GLP-1 weight loss drugs are likely to impact long-term category growth rates for food consumption.

Their main mechanism of action is to make users feel satiated more quickly, reducing overall food intake as well as consumption of alcohol and tobacco.

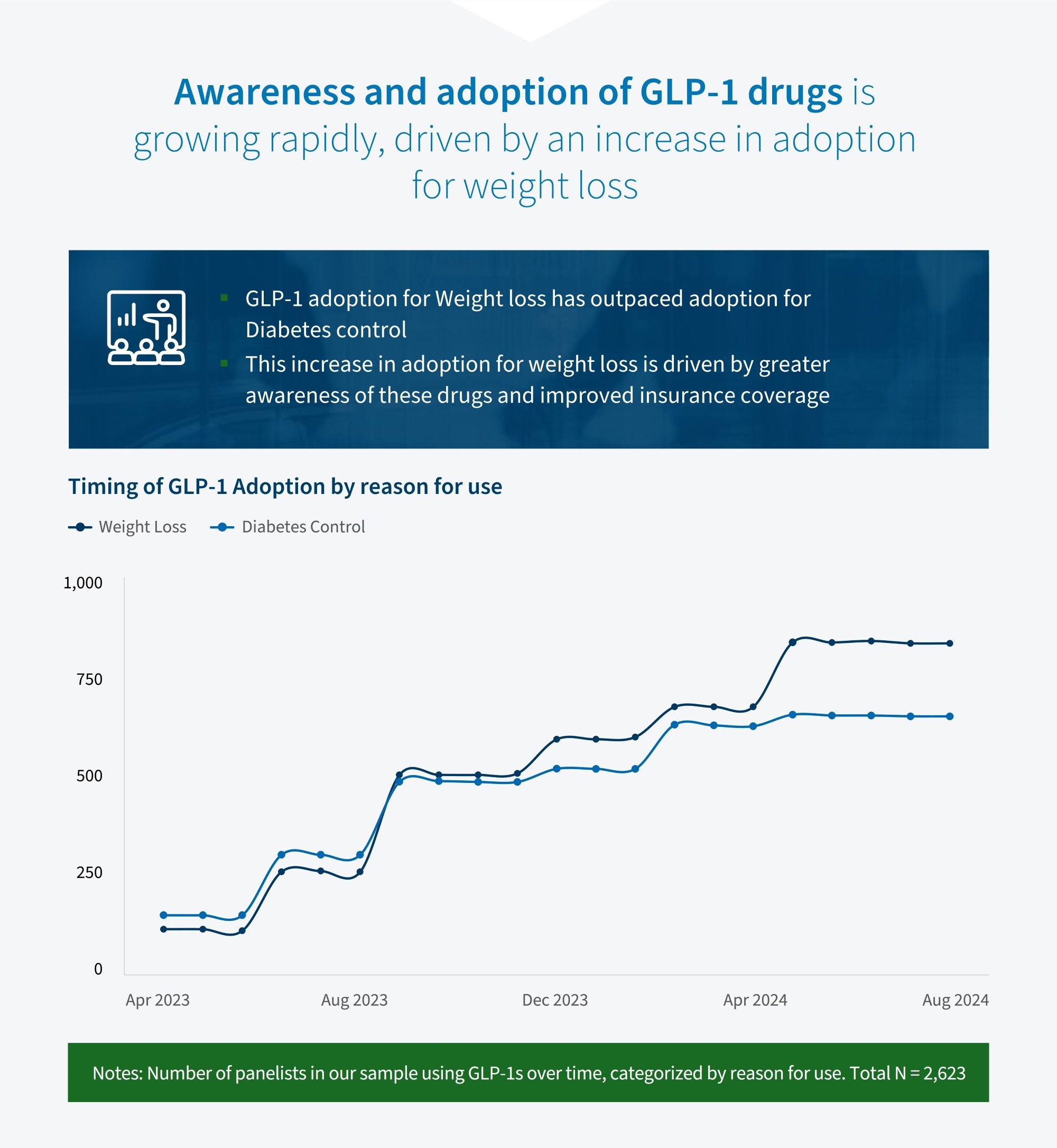

Users report a 30 percent reduction in calories consumed. Adoption of these drugs is rising rapidly. FTI Consulting’s survey shows that more than 20 percent of US adults have used them in the past 12 months, despite high costs, side effects and the need for injectable delivery.

