- Cyber Insurance Market Outlook 2026: Resilient Earnings, Tougher Competition, Pockets Of Growth S&P Global

- Beazley committed to US cyber but warns market pricing ‘not sustainable’ The Insurer

- Why insurers must take charge on cybersecurity Business Daily

- UK specialty insurer Beazley lowers written premiums outlook Global Banking And Finance Awards®

- Cyber Insurance Quotes: Compare Rates Online HowMuch.net

Category: 3. Business

-

Cyber Insurance Market Outlook 2026: Resilient Earnings, Tougher Competition, Pockets Of Growth – S&P Global

-

Hydrogen Europe

Hystar announces strategic collaboration with McDermott to develop 100 MW green hydrogen plant design

Hystar AS (www.hystar.com), a leading provider of the world’s most efficient PEM electrolysers, today announced a strategic collaboration with McDermott (www.mcdermott.com) to develop a comprehensive 100-megawatt (MW) green hydrogen plant design. This collaboration marks a significant milestone in Hystar’s mission to accelerate global deployment of its large-scale green hydrogen solution.

Under the agreement, Hystar will provide its proprietary, high-efficiency and high-safety PEM electrolyser technology. McDermott will leverage its extensive global expertise as an engineering, procurement and construction (EPC) provider for major energy infrastructure. With more than a century of engineering excellence, McDermott has delivered numerous large-scale hydrogen, ammonia, and low-carbon projects. Its portfolio includes pre-FEED, FEED and EPC execution for blue and green hydrogen facilities, ammonia plants, hydrogen hubs, and modularized energy projects worldwide.

Continue Reading

-

Rate the Raters 2025 | EMEA/APAC webinar

The ERM Sustainability Institute is pleased to present the latest Rate the Raters 2025: ESG Ratings in Evolution – results of the Corporate Survey.

To help you make sense of the findings and their implications for your business, ERM will host a webinar on February 05 (Europe and Asia friendly). Join us as we unpack the results and explore what they mean for shaping effective ESG strategies.

Why ESG Ratings Matter More Than Ever

ESG ratings remain integral to corporate sustainability strategies despite ongoing challenges with 88% of companies planning to continue engaging with them. At the same time, new regulations are reshaping the landscape by requiring increased transparency. Strategic engagement is also evolving, as companies are actively engaging with fewer raters.

What you’ll learn:

- Which ESG raters are seen as the most useful and highest quality

- What drived engagement with rating agencies

- Regional differences in corporate perspectives

Why Attend?

This is your chance to hear directly from ERM experts and explore how ESG ratings are shifting.

Continue Reading

-

Milan Nedeljković appointed new Chairman of the Board of Management of BMW AG

- Oliver Zipse will leave the Board of Management after the Annual

General Meeting in May 2026 as planned - Nicolas Peter: „Nedeljković convinces with strategic foresight,

strong implementation skills, and entrepreneurial thinking“ - Appreciation to Oliver Zipse: „Significant contribution to BMW“

Munich. Dr.-Ing. Milan Nedeljković will assume the

role of Chairman of the Board of Management of BMW AG effective on 14

May 2026. The company’s Supervisory Board took this decision today.

Following the successful launch of the Neue Klasse, Nedeljković will

succeed Oliver Zipse, who has been a member of the Board of Management

of BMW AG for more than ten years and has served as its Chairman since

August 2019. The Supervisory Board extends its sincere thanks to

Oliver Zipse for his outstanding achievements for the BMW Group.“Milan Nedeljković convinces with his strategic foresight,

strong implementation skills, and entrepreneurial thinking. He stands

for very focused management of resources—whether financial or

ecological,” said Dr. Nicolas Peter, Chairman of the Supervisory

Board of BMW AG. ” Milan Nedeljković inspires people with ideas,

unites them behind shared values, and thereby motivates them to

realize peak performance. This is a crucial leadership quality to

maintain the BMW Group’s successful course in this time of transformation.”In 2023, Oliver Zipse’s contract as Chairman of the Board of

Management of BMW AG was extended beyond the usual retirement age

until 2026. Subsequently, he will leave the Board of Management as

planned after the Annual General Meeting on 13 May 2026, concluding a

total of 35 years with the BMW Group.“Oliver Zipse has made a significant contribution to the BMW

Group and deserves our sincere gratitude. He has led BMW through

global crises such as the COVID-19 pandemic and represents the Neue

Klasse as the largest strategic project in the company’s

history,” said Peter. “Oliver Zipse has always prioritized

BMW’s success. He consistently took a clear stance—even in the face of

great external headwinds—and thus kept the company on track during

turbulent times.”Milan Nedeljković, the designated Chairman of the Board of

Management, has been a member of the Board of Management of BMW AG

since 2019 and is currently responsible for the Production division.

