Category: 3. Business

-

Mars Receives Final Regulatory Approval and Moves to Close the Acquisition of Kellanova

Mars Receives Final Regulatory Approval and Moves to Close the Acquisition of Kellanova

McLean, Virginia, and Chicago, Illinois (December 8, 2025) – Mars, Incorporated, a family-owned, global leader in pet care, snacking and food and Kellanova (NYSE: K), a leader in global snacking, international cereal and noodles and North America frozen foods, today announced that Mars has received unconditional approval from the European Commission for its pending acquisition of Kellanova. As a result, all required regulatory approvals and clearances for the pending transaction have been obtained.

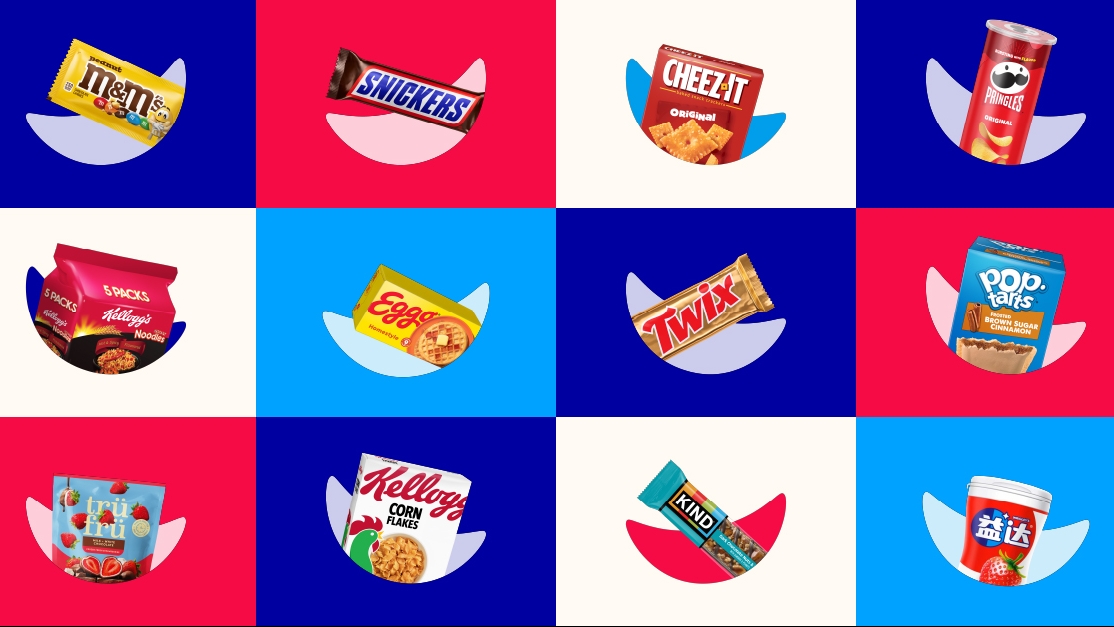

Mars and Kellanova anticipate closing the pending transaction on December 11, 2025, subject to the satisfaction or waiver of customary closing conditions. Upon close, Kellanova’s portfolio of snacking brands, which includes Pringles®, Cheez-It®, Pop-Tarts®, Rice Krispies Treats®, RXBAR® and Kellogg’s international cereal brands, will join the existing Mars Snacking portfolio, which includes beloved brands like SNICKERS®, M&M’S®, TWIX®, SKITTLES®, EXTRA® and KIND®.

Following the close of the pending transaction, Mars expects the combined Snacking business to generate around $36 billion in annual revenues, with a portfolio that includes 9 billion-dollar brands. Mars Snacking will continue to be headquartered in Chicago, IL and will operate in more than 145 markets, serving millions of consumers. Powered by a team of more than 50,000 Associates, it will operate 80 global production facilities and more than 170 retail outlets like Hotel Chocolat and M&M’S World.

“We are excited to have received final regulatory approval for the pending acquisition of Kellanova,” said Poul Weihrauch, CEO and Office of the President of Mars, Incorporated. “Our focus now turns to welcoming Kellanova employees to Mars and creating an even more innovative global snacking business that delivers greater choice and quality to more consumers around the world.”

“Today marks an extraordinary milestone and the culmination of years of work for many of our Associates,” said Andrew Clarke, Global President of Mars Snacking. “We can’t wait to welcome Kellanova talent to Mars and create a shared, global snacking leader with a beloved range of brands. We’ve said all along that Mars Snacking and Kellanova will be better together, building on the strength of our respective legacies and capabilities to unlock new possibilities and drive growth.”

