Imagine being unable to get a loan, pay an urgent medical bill or secure your new family home with a rental down-payment. Why? All because you lack access to the kind of modern-day financial tools which much of the developed world takes for granted.

You are, to use that quietly damning word, unbanked.

Financial exclusion isn’t confined to the world’s poorest people. It is widespread. It is overlooked. And it is a notoriously difficult trap from which to escape.

Altogether, around a quarter of the world’s adult population – an estimated 1.4 billion people – do not have access to a bank account or appropriate alternative such as a building society or credit union.[1] A further half of adults qualify as ‘underbanked’, relying solely on cash and lacking any avenues of credit.[2]

In today’s hyper-connected world, breaking out of the poverty cycle means having digital access to your finances. Likewise, it demands access to the suite of systems many of us in mature markets already use to receive wages, pay invoices, source credit cards, earn interest, and insure our homes and businesses.

In the absence of these facilities, those affected are likely to endure a form of second-class citizenhood.

Financial exclusion is particularly pernicious because it often leads to inequality and injustice. Of those 1.4 billion financially excluded adults, around 80% live in emerging markets on the frontline of the existential battle against climate change.[3] Already these societies are facing an uncertain future and struggling to implement long-term plans as climate disasters such as floods, droughts and heatwaves derail economic development. Green energy, climate-proof infrastructure and sustainable farming are the solutions – yet all remain beyond the reach of communities marooned in an era of physical currency and 20th Century technology.

Financial inclusion is not simply about convenience – it is about livelihoods and lives. Indeed, financial inclusion is deemed necessary for satisfying at least seven of the United Nations’ 17 Sustainable Development Goals to ensure ‘peace and prosperity for people and the planet’.[4]

Only a fairer and more equitable system of financial access can narrow the opportunity gap worldwide.

How is technology turning the tide for world’s unbanked?

The financial symptoms of a digitally-divided world are detectable everywhere. While savings have increased globally over the past decade, the gap between prosperous and struggling economies is as profound as ever. Mature markets have an average savings rate (the proportion of disposable income set aside rather than instantly spent) of 58% compared to just 25% in developing markets.[5]

In lower and middle income countries (LMICs), there is ample evidence that financial exclusion is limiting business growth. Globally, it remains far easier to borrow money in an advanced economy (where 56% of enterprises are eligible for a loan) compared to emerging economies (23%).[6] Of the approximately 400 million micro-enterprises in developing regions, up to 345 million are classed as informal: Having no employees other than the owner, generating only subsistence-level incomes, and unlikely to be registered for tax therefore failing to elevate national GDPs.[7]

These pen-and-paper businesses cannot grow, advertise or diversify in the way their rivals might in developed markets. Nor can they strengthen their resilience by saving funds to survive fallow periods. In particular, research has highlighted a US$ 173 billion finance shortfall for female-led micro-enterprises in LMICs.

However, other indicators are suggesting a gradual change in momentum. While it is little comfort to the 1.4 billion worldwide who remain unbanked, fewer people are excluded from the financial apparatus with each passing year. In 2011, some 2.5 million adults were forced to live hand-to-mouth, day-to-day, without a bank account – far exceeding the number who find themselves in a similar predicament today.[8]

Similarly, the gender gap between the banked and unbanked is slowly narrowing. In developing countries, around 9% more men than women possessed a bank account in 2017. By 2021 this gulf had narrowed to 6%, indicating positive steps towards female independence.

Forward-thinking governments are taking a more proactive approach to increasing financial inclusion. More than 60 countries have launched national financial inclusion strategies with input from multiple stakeholders spanning telecoms, the environment, education and financial regulation.

In India, for instance, the Aadhaar scheme has equipped 1.2 billion workers with Universal Digital Identification, allowing salaries to be paid into formal bank accounts. In Mexico, the National Council for Financial Inclusion is encouraging digital adoption by increasing the number of ATMs and point-of-sale terminals throughout the country.

As a major intergovernmental organization the World Bank also runs more than 100 schemes worldwide to promote financial inclusion. These funnel cash towards agricultural resilience, social security, energy access and climate mitigation. In 2024 the World Bank contributed to 6.8 million small businesses (around half of them women-led) needing financial services. One project in Africa, for example, mobilized green private capital to help SMEs on their clean energy journey.

By bolstering economic growth and boosting productivity, financial inclusion is a goal worth striving for. Progress in the sector is chiefly credited to our ubiquitous modern-day savior: Technology.

How are smartphones leading the fintech revolution?

Why have the numbers of unbanked individuals fallen, and why are we optimistic that the world will continue welcoming new members into the global financial community? One of the most significant reasons is probably nestled right now in your hand or pocket.

