SAVE $500: As of March 11, the DJI Mini 5 Pro Fly More Combo is on sale for $1,099 at Amazon. That’s a 31% discount on the list price.

…

SAVE $500: As of March 11, the DJI Mini 5 Pro Fly More Combo is on sale for $1,099 at Amazon. That’s a 31% discount on the list price.

Before a close childhood friend introduced tech entrepreneur Dan Haddad to Inward founder Sofia Alva, she declared the two were just “too similar not to meet.” Dan decided to finally reach out and joined one of Sofia’s online courses on…

More than a decade on from his Exeter Chiefs debut, winger Olly Woodburn is capping off an already impressive season by penning a new deal.

The near 200-cap Exeter man, who already has two Gallagher PREM titles and an Investec Champions Cup on his…

Summary

Attaullah Tarar says Operation Ghazab lil Haq against militants continues, with hundreds killed, checkpoints destroyed and aerial strikes targeting militant hideouts…

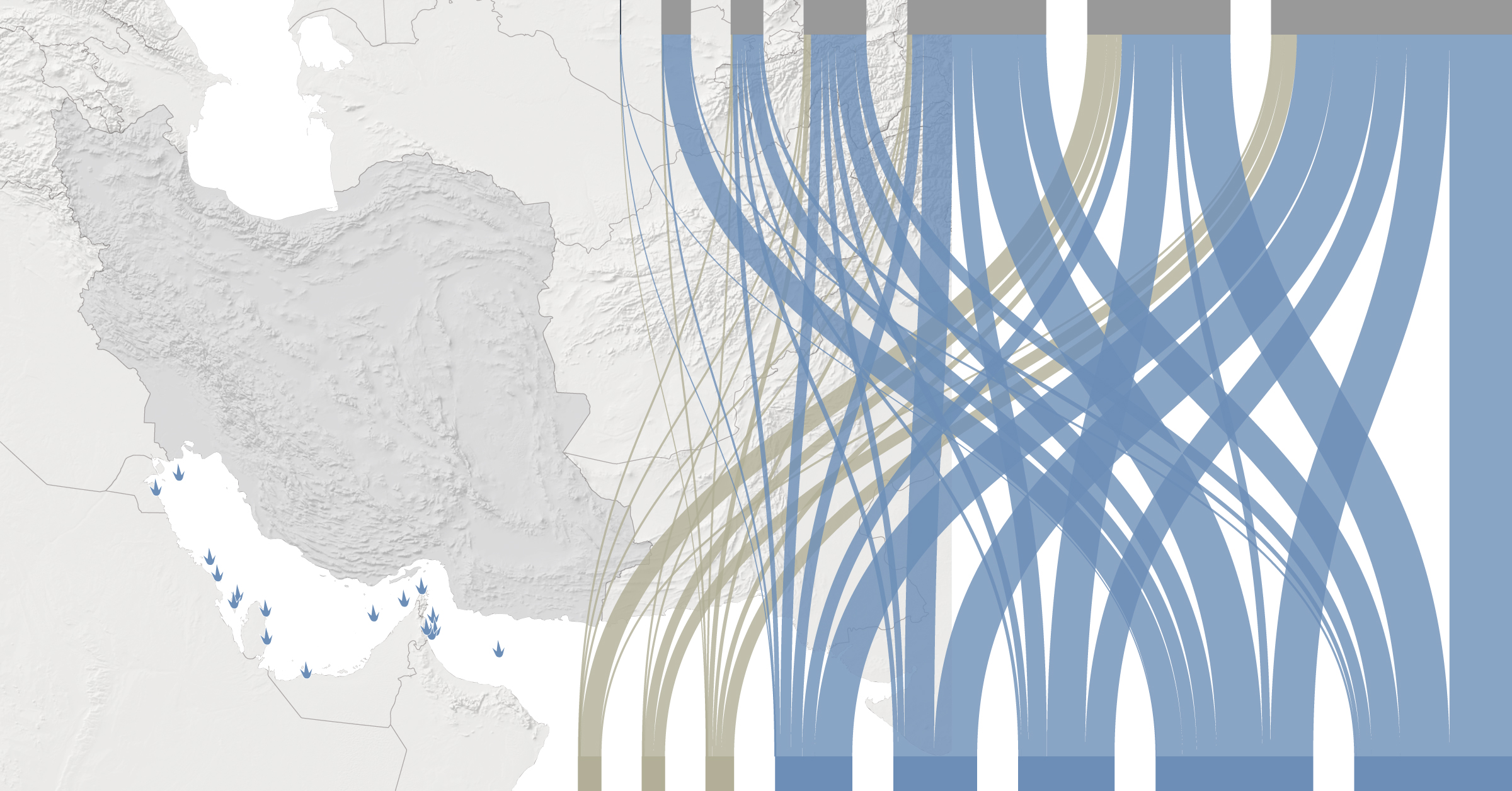

The U.S.-Israeli war on Iran has effectively shut the Strait of Hormuz, the narrow shipping lane between Iran and Oman through which around a fifth of the world’s daily oil and liquefied natural gas (LNG) supply passes. Top Middle East oil…

Madrid recalls ambassador amid rising diplomatic tensions and criticism of US-Israeli actions in Iran.

Published On 11 Mar 2026

Insect-derived lipids are proving to be a functional and cost-effective delivery system for naturally sourced vitamin D3 that can address supply chain constraints and sustainability pressures. Nutriearth, a specialist extracting the nutrient from…