Airbus A320neo Production Ramps Up, While 737 MAX Output Holds Steady /// 787 Production Continues to Post Strong Results

Boeing 787 – Image – Boeing

For the purposes of this article, Forecast International considers an aircraft to be “produced” once it completes its first test flight, and “delivered” when it is contractually handed over to the customer.

Overview

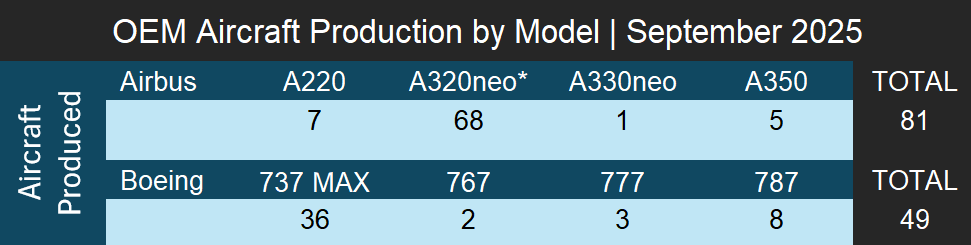

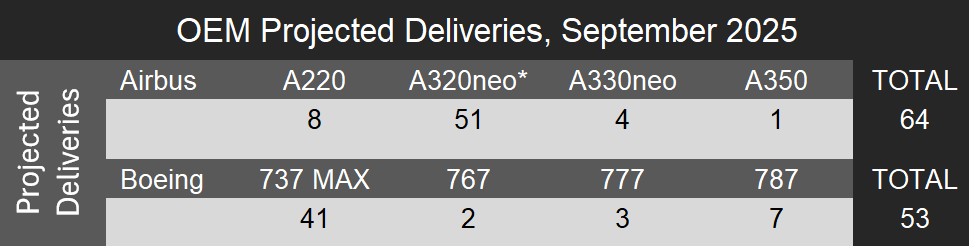

Airbus led the month in total production, completing 81 aircraft, followed by Boeing with 49, resulting in a combined total of 130 aircraft. Of these, 113 were narrowbody aircraft, while the remaining 17 were widebodies. On the delivery side, Forecast International expects Boeing to have delivered a total of 53 aircraft in September, including 41 737 MAXs with the remaining 12 aircraft to be widebodies. For Airbus, we estimate total deliveries of 64 aircraft, comprising 59 narrowbodies and five widebodies. 51 of the narrowbodies are expected to be A320neo family aircraft, and the remaining eight are expected to be of the A220 family.

Notes:

- Production data represents the actual number of aircraft produced in September 2025. Forecast International considers an aircraft produced upon its first flight. This may differ from an OEM’s definition of produced.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

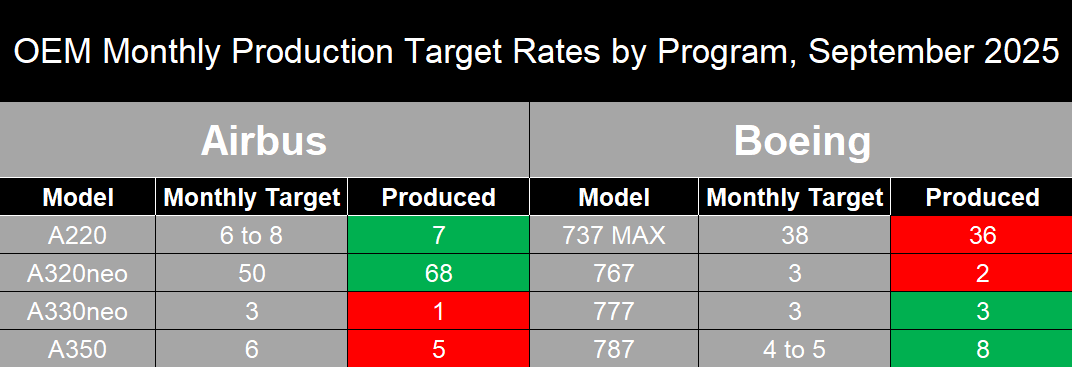

A320neo family production dipped to 38 aircraft in the month of August, but significantly rebounded in Septmeber, with Airbus producing a total of 68 aircraft in the family. Though this is above the program’s 50 aircraft per month target, this is only the third month in 2025 in which Airbus has been able to meet or exceed this target rate for the aircraft. The company also produced seven A220s during the month. On the widebody front, Airbus completed one A330neo and five A350s. Boeing’s September production was dominated by the 737 MAX, with 36 units completed, along with two 767s, three 777s, and eight 787 Dreamliners.

- Monthly production targets are generalized figures based on monthly production estimates derived from OEM guidance and internal research conducted by Forecast International.

The A320neo continues to shoulder the bulk of Airbus’s effort to reach its 2025 delivery target of 820 aircraft. Meanwhile, the A220 remains well below its goal of achieving a rate of 14 aircraft per month by 2026, and the A350 has endured a disappointing year in terms of production. Despite a notable increase in A320neo family output in September, Forecast International believes that even a rate of 68 aircraft per month is still insufficient for Airbus to meet its delivery objectives for 2025. Based on our delivery estimates for September 2025, Airbus would have delivered approximately 498 aircraft through September 30th. Given current production rates for the A220, A350, and A330neo, which are not expected to rise significantly before year-end, Airbus would need to produce and deliver an average of roughly 90 A320neo family aircraft per month during the final three months of the year.