Steve Cahillane, Chairman, President and CEO of Kellanova, said, “This combination will bring together two purpose-driven and principles-led companies. Serving as Kellanova’s Chairman, President and CEO has been a true honor, and I’m looking forward to seeing Kellanova people and brands thrive as part of Mars Snacking.”

The parties announced on August 14, 2024, that they had entered into a definitive agreement under which Mars agreed to acquire Kellanova. The pending transaction received Kellanova shareowner approval on November 1, 2024. The pending merger received the final of all 28 required regulatory approvals and clearances on December 8, 2025. Following the completion of the pending transaction, which remains subject to customary closing conditions, Kellanova’s common stock will be delisted and will cease trading on the New York Stock Exchange.

About Mars, Incorporated

Mars, Incorporated is driven by the belief that the world we want tomorrow starts with how we do business today. As an approximately $55bn, family-owned business with 150,000 Associates, our diverse portfolio of leading pet care products and veterinary services serve pets all around the world and our quality snacking and food products delights millions of people every day. We produce some of the world’s best-loved brands including ROYAL CANIN®, PEDIGREE®, WHISKAS®, CESAR®, DOVE®, EXTRA®, M&M’S®, SNICKERS® and BEN’S ORIGINAL™. Our international networks of pet hospitals, including BANFIELD™, BLUEPEARL™, VCA™ and ANICURA™ deliver high quality veterinary care and ANTECH ™ offers breakthrough capabilities in pet diagnostics.

For more information about Mars, please visit www.mars.com. Join us on Facebook, Instagram, LinkedIn and YouTube.

About Kellanova

Kellanova (NYSE: K) is a leader in global snacking, international cereal and noodles, and North America frozen foods with a legacy stretching back more than 100 years. Powered by differentiated brands including Pringles®, Cheez-It®, Pop-Tarts®, Kellogg’s Rice Krispies Treats®, RXBAR®, Eggo®, MorningStar Farms®, Special K®, Coco Pops®, and more, Kellanova’s vision is to become the world’s best-performing snacks-led company, unleashing the full potential of our differentiated brands and our passionate people.

For more detailed information about Kellanova, please visit https://www.Kellanova.com.

Forward-Looking Statements

This communication includes statements that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, each as amended, including statements regarding the proposed acquisition (the “Merger”) of Kellanova (the “Company”) by Mars, Incorporated (“Mars”), the expected timetable for completing the Merger, the expected benefits and other effects of the Merger, the integration of the companies, the combined business going forward and any other statements regarding the Company’s future expectations, beliefs, plans, objectives, financial conditions, assumptions or future events or performance that are not historical facts. This information may involve risks and uncertainties that could cause actual results to differ materially from such forward-looking statements. These risks and uncertainties include, but are not limited to: the timing to consummate the Merger and the risk that the Merger may not be completed at all or the occurrence of any event, change, or other circumstances that could give rise to the termination of the merger agreement, including circumstances requiring a party to pay the other party a termination fee pursuant to the merger agreement; the risk that the conditions to closing of the Merger may not be satisfied or waived; litigation relating to, or other unexpected costs resulting from, the Merger; legislative, regulatory, and economic developments; risks that the Merger disrupts the Company’s current plans and operations; the risk that certain restrictions during the pendency of the Merger may impact the Company’s ability to pursue certain business opportunities or strategic transactions; the diversion of management’s time on transaction-related issues; continued availability of capital and financing and rating agency actions; the risk that any announcements relating to the Merger could have adverse effects on the market price of the Company’s common stock, credit ratings or operating results; the risk that the proposed transaction and its announcement could have an adverse effect on the ability to retain and hire key personnel, to retain customers and to maintain relationships with business partners, suppliers and customers; the impact of macroeconomic conditions; other business disruptions; and consumers’ and other stakeholders’ perceptions of the Company’s brands. The Company can give no assurance that the conditions to the Merger will be satisfied, or that it will close within the anticipated time period.