The 56-year-old began his professional career at BMW as a Trainee in

1993 and has accumulated extensive international experience. He has

held senior leadership positions at Plant Oxford, as Managing Director

Plant Leipzig and Munich and as Senior Vice President Corporate

Quality. His contract as Chairman of the Board of Management will

extend into 2031.Dr. Martin Kimmich, Chairman of the Global Works Council and deputy

Chairman of the Supervisory Board, said: “Milan Nedeljković is

held in high regard by and enjoys the trust of BMW’s workforce.

Together with him, we look forward to continuing the long tradition of

cooperative collaboration between the Works Council and corporate

management as a foundation for our BMW success story.”If you have any questions, please contact:

BMW Group Corporate Communications

Max-Morten Borgmann, Head of Communications BMW Group, Finance, Sales

Telephone: +49 89 382-24118

Email: max-morten.borgmann@bmwgroup.com

Media website: www.press.bmwgroup.com/deutschland

Email: presse@bmwgroup.com

The BMW Group

With its four brands, BMW, MINI, Rolls-Royce and BMW Motorrad, the

BMW Group is the world’s leading premium manufacturer of automobiles

and motorcycles and also provides premium financial and mobility

services. The BMW Group production network comprises over 30

production sites worldwide; the company has a global sales network in

more than 140 countries.In 2024, the BMW Group sold 2.45 million passenger vehicles and more

than 210,000 motorcycles worldwide. The profit before tax in the

financial year 2024 was € 11.0 billion on revenues amounting to €

142.4 billion. As of 31 December 2024, the BMW Group had a workforce

of 159,104 employees.The success of the BMW Group has always been based on long-term

thinking and responsible action. Sustainability is a key component of

the BMW Group’s corporate strategy – from the supply chain through

production to the end of the use phase of all products.www.bmwgroup.com

LinkedIn: http://www.linkedin.com/company/bmw-group/

YouTube: https://www.youtube.com/bmwgroup

Instagram: https://www.instagram.com/bmwgroup

Facebook: https://www.facebook.com/bmwgroup

X: https://www.x.com/bmwgroup

Continue Reading

- Oliver Zipse will leave the Board of Management after the Annual

-

Webinar: EU Green Deal Policies and their Relevance in Asia-Pacific

In December 2015, the Paris Agreement was adopted. It aims to limit the global average temperature increase to well below 2°C above pre-industrial levels, and to increase parties’ ability to adapt to the adverse impacts of climate change and make financial flows consistent with a pathway toward low GHG emissions and climate resilient development. Each party shall communicate, at five-year intervals, successively more ambitious NDCs.

At COP29 in Baku last year, a new collective quantified goal (NCQG) on climate finance, to at least USD 300 billion per year by 2035, was reached, calling on all actors to work together to scale up financing to developing countries for climate action from all public and private sources.

Meanwhile, it is expected that the next round of NDCs must deliver on the promise to ramp up renewables and transition away from fossil fuels. At the Bonn June Climate meetings in preparation of annual COP, the closing statement includes a renewed call for fossil fuel phase out, concerns about limited progress on technology and the need for a clear roadmap to the USD 1.3 trillion in climate finance to deliver concrete milestones. It also puts the most vulnerable at the center and supports a tripling of adaptation finance.

Expectations from COP30 in Belem are very high, including synthesis reports on NDCs and biennial transparency reports. While concerns about climate change are on the rise and negotiations will continue for many years to come, it is important to remind ourselves that climate change is not just about CO2; it is about overconsumption and irresponsible production, irresponsible extraction and use of material. If actions at individual level are important, it is through collective action for a common good, based on the principles of SCP and circular economy, that the fight against climate impacts and building the path towards sustainability can be achieved.

