Danish renewable power developer Ørsted has successfully raised DKK60 billion (US$9.4 billion) through a rights issue, where current stockholders are given the right to purchase additional shares in the company. Ørsted announced on 6 October that shareholders had subscribed to 99.3% of the new shares at DKK66.6 per share as part of the fully underwritten offering.

Ørsted is a world leader in offshore wind, with 18.5 gigawatts (GW) of installed renewables capacity, primarily in Europe.

Ørsted decided to raise equity to help withstand the highly challenging and uncertain regulatory environment in the US, where the Trump administration has sought to cancel offshore wind projects, including projects close to completion. Ørsted has major projects underway in the US, including Sunrise Wind off the coast of New York and Revolution Wind off the coast of Rhode Island. Two-thirds of the proceeds from the rights issue will fund the construction of the 924-megawatt Sunrise Wind project, closing the gap caused by the company’s inability to sell a stake in Sunrise Wind or complete non-recourse financing for the project due to political uncertainties.

Meanwhile, on 22 August, the US federal government ordered Ørsted to stop work on the 80% complete 704-megawatt Revolution Wind project. However, a subsequent court ruling on 22 September allowed the project to resume, and it is unclear whether that case will be appealed.

The expected completion of the equity issuance demonstrates Ørsted’s financial discipline and its support from shareholders, in IEEFA’s view. While dilutive in shareholder value, the large share capital raise supports the company’s credit profile. This provides a financial buffer to deliver on its pipeline of other committed projects in the UK, Poland, Taiwan and Germany, which in turn underpins its guidance of earnings growth and cash flow visibility.

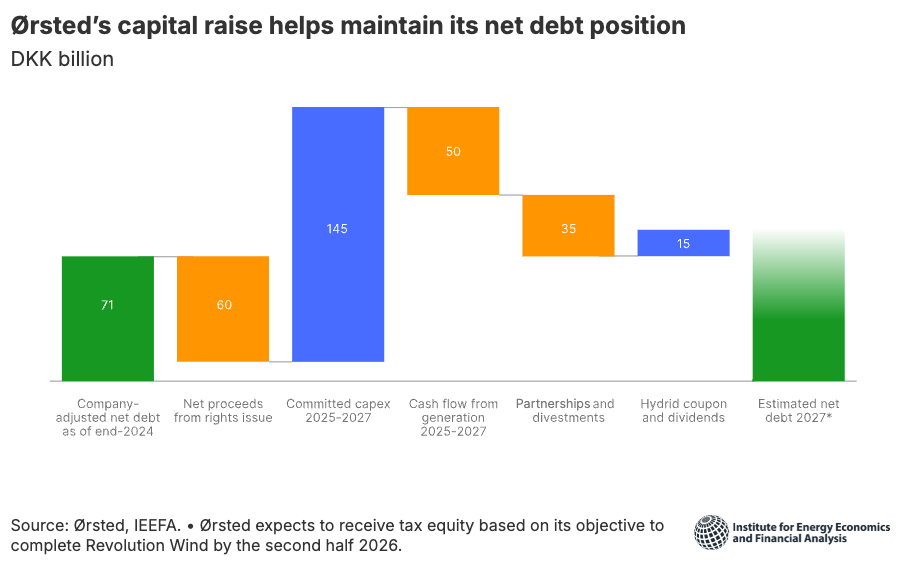

Post-transaction, Ørsted’s net debt position will improve to DKK19 billion, from DKK78 billion as of June 2025. This should help the company navigate the risks of any cash flow impacts arising from project cost overruns, cancellations and delays. The company maintains investment-grade credit ratings from all three major credit rating agencies, and its actions indicate that it remains committed to preserving them. Ørsted’s clear financial policy of maintaining its funds from operations to net debt ratio above 30% underpins this commitment. However, retaining a solid financial position will also rely on the successful execution of its sell-down plans.

Ørsted’s increased debt headroom may help support financial and environmental returns for its green bond investors, despite short-term operational setbacks. The equity raise accounts for around 60% of the company’s gross debt and hybrid instruments of DKK104 billion as of June 2025, of which the majority are green labelled.

Ørsted’s long-term fundamentals appear to remain intact. Its assets are backed by long-term agreements and benefit from Europe’s commitments to renewable power systems and secular trends of electrification and declining gas demand. EU countries target 88GW of offshore wind capacity by 2030 and 360GW by 2050.

The company’s largest single market is the UK, which aims to generate at least 95% of its electricity from clean sources and have 43-50GW of offshore wind by 2030. Ørsted’s 2.9GW Hornsea 3 project off the east coast of the UK is progressing as planned, with a 50% stake expected to be divested to raise funds. The company said it will be the world’s largest offshore wind farm upon completion in 2027.

_0.png)