Author: Petras Katinas

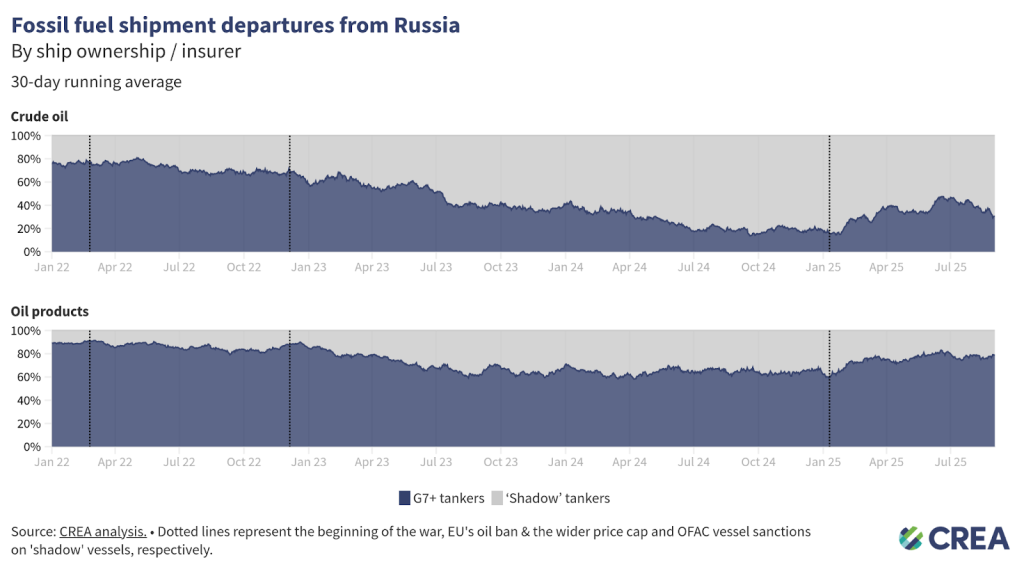

Shadow tankers’ transport of Russian oil rebounded in August, as G7+ tankers’ share dropped by 8 percentage points month-on-month