As insurance coverage expands and out-of-pocket costs fall, use of GLP-1 drugs is likely to increase further, especially for weight loss. A reduction in pricing as production costs fall is expected to support adoption among lower-income groups. The potential launch of oral versions of the underlying molecule, expected around 2027–28, represents another catalyst that could broaden penetration into the US population.

Our analysis indicates that between 20 and 30 percent of annual patients stop using the drugs, particularly those focused on weight loss, and these patients regain about two-thirds of the weight they lost.

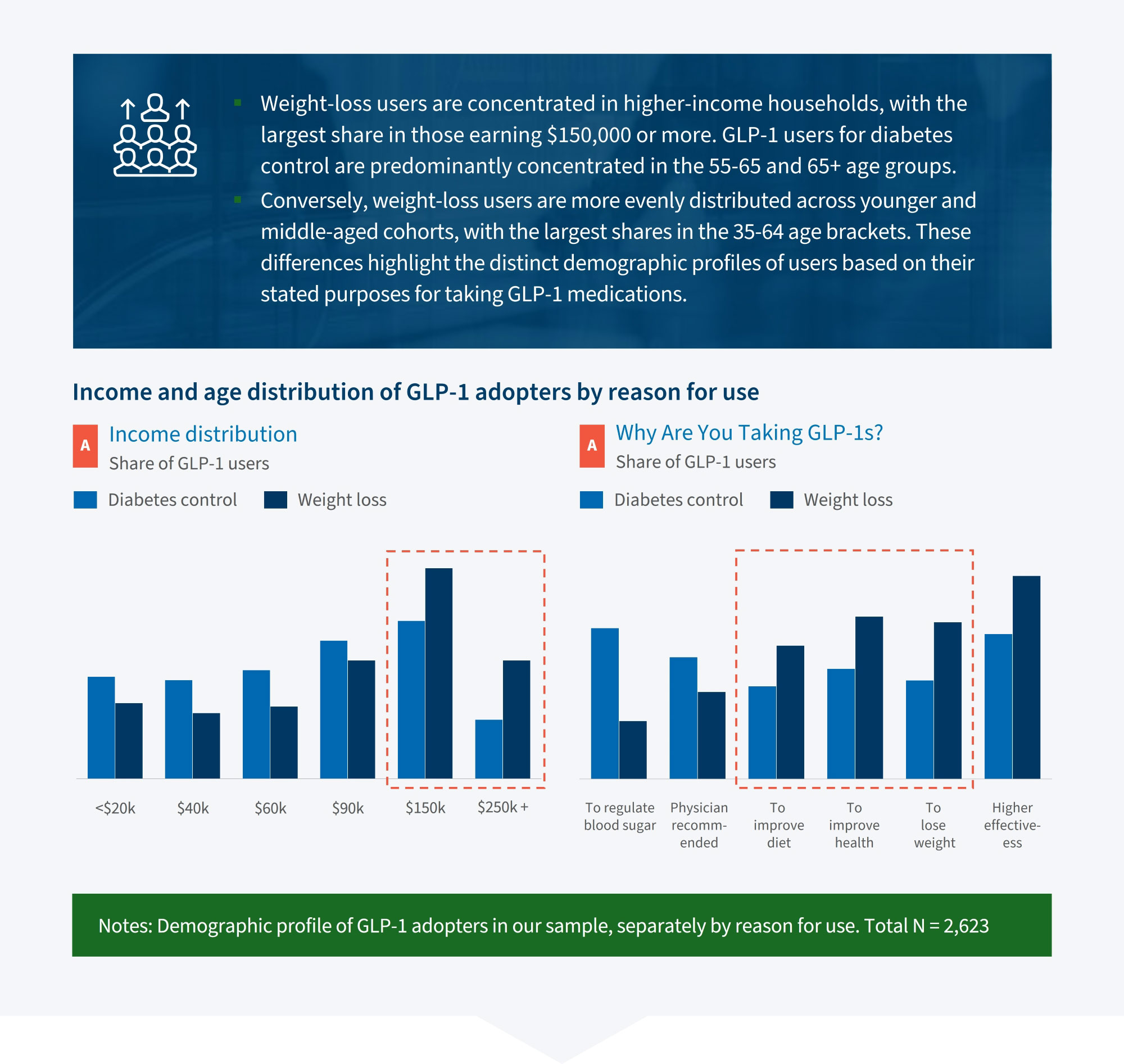

The rise in GLP-1 adoption is creating important shifts in consumer behavior.

