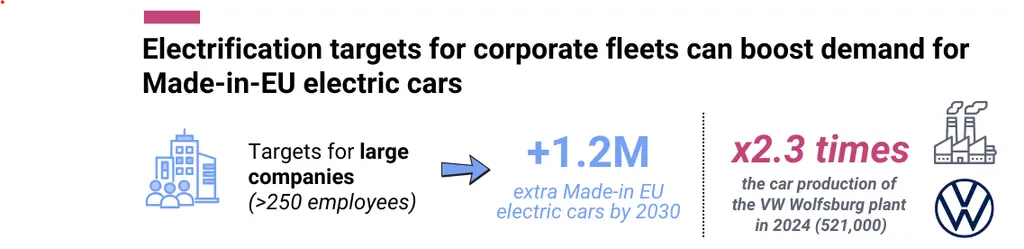

The European Commission is preparing a legislative proposal on Clean Corporate Vehicles. This is a big opportunity to boost demand for Made-in-EU electric cars.

Our analysis shows that already today, 73% of electric cars registered by companies were produced in the EU. For the private segment this was 63%. Because the majority of new vehicle sales in the EU are company cars, this 73% translates into 403,000 Made-in-EU EVs while for the private market this was only 184,000.

With the upcoming Clean Corporate Vehicles proposal, the European Commission can further tap into this potential. Asking the corporate market to accelerate and lead Europe’s shift to electric is legitimate:

