22 July 2025

- Credit standards for firm loans remained broadly unchanged

- Credit standards tightened slightly for housing loans and more markedly for consumer credit

- Housing loan demand continued to increase strongly, while demand for firm loans remained weak

According to the July 2025 bank lending survey (BLS), euro area banks reported broadly unchanged credit standards – banks’ internal guidelines or loan approval criteria – for loans or credit lines to enterprises in the second quarter of 2025 (net percentage of banks of -1%; Chart 1). Banks also reported a slight net tightening of credit standards for loans to households for house purchase (net percentage of 2%) and a more pronounced net tightening for consumer credit and other lending to households (net percentage of 11%). For credit standards on loans to firms, the net percentage was smaller than banks had expected in the previous survey (a net tightening of 5%) and follows the small net tightening in credit standards seen in the first quarter (3%). Perceived risks related to the economic outlook continued to contribute to a tightening of credit standards, whereas competition had an easing impact. For the most part, banks reported no specific additional tightening impact on their credit standards related to geopolitical uncertainty and trade tensions, although they intensified their monitoring of the most exposed sectors and firms. For loans to households for house purchase, the net tightening followed the easing of credit standards seen in the first quarter (-7%) but was lower than banks anticipated (7%). For both housing loans and consumer credit, changes in risk perceptions and the risk tolerance of banks were the main drivers of the net tightening of credit standards. For the third quarter of 2025, banks expect credit standards to remain unchanged for firms (0%), ease slightly for housing loans (-3%) and tighten further for consumer credit (4%).

Banks’ overall terms and conditions – the actual terms and conditions agreed in loan contracts – eased for loans to firms, remained unchanged for housing loans and tightened for consumer credit.

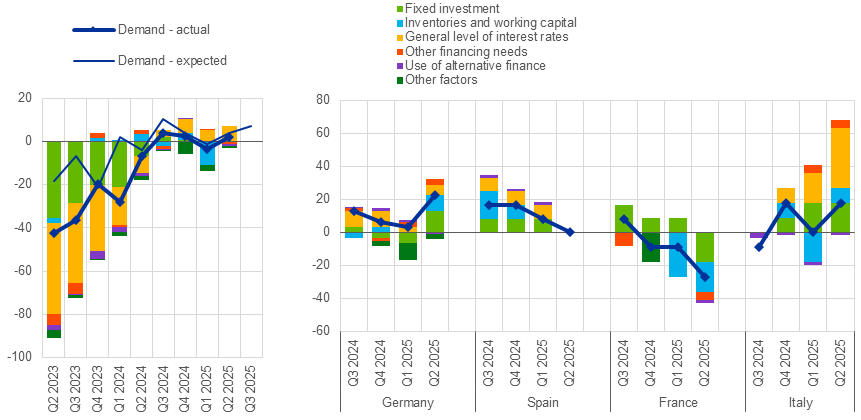

In the second quarter of 2025, euro area banks reported a slight net increase in demand for loans or credit lines to firms (Chart 2), with demand remaining weak overall. This followed a small net decrease in loan demand in the previous quarter (-3%) and was broadly in line with banks’ expectations in that quarter (4%). Loan demand was supported by declining interest rates, but dampened by global uncertainty and trade tensions, while the impact of fixed investment and inventories and working capital was neutral. Demand for housing loans continued to increase substantially in net terms. Declining interest rates, improved housing market prospects and, to a lesser extent, consumer confidence, were the main drivers of the continued increase in housing loan demand. Demand for consumer credit and other lending to households increased only slightly, with declining interest rates and other factors offsetting negative contributions from lower consumer confidence and spending on durable goods. In the third quarter of 2025, banks expect a net increase in loan demand from firms (net percentage of 7%), a further substantial net increase for housing loans (net percentage of 21%) and broadly unchanged demand for consumer credit (1%).

Euro area banks’ access to retail and wholesale funding improved slightly in the second quarter of 2025, driven by short-term retail funding, money markets and debt securities, and remained broadly unchanged for securitisations. Over the next three months, banks expect access to these funding sources to remain broadly unchanged.

Euro area banks reported that non-performing loan (NPL) ratios and other credit quality indicators had a net tightening impact on their credit standards across all loan categories, as well as a net tightening impact on terms and conditions for loans to firms and consumer credit. Banks expect these trends to continue in the third quarter for loans to firms and consumer credit, driven mostly by pressures related to supervisory or regulatory requirements.