All statements, other than statements of historical fact, should be considered forward-looking statements made in good faith by the Company, as applicable, and are intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. When used in this communication, or any other documents, words such as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “goal,” “intend,” “objective,” “plan,” “project,” “seek,” “strategy,” “target,” “will” and similar expressions are intended to identify forward-looking statements. These forward-looking statements are based on the beliefs and assumptions of management at the time that these statements were prepared and are inherently uncertain. Such forward-looking statements are subject to risks and uncertainties that could cause the Company’s actual results to differ materially from those expressed or implied in the forward-looking statements. These risks and uncertainties, as well as other risks and uncertainties that could cause the actual results to differ materially from those expressed in the forward-looking statements, are described in greater detail under the heading “Item 1A. Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 28, 2024 filed with the United States Securities and Exchange Commission (the “SEC”) and in any other SEC filings made by the Company. The Company cautions that these risks and factors are not exclusive. Management cautions against putting undue reliance on forward-looking statements or projecting any future results based on such statements or present or prior earnings levels. Forward-looking statements speak only as of the date of this communication or as of any earlier date when made or deemed to have been made, and, except as required by applicable law, no person is undertaking any obligation to update or supplement any forward-looking statements to reflect actual results, new information, future events, changes in its expectations or other circumstances that exist after the date as of which the forward-looking statements were made.

Contacts

Mars

Media:

Denise Young

Mars, Incorporated

denise.young@effem.com

MarsChristi O’Brien

Mars, Incorporated

christi.obrien@effem.comKellanova

Media:

Kellanova Media Hotline

Media.Hotline@kellanova.comInvestors

John Renwick, CFA

269-961-9050Brunswick Group

Jayne Rosefield / Monica Gupta

jrosefield@brunswickgroup.com / mgupta@brunswickgroup.com

Continue Reading

-

The role of pan-cytokeratin in tumor budding upgrading in malignant co

Introduction

Colorectal cancer (CRC) is one of the most common and lethal malignancies worldwide, particularly in developing countries. According to GLOBOCAN 2022, more than 1.93 million new CRC cases were diagnosed and approximately 904,000 deaths were recorded.1 With the increasing implementation of colorectal cancer screening programs, a greater number of lesions are now being detected at an early stage, including malignant colorectal polyps.2

A malignant colorectal polyp is defined as a polypoid lesion in which cancer cells invade the submucosa but do not extend into the muscularis propria, corresponding to pathological stage pT1.3 The detection of such lesions raises the need to balance two treatment strategies: endoscopic polypectomy versus segmental colectomy.4 This growing number of early-stage diagnoses highlights the urgent need for accurate assessment of prognostic factors to guide optimal treatment decisions. Although malignant polyps represent an early stage of colorectal cancer, previous studies have reported that the rate of lymph node metastasis ranges from 5.6% to 15.2% of cases are associated with lymph node metastasis, underscoring the critical role of prognostic evaluation in determining the risk of recurrence and the need for definitive surgical management.5–9 Several clinicopathological factors have been reported to be associated with lymph node metastasis in pT1 colorectal cancer, including tumor differentiation, lymphovascular invasion, depth of submucosal invasion, tumor budding, and tumor location.10,11

In the context of early-stage disease, tumor budding (TB)—defined as the presence of single cancer cells or small clusters of fewer than five cells at the invasive front—has been recognized as a significant independent prognostic factor.12 Several studies have demonstrated that in pT1 colorectal cancer, high-grade TB (≥5 buds per 0.785 mm2, corresponding to grade 2 or higher according to the International Tumor Budding Consensus Conference (ITBCC) criteria) is strongly associated with lymph node metastasis.8,12,13 Biologically, this phenomenon is closely linked to the epithelial–mesenchymal transition (EMT), a process that enables cancer cells to detach from the primary tumor and invade the surrounding stroma.14,15 Accordingly, international guidelines, including those from CAP and NCCN, have recommended the reporting of TB in pathology assessments of pT1 colorectal cancer to support prognostication and treatment decision-making.16,17

In routine practice, the assessment of TB on hematoxylin–eosin (H&E) slides is challenging. Tumor buds are often very small, easily mistaken for stromal elements, or obscured by inflammatory infiltrates and disrupted glandular fragments at the invasive front, leading to underestimation. Moreover, interobserver agreement in evaluating TB on H&E is generally only moderate to low.18–20 To address these limitations, several authors have proposed the use of immunohistochemistry with pan-cytokeratin (Pan-CK), which highlights isolated tumor cells and increases sensitivity in TB detection.21–23 Data from both research and clinical practice have shown that Pan-CK can reveal three- to four-fold more tumor buds compared with H&E,7 while also significantly improving reproducibility (with ICC increasing from moderate on H&E to high on Pan-CK).18,20,24,25 Although Pan-CK offers clear advantages in early-stage CRC and has been recommended by some authors for broader application, its routine use in all cases is not feasible, particularly in resource-limited settings, due to constraints of cost, time, and technical capacity. This raises an important question as to which factors determine the necessity of Pan-CK staining in order for TB upgrading to carry prognostic significance. Based on this rationale, the present study was designed to clarify the role of Pan-CK in evaluating TB in malignant colorectal polyps (pT1) and to identify independent predictors of TB upgrading after Pan-CK staining. We anticipate that our findings will provide scientific evidence to support selective use of Pan-CK in routine practice. This selective approach is particularly relevant for low-resource settings, thereby contributing to global oncology equity.

