Introduction

The Soybean Innovation Lab (SIL) introduces readers to the question whether Sub Saharan Africa (SSA) presents a new market opportunity for US soybean growers. Over the next three weeks SIL and farmdoc will deliver three articles on the topic of Africa as a potential export market for US soybeans. The African market presents a very complex landscape. While it is large, diverse, and growing rapidly, there exists great uncertainty, significant business risks, and demand for soybean and associated products are just beginning to emerge.

This first article in the series focused on the larger food and oil trends dominating the African continent (see farmdoc daily from November 13, 2025). Today’s article delves into the import flows of soybean, oil, and meal into Africa. The third article will wrap up the series by outlining four specific country examples – Egypt, Ghana, Nigeria, and Tanzania – touching on their imports of soy and soy products, logistics infrastructure, and existing policies on genetically modified soybean imports. The third and final article will also include a relevant literature review on the subject of soy trade and Africa.

Soy Import Demand in SSA

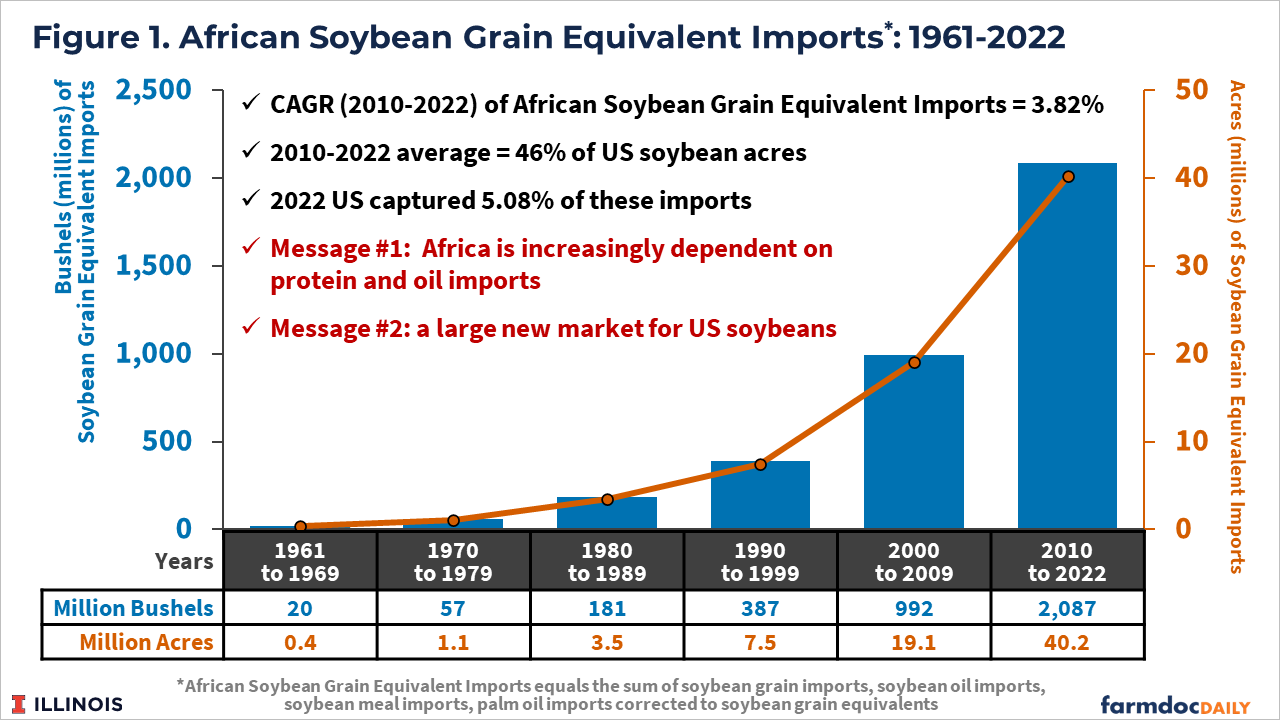

Is SSA soy import demand significant, or at least potentially significant? The answer is yes. Soy product demand is potentially very significant. Using the soybean equivalent import metric, Africa imported a soybean equivalent of 2.1 billion bushels on average per year for the period 2010-2022. That equals the production of about 40 million acres, about 47% of US plantings (see Figure 1). Most of that value results from palm oil imports (64%). Soybean oil, meal, and grain imports amount to 21%, 8%, and 7%, respectively.

