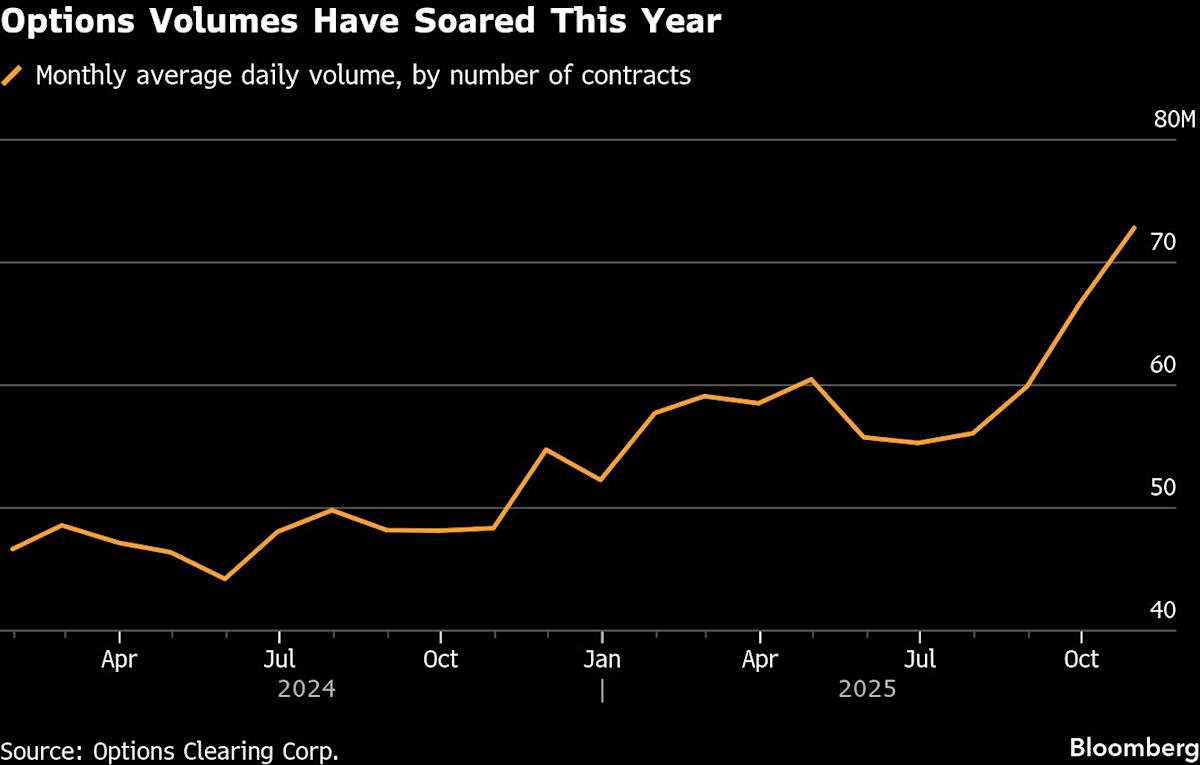

(Bloomberg) — As the US options market heads for a sixth straight year of record volume, some best-known names in the industry are growing nervous about its over-reliance on a small group of banks to guarantee trades for the biggest market makers.

Every listed US options trade goes through The Options Clearing Corp., a central counterparty that handles more than 70 million contracts a day during busy periods. The trades are submitted to the OCC by its members — who help trades get to the clearing house and act as guarantors in case their clients go bust.

Most Read from Bloomberg

There’s a small group of firms at the top. Out of dozens of members, the top five contributed almost half of the OCC’s default fund in the second quarter of 2025. Market participants cite Bank of America Corp., Goldman Sachs Group, Inc. and ABN Amro Bank NV as the three biggest, handling most positions from market makers, who take the other side of almost every options trade. The fact so much volume goes through such a small number of firms raises the risk of widespread losses if one of them should fail.

“I think there is significant concentration risk in clearing intermediation,” Craig Donohue, chief executive officer of Cboe Global Markets, Inc., said in an interview, without naming specific banks. “I do worry about that.”

The risk of a major bank failing is unlikely — but not unheard of. Donohue has his own battle scars from a clearing member default: in October 2011, when he was CEO of CME Group Inc., MF Global declared bankruptcy.

The more immediate risk is that these banks may run out of capacity to support the extraordinary growth of the listed derivatives market, with OCC average daily volume soaring 52% in October from a year earlier. That’s leading to a rise in “self-clearing” by market makers — meaning they become more direct members of the clearing house — which comes with its own risks, given that market makers are more thinly capitalized than banks.

Bank of America and Goldman Sachs declined to comment. ABN Amro did not immediately respond to a request for comment.

Related: SGX to List Perpetual Futures to Rival Crypto ‘Bucket Shops’

Only a handful of clearing brokers have the ability to cross-margin between futures and options, where opposite positions in related instruments can cancel each other out, reducing the amount of margin needed. For example, if a trader is long S&P 500 E-Mini Futures, but short S&P 500 Index Options, the net risk position would be reduced.

“There’s only a few members that can actually support some of the market makers and especially the cross margin program,” Andrej Bolkovic, OCC’s chief executive, said in an interview. “I think the market makers would like to see that change. That’s been a well known thing in the industry and something that we would also honestly support seeing change.”

The challenge for banks is that even if the clearing house involved agrees to give a customer a discount based on the level of net risk, the bank’s own capital framework may treat the two trades separately, requiring extra charges.

Patchwork Regulation

The patchwork US regulatory regime doesn’t help. Banks are regulated through the Federal Reserve System, broker dealers and the options market fall under the Securities and Exchange Commission, while futures, including equity futures, are the purview of the Commodity Futures Trading Commission. That means there are situations when a bank may give its customer the benefit of a cross-margin agreement, while still having to set aside funds itself to back the trade.

The rise of zero-day-to-expiry options and the explosion in retail trading volumes has brought new challenges for clearing members. Any move toward 24 hour, 7 day a week trading could put even more stress on the system and raise the bar higher for other firms to get involved.

The additional investment in upgrading capacity and technology to handle the greater volume and risk is likely to be passed on to clients. Bank of America has already raised the amount it charges clients per trade for options clearing, from between $0.02 – $0.03 to as much as $0.04, according to a person familiar with the matter.

Default Fund

OCC has proposed changing the way it calculates the proportion that each member pays into the roughly $20 billion default fund, to more fairly account for the market risks of each broker’s portfolio. That pot of money is designed to be big enough indemnify other members if the two largest clearing firms go bust at the same time.

Under the current system, 70% of the allocation is based on how a member copes with a roughly ~5% market move, according to Bolkovic. OCC has asked the SEC if it can change that metric to account for a more extreme scenario — a 1987-style market crash, when the Dow Jones Industrial Average plunged 22.6% in a day.

Clearing houses’ ongoing vigilance is itself a sign of strength, Donohue noted. “The regulatory and operational paradigm has adapted to better manage those kinds of risks.”

Donohue — who was OCC chairman from 2014 to 2025 — wants more institutions to step into the options clearing breach.

“If we could wave a magic wand and we could have more competition in that space, more clearing capacity, that was more distributed and dispersed and diverse, that would clearly be very beneficial for the market,” Donohue said.