Materials and Methods

Patient Selection and Data Collection

This retrospective study included 265 patients who were initially diagnosed with colorectal adenocarcinoma at the pT1 stage between January 2015 and June 2024 at the University Medical Center Ho Chi Minh City, Vietnam. After applying inclusion and exclusion criteria, 104 patients were eligible and included in the final analysis (Figure 1). Demographic characteristics (age, sex), clinical and endoscopic findings (tumor site and number of polyps), and laboratory data (serum CEA, lipid profile, total protein, albumin) were retrieved from electronic medical records.

Figure 1 Flow diagram of patient selection.

Inclusion criteria were: (1) histopathological confirmation of invasive adenocarcinoma confined to the submucosa (pT1 stage), (2) availability of adequate H&E-stained slides for TB assessment, and (3) complete and clearly documented clinical and pathological records. Exclusion criteria were: (1) history or synchronous of another primary malignancy, (2) prior chemotherapy, and (3) technically inadequate specimens (eg, unreadable H&E slides or severely damaged paraffin blocks).

Pathological Assessment

Histopathological variables assessed on H&E slides included histological subtype, tumor grade, depth of submucosal invasion, distance to resection margin, precursor lesion, Haggitt/Kikuchi classification, lymphovascular invasion, perineural invasion, tumor necrosis, tumor-infiltrating lymphocytes (TILs), and nodal status (for surgical specimens). Depth of submucosal invasion was assessed according to standardized criteria. Pedunculated malignant polyps were evaluated using the Haggitt classification (levels 1–4), whereas sessile lesions were assessed using the Kikuchi classification (SM1–SM3). In addition, invasion <1000 µm from the muscularis mucosae was defined as superficial and ≥1000 µm as deep. TB was initially evaluated on H&E slides according to the ITBCC 2016 criteria,12 and the counts were recorded as baseline values. After Pan-CK immunostaining, the same invasive front was re-examined to identify the corresponding hotspot (0.785 mm2 at ×20 objective). Pan-CK staining was used to confirm the epithelial nature of buds and reveal additional discrete clusters obscured by stromal or inflammatory components. The interpretation of budding morphology was based primarily on H&E features, with Pan-CK serving as a complementary tool to enhance TB detection. TB was classified as Bd1 (0–4 buds), Bd2 (5–9 buds), or Bd3 (≥10 buds). For analytical purposes, Bd1 was categorized as “low risk”, while Bd2–3 were grouped as “high risk”. Upgrading was defined as an increase in TB grade on Pan-CK compared with H&E. TB evaluation was independently performed by two pathologists who were blinded to clinical and outcome information. In cases of disagreement, the slides were jointly reviewed at a multi-headed microscope to reach a consensus. This consensus-based evaluation was intended to enhance reproducibility and ensure methodological rigor.

Immunohistochemistry Staining

For each case, serial sections were cut from formalin-fixed paraffin-embedded blocks and immunostained for cytokeratin using the Pan-CK antibody (clone AE1/AE3, Ventana, Roche Diagnostics, USA) on a fully automated BenchMark XT platform. The protocol included deparaffinization with EZ Prep solution, antigen retrieval using Cell Conditioning 1 buffer (CC1, pH 8.5, 95°C, 30 minutes), and visualization via the OptiView DAB IHC Detection Kit. Positive staining highlighted epithelial tumor cells, including isolated cells and small clusters, which were then evaluated for tumor budding (TB) according to the ITBCC 2016 criteria as described above. TB evaluation on Pan-CK–stained slides was performed by two pathologists using the same scoring approach as for H&E slides.

Statistical Analysis

All statistical analyses were conducted using Stata version 17 (StataCorp, College Station, TX, USA). Continuous variables were summarized as means ± standard deviations or medians with interquartile ranges, depending on data distribution, while categorical variables were presented as counts and percentages. Group comparisons were performed using Student’s t-test, chi-square test, or Fisher’s exact test, as appropriate. The correlation between TB counts on H&E and Pan-CK slides was assessed using Spearman’s rank correlation coefficient. To evaluate factors associated with TB upgrading, logistic regression models were applied. Multivariable logistic regression was performed, including the three variables that showed the lowest p-values in univariate analysis, given the limited number of upgrading events. A two-sided p-value < 0.05 was considered statistically significant.