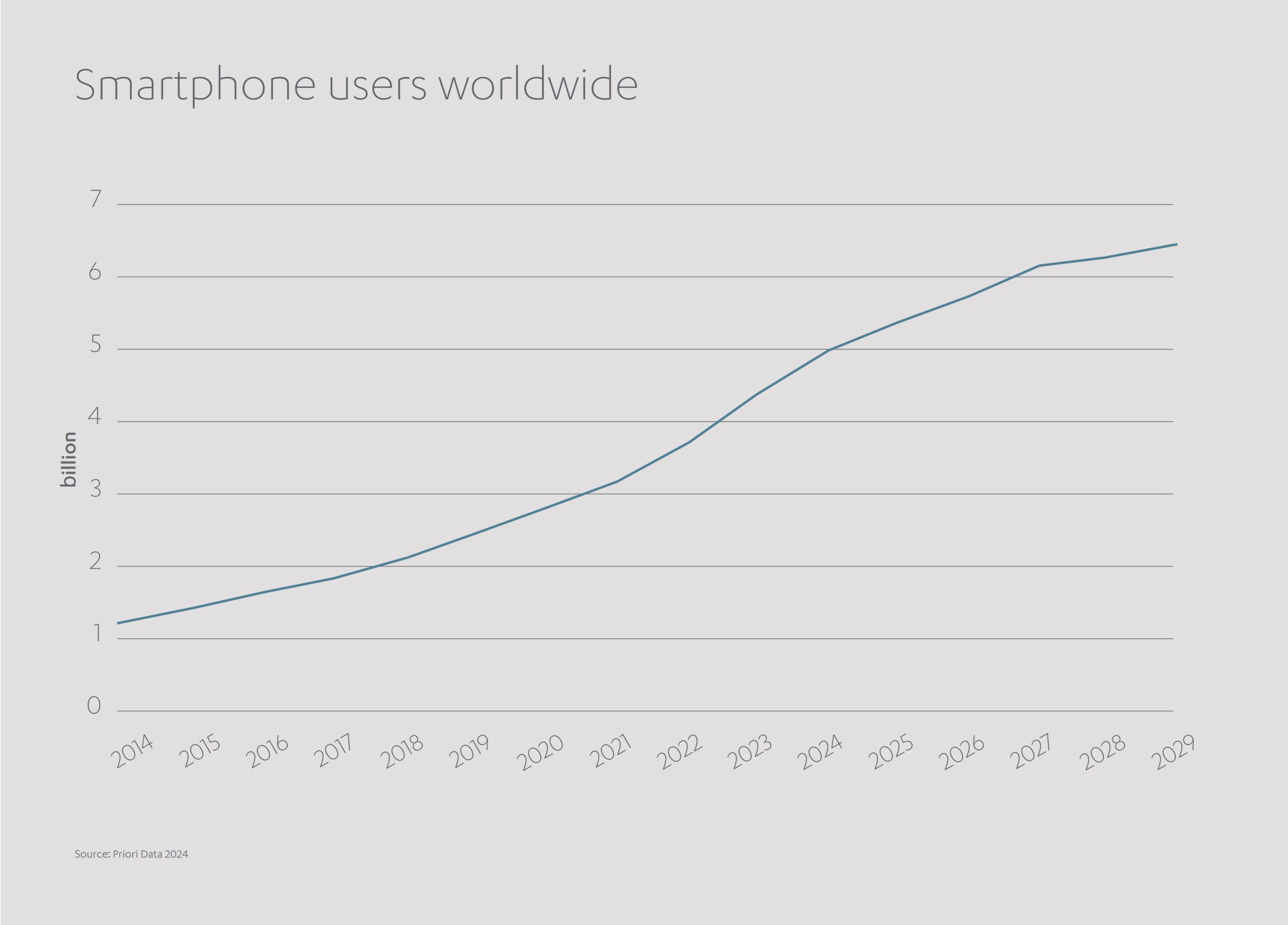

As of 2023 the number of cellphone owners worldwide reached 4.3 billion, or over half of the global population.[9] This trajectory is set to continue so that by the end of the decade the number of cellphone owners could top six billion.

Mobile technology is critical because modern smartphones are about so much more than texts and calls. Smartphones mean access to the worldwide web. Access to banks, both domestic and foreign. Access to apps allowing users to pay for products with a simple swipe or accept payments for services rendered. A cellphone opens the door to economic inclusion by introducing newcomers into the fundamentals of finance, helping them establish a verifiable credit record which can in turn be used to secure loans or make profitable investments. Increasingly, cellphones are the keys which can unlock the door to financial liberty.

