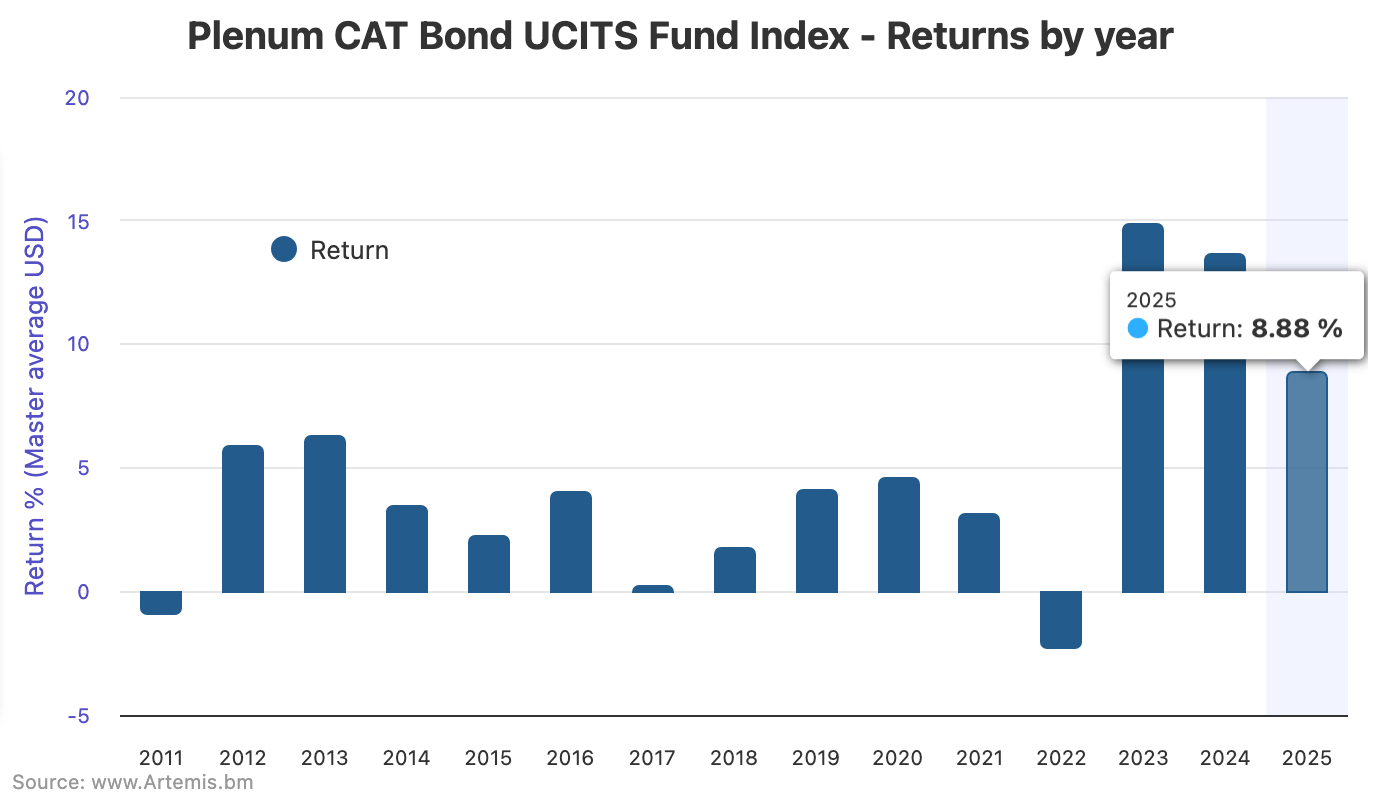

Catastrophe bond investment funds in the UCITS format have continued to deliver strong returns for their investors through October, with the average 2025 year-to-date return for these cat bond funds running at 8.88% by the end of that month, according to the latest data from the Plenum CAT Bond UCITS Fund Indices.

Previously, the UCITS cat bond fund sector was running at an average return of 7.25% for the year to September 26th.

Since, then UCITS cat bond funds have on average added 1.51% in returns through the period to October 31st, a very strong few weeks of performance for the asset class.

Performance has been driven by coupons and spread developments in the catastrophe bond market, with some cat bond funds seeing near record monthly performance during the last two months.

Reviewing monthly performance for 2025 year-to-date, the Plenum CAT Bond UCITS Fund Indices delivered a 0.40% return for January, 0.32% for February, 0.56% for March, 0.28% for April, 0.52% for May, 0.58% for June, 1.09% for July, 1.34% for August and 1.38% for September up to the 26th.

Now, the latest data for the Plenum CAT Bond UCITS Fund Indices shows that from September 26th through to the end of October 2025 saw the average return across the group of UCITS catastrophe bond funds reach 1.51%, as the run-rate of returns continues to be strong.

The year-to-date average return of 8.88%, as of October 31st, demonstrates the continued attractiveness of the catastrophe bond asset class, while some funds have fared better and are nearing double-digits at this stage of the year, we understand.

For the full-year 2025, double-digits remains in sight for this index of UCITS catastrophe bond fund performance.

Without doubt, unless there is a major loss event then 2025 will be the third strongest year for the index in its history, by quite a margin.

For the period of September 26th through October 31st, lower-risk cat bond funds fared slightly better at 1.53%, while the higher-risk cat bond funds averaged a 1.49% return.

Year-to-date, higher risk UCITS cat bond funds averaged 8.94% while the lower-risk cohort averaged 8.90%.

On a rolling twelve month return basis, the average for the index stands at 11%, while for lower-risk cat bond funds it is 10.56% and higher-risk 11.42%.

These levels of performance remain very attractive historically for the catastrophe bond asset class and are more than adequate to continue driving investor interest.

Given the recent softening of pricing, across reinsurance in general and in the pricing of recent catastrophe bond issues though, it is hard to envisage double-digit returns being sustained on the rolling twelve-month basis for too much longer and that metric may revert to single digits in 2026 it currently seems.

Analyse UCITS cat bond fund performance, using the Plenum CAT Bond UCITS Fund Indices.

Analyse UCITS catastrophe bond fund assets under management using our charts here.

Analyse catastrophe bond market yields over time using this chart.