Results

A total of 104 malignant colorectal polyps at the pT1 stage were included, comprising 58 males and 46 females, with a mean age of 63.88 ± 11.48 years. Of the 104 malignant polyps, 61 lesions (58.7%) were treated by endoscopic resection alone, 38 (36.5%) by surgical resection, and 5 (4.8%) by endoscopic resection followed by additional surgical resection. Most polyps were pedunculated (101 cases, 97.12%), with a mean size of 20.6 ± 12.4 mm. The most frequent tumor locations were the sigmoid colon (43 cases, 41.35%) and rectum (40 cases, 38.46%). Histologically, tubulovillous adenoma was the most common precursor lesion (60 cases, 57.69%), and adenocarcinoma not otherwise specified accounted for 94 cases (90.38%). Deep submucosal invasion was present in 87 (83.65%) cases, while lymphovascular invasion was identified in 2 cases (1.92%). Perineural invasion was not observed. Among 43 patients who underwent segmental resection or additional surgical resection, lymph node metastasis was identified in 2 cases (4.65%).

TB Assessment by Sequential H&E and Pan-CK

The number of TB foci was significantly higher on Pan-CK immunostained slides compared to H&E slides (median [IQR]: 1.0 [0.0–7.0] vs 0.5 [0.0–3.0]; p < 0.001). A strong positive correlation was observed between the two methods (Spearman’s r = 0.90, p < 0.001) (Figure 2). Based on H&E, the majority of cases were classified as Bd1 (86.54%), followed by Bd2 (12.50%) and Bd3 (0.96%). In contrast, Pan-CK staining increased the proportions of Bd2 (26 cases, 25.00%) and Bd3 (13 cases, 12.50%), while Bd1 decreased to 65 cases (62.50%). The overall agreement between H&E and Pan-CK across three Bd categories was only fair (κ = 0.301). When TB was dichotomized into low- vs high-risk (Bd1 vs Bd2/3), agreement slightly improved (κ = 0.411). Representative histological images illustrating TB on H&E and Pan-CK immunostaining are shown in Figure 3.

Figure 2 Distribution of tumor budding grades on H&E and Pan-CK immunostaining across study sample.

Figure 3 Representative histological images of tumor budding. (A and B) Cases without change in TB grade after Pan-CK immunostaining (A: H&E, ×200; (B) Pan-CK, ×200). (C and D) Cases showing upgrading from Bd1 on H&E to Bd2 on Pan-CK (C: H&E, ×200; (D) Pan-CK, ×200). Yellow arrows indicate tumor buds.

To investigate factors associated with TB grade upgrading, we focused on cases initially classified as Bd1 on H&E (n = 90), in which some were upgraded to Bd2 or Bd3 after Pan-CK immunostaining.

Clinicopathological Features Associated with TB Upgrading

Among the 90 cases initially classified as Bd1 on H&E, 25 (27.78%) were upgraded on Pan-CK (19 to Bd2 and 6 to Bd3). Several clinicopathological factors were associated with TB grade upgrading on Pan-CK staining (Tables 1 and 2). The presence of synchronous polyps defined as the coexistence of one or more additional polyps in the colorectal segment, was significantly associated with TB upgrading (36.73% vs 17.07%; OR = 2.82, 95% CI: 1.04–7.66; p = 0.042). Tumor grade 2 showed a borderline association with upgrading compared to grade 1 (33.33% vs 5.88%; OR = 8.00, 95% CI: 1.00–64.12; p = 0.050). Similarly, cases with a Haggitt/Kikuchi level ≥ 2 had a higher likelihood of upgrading than those with level 1 (38.64% vs 17.39%; OR = 2.99, 95% CI: 1.13–7.92; p = 0.028). In contrast, polyp morphology, tumor subtype, depth of invasion, precursor lesion, distance to resection margin, tumor-infiltrating lymphocytes, and tumor necrosis were not significantly associated with TB upgrading (p > 0.05).

Table 1 Clinical and Laboratory Features Associated with Tumor Budding Upgrading From Bd1 on H&E to Bd2/3 on Cytokeratin Staining

Table 2 Histopathological Features Associated with Tumor Budding Upgrading From Bd1 on H&E to Bd2/3 on Cytokeratin Staining

Multivariate Analysis

In the multivariable logistic regression model including the three significant histopathological variables from univariate analysis (Figure 4), the presence of synchronous polyps remained independently associated with TB grade upgrading (OR = 3.00, 95% CI: 1.03–8.76, p = 0.045). Tumor grade (OR = 6.42, 95% CI: 0.77–53.41, p = 0.085) and Haggitt/Kikuchi classification (OR = 2.49, 95% CI: 0.86–7.19, p = 0.091) showed strong trends toward association but did not reach statistical significance.