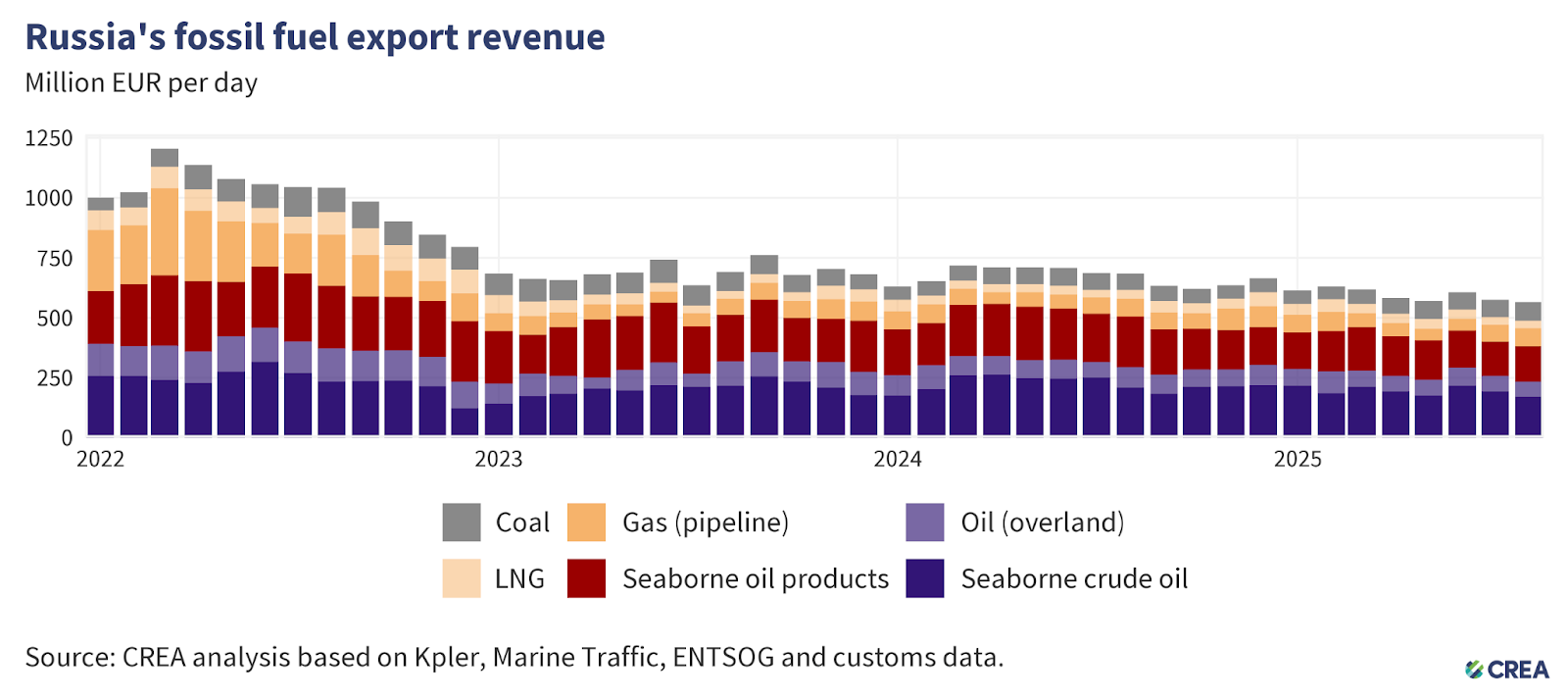

- Russia’s monthly fossil fuel export revenues dropped for a third consecutive month in August, recording a 2% month-on-month decline to EUR 564 mn per day.

- Revenues from coal exports increased by 7% month-on-month to the highest levels of the year.

- Russian coal exports increased this month mainly because South Korea’s purchases went up, driven by higher electricity use in the country. South Korea’s imports of Russian coal rose 36% month-on-month to their highest levels ever.

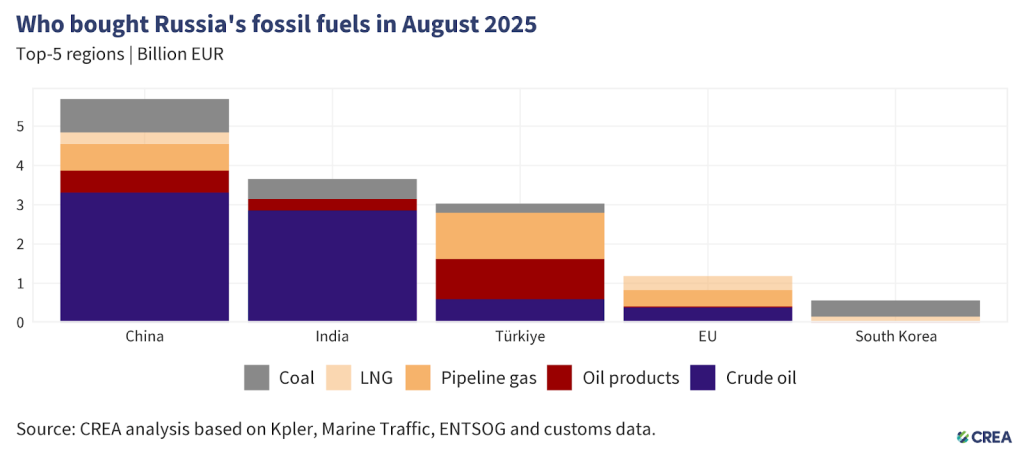

- In August 2025, the five largest EU importers of Russian fossil fuels — China, India, Turkiye, the EU, and South Korea — paid Russia a combined EUR 979 mn for fossil fuels.

- In August 2025, just over half (53%) of Russian oil shipments were carried on G7+ tankers, an 8 percentage point decline from July — suggesting a renewed reliance on the ‘shadow’ fleet.

- In August 2025, a quarter of the oil delivered by ‘shadow’ tankers was transported on tankers currently under sanctions. These sanctioned tankers carried 12% of Russian oil exports in August.