-

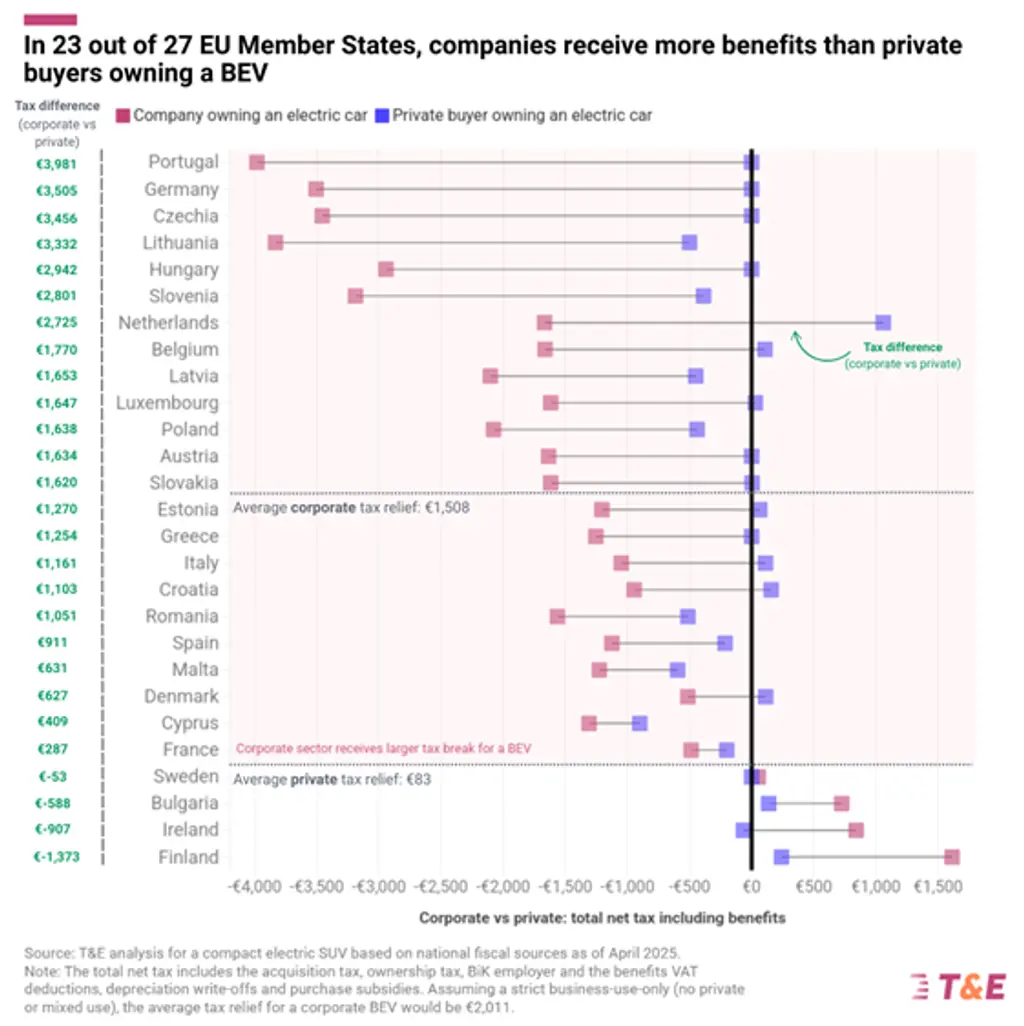

In 23 out of 27 Member States, companies receive more benefits than private buyers for owning an EV. In Germany this goes up to €14.000 per car.

-

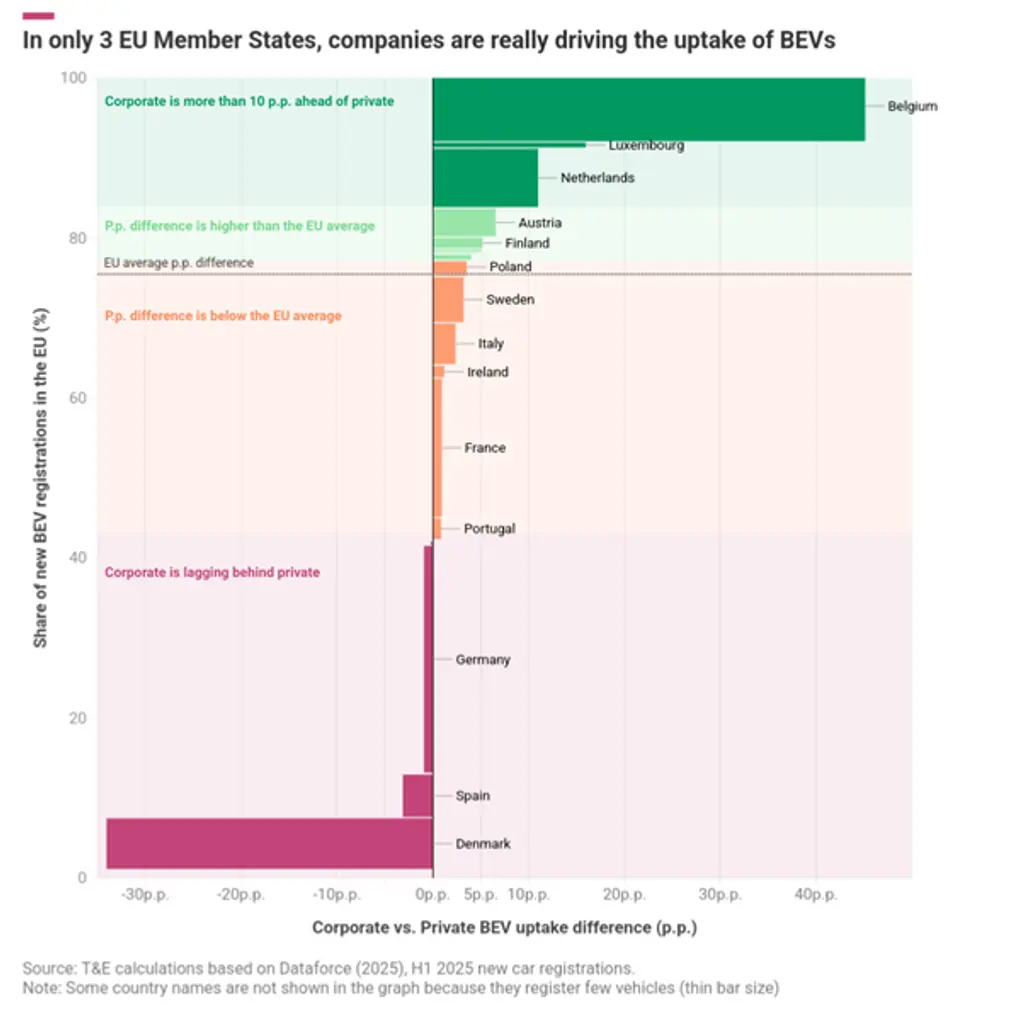

Despite such benefits, in only 3 Member States companies are really driving the uptake of electric cars.