Figure 4 Multivariable logistic regression analysis of clinicopathological factors associated with tumor budding upgrading. Error bars represent 95% confidence intervals.

Discussion

TB, a histological manifestation of EMT has been recognized as an important prognostic factor in early-stage colorectal cancer, with high-grade TB closely associated with lymph node metastasis and poor outcomes.12,14,15 In our study, we observed a strong correlation between H&E and Pan-CK in the assessment of TB (Spearman r = 0.90; p < 0.001). However, the number of TB identified on Pan-CK was significantly higher compared with H&E, with 27.8% (25/90) of cases initially classified as Bd1 on H&E being upgraded to Bd2–3 following Pan-CK staining.

Pan-CK has been consistently shown in multiple studies to substantially increase the number of TB detected compared with H&E. Yamadera et al reported a median TB count of 4 (range 0–20) on H&E versus 8 (range 0–40) on cytokeratin, with a statistically significant difference (p < 0.001).25 Fisher et al likewise observed that the number of TB identified on Pan-CK was more than four times higher than on H&E when examined on parallel sections.26 Similarly, Koelzer et al documented a three- to six-fold increase in TB counts on Pan-CK compared with H&E.20 This discrepancy reflects the inherent limitations of H&E, in which TB recognition can be hampered by inflammatory infiltrates, desmoplastic reactions, or fragmented glands at the invasive front, resulting in subjectivity and suboptimal interobserver agreement. In this context, Pan-CK provides important added value by improving both the sensitivity and reliability of TB assessment in routine pathology practice. Our study also yielded similar findings, with Pan-CK detecting significantly more TB than H&E, further confirming its diagnostic utility. These results support the selective application of Pan-CK in challenging or borderline cases, consistent with CAP and ITBCC 2016 recommendations that emphasize TB reporting in pT1 CRC.12,16 By integrating Pan-CK staining into diagnostic workflows when H&E assessment is equivocal, pathologists may achieve more reproducible TB scoring, thereby enhancing risk stratification and clinical decision-making.

In univariate analysis, two histopathological factors—Haggitt/Kikuchi classification, and the presence of synchronous polyps—were significantly associated with the likelihood of TB upgrading after Pan-CK staining. Tumors with moderate differentiation (grade 2) showed a borderline association with upgrading compared with well-differentiated tumors (grade 1). However, in multivariate analysis, only the presence of synchronous polyps remained independently associated with TB upgrading. This finding may be explained by the “field cancerization” hypothesis, which proposes that multiple neoplastic lesions represent a broader epithelial field that has undergone premalignant molecular alterations. Patel et al provided supporting evidence for this mechanism, demonstrating the presence of cancer stem cell (CSC)-like populations in morphologically normal colonic mucosa of patients with adenomatous polyps. Moreover, CSC markers such as CD44, CD166, and ESA were found to increase with age and were expressed at approximately twice the level in individuals with three to four polyps compared with those with only one to two.27 These observations suggest that CSC-like cells are present not only within premalignant adenomatous polyps but also in histologically normal colonic mucosa, indicating a broader predisposition to CRC development. Taken together, our findings indicate that synchronous polyps may serve as a practical marker for identifying cases more likely to experience TB upgrading with Pan-CK. To our knowledge, this is the first study to report such an association, although further validation in larger, multicenter cohorts is warranted.

The findings of this study have important clinical implications, demonstrating that Pan-CK should be applied selectively rather than routinely to all pT1 colorectal polyps. The presence of synchronous polyps was identified as an independent predictor associated with TB upgrading. This observation suggests that Pan-CK staining should be considered particularly in cases with synchronous polyps, instead of being performed indiscriminately for all pT1 lesions. Such a selective approach may not only optimize resources and diagnostic workflows but also enhance the effectiveness of Pan-CK in risk stratification, thereby assisting clinicians in making more appropriate follow-up and treatment decisions, especially for patients with tumors harboring aggressive biological features that require definitive surgical intervention.