The Africa soybean grain import equivalent metric comprises the sum of: 1) soybean imports, 2) soybean oil imports, 3) soybean meal imports, and 4) palm oil imports all corrected to soybean grain equivalents. That is, based on current soy and palm product imports, were it grain, the metric captures how much grain would theoretically be demanded by Africa’s processors and manufacturers. The grain equivalent metric melds both current import activity and the potential to expand soybean export demand by taking market share from palm oil. The equivalent metric, when measured in bushels and acres also allows comparison with US production.

These imports grew at a compound annual growth rate (CAGR) of 3.82% between 2010 and 2022. Soybean grain imports lead the group growing at a CAGR of 8.04%, with palm oil, soybean oil, and soybean meal growing at 4.46%, 2.05%, and -0.34%, respectively.

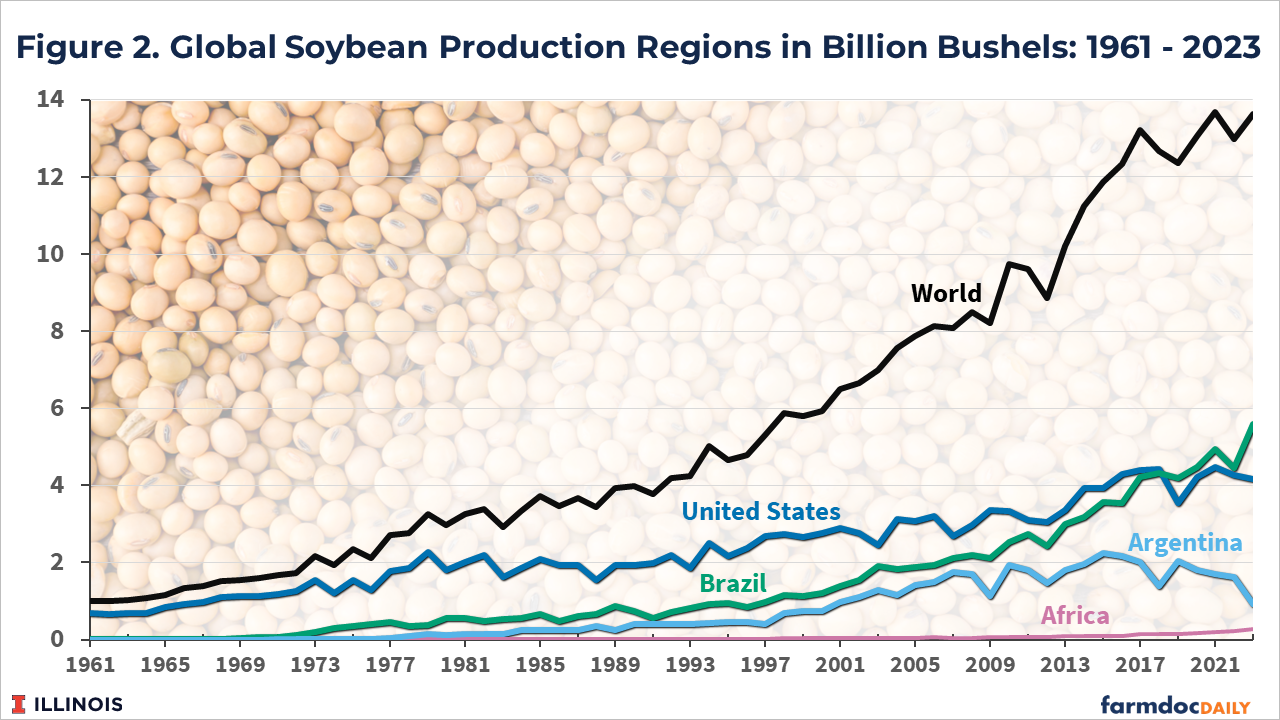

African soybean production currently amounts to 270 million bushels or about 6% of US production and 2% of global production (see Figure 2). Global soybean output over the last ten years has grown at a CAGR of 2% while African production has grown at an annual rate of 11%. While growing rapidly, Africa will remain far from being self- sufficient in the future and require significant imports. For example, forecasts to 2050 show Africa would still only be able to supply 35% of its current soybean equivalent import demand, even assuming the current soybean production growth rate.