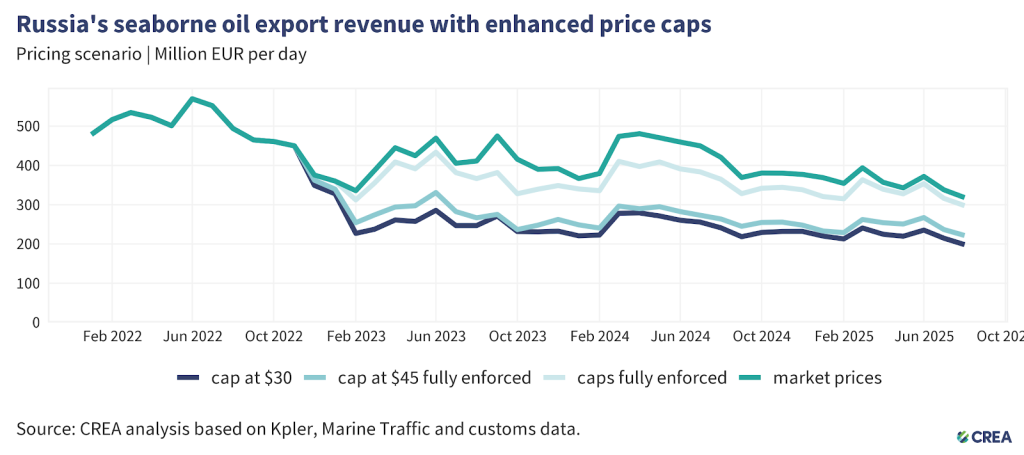

- A lower price cap of USD 30 per barrel (still well above Russia’s production cost, which averages USD 15 per barrel) would have slashed Russia’s oil export revenue by 40% (EUR 153 bn) from the start of the EU sanctions in December 2022 until the end of August 2025. In August alone, a USD 30 per barrel price cap would have slashed Russian revenues by 38% (EUR 3.71 bn).

- In August, Russia’s monthly fossil fuel export revenues saw a 2% month-on-month decline to EUR 564 mn per day — a third consecutive month in which Russia’s fossil fuel export revenues have dropped.

- Seaborne crude oil revenues saw a sharp 12% month-on-month decrease to EUR 170 mn per day, whereas volumes dropped by 10%. Russian seaborne crude oil revenues have declined for the third consecutive month, reaching their lowest levels of 2025.

- Revenues from crude oil via pipeline marginally increased by 2% month-on-month, to EUR 62 mn per day.

- Liquefied natural gas (LNG) revenues increased by 4% to EUR 31 mn per day, corresponding to a 7% increase in exported volumes.

- Pipeline gas revenues increased by 8% to EUR 75 mn per day, albeit volume increased by 10% month-on-month.

- Revenues from exports of seaborne oil products saw a 2.5% month-on-month increase, reaching EUR 147 mn per day, while volumes marginally increased by 2% even in the face of Ukrainian drone strikes on Russian oil refineries.

- Coal revenues rose by 7% month-on-month to EUR 76 mn per day, with exported volumes increasing by 6%. This month, coal export revenues reached their highest level of 2025.

- Russia’s fossil fuel exports remain highly concentrated, with China dominating coal and crude oil purchases, Turkiye dominating purchases of oil products, and the EU still the largest buyer of LNG and pipeline gas — showing Moscow’s dependence on a narrow set of key customers.