This study, however, has several limitations. First, it was a retrospective, single-center study with a relatively limited sample size, which reduces the statistical power and generalizability of the findings. Second, TB assessment was performed independently by two pathologists, followed by joint discussion to reach a consensus. While this approach may have improved accuracy through consensus-based interpretation, it limited the ability to assess interobserver variability, which is a critical factor when considering the true impact of Pan-CK in routine practice. Third, as 97.1% of malignant polyps in our cohort were pedunculated and only three were sessile, the findings of this study primarily apply to pedunculated lesions. The small number of sessile or non-pedunculated polyps precluded subgroup analysis; therefore, the generalizability of our results to non-pedunculated lesions should be interpreted with caution. Finally, due to the limited number of lymph node metastasis events in our cohort, we were unable to comprehensively evaluate the prognostic significance of TB upgrading on Pan-CK or determine an optimal cut-off value. These issues should be addressed in future prospective, multicenter studies with larger cohorts and long-term follow-up data.

Conclusion

Pan-CK immunohistochemistry substantially increases TB detection and grading in malignant colorectal polyps at the pT1 stage. Among cases initially classified as low-grade TB on H&E, nearly one-third were upgraded after Pan-CK staining. Notably, the presence of synchronous polyps was identified as the only independent predictor of TB upgrading—suggesting a biologically broader field effect and highlighting its potential role in refining risk stratification.

Therefore, Pan-CK should not be applied routinely to all pT1 lesions, but rather selectively—especially when synchronous polyps are present—to optimize diagnostic cost-effectiveness and support personalized decision-making. This targeted approach is particularly relevant in resource-constrained settings and aligns with the need for more sustainable, evidence-based diagnostic strategies in early colorectal cancer.

Data Sharing Statement

The datasets generated and/or analyzed during the current study are available from Dr. Phat Thi Hong Ho upon reasonable request.

Ethical Approval

The study protocol was approved by the Institutional Review Board of the University of Medicine and Pharmacy at Ho Chi Minh City (approval number: 2855/ĐHYD-HĐĐĐ). The study was conducted in accordance with the Declaration of Helsinki. Because this was a retrospective analysis of anonymized archival material, the requirement for informed consent was waived.

Acknowledgments

We gratefully acknowledge the Board of Directors of the University Medical Center, Ho Chi Minh City, as well as the Pathology Department, its physicians, technicians, and staffs for their support in data collection and laboratory procedures.

Author Contributions

All authors made a significant contribution to the work reported, whether that is in the conception, study design, execution, acquisition of data, analysis and interpretation, or in all these areas; took part in drafting, revising or critically reviewing the article; gave final approval of the version to be published; have agreed on the journal to which the article has been submitted; and agree to be accountable for all aspects of the work.

Funding

This research was financially supported by the Faculty of Medicine, University of Medicine and Pharmacy at Ho Chi Minh City.

Disclosure

All authors have no conflicts of interest in the subject of this study.

References

1. Bray F, Laversanne M, Sung H, et al. Global cancer statistics 2022: GLOBOCAN estimates of incidence and mortality worldwide for 36 cancers in 185 countries. CA. 2024;74(3):229–263. doi:10.3322/caac.21834

2. Logan RF, Patnick J, Nickerson C, Coleman L, Rutter MD, von Wagner C. Outcomes of the Bowel Cancer Screening Programme (BCSP) in England after the first 1 million tests. Gut. 2012;61(10):1439–1446. doi:10.1136/gutjnl-2011-300843

3. Aarons CB, Shanmugan S, Bleier JI. Management of malignant colon polyps: current status and controversies. World J Gastroenterol. 2014;20(43):16178–16183. doi:10.3748/wjg.v20.i43.16178

4. Teo NZ, Wijaya R, Ngu JC-Y. Management of malignant colonic polyps. J Gastrointest Oncol. 2020;11(3):469. doi:10.21037/jgo.2020.02.07

5. Guo K, Feng Y, Yuan L, et al. Risk factors and predictors of lymph nodes metastasis and distant metastasis in newly diagnosed T1 colorectal cancer. Cancer Med. 2020;9(14):5095–5113. doi:10.1002/cam4.3114

6. Chok KS, Law WL. Prognostic factors affecting survival and recurrence of patients with pT1 and pT2 colorectal cancer. World J Surg. 2007;31(7):1485–1490. doi:10.1007/s00268-007-9089-0

7. Song J, Yin H, Zhu Y, Fei S. Identification of predictive factors for lymph node metastasis in pt1 stage colorectal cancer patients: a retrospective analysis based on the population database. Pathol Oncol Res. 2022;28:1610191.

8. Bosch SL, Teerenstra S, de Wilt JH, Cunningham C, Nagtegaal ID. Predicting lymph node metastasis in pT1 colorectal cancer: a systematic review of risk factors providing rationale for therapy decisions. Endoscopy. 2013;45(10):827–834. doi:10.1055/s-0033-1344238

9. Cappellesso R, Luchini C, Veronese N, et al. Tumor budding as a risk factor for nodal metastasis in pT1 colorectal cancers: a meta-analysis. Hum Pathol. 2017;65:62–70.