Yet this represents just the tip of the iceberg of the financial technology (fintech) revolution helping democratize access to money.

Research shows that over the past 10 years fintech, in its various forms, has helped more than a billion unbanked people access financial services for the first time – notably across emerging markets in Sub-Saharan Africa and Asia.[10]

Cellphones are enabling a new concept in personal finance for developing nations – the mobile money service.

Accessible through any app-equipped smartphone, a mobile money service allows users to send, store and receive payments without need for a conventional bank account. For convenience, it also permits cash withdrawals at authorized agents. Deposits are protected by local financial regulations, and a record is kept of every transaction so that money is safe if a SIM card is lost or stolen. A trial scheme in Kenya among rural populations managed to lift around 2% of participating families out of poverty.[11]

With increasing numbers of people working in the gig economy, or being paid by the hour, the era of the monthly pay slip is waning. How to settle that urgent bill, or buy the supermarket shopping, if you have worked for multiple employers during the week each with different payment terms? Real Time Payment technology is emerging to fill the gap, allowing workers to quickly access pay accrued via an ‘earned-wage’ platform. It is proving a vital lifeline for those on insecure incomes even in developed countries like the USA, where more than a quarter of workers report having zero savings.[12]

Liberating finance in emerging markets begins with a robust network infrastructure. Tech firms are at the forefront of plans to invest billions of dollars in affordable connectivity and digital services across 16 Middle East, African and Asian countries between now and 2026. The money will be spent on improving network speeds and driving fiber adoption. A million households in Pakistan have already been introduced to the digital economy, with millions more set to follow.

Technology can help improve financial inclusion for female entrepreneurs too, who often have to fight to make their voices heard in many parts of the world. Digital bookkeeping apps are helping small- and medium-sized enterprises (SMEs) to accurately record cash flow and inventory – vital financial records which in the absence of collateral can be used to secure a loan. Similarly, electronic Know Your Customer (e-KYC) technology is helping female business owners in emerging markets access loans of up to US$ 20,000 by verifying their identities digitally.[13]

Fintech innovations can help protect customer assets while assuring compliance with state legislation, essential for any functioning system of financial inclusion. Regulatory technology (regtech) and supervisory technology (suptech) tools are helping formalize the oversight of new finance platforms. Regtech incorporates cutting-edge technologies such as AI, machine learning and blockchain to help companies abide by finance regulations within a given territory. Suptech tools allow regulators to scrutinize mass volumes of data from financial institutions to expose violations or risk. Together, regtech and suptech technology automates compliance processes for real-time monitoring, ultimately helping financial inclusion to flourish.

Embedded finance technologies (direct payment or loan tools accessible through non-banking websites) are proliferating, offering anyone with internet access faster and more versatile transaction choices.

New Fast Payment Systems are also hastening the spread of fintech across developing markets. They permit the near-instantaneous transfer of funds between accounts far quicker than traditional electronic payments. The technology is increasingly available to everyone and covers every type of transaction, whether person-to-person or business-to-business, either domestic or cross-border. International initiatives such as the Payment Systems Development Group (PSDG) have so far helped more than 120 countries modernize their payment systems, with Brazil’s Pix and Costa Rica’s SINPE Móvil serving as key templates.

The private sector is enthusiastically pursuing the digitization of financial services to improve access to money. Abdul Latif Jameel is leading from the front in global efforts to deploy fintech and widen inclusivity.

Bab Rizq Jameel Microfinance, part of Abdul Latif Jameel Finance Saudi Arabia, offers Sharia-compliant loans to long-neglected markets, helping nurture entrepreneurialism among innovators and SMEs. Elsewhere in Saudi Arabia Cash Jameel allows customers to apply for a 10,000 to 300,000 Saudi riyals loan, without guarantor, through a phone app, with approval granted in minutes.

The Abdul Latif Jameel Investment Management Company (JIMCO), meanwhile, is investing in numerous businesses that enable individuals and corporates to access the finance they need, when they need it most. Investments include:

- Social impact fintech business Ziina, an instant payment platform allowing workers across the MENA region to withdraw wages early for work already completed but not yet paid.

- Buy-now-pay-later startup Tabby, helping customers across the UAE and Saudi Arabia pay for purchases in multiple instalments or via a deferred single payment at no extra cost.

- Turkish fintech firm Figopara, offering extended working capital to businesses by lengthening payment terms to suppliers.

- Thndr, a mobile-first equities trading platform allowing individuals to make commission-free investments in stocks, bonds and funds on the Egyptian Stock Exchange.