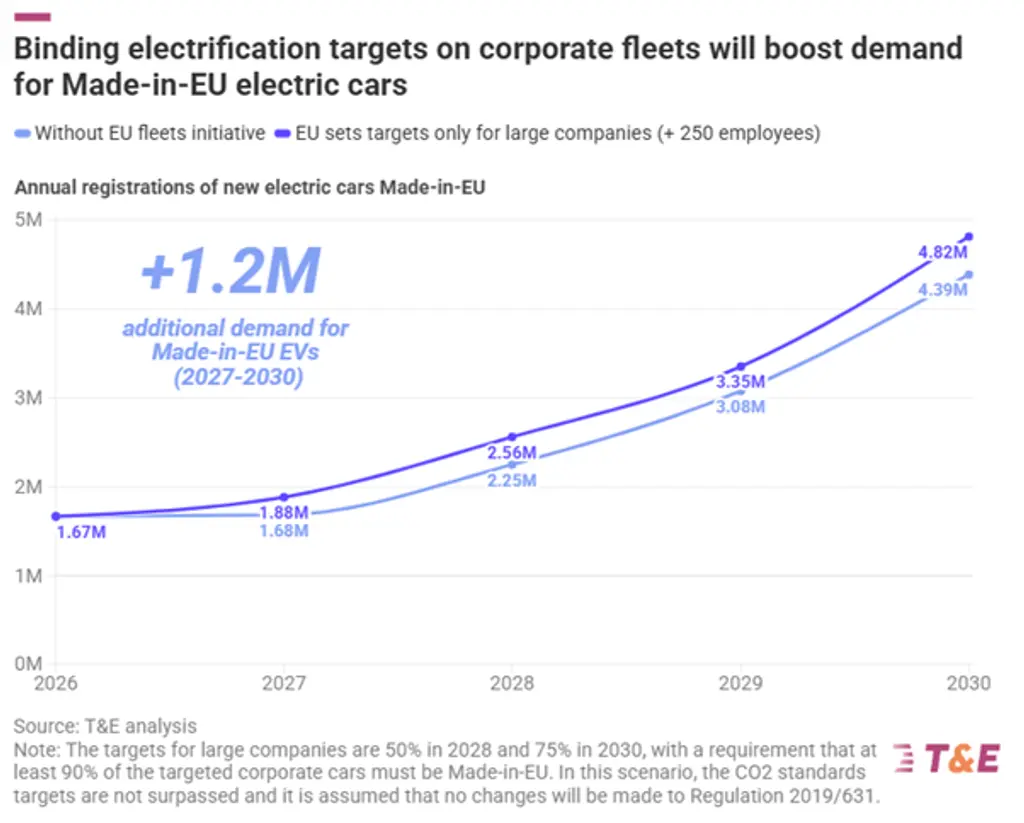

This means that the corporate market’s potential is far from exhausted: an EU-wide target (on Member States or companies) asking large corporations to electrify 75% of their new cars in 2030, with Made-in-EU requirements, could lead to an additional 1.2 million locally produced EVs by 2030.

1. Why the EC should ask companies to lead on electrification

The European Commission is preparing a legislative proposal on Clean Corporate Vehicles. This law is expected to set binding electrification targets on corporate cars – either on Member States or on large companies.

1.1. Companies benefit from tax breaks when owning an electric car

There are good reasons for the Commission to ask companies to lead Europe’s switch to electric: when companies buy or lease a car, they benefit from fiscal advantages that are not available to private buyers. Examples are VAT deductions, depreciation write-offs and Benefit-in-Kind.

In 23 out of 27 Member States, companies receive more benefits than private consumers when owning an electric car. T&E analysis shows that the average EU corporate tax relief for an EV buyer is €1,508 yearly. In Germany, where corporate EV tax benefits are among the highest, this goes up to €3,505 per year, or €14,020 over a typical ownership period of four years. Companies benefit from public money when owning an electric vehicle and should therefore drive the EU’s efforts in decarbonising road transport and boost demand for electric vehicles.

