next three months. The results are usually presented as the proportion (or net balance) of businesses expecting price rises. This is a forward-looking indicator, rooted in firms’ own assessments of costs, margins, and market conditions.

Crucially, the measure reflects intentions, not outcomes. Businesses may plan to raise prices but later adjust those plans in response to weak demand or competitive pressure. For that reason, QES price expectations should be read as a signal of inflationary momentum, not a point forecast for CPI.

A historic perspective

Looking back over the decades of QES data, a clear pattern emerges. Periods when a large share of firms report plans to raise prices have tended to coincide with, or slightly precede, periods of elevated UK inflation. Conversely, when price expectations in the QES have eased, official inflation has usually followed suit with a lag.

This relationship has been especially visible since the pandemic. As supply chains tightened, energy prices surged, and labour costs rose, QES price expectations climbed to historically high levels. In Q2 2022, 65% of QES respondents said that they expected their prices to rise. By October of that year, CPI inflation had peaked at 11.1%. When those pressures began to unwind, the proportion of firms planning price increases also fell, broadly tracking the disinflation seen in official data.

Source: BCC QES Q4 2025

The link is not mechanical or perfectly timed. Inflation is shaped by many forces beyond business pricing plans, including global energy markets, exchange rates, fiscal policy, and monetary conditions. But the direction of travel in the QES has consistently aligned with the direction of travel in inflation.

What makes the QES a useful indicator

The strength of the QES lies in its timeliness and breadth. It captures real-time intelligence from thousands of firms across sectors and regions, often well before official statistics are available. For policymakers, analysts, and businesses, this provides early insight into whether price pressures are building or easing on the ground.

At the same time, history shows why caution is warranted. QES price expectations tend to be better at signalling whether inflationary pressure is present than at predicting how high inflation will go or how quickly it will fall. In periods of weak demand, firms’ ability to pass on costs can be constrained, even when cost pressures are intense.

Interpreting the Q4 results

Against this backdrop, the Q4 QES results suggest that inflationary pressure remains embedded in the business environment. While expectations are below the peaks seen during the height of the inflation surge, they remain elevated by historical standards. This points to ongoing cost-push pressures, particularly from labour, energy, and regulatory costs, rather than a renewed acceleration in demand.

As we move into 2026, the central question is likely to be whether businesses can absorb these persistent costs without passing them on. If not, inflation could remain a defining feature of the UK economy.

The historic relationship between QES price expectations and official inflation suggests that this persistence matters. Elevated expectations tend to be consistent with inflation remaining above target for longer, even if headline rates continue to ease gradually.

What this means for inflation in 2026

The lesson from the past decade is not that the QES “predicts” inflation, but that it offers an early and reliable signal of inflationary stress within the business community. The Q4 results reinforce the view that, while inflation has come down from its highs, the journey back to more stable price growth is unlikely to be smooth.

Looking ahead, persistently elevated price expectations have important implications for the policy and economic outlook. For the Bank of England, they suggest a case for caution on the pace of interest rate cuts, even as headline inflation continues to ease. If firms still expect to raise prices, underlying inflationary pressure may prove more stubborn than recent data alone imply.

For policymakers, this underlines the importance of tackling the structural drivers of costs facing firms. For businesses, it highlights a trading environment where pricing decisions remain difficult, margins remain under pressure, and uncertainty persists.

As ever, the QES provides a timely snapshot of these realities, and a reminder that inflation is not shaped by nebulous statistics, but by the decisions businesses are faced with every day.

Further reading

QES Q4 2025: https://www.britishchambers.org.uk/news/2026/01/more-clouds-gathering-over-business-confidence/

BCC Insights Unit publications: https://www.britishchambers.org.uk/insights-unit/publications-and-commentary

[1] https://www.britishchambers.org.uk/news/2026/01/more-clouds-gathering-over-business-confidence/