We are not suggesting this is impossible, but it clearly represents a formidable challenge. For context, in 2024 Airbus delivered nearly the same number of aircraft through September 30 (497) toward a goal of 770 aircraft, ultimately falling just short with 766 deliveries by year-end. The clock is ticking, and the ramp-up required in the final months of 2025 will need to be even steeper than last year’s, which will depend largely on Airbus’s ability to further accelerate A320neo family production.

As mentioned, A350 production remains subdued, with Airbus producing five aircraft in September, below the current target of six per month. The program has struggled throughout the year and has shown no signs of stabilizing, even at the six-per-month rate. In 2025, Airbus has produced an average of just over four A350s per month, for a total of 40 aircraft so far this year. This shortfall comes despite ambitious plans announced at the beginning of the year to ramp up output to 10 aircraft per month by 2026 and 12 per month by 2028. Forecast International maintains the view that to make meaningful progress toward these goals, Airbus must first achieve consistent production at the current six-per-month target.

The A330neo also experienced a soft month in September, with Airbus producing only one A330-900neo. However, the manufacturer plans to raise the program’s production rate target from three aircraft per month to five per month by 2029. Forecast International considers this rate both viable and sustainable given the aging A330ceo fleet and the approaching replacement window for many operators. We expect a significant number of current A330ceo operators to select the A330neo as a replacement for the A330ceo, which should generate additional orders and support higher production volumes for the program.

737 MAX production continues to remain stable in the range of 36 to 38 aircraft per month. In September, Boeing produced 36 737 MAXs, all of which were 737 MAX 8 and MAX 8-200 variants. We expect production of the 737 MAX 9 to remain limited due to weak demand and a dwindling backlog. Order activity for the variant has been limited in recent years, and the MAX 9 currently accounts for less than 4 percent of the total 737 MAX backlog. It is also possible that some operators may choose to convert existing MAX 9 orders to the MAX 10, reflecting the industry’s broader trend towards a preference for higher-capacity variants. Additionally, certification of the MAX 7 and MAX 10 has now been pushed into 2026 as Boeing continues to address challenges with the LEAP-1B engine’s de-icing system. It remains uncertain when deliveries of either model will begin, given the limited progress made on resolving the engine issue.

As for widebodies, the 787 program continues to show strong performance in terms of production. In September, Boeing produced eight 787s, exceeding its current target of four to five aircraft per month. This represents a positive indicator toward achieving the company’s goal of 10 aircraft per month by 2026, as Boeing has demonstrated the ability to maintain stable production at around seven aircraft per month in recent months. There are also reports suggesting that Boeing may target a long-term rate of up to 16 aircraft per month by the 2030s, an increase from its earlier goal of 12 per month, driven by robust order activity and sustained demand for long-haul widebodies.

Regarding Boeing’s other widebody programs, the manufacturer produced one 767-300F, one 767-2C, and three 777Fs in September. Forecast International does not anticipate any rate increases for these programs in the near term. Production of the 767-300F is scheduled to conclude in 2027, while the 777-8 Freighter is not expected to enter service until later in the decade. The 777X program remains in the certification process, and Boeing has delayed the first delivery to Lufthansa into 2027, pushing it back from the previously planned 2026 timeline.

Another notable development for Boeing is the FAA’s decision to reinstate partial certification authority following a comprehensive safety review. This allows the company to once again issue airworthiness certificates for certain 737 MAX and 787 aircraft. Under the new arrangement, Boeing and the FAA will alternate weekly in granting certifications, while federal inspectors maintain close oversight of production lines. Forecast International views this as an important but limited milestone for Boeing. Although the change could improve delivery efficiency by reducing delays associated with FAA certification processing, it is not expected to materially increase overall production rates, as the 737 MAX program still remains subject to the FAA-imposed rate cap of 38 aircraft per month.

Unofficial/Preliminary Deliveries

Forecast International expects Boeing to have delivered an estimated 53 aircraft in the month of September 2025. The 41 narrowbodies expected to be delivered account for 38 737 MAX 8s and three 737 MAX 9s. On the widebody side, Forecast International expects Boeing to deliver an estimated seven 787s; six 787-9s and one 787-10. We also expect Boeing to have delivered three 777Fs and two 767-300Fs.

- Delivery data is the expected number that Boeing and Airbus will report in their September 2025 Orders and Deliveries summary and is based on Forecast International’s internal research. Numbers are not official and are not provided by Airbus or Boeing.

- A320neo numbers include all variants for the family; A319neo, A320neo and A321neo

As for Airbus, we expect the manufacturer to have delivered a total of 64 aircraft in September 2025. As for the A220 specifically, Forecast International expects one A220-100 delivery and seven A220-300 deliveries. The majority of narrowbody deliveries are expected to be from the A320neo Family, with one A319neo, 14 A320neos and 36 A321neos deliveries, or a total of 51 for the A320neo family. For widebodies we expect a total of one A350-900, and four A330-900neos to have been delivered.

With diverse experience in the commercial aviation industry, Grant joins Forecast International as the Lead Analyst for Commercial Aerospace. He began his career at the Boeing Company, where he worked as a geospatial analyst, designing and building aeronautical navigation charts for Department of Defense flight operations.

Grant then joined a boutique global aviation consulting firm that focused on the aviation finance and leasing industry. In this role he conducted valuations and market analysis of commercial aircraft and engines for banks, private equity firms, lessors and airlines for the purposes of trading, collateralizing and securitizing commercial aviation assets.

Grant has a deep passion for the aviation industry and is also a pilot. He holds his Commercial Pilots License and Instrument Rating in addition to being a FAA Certified Flight Instructor.

Related