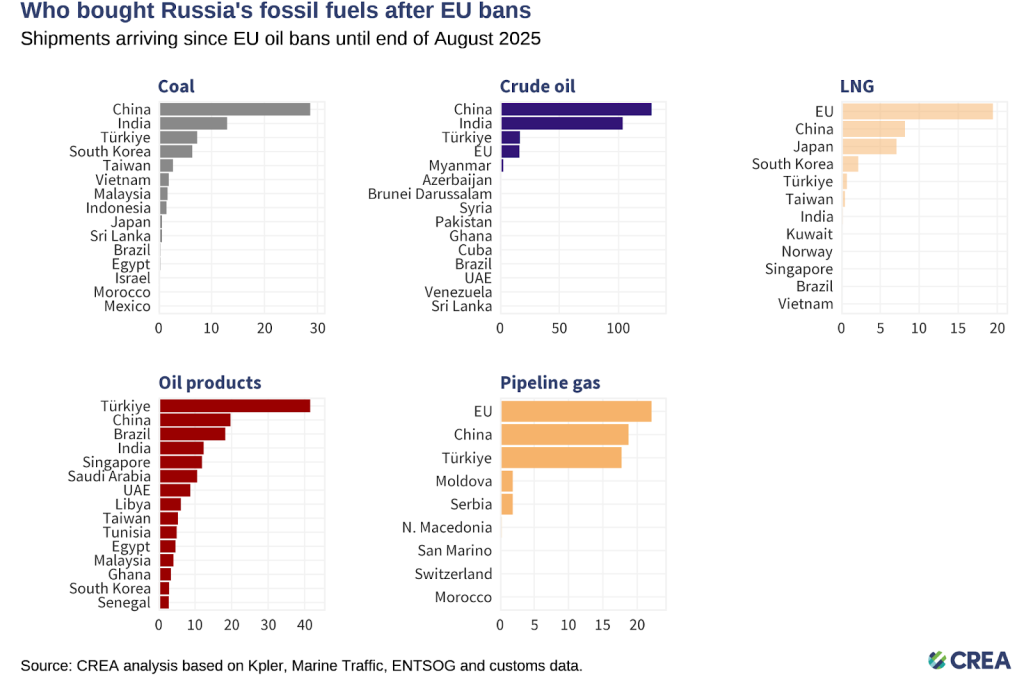

- Coal: From 5 December 2022 until the end of August 2025, China purchased 44% of all of Russia’s coal exports. India (20%), Turkiye (11%), South Korea (10%), and Taiwan (4%) round off the top five buyers list.

- Crude oil: China has bought 47% of Russia’s crude exports, followed by India (38%), the EU (6%), and Turkiye (6%).

- Oil products: Turkiye, the largest buyer, has purchased 26% of Russia’s oil product exports, followed by China (13%) and Brazil (12%) and Singapore (7%).

- LNG: The EU was the largest buyer, purchasing 50% of Russia’s LNG exports, followed by China (21%) and Japan (18%).

- Pipeline gas: The EU was the largest buyer, purchasing 35% of Russia’s pipeline gas, followed by China (30%) and Turkiye (28%).

- In August 2025, China remained the largest global buyer of Russian fossil fuels, accounting for 40% (EUR 5.7 bn) of Russia’s export revenues from the top five importers. Crude oil made up the largest share of China’s purchases at 58% (EUR 3.1 bn), followed by coal at 15% (EUR 855 mn), pipeline gas at 12% (EUR 676 mn), and oil products at 10% (EUR 553 mn).

- India remained the second-largest buyer of Russian fossil fuels, importing a total of EUR 3.6 bn. Crude oil dominated India’s purchases at 78% (EUR 2.9 bn), followed by coal at 14% (EUR 510 mn) and oil products at 8% (EUR 282 mn).

- Turkiye was the third-largest importer of Russian fossil fuels, accounting for 21% (EUR 3 bn) of Russia’s export revenues from its top five buyers. Pipeline gas constituted the largest share of Turkiye’s imports at 39% (EUR 1.2 bn), followed by oil products at 34% (EUR 1 bn), crude oil at 20% (EUR 596 mn), and coal at 7% (EUR 225 mn).

- The EU was the fourth-largest buyer of Russian fossil fuels, accounting for 8% (EUR 1.2 bn) of Russia’s export revenues from the top five importers. The majority of imports, 66% (EUR 773 mn), consisted of LNG and pipeline gas, followed by crude oil at 32% (EUR 379 mn).

- South Korea became the fifth-largest importer of Russian fossil fuels. Coal dominated its imports at 73% (EUR 413 mn), followed by LNG at 21% (EUR 118 mn) and oil products at 6% (EUR 33 mn). Due to high temperatures and increased electricity consumption, South Korea’s coal imports saw a 19% month-on-month increase. Russian coal supplied to South Korea shot up in turn — recording a 36% month-on-month rise to their highest volumes ever — and constituted 30% of the total imports while also dominating other sources for the first time.