Guided by science and economy, policy makers can bridge the gap between what is possible and what is needed by knowingly advancing policies that will be well received by most, embracing pragmatism to build trust before handling the most serious and complicated issues, starting with what is possible, creating momentum and helping catalyze new technologies, new economics, and new politics, making accelerated change possible.

Webinar Session:

The EU SWITCH-Asia Policy Support Component and the European Environmental Bureau, are convening the webinar, Between Ambitions and Pragmatism for actionable climate outcomes: the circular economy enabler.

The objectives of the webinar are:

- To assess the key conclusions, decisions and directions from UNFCCC COP30 with special reference to integration of circular economy principles into climate mitigation and adaptation strategies.

- To explore how the circular economy-climate linkages could support the operationalization of the COP30 outcomes and their potential impacts to de-risk and attract public and private finance, thereby transforming markets and value chains towards low-carbon and climate-resilient economies.

- To discuss the policies, partnerships, and support mechanisms required to empower businesses, particularly SMEs, as central actors in implementing circular, low-carbon, and resilient solutions at scale.

- To discuss and derive concrete policy guidance and actionable strategies from the COP30 stocktake, focusing on how to effectively implement the material-CE-climate nexus for accelerated on-the-ground results.

Continue Reading

- To assess the key conclusions, decisions and directions from UNFCCC COP30 with special reference to integration of circular economy principles into climate mitigation and adaptation strategies.

-

Energy efficiency in buildings tops organizations’ infrastructure priorities: Siemens study | Press | Company

[{“nid”:0,”name”:”Products & Solutions”,”tid”:0,”url_str”:”https://www.siemens.com/global/en/products.html”,”alias”:”https://www.siemens.com/global/en/products.html”,”level”:1,”image”:{“fid”:false,”furl”:””},”options”:{“menu_icon”:{“fid”:false},”external”:true},”depth”:1,”parent”:false,”children”:[]},{“nid”:0,”name”:”Industries”,”tid”:1,”url_str”:”https://xcelerator.siemens.com/global/en/industries.html”,”alias”:”https://xcelerator.siemens.com/global/en/industries.html”,”level”:1,”image”:{“fid”:false,”furl”:””},”options”:{“menu_icon”:{“fid”:false},”external”:true},”depth”:1,”parent”:false,”children”:[]},{“nid”:0,”name”:”Company”,”tid”:2,”url_str”:”https://www.siemens.com/global/en/company.html”,”alias”:”https://www.siemens.com/global/en/company.html”,”level”:1,”image”:{“fid”:false,”furl”:””},”options”:{“menu_icon”:{“fid”:false},”external”:true},”depth”:1,”parent”:false,”children”:[]}]

Continue Reading

-

Fixed-Duration Regimens Noninferior to Continuous in CLL – Medscape

- Fixed-Duration Regimens Noninferior to Continuous in CLL Medscape

- Fixed-duration therapy works as effectively as continuous treatment for chronic lymphocytic leukemia news-medical.net

- Fixed-Duration Venetoclax Combos Show Noninferior PFS to Ibrutinib in CLL CancerNetwork

- In CLL, Fixed-Duration Venetoclax Combos Are Equal to Continuous Ibrutinib in Head-to-Head Comparison AJMC

- Fixed-Duration Venetoclax (Venclexta) Matches Continuous Ibrutinib (Imbruvica) in Frontline CLL Oncology News Central

