Consumer survey data from S&P Global highlight a wide and

growing divergence between the financial wellbeing of the lowest

income and wealthiest households in the UK.

Measuring wellbeing

The Consumer Sentiment Index survey tracks key metrics among UK

households on a monthly basis, with the data series dating back to

early-2009. The most recent monthly datasets have shown some

encouraging signs of recovery, with the headline index reaching one

of its highest levels recorded in the survey. However, a closer

examination of the underlying data reveals markedly divergent

trends by income group, particularly since the pandemic and

throughout the ongoing cost of living crisis.

One of the questions included in the CSI questionnaire asks

respondents to compare their household’s financial situation to

that of the previous month. While the tracker has generally been

relatively elevated in recent months compared to the survey’s

long-run average, further analysis reveals significant divergences

in financial wellbeing based on household income levels.

The data breaks downs households into five different income

tiers:

• less than £15,000 per year

• £15,001 to £23,000 per year

• £23,001 to £34,500 per year

• £34,501 to £57,750 per year

• £57,751 or more per year.

Individuals in the higher income tiers generally report more

positive responses than their counterparts in all other income

brackets, but the disparity between the highest income tier and the

other brackets has widened in recent years.

This note will specifically examine the increasing gap between

the highest and lowest income brackets.

Growing divergence between higher and lower income

households since the pandemic

The COVID-19 pandemic introduced substantial shocks to

households’ financial wellbeing in the early months. All income

brackets reported a marked deterioration in their financial

situations in 2020, a trend that not only persisted but deepened

over the following years amid the cost-of-living crisis with the

notable exception of the highest income bracket, where the

experience has been more mixed.

Since the pandemic, households have faced mounting pressure from

rising costs of essentials such as food, energy, and housing.

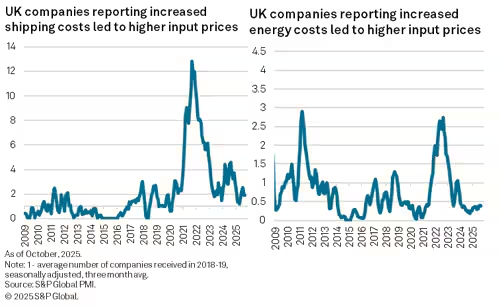

Energy prices, in particular, have undergone extreme fluctuations,

largely driven by the Ukraine-Russia conflict. Furthermore, supply

chain disruptions, including shipping challenges in the Red Sea,

have compounded shortages and elevated costs for essential

goods.

The repercussions of soaring energy costs and supply-side

challenges on input prices are captured in S&P Global Panel

Comments Trackers data, which provide qualitative insights from PMI

survey contributors around the globe.

The peak of this inflation crisis in the UK was experienced in

late 2022, when inflation soared to a 41-year high of 11.1%,

significantly surpassing the Bank of England’s target of 2%. This

period coincided with households reporting the most severe decline

in monthly financial wellbeing on record in October 2022, with the

seasonally adjusted headline index plunging to 26.9.

Notably, the gap between the highest and lowest earners at this

time was relatively narrow compared to historical averages.

The central bank reacted by tightening its monetary policy with

a series of interest rate hikes. However, as inflation began to

subside, this shift coincided with an expanding divide between the

highest and lowest earning households. Indeed, high-earning

households have consistently outperformed all other income brackets

during this period.

Wealthy households bounce back, but lower income

households struggle

As a result, differences in financial wellbeing among households

based on income have become more pronounced in recent years. The

chasm between the highest and lowest earners reached its zenith in

June 2024, just before the General Election. At that juncture, the

Bank of England’s policy rate had risen to a high of 5.25%,

occurring just one month prior to the central bank’s first rate

cut, which was followed by a series of further reductions.

Higher income households have demonstrated a more robust

recovery from the economic repercussions of the pandemic and the

ongoing cost of living crisis, as illustrated by the chart below,

which plots the shifts in financial wellbeing among the highest and

lowest income tiers since 2009, based on yearly averages. For the

years 2024 and 2025 (data available up to October), the highest

earning households have reported noteworthy improvements in their

financial circumstances. This trend underscores the resilience of

affluent households as they navigate the economic landscape,

achieving performance levels not previously seen in the series’

history.

Meanwhile, lower income households displayed some signs of

recovery in 2023 and 2024; however, they are experiencing greater

financial pressures again in 2025.

Outlook

The CSI data suggest that the disparity between higher and lower

earning households is set to endure, with affluent households

displaying relatively higher optimism regarding their financial

wellbeing outlook. In contrast, lower income households are bracing

for further declines in their financial health.

The upcoming Autumn Budget will be pivotal in shaping the

financial landscape for households in the year ahead. Adjustments

to the National Minimum Wage and National Insurance contributions,

alongside evolving tax implications, are fostering an environment

of uncertainty for both consumers and businesses.

Moreover, it will be crucial to assess the measures the

Chancellor may implement to support households, particularly as the

winter months loom.

Access the October CSI press release

here.

The next CSI release is scheduled for 17th

November.

Maryam Baluch, Economist, S&P Global Market

Intelligence

Tel: +44 1344 327 213

maryam.baluch@spglobal.com

© 2025, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers’ Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Learn more about PMI data

Request a demo

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.