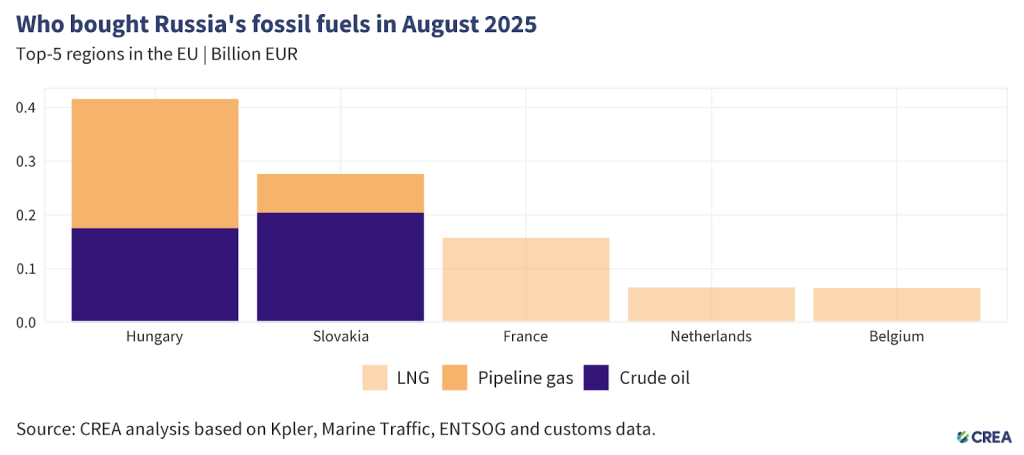

- In August 2025, the five largest EU importers of Russian fossil fuels paid Russia a combined EUR 979 mn for fossil fuels. Natural gas — unsanctioned by the EU — accounted for more than 61% of these imports, delivered mainly by pipeline or as liquefied natural gas (LNG). The remainder was largely crude oil, which continues to flow to Hungary and Slovakia through the southern branch of the Druzhba pipeline under an EU exemption.

- Hungary was the EU’s largest importer, purchasing EUR 416 mn worth of Russian fossil fuels. This included EUR 176 mn of crude oil and EUR 240 mn of pipeline gas.

- Slovakia ranked second, with imports totaling EUR 276 mn. Crude oil delivered via the Druzhba pipeline made up 74% of the total (EUR 204 mn), while pipeline gas accounted for EUR 72 mn. The derogation allowing Slovak refineries to process Russian crude into oil products and re-export them to Czechia expired on 5 June.

- France was the third-largest buyer, importing EUR 157 mn of Russian fossil fuels, all in the form of LNG. However, not all of this gas is consumed domestically — a study shows that some LNG entering through the Dunkerque terminal is subsequently delivered to Germany.

- The Netherlands was the fourth biggest importer, importing EUR 65 mn of Russian LNG, while Belgium, in fifth place, purchased EUR 64 mn, also entirely in LNG.