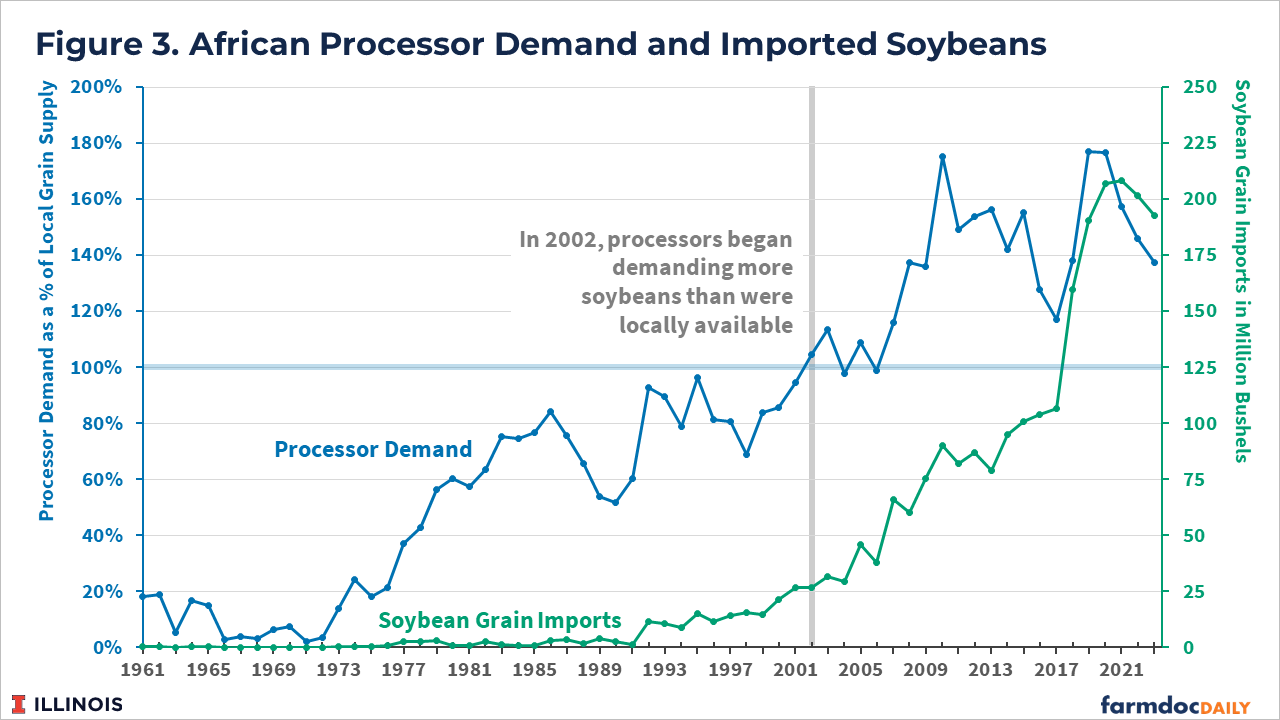

Finally, African soybean processors in the 1960’s had very little use for soybean, processing less than 20% of the region’s soybean crop to produce food oil (see Figure 3). Over time, processors have expanded capacity and by 2002 the industry switched from an under capacity position to overcapacity where local supplies were not sufficient to meet demand resulting in significant acceleration in the imports of soybean grain. Most recently, processors are 40-60% overcapacity relative to domestic supply and import about 200 million bushels of soybeans to keep their factories operating. Demand for soybean grain imports since 2010 has been quite fast with a compound annual growth rate of just over 8%.

Note: The Soybean Innovation Lab (SIL) at the University of Illinois is the world’s leading organization focused on establishing soybean as the feed, oil, industrial materials, and biofuels standard in Sub Sharan Africa (SSA). SIL’s strong network across 31 countries, experienced team, track record of success, and partners on the ground support clients looking to serve the fastest growing and a potentially large new soy market.