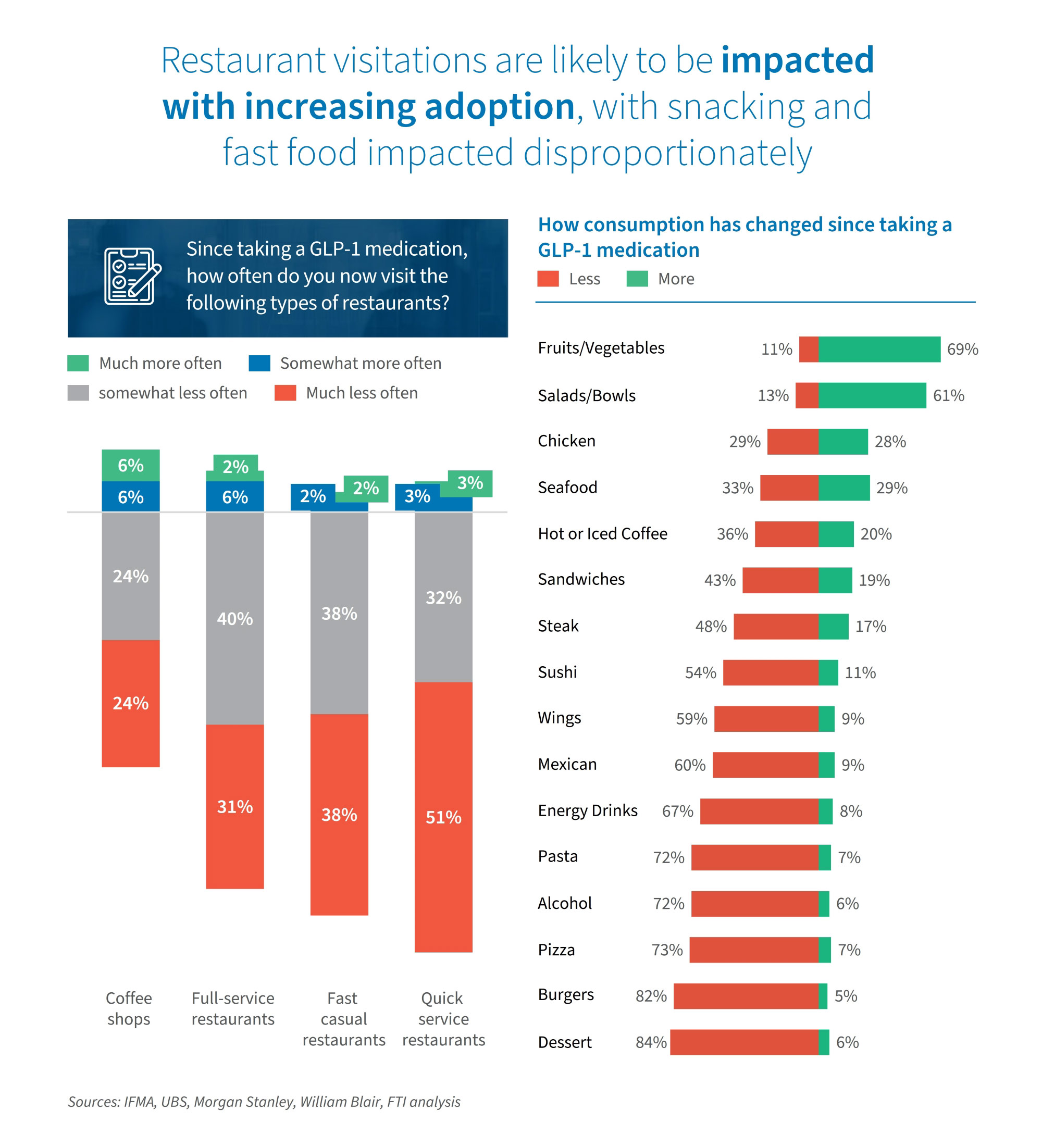

Traditional high-calorie snacking categories and center-store products are seeing reduced consumption, slowing growth for portfolios heavily indexed to these areas. At the same time, recent adopters who use GLP-1 drugs for weight loss show greater interest in healthier and better-for-you alternatives across snacking categories.