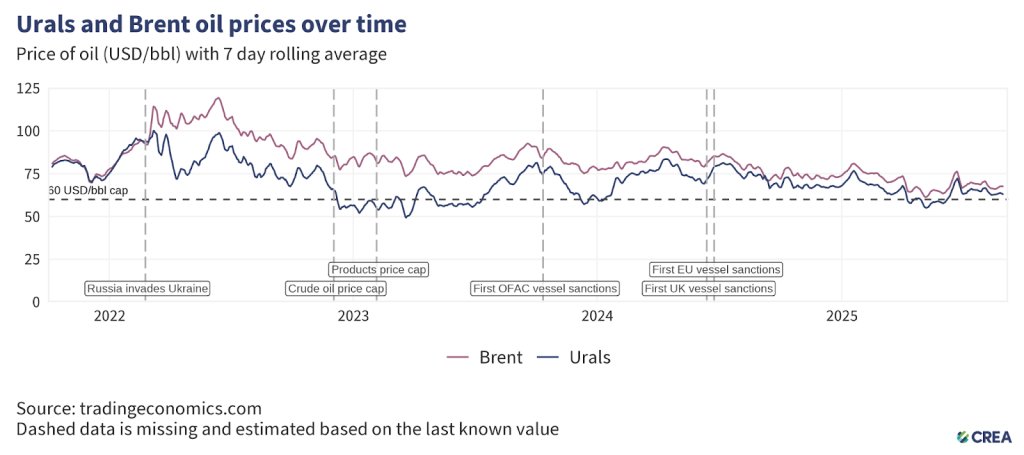

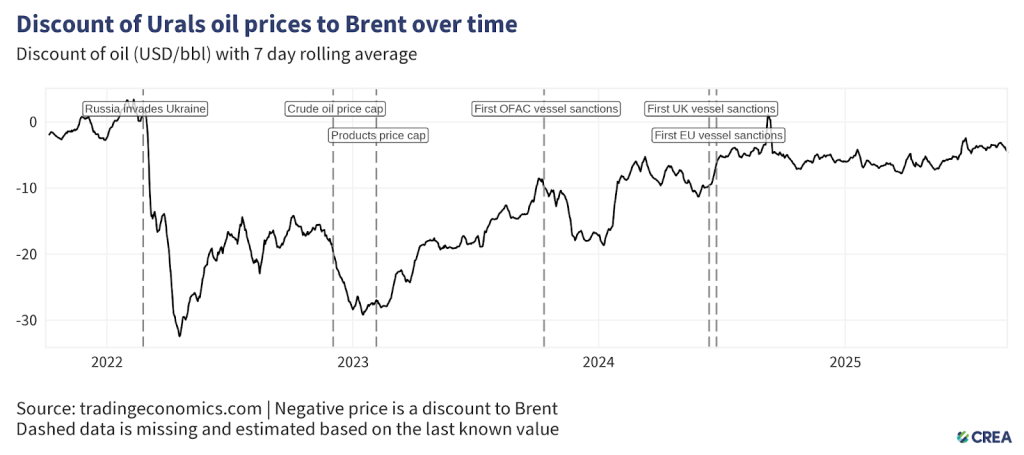

- In August 2025, the average price of Urals crude stood at USD 63.4 per barrel, down 2.3% from July.

- The discount on Urals crude narrowed by 6% month-on-month, averaging USD 3.7 per barrel against Brent in August.

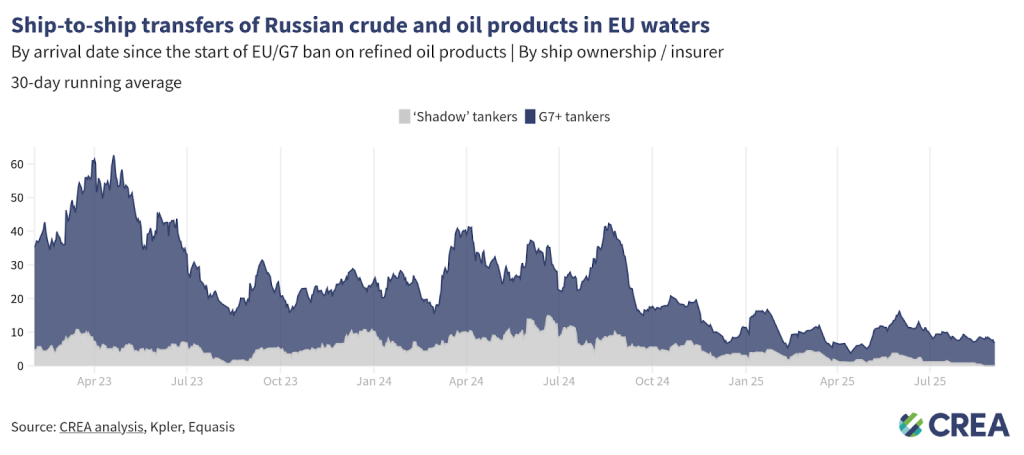

- In August 2025, Russia exported 25 mn tonnes of oil by sea. Just over half (53%) of these shipments were carried on G7+ tankers, an 8 percentage point decline from July — suggesting a renewed reliance on the ‘shadow’ fleet.

- G7+ tankers carried 36% of Russian crude oil exports in August, while the share of ‘shadow’ tankers rose by 11% month-on-month. Oil products, by contrast, remain less dependent on ‘shadow’ vessels, with G7+ tankers transporting 78% of shipments — a marginal increase compared to July.