1.2. Only in three EU countries the corporate car market is clearly leading on electrification

Despite these fiscal benefits, companies are not clearly outpacing the private market in terms of electrification. This is partly due to the tax benefits that polluting company cars continue to receive. In only three EU countries the corporate market is significantly steering the adoption of BEVs (Belgium, Luxembourg, Netherlands). In large car markets such as Germany, France, Spain or Italy, their performance is underwhelming. Countries that have introduced structural fiscal reforms have a much higher corporate car electrification share. Since 2021, Belgium progressively phased out the fiscal deductibility for fossil fuel vehicles, creating a clear and growing incentive for BEV uptake. This has resulted in corporate BEV registrations of over 54% in the first half of 2025 (compared to 9% in the private market).

2. Electrifying corporate fleets brings more benefits for EU automotive industry

2.1. Companies buy more Made-in-EU EVs

Looking at the registration data of the first half year of 2025, companies tend to prefer purchasing more EVs that are made-in-EU than private households (73% against 63% for private buyers). Made-in-EU is defined as vehicles for which the final assembly line is located in the EU-27 (i.e. EVs of European brands that are produced in China and imported into the EU are not counted as Made-in-EU). Due to their high market share – 60% of new cars are corporate – and higher preference, there are 2.2 times more Made-in-EU electric cars registered by companies than private: 403,000 compared to 184,000 in just the first half of 2025.