Continue Reading

-

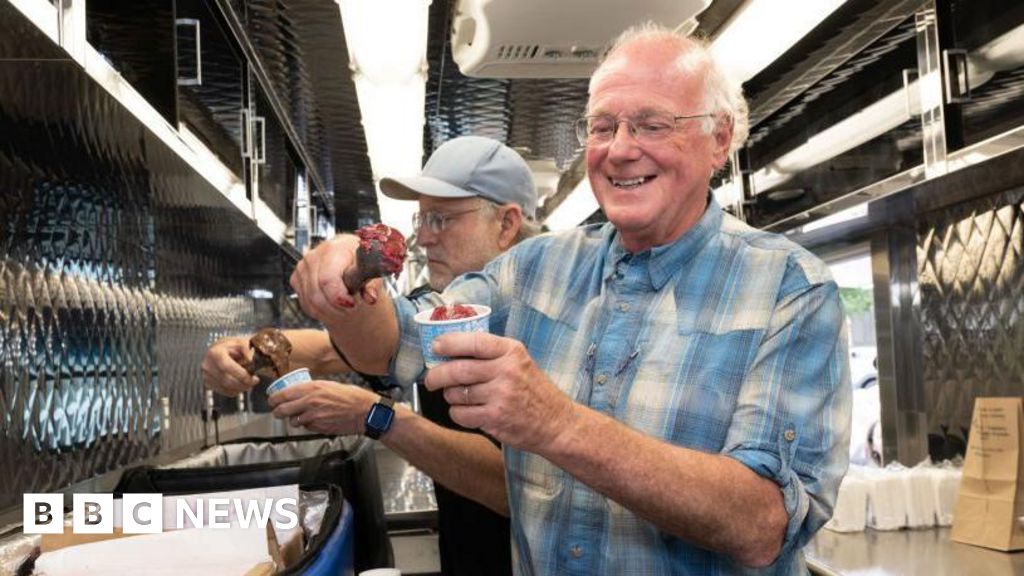

Ben & Jerry’s brand could be destroyed, says co-founder

Ben & Jerry’s will be destroyed as a brand if it remains with parent company Magnum, the company’s co-founder Ben Cohen has told the BBC.

His remarks are the latest in a long-running spat between the ice cream brand and its parent company over its ability to express its social activism and the continued independence of its board.

It comes on the day that the Magnum Ice Cream Company (TMICC) started trading on the European stock market – spinning off from owner Unilever.

A spokesperson for Magnum said the firm wanted to build and strengthen Ben & Jerry’s “powerful, non-partisan values-based position in the world”.

Ben & Jerry’s was sold to Unilever in 2000 in a deal which allowed it to retain an independent board and the right to make decisions about its social mission.

Since the sale there have been deepening clashes between the Vermont-based brand and Unilever, with this conflict now inherited by Magnum.

In 2021, Ben & Jerry’s refused to sell its products in areas occupied by Israel, resulting in its Israeli operation being sold by Unilever to a local licensee, and in October, Ben Cohen said it was prevented from launching an ice cream which expressed “solidarity with Palestine”.

Last month, ahead of its spin off from Unilever, Magnum said the chair of Ben & Jerry’s board Anuradha Mittal, who has held the position since 2018, “no longer meets the criteria to serve” – saying this was the result of an internal audit.

A spokesperson for Magnum said it had found “a series of material deficiencies in financial controls, governance and other compliance policies, including conflicts of interest”.

“So far, the trustees have not fully addressed the deficiencies identified,” they said.

In a statement to Reuters, Ms Mittal said: “The so-called audit of the foundation was a manufactured inquiry – engineered to attempt to discredit me.

“It is important to understand that this is not simply an attack on me as chair. It is Unilever’s attempt to undermine the authority of the Board itself.”

The BBC has contacted Ben & Jerry’s to request this statement.

Mr Cohen said Magnum “has no standing to determine who the chair of the independent board should be”.

“Therefore, by trying to [change the chair of the board], I would say that Magnum is not fit to own Ben & Jerry’s,” he added.

Mr Cohen called for either the business to be “owned by a group of investors that support the brand and want to encourage the values” or for Magnum to make a “180 degree turn around and say they support the chairman of the independent board”.

Ahead of the spin off on Monday, news agency Reuters reported that Ms Mittal said she had no plans to step down from the board.

Ben Cohen remains an employee of Ben & Jerry’s and the brand’s most high-profile spokesperson.

He told the BBC he feared under the current ownership the ice cream maker’s “loyal” followers would be lost for good.

“If the company continues to be owned by Magnum, not only will the values be lost, but the essence of the brand will be lost,” he said.

On Sunday, Magnum’s chief executive Peter ter Kulve told the Financial Times the Ben & Jerry’s founders were in their seventies and “at a certain moment they need to hand over to a new generation”.

Jerry Greenfield, Mr Cohen’s co-founder, left the ice cream maker in September after almost half a century at the firm – citing concerns about the stifling of its social mission.

“It’s absurd,” said Mr Cohen.

“This is about values and abiding by a legally binding agreement.”

Mr Cohen added investors in Magnum were being asked to pay a premium for the Ben & Jerry’s brand “because it has such a loyal following”.