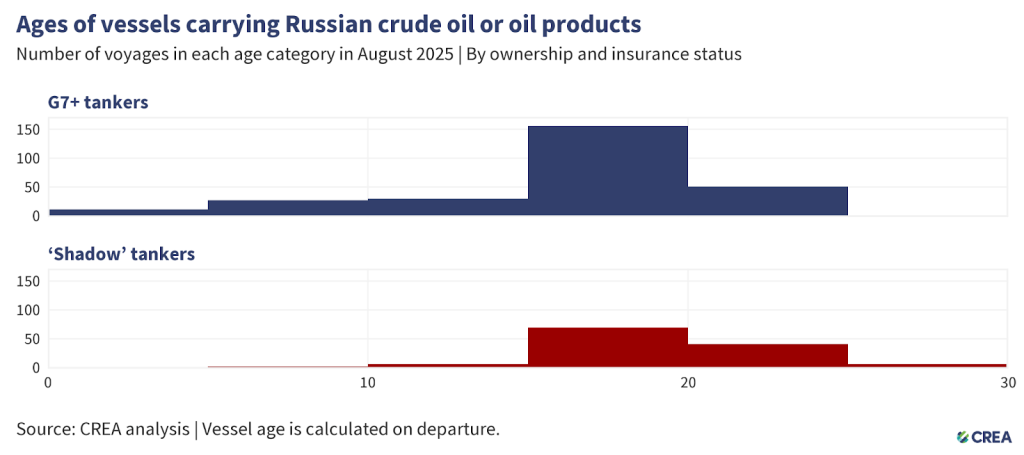

- In August 2025, a quarter of the oil delivered by ‘shadow’ tankers was carried on tankers currently under sanctions. These sanctioned tankers transported 12% of Russian oil exports in August.

- In August 2025, 400 vessels exported Russian crude oil and oil products, of which 125 were ‘shadow’ tankers. Thirty-eight ‘shadow’ tankers were at least 20 years or older.

- Older ‘shadow’ tankers transporting Russian oil and petroleum products across EU Member States’ exclusive economic zones, territorial waters, or maritime straits raise environmental and financial concerns due to their age, questionable maintenance records, and insurance coverage. Their insurance potentially lacks sufficient protection & indemnity (P&I) coverage to cover the cost in the event of an oil spill or other catastrophe. In the event of accidents, coastal countries may bear the financial burden of cleanup, as well as the repercussions of damage to their marine ecosystems.

- The cost of cleanup and compensation resulting from an oil spill from tankers with dubious insurance could amount to over EUR 1 bn for coastal country’s taxpayers.

- In August 2025, an estimated EUR 121 mn worth of Russian oil was transferred daily via ship-to-ship (STS) transfers in EU waters — a 9% decrease from the previous month. G7+ tankers conducted 94% of these transfers, while the rest involved ‘shadow’ vessels, which are often uninsured or registered under flags of convenience.

Russia’s fossil fuel export revenues have fallen since the sanctions were implemented, subsequently constricting Putin’s ability to fund the war. However, much more should be done to limit Russia’s export earnings and constrict the funding of the Kremlin’s war chest. This includes lowering the oil price cap, increasing monitoring and enforcement of sanctions, and banning unsanctioned fossil fuels such as LNG and pipeline fuels that are legally allowed into the EU.

Lowering the oil price cap

- A lower price cap of USD 30 per barrel (still well above Russia’s production cost, which averages USD 15 per barrel) would have slashed Russia’s oil export revenue by 40% (EUR 153 bn) from the start of the EU sanctions in December 2022 until the end of August 2025. In August alone, a USD 30 per barrel price cap would have slashed Russian revenues by 38% (EUR 3.71 bn).

- Lowering the price cap would be deflationary, reducing Russia’s oil export prices and inducing more production from Russia to make up for the drop in revenue.

- Since introducing sanctions until the end of August 2025, thorough enforcement of the price cap would have cut Russia’s export revenues by 11% (EUR 40 bn). In August 2025 alone, full enforcement of the price cap would have reduced revenues by 6% (approximately EUR 0.68 bn).

Restrict the growth of ‘shadow’ tankers & tighten regulations targeting the refining loophole

- Frequent sanctioning of Russian ‘shadow’ vessels has shifted Russian oil back to tankers owned or insured in G7+ countries. Nonetheless, Russian ‘shadow’ tankers still hold sway on the transport of Russian crude oil. In addition, many sanctioned vessels continue to deliver oil to ports globally, with EU and UK sanctions in particular, frequently violated. Sanctioning countries must align their vessel lists, and enforcement paradigms for a magnified effect on their operations.

