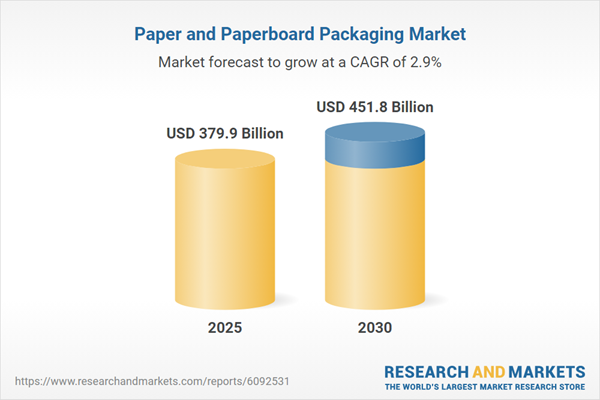

The global paper and paperboard packaging market, valued at USD 379.9 billion in 2024, is projected to reach USD 451.8 billion by 2030, growing at a CAGR of 2.9%. This rise is fueled by increasing environmental consciousness, regulatory bans on single-use plastics, and the expansion of e-commerce necessitating eco-friendly packaging. The glassine & greaseproof segment leads with the highest growth, favored for its sustainable, food-safe properties. Flexible paper also shows strong growth, meeting demands for recyclable, high-performance options. Dominating the market share, the Asia Pacific region benefits from urbanization and robust consumer demand. Key players include Mondi Group, International Paper, and Smurfit Kappa.

Paper and Paperboard Packaging Market

Paper and Paperboard Packaging Market

Dublin, July 14, 2025 (GLOBE NEWSWIRE) — The “Paper and Paperboard Packaging Market by Grade, Type, Source, Pulping, Application, & Region – Global Forecast to 2030” report has been added to ResearchAndMarkets.com’s offering.

The market for paper and paperboard packaging was valued at USD 379.9 billion in 2024, and it is projected to reach USD 451.8 billion by 2030, at a CAGR of 2.9 %

The report is expected to help the market leaders/new entrants in this market share the closest approximations of the revenue numbers of the overall paper and paperboard packaging market and its segments and subsegments. This report is projected to help stakeholders understand the competitive landscape of the market, gain insights to improve the positions of their businesses, and plan suitable go-to-market strategies. The report also aims to help stakeholders understand the pulse of the market and provides them with information on the key market drivers, challenges, and opportunities.

The demand for paper & paperboard packaging is steadily rising due to stricter regulations to reduce the use of plastic and growing environmental consciousness. Many governments now forbid or restrict the use of single-use plastics, which is encouraging companies to use more ecologically friendly alternatives, such as packaging made of paper.

The rapid expansion of e-commerce has increased demand for packaging that is both, recyclable and robust enough to support branding through printability. The food and beverage industry is witnessing a surge in the use of biodegradable, food-safe materials in response to consumer preferences for environmentally conscious packaging.

Mondi Group (UK), International Paper (US), Smurfit Kappa (Ireland), NIPPON PAPER INDUSTRIES CO., LTD. (Japan), Amcor (Switzerland), Oji Holdings Corporation (Japan), ITC Limited (India), Metsa Group (Finland)., Clearwater Paper Corporation (US), and Packaging Corporation of America (US) are some of the key players in the paper and paperboard packaging market.

It is expected that the Asia Pacific will continue to account for a majority of the market share within the paper and paperboard packaging market during the forecast period as well due to many factors such as rapid industrialization, urbanization, and increased consumer demand in economic powerhouses, such as China, India, Indonesia, and Vietnam. The growing middle class and increasing populations lead to increased consumption in food, beverage, personal care, and e-commerce categories, and will become extraordinarily dependent on sustainable, efficient, and affordable packaging solutions for the delivery of products such as food and beverages.

China and India are investing extensively in packaging infrastructure and adopting highly advanced technologies as the paper & paperboard industry is one of the highest performing sectors of their economies. Given its abundance of raw materials, low production costs, and strong export capabilities, the Asia Pacific is poised to manage and control worldwide growth and catch up with or stay ahead of developments in consumer markets, environmental policies, and economic engines.

Based on Grade, the glassine & greaseproof segment is expected to account for the highest CAGR during the forecast period.

Over the forecast period the glassine and greaseproof segment is expected to grow at the highest CAGR in the paper and paperboard packaging market by grade. This is driven by the increasing demand for sustainable, food-safe, and oil-resistant packaging solutions, especially in the foodservice and bakery segments.