- Rain, easing access to cryptocurrency markets for investors across the Middle East.

- Riyadh-based Lean Technologies, a B2B platform developing user-friendly software for securely connecting financial service institutions to customer bank accounts.

Fintech will continue evolving in the future, bringing financial inclusion to the masses and resolving at least some of the woes endured by the world’s unbanked minority. What does the future look like, and what should governments, NGOs and businesses be doing to prepare?

Will fintech and financial inclusion lead to a fairer future?

Based on the data, it appears that technology is propelling us to a more equitable and inclusive financial ecosystem. As more countries digitize their economies, and as more citizens migrate their personal finances online, valuable new insights will be gained and funding opportunities unlocked.

Increasingly, ‘big tech’ will harness multiple data points – utility bills, rent receipts, sporadic income – to evaluate loan applications. Data channels with unprecedented layers of security will allow governments, businesses and banks to incubate a fertile culture of open banking. The secure exchange of sensitive financial information will help sole traders become SMEs, SMEs become large businesses, and large businesses one day become multinational corporations.

Looking further ahead, public and private sectors must unite to focus on the underlying priorities of a digital ecosystem: Connectivity, cybersecurity, data privacy, digital ID and physical infrastructure.

More research is needed to circumvent the problems inherent in a financial system which is becoming more automated and, arguably, less human. We need to assess potential hazards surrounding consumer protection. We need to understand the dangers of overborrowing, for both individuals and businesses. We need to ensure that women and other under-served minorities are also able to share in the wealth of new opportunities.

All institutions have a part to play.

Banks must develop strategies to promote responsible borrowing and spending. Payment providers must work with fintechs to analyze data and enable sustainable investing.

Governments must legislate for the open sharing of data and encourage the transition by shifting their own payments to the digital realm.

International lawmakers must harmonize regulatory frameworks and ensure cross-border technological compatibility. NGOs must further expand inclusion by helping to improve financial literacy and by leveraging the benefits of fintech at grassroots level.

Chief Executive Officer

Financial Services & FinTech,

Abdul Latif Jameel

“The rewards could be deep and enduring,” says Jaroslav Gaisler, Chief Executive Officer, Financial Services & FinTech, Abdul Latif Jameel.

“Fusing fintech with the concept of financial inclusion unleashed the ideas and energies of untapped innovators within markets too often overshadowed by more mature economic rivals.

“We all stand to benefit from a mutually prosperous world.”

Fast Facts: Tech’s impact on financial inclusion

How many adults worldwide lack access to basic banking services?

Approximately 1.4 billion people – about a quarter of the world’s adult population – are unbanked, with no access to a bank account or appropriate alternatives.

How has mobile technology adoption changed the financial landscape?

As of 2023, there are 4.3 billion cellphone owners worldwide (over half the global population), and fintech has helped more than a billion previously unbanked people access financial services over the past decade.

Which regions are most affected by financial exclusion?

Around 80% of the 1.4 billion financially excluded adults live in emerging markets, particularly in Sub-Saharan Africa and Asia, which are also on the frontline of climate change challenges.

How much progress has been made in reducing the number of unbanked people?

The number of unbanked adults has fallen significantly from 2.5 billion in 2011 to 1.4 billion today, demonstrating steady improvement in financial inclusion.

How many countries have national financial inclusion strategies?

More than 60 countries have launched national financial inclusion strategies involving multiple stakeholders from telecoms, environment, education, and financial regulation sectors.

[1] https://www.weforum.org/stories/2024/07/why-financial-inclusion-is-the-key-to-a-thriving-digital-economy/

[2] https://www.bcg.com/publications/2024/to-expand-financial-inclusion-embrace-innovation

[3] https://www.worldbank.org/en/topic/financialinclusion/overview#1

[4] https://sdgs.un.org/goals

[5] https://www.worldbank.org/en/topic/financialinclusion/overview#1

[6] https://www.worldbank.org/en/topic/financialinclusion/overview#1

[7] https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/wp-content/uploads/2023/02/Empowering-women-micro-entrepreneurs-through-mobile.pdf

[8] https://www.worldbank.org/en/publication/globalfindex

[9] https://www.gsma.com/newsroom/press-release/smartphone-owners-are-now-the-global-majority-new-gsma-report-reveals/

[10] https://www.weforum.org/stories/2025/01/financial-equity-through-technology/

[11] https://www.weforum.org/stories/2025/01/financial-equity-through-technology/

[12] https://www.bankrate.com/banking/savings/emergency-savings-report/

[13] https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/wp-content/uploads/2023/02/Empowering-women-micro-entrepreneurs-through-mobile.pdf