2.2. What are the most popular EV models in the corporate and private market?

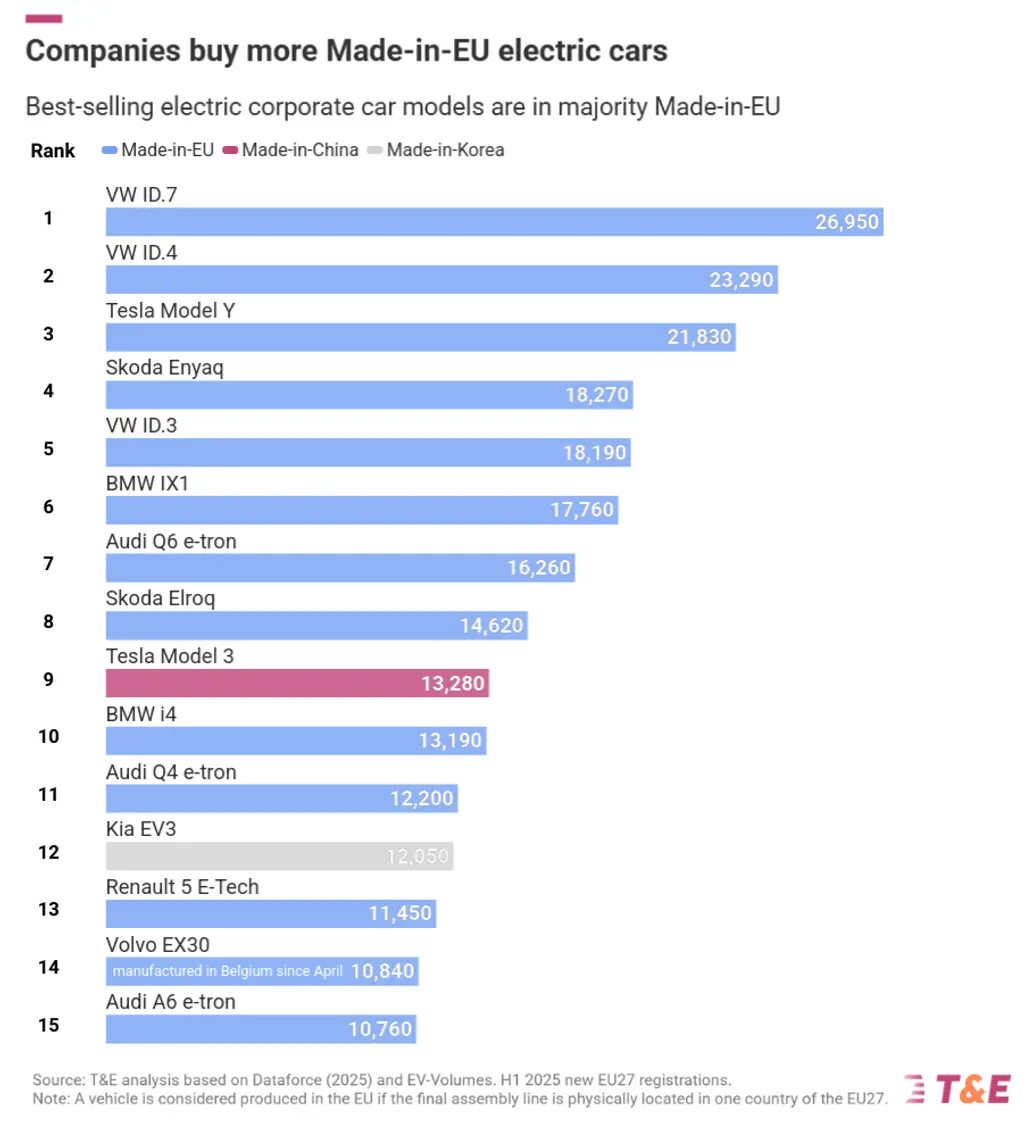

This trend is also reflected when zooming in on the most popular EV models for both the corporate and private segment: Made-in-EU EVs currently dominate the business segment, with 13 out of the 15 most popular models manufactured in the EU. For private buyers, these numbers are telling a different story: only 10 out of 15 top-selling models are EU made (see annex in full briefing attached on the left side of this page).

This gap becomes even more apparent when zooming in on the market share of the top 15 models that are not Made-in-EU (see figure below): for the corporate segment, the non Made-in-EU models (Tesla Model 3 and the Kia EV3), account for only 10% of the best-selling corporate EV sales in the first half of 2025. For the private segment, this is 32%.

3. How EU fleet targets can further boost demand for made-in-EU EVs

As T&E analysis confirms, companies currently have a higher preference for a Made-in-EU vehicle when purchasing an EV. Nevertheless, there is still a lot of untapped potential, as companies are currently not clearly leading on electrification (see Section 1). In order to assess the additional benefits of the forthcoming EU Clean Corporate Vehicles legislation on Made-in-EU EV production, we have analysed the impact of EU fleet targets on the demand for EVs produced in the EU under two scenarios.

-

Business as usual: without any obligations on corporate vehicles and under today’s market conditions and CO2 standards (Regulation 2019/631), we expect 13.1 million Made-in-EU electric vehicle sales between 2026 and 2030.

-

Binding electrification targets on Member States (only affecting large companies): in this scenario, the European Commission proposes binding ZEV-purchasing targets on large companies (+250 employees) as part of the Clean Corporate Vehicles legislation: 50% of new large company registrations by 2028, and 75% by 2030 have to be zero emission vehicles, with a requirement that at least 90% of the targeted corporate cars must be Made-in-EU. These targets would increase the demand for additional made-in-EU electric cars by 1.2 million, bringing total production to 14.3 million vehicles. For illustration: the total production of the VW Wolfsburg plant in 2024 (all powertrain types) reached 521,000 units.

Being Europe’s largest manufacturing country, the benefits for electric car production in Germany are particularly big. Results for Germany can be found in the annex.

This potential increase is crucial for Europe. It proves the CCV initiative is essential for growing the European manufacturing scale and keeping our domestic EV supply chain competitive. It achieves this industrial boost without needing to raise the ambition of current CO2 emission standards.

4. Policy recommendations

To fully unlock the potential of the corporate car market to drive both the clean transition and the competitiveness of European car manufacturers, the European Commission should:

-

1

Propose a Regulation on Clean Corporate Vehicles: corporate fleets make up 60% of new cars and therefore have a lot of potential for both decarbonisation and European car manufacturing. Today, however, the corporate segment is not really leading on electrification in most Member States, despite existing tax benefits and incentives.

-

2

Include ambitious, binding ZEV-targets: the Regulation must set ambitious, binding Zero-Emission Vehicle (ZEV) targets on Member States. When designing national policies, SMEs should be exempted from any requirements to obtain the targets. Instead, Member States should aim their measures at large companies (+250 employees) in order to tap into the industrial potential of corporate vehicles while limiting the impact on European businesses.

-

3

Introduce local content requirements: this legislation should also include Made-in-EU requirements to further boost domestic EV production. By doing so, the Commission should clearly define what Made-in-EU EVs and batteries are and set up a transparent methodology rewarding Made-in-EU EVs, batteries, key components and materials.