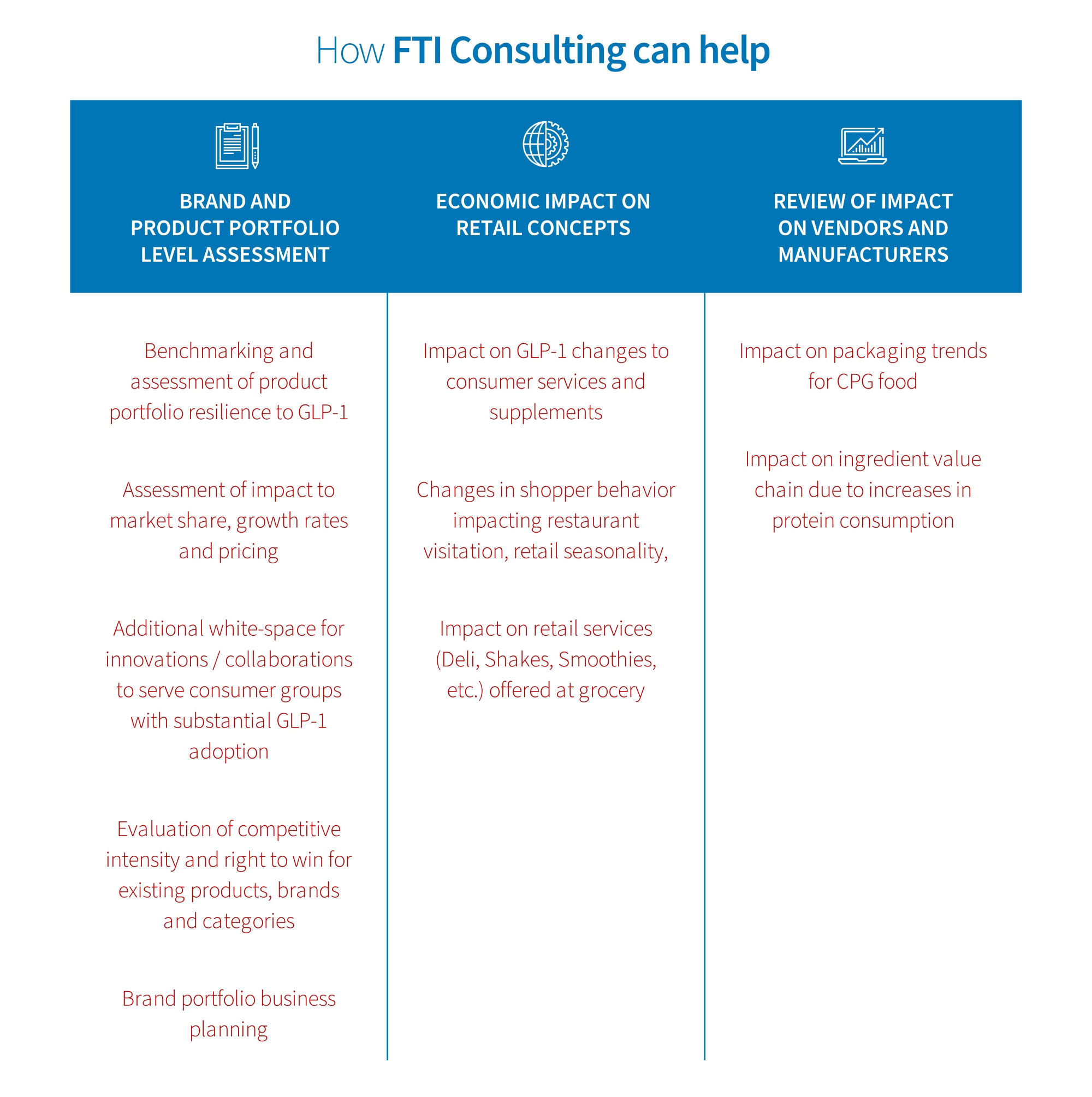

Companies, both established and new, would benefit from recognizing this trend and aligning their innovation pipelines with the needs of this expanding segment of the US adult population.

Weight management and active nutrition products are also benefiting from a broader adoption of GLP-1 drugs, as they are perceived as better supplements.

In addition, some frozen food and dairy categories are experimenting with GLP-1-friendly labels.

The trend is also affecting food consumed away from home, with noticeable impacts across different day parts and restaurant concepts.

Survey results show that most fast-casual dining brands have a comparable or higher share of GLP-1 users than the general population.

Health-focused brands tend to outperform other quick-service restaurants, likely due to a higher proportion of weight-conscious users, and casual dining brands overall are attracting a greater share of GLP-1 users among their guests.