Glassine, with its smooth, glossy, and air-tight properties, is used for wrapping confectionery, bakery items, and grease-sensitive products. Its biodegradability and recyclability make it a preferred alternative to plastic-based wraps in line with global environmental goals. Greaseproof paper’s oil and moisture resistance makes it ideal for fast food, snacks, and convenience meals. With increasing regulatory pressure to reduce plastic and growing consumer awareness of eco-friendly packaging, manufacturers are increasingly adopting these specialty papers, and hence, their market share is growing and driving segment growth.

Based on type, the flexible paper segment accounted for the highest CAGR during the forecast period

The flexible paper segment is expected to grow at the highest CAGR in the paper & paperboard packaging industry during the forecast period, with its sustainable and high-performance interchangeable functionality continuing to flourish in the food, personal care, and retail sectors. As regulations continue to push legislation to move away from the consumption of plastic, manufacturers are exploring flexible paper alternatives to pouches, wraps, and sachets that provide environmental benefits and functional performance.

The increased on-the-go consumption patterns and preference for packaged snack and single-serve items create demand for lightweight, recyclable, and compostable forms of packaging. Flexible paper meets the demands for high-end printing specifications that showcase brand and can also have barrier coatings applied to improve moisture and grease resistance while retaining recyclability. As the demand for sustainable packaging products increases among consumers, combined with the positive advances taking place with coating technologies, flexible paper is positioned well to have an edge as a preferred choice, especially in applications where sustainability and shelf appeal factor into the decision-making parameters.

Based on application, the food segment to hold the largest market share during the forecast period

The food application category is expected to capture the largest market share in the paper and paperboard packaging market over the forecast period as a result of increased growth in demand for sustainable, safe, and functional packaging for a vast range of food applications. The use of paperboard cartons, trays, wraps, and containers is increasing for dry foods, frozen meals, baked goods, snacks, and ready-to-eat food, which all need protection but need good printing surfaces for quality printing and branding.

Also, advances in barrier coatings and moisture resistance have opened the doors to increasing paperboard applications that were previously occupied by plastic and foil without compromising food safety and shelf life. The increasing use of eco-friendly ‘in a consumer’s mind’ packaging solutions, particularly in developed economies, and the rise in the consumption of packaged and convenience foods in emerging economies are supporting further growth in this segment. Included in the continued use of paper & paperboard packaging is that the food industry is a huge volume-based sector that requires consistency, cost savings, and packaging that meets regulations. It is clear that the food application category will remain the most significant contributor to the growth of paper & paperboard packaging globally.

Key Attributes:

Report Attribute

Details

No. of Pages

316

Forecast Period

2025 – 2030

Estimated Market Value (USD) in 2025

$379.9 Billion

Forecasted Market Value (USD) by 2030

$451.8 Billion

Compound Annual Growth Rate

2.9%

Regions Covered

Global

Market Overview

Drivers

Rising Consumer Preference for Sustainable Paper-based Packaging Solutions

Recyclability of Paper & Paperboard Key Driver in Adoption of Sustainable Packaging

Growth in Demand for Recyclable Mailers and Corrugated Inserts in E-Commerce Packaging

Legislative Bans on Single-Use Plastics Fueling Substitution with Fiber-based Formats

Restraints

Price Volatility of Raw Materials

Opportunities

Challenges

Industry Trends

Trends/Disruptions Impacting Customer Business

Pricing Analysis

Average Selling Price Trend of Key Players, by Type, 2024

Pricing Analysis Based on Region

Value Chain Analysis

Ecosystem Analysis

Technology Analysis

Key Technologies

Calendering

Pulping Technology

Complementary Technologies

Adjacent Technologies

Case Study Analysis

Green Bay Packaging’s Digital Transformation

Smurfit Kappa’s Collaboration with Priwatt

Metsa Board’s Adoption of 3Dexperience Platform

Company Profiles

Mondi Group

International Paper

Smurfit Kappa

Nippon Paper Industries Co. Ltd.

Amcor

Oji Holdings Corporation

Itc Limited

Metsa Group

Clearwater Paper Corporation

Packaging Corporation of America

Klabin SA

Sappi Ltd

Orcon Industries Corp.

Proampac

Trident Paper Box Industries

Stora Enso

Tgi Packaging Pvt. Ltd.

Saica

Releaf Paper

Athar Packaging Solutions Pvt. Ltd.

Ecoenclose Inc.

Coveris

Epac Holdings, LLC.

Edpack Karunia Persada, Pt.

Adeera Packaging Pvt. Ltd.

For more information about this report visit https://www.researchandmarkets.com/r/19mdsi

About ResearchAndMarkets.com ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900