- Maritime coastal states should intensify efforts to monitor, inspect, and detain ‘shadow’ fleet vessels that lack legal passage rights, such as those unflagged, unlawfully idle, or posing security risks. Authorities must enforce and improve environmental and navigation laws within their territorial waters, investigating and boarding suspicious vessels when justified. Crews involved in criminal activity should face prosecution, with noncompliant ships and personnel subject to international arrest warrants.

- In its 18th sanctions package, the EU has banned the imports of ‘oil refined from Russian crude’. The regulation bans imports from countries that are ‘net importers’ of crude oil. Net export status does not preclude the import and refining of Russian-origin crude, especially in jurisdictions with flexible or opaque crude sourcing practices. To close this enforcement gap, the exemption should be applied at the refinery level, not the national level. Refined petroleum products should be subject to import restrictions if produced at facilities that have processed Russian crude within the past six months, regardless of the final product’s declared origin or the host country’s net export position.

- The current grace period provides Russia as well as traders buying oil refined using Russian crude with excessive time to adjust supply chains and maintain oil revenue. A shorter 60-day wind‑down period, focused on high‑risk refined products like diesel and jet fuel, would reduce Russia’s fiscal gains and limit circumvention opportunities. It would also give the EU sufficient time to secure alternative suppliers.

- The exemption of countries including the UK, USA, Canada, Norway, and Switzerland creates an opportunity for oil products refined from Russian crude to be re-exported to the EU. This gap should be closed to ensure the sanctions are comprehensive and watertight.

Stronger enforcement & monitoring of the price cap

- Despite clear evidence of violations, agencies must do more to enforce penalties against shippers, insurers, or vessel owners. This information must be shared widely in the public domain. Penalties against violating entities increase the perceived risk of being caught and serve as a deterrent.

- Penalties for violating the price cap must be significantly harsher. Current penalties include a 90-day ban on vessels from securing maritime services after violating the price cap, a relatively minor sanction. If found guilty of violating sanctions, vessels should be fined and banned in perpetuity.

- The G7+ countries should ban STS transfers of Russian oil in G7+ waters. STS transfers undertaken by old ‘shadow’ tankers with questionable maintenance records and insurance pose environmental and financial risks to coastal states and support Russia logistically in exporting high volumes of crude oil. Coastal states should require oil tankers suspected of being ‘shadow’ tankers transporting Russian oil through their territorial waters to provide documentation showing adequate maritime insurance. Upon failing to do so, having been identified as a ‘shadow’ tanker, they should be added to the OFAC, UK, and European sanctions list. This policy could limit Russia’s ability to transport its oil on ‘shadow’ tankers, which are not required to comply with the oil price cap policy.

- To strengthen the integrity of maritime operations, it is imperative that the International Maritime Organization (IMO) revises its guidelines to enhance transparency regarding maritime insurance. The IMO should mandate that flag states require shipowners and insurers to publicly disclose key financial information, including insurer solvency data, credit ratings from recognized agencies, and audited financial statements. Maritime authorities of coastal states should be legally able and encouraged to detain tankers that fly false flags which therefore pose environmental and security threats.

Relevant reports:

| Note on methodology:

This monthly report uses CREA’s fossil shipment tracker methodology. The data used for this monthly report is taken as a snapshot at the end of each month. The data provider revises and verifies data on trades and oil shipments throughout the month. We subsequently update this verified data each month to ensure accuracy. This might mean that figures for the previous month change in our updated subsequent monthly reports. For consistency, we do not amend the previous month’s report; instead, we treat the latest one as the most accurate data for revenues and volumes. Russia’s daily revenues for commodities used in this report are derived as an average, using CREA’s pricing methodology. CREA’s estimates of the impact of a revised and lowered price cap have been updated since February 2025. These numbers are a more accurate representation of the revenue losses Russia would incur. Our earlier numbers severely underestimated the impact of a lower price cap due to a bug that we identified that mislabelled commodities in our model. |