“As they destroy Ben and Jerry’s values, they will destroy that following and they will destroy that brand,” he said.

“It’ll become just another piece of frozen mush that just going to lose a lot of market share.”

A spokesperson for Magnum said Ben & Jerry’s was “not for sale” and it had “always respected” the brand’s commitment to continue its “social mission”.

The demerger of Unilever’s ice cream business saw primary shares in Magnum open at €12.20 (£10.66) – down on the expected €12.80 (£11.18) reference price set by the EuroNext exchange in Amsterdam. But it bounced back up by 1.3% at close of trading.

The spin off means Magnum is now the world’s biggest standalone ice cream business.

Continue Reading

-

Global Fashion Agenda Grows Efforts to Combat Textile Waste through New Initiative in Türkiye

Today, Global Fashion Agenda (GFA) announced the launch of the Circular Fashion Partnership: Türkiye, a new initiative that aims to support the development of a circular textile system in the country by capturing and recycling post-industrial textile waste. Announced during Sustainability Talks Istanbul, the partnership is led by GFA in collaboration with national lead Rematters, supported by implementation partners Reverse Resources, Closed Loop Fashion, and Circle Economy Foundation and funded by H&M Foundation.

Set to commence in early 2026, the Circular Fashion Partnership: Türkiye aims to establish textile waste management systems within factories, enhance traceability through digital tools, and connect manufacturers with recyclers to ensure higher-value recovery of post-industrial textile waste. The programme will also provide supplier support on compliance with evolving policy frameworks and foster national collaboration to drive systemic change. GFA is now calling on brands producing in Türkiye to participate in the programme.

As one of the world’s leading apparel manufacturing hubs, Türkiye is uniquely positioned to scale textile-to-textile recycling due to its vertically integrated industry, proximity to the EU, and increasing regulatory pressure to reduce waste and emissions. The Circular Fashion Partnership: Türkiye will build on these strengths by developing scalable models for improved waste segregation, fibre-to-fibre recycling, and domestic recovery routes that reduce dependency on virgin materials and landfill.

The programme is part of the Global Circular Fashion Forum (GCFF), a wider initiative led by Global Fashion Agenda to advance post-industrial textile recycling through local partnerships in manufacturing regions. Building on successful implementation in Bangladesh, Cambodia, and Indonesia, the Circular Fashion Partnership: Türkiye becomes the fourth national programme to deploy this model — which has already digitally traced over 21,000 tonnes of textile waste and connected more than 100 factories and 20 global brands to recycling partners across its programmes. The locally owned and led partnership in Türkiye will be customised to the regional context, while drawing on best practices from other countries. Throughout 2026, the Circular Fashion Partnership: Türkiye will engage stakeholders across the value chain via targeted activities including on-site waste management assessments, training and capacity building through a Train-the-Trainer model, recycling pitch sessions and matchmaking events, as well as roundtables and policy dialogues with key national actors. In doing so, the partnership aims to support Türkiye in futureproofing its textile ecosystem, unlock economic value from waste, and contribute to a just, circular transition in one of the industry’s most influential sourcing regions.

Continue Reading

-

Treasury yields little changed as markets await jobs report

U.S. Treasury yields were little changed as investors anticipate jobs and employment data coming out later in the day.

The 10-year Treasury yield was relatively flat at 4.178%. The 30-year Treasury yield slid by less than one basis point to 4.81%, as did the 2-year Treasury yield to 4.781%.

One basis point is equivalent to 0.01%, and yields and prices share an inverse relationship.

The Job Openings and Labor Turnover Summary (JOLTS) Job Openings report for October is slated to come in at 7.15 million, according to LSEG estimates.

Market participants are expecting that the Federal Reserve will lower its benchmark interest rate at its final meeting of the year.

“We believe a December rate cut will work to support equity markets and credit quality,” Eastspring Investments wrote in a note.

If Fed Chair Jerome Powell suggests that he views the Fed is now in a good enough place to skip the next few meetings to assess the economy, this would likely reinforce the current stability of the U.S. dollar and keep Treasury yields in their recent range, the economists added.

“In contrast, a more dovish message – keeping the prospect of a January rate cut alive – would likely weaken the USD and lead to a bearish steepening of the US Treasury curve,” the analysts noted.

Continue Reading