Changes in credit standards and loan demand were heterogeneous across the main economic sectors in the first half of 2025. Credit standards tightened in commercial real estate (CRE), manufacturing, wholesale and retail trade and, to a lesser extent, in construction, while they eased slightly across most services (excluding financial services and real estate) and in residential real estate (RRE). Banks reported a net decrease in loan demand for construction, manufacturing, CRE and wholesale and retail trade, and net increases in RRE and in the transport, accommodation and food services sectors. For the second half of 2025, in most of the main economic sectors, banks expect either broadly unchanged or easier credit standards and overall small changes in loan demand. The exception is RRE, for which banks expect a further moderate increase.

Banks continue to take firms’ climate performance into consideration in their lending policies, reporting an easing impact on credit standards and terms and conditions for green firms and firms in transition and a tightening impact for high-emitting firms over the past twelve months. Both physical risk and firms’ transition risk had a moderate net tightening impact on banks’ lending policies, while climate-related fiscal support continued to have an easing impact. Banks also reported a net increase in demand for loans to green firms and firms in transition owing to climate change, while uncertainty over future climate regulation was perceived as an obstacle. Banks expect a similar impact overall over the next twelve months.

Based on a new question on the impact of climate change on housing loans, banks reported an easing impact on credit standards for buildings with high energy performance and a tightening impact for buildings with low energy performance over the past twelve months. They expect a broadly corresponding impact over the next twelve months. As the easing impact for new buildings mostly offset the tightening impact for old buildings, the net impact of energy performance was low overall. The physical risk of real estate was, however, an important driver of further net tightening in lending conditions overall, and an even higher net percentage of banks reported that it will be a driver over the next year. Banks also reported a positive impact on loan demand for buildings with high and medium energy performance but a negative impact for those with low energy performance. Investment in energy performance was the key factor for climate-related loan demand, supported by preferential lending rates for increasing sustainability, whereas uncertainty over future climate regulation was reported as a dampening factor for loan demand.

Banks indicated that changes in excess liquidity held with the Eurosystem in the first half of 2025 had a neutral impact on bank lending conditions. They expect to see similar effects in the second half of 2025.

The quarterly BLS was developed by the Eurosystem to improve its understanding of bank lending behaviour in the euro area. The results reported in the July 2025 survey relate to changes observed in the second quarter of 2025 and changes expected in the third quarter of 2025, unless otherwise indicated. The July 2025 survey round was conducted between 13 June and 1 July 2025. A total of 155 banks were surveyed in this round, with a response rate of 100%.

Chart 1

Changes in credit standards for loans or credit lines to enterprises, and contributing factors

(net percentages of banks reporting a tightening of credit standards, and contributing factors)

Source: ECB (BLS).

Notes: Net percentages are defined as the difference between the sum of the percentages of banks responding “tightened considerably” and “tightened somewhat” and the sum of the percentages of banks responding “eased somewhat” and “eased considerably”. The net percentages for “Other factors” refer to an average of the further factors which were mentioned by banks as having contributed to changes in credit standards. Data are for the euro area and for the largest four euro area countries.

Chart 2

Changes in demand for loans or credit lines to enterprises, and contributing factors

(net percentages of banks reporting an increase in demand, and contributing factors)

Source: ECB (BLS). Notes: Net percentages for the questions on demand for loans are defined as the difference between the sum of the percentages of banks responding “increased considerably” and “increased somewhat” and the sum of the percentages of banks responding “decreased somewhat” and “decreased considerably”. The net percentages for “Other factors” refer to an average of the further factors which were mentioned by banks as having contributed to changes in loan demand. Data are for the euro area and for the largest four euro area countries.

For media queries, please contact William Lelieveldt, tel.: +49 170 227 9090.

Notes

- A report on this survey round is available on the ECB’s website, along with a copy of the questionnaire, a glossary of BLS terms and a BLS user guide with information on the BLS series keys.

- The euro area and national data series are available on the ECB’s website via the ECB Data Portal. National results, as published by the respective national central banks, can be obtained via the ECB’s website.

- For more detailed information on the BLS, see Köhler-Ulbrich, P., Dimou, M., Ferrante, L. and Parle, C., “Happy anniversary, BLS – 20 years of the euro area bank lending survey”, Economic Bulletin, Issue 7, ECB, 2023, and Huennekes, F. and Köhler-Ulbrich, P., “What information does the euro area bank lending survey provide on future loan developments?”, Economic Bulletin, Issue 8, ECB, 2022.