10. Ichimasa K, Kudo SE, Miyachi H, Kouyama Y, Misawa M, Mori Y. Risk stratification of T1 colorectal cancer metastasis to lymph nodes: current status and perspective. Gut Liver. 2021;15(6):818–826. doi:10.5009/gnl20224

11. Chen P-C, Kao Y-K, Yang P-W, Chen C-H, Chen C-I. Long-term outcomes and lymph node metastasis following endoscopic resection with additional surgery or primary surgery for T1 colorectal cancer. Sci Rep. 2025;15(1):2573. doi:10.1038/s41598-024-84915-x

12. Lugli A, Kirsch R, Ajioka Y, et al. Recommendations for reporting tumor budding in colorectal cancer based on the International Tumor Budding Consensus Conference (ITBCC) 2016. Mod Pathol. 2017;30(9):1299–1311. doi:10.1038/modpathol.2017.46

13. Pai RK, Chen Y, Jakubowski MA, Shadrach BL, Plesec TP, Pai RK. Colorectal carcinomas with submucosal invasion (pT1): analysis of histopathological and molecular factors predicting lymph node metastasis. Mod Pathol. 2017;30(1):113–122.

14. Mitrovic B, Schaeffer DF, Riddell RH, Kirsch RJMP. Tumor budding in colorectal carcinoma: time to take notice. Mod Pathol. 2012;25(10):1315–1325. doi:10.1038/modpathol.2012.94

15. Bhangu A, Wood G, Mirnezami A, Darzi A, Tekkis P, Goldin RJ. Epithelial mesenchymal transition in colorectal cancer: seminal role in promoting disease progression and resistance to neoadjuvant therapy. Surg Oncol. 2012;21(4):316–323. doi:10.1016/j.suronc.2012.08.003

16. Jain D, Chopp WV, Graham RP, Xue Y. Protocol for the Examination of Resection Specimens From Patients with Primary Carcinoma of the Colon and/or Rectum; Version 4.4.0.0. Northfield, IL: College of American Pathologists; 2025.

17. Benson AB, Venook AP, Adam M, et al. Colon Cancer, Version 3.2024, NCCN Clinical Practice Guidelines in Oncology. J Natl Compr Canc Netw. 2024;22(2 d).

18. Kai K, Aishima S, Aoki S, et al. Cytokeratin immunohistochemistry improves interobserver variability between unskilled pathologists in the evaluation of tumor budding in T1 colorectal cancer. Pathol Int. 2016;66(2):75–82. doi:10.1111/pin.12374

19. Martinez‐Ciarpaglini C, Fernandez‐Sellers C, Tarazona N, et al. Improving tumour budding evaluation in colon cancer by extending the assessment area in colectomy specimens. Histopathology. 2019;75(4):517–525. doi:10.1111/his.13900

20. Koelzer VH, Zlobec I, Berger MD, et al. Tumor budding in colorectal cancer revisited: results of a multicenter interobserver study. Virchows Archiv. 2015;466:485–493. doi:10.1007/s00428-015-1740-9

21. Prall F, Nizze H, Barten M. Tumour budding as prognostic factor in stage I/II colorectal carcinoma. Histopathology. 2005;47(1):17–24. doi:10.1111/j.1365-2559.2005.02161.x

22. Ohtsuki K, Koyama F, Tamura T, et al. Prognostic value of immunohistochemical analysis of tumor budding in colorectal carcinoma. Anticancer Res. 2008;28(3B):1831–1836.

23. Satoh K, Nimura S, Aoki M, et al. Tumor budding in colorectal carcinoma assessed by cytokeratin immunostaining and budding areas: possible involvement of c‐Met. Cancer Sci. 2014;105(11):1487–1495. doi:10.1111/cas.12530

24. Jepsen RK, Klarskov LL, Lippert MF, et al. Digital image analysis of pan-cytokeratin stained tumor slides for evaluation of tumor budding in pT1/pT2 colorectal cancer: results of a feasibility study. Pathol Res Pract. 2018;214(9):1273–1281. doi:10.1016/j.prp.2018.07.002

25. Yamadera M, Shinto E, Kajiwara Y, et al. Differential clinical impacts of tumour budding evaluated by the use of immunohistochemical and haematoxylin and eosin staining in stage II colorectal cancer. Histopathology. 2019;74(7):1005–1013. doi:10.1111/his.13830

26. Fisher NC, Loughrey MB, Coleman HG, Gelbard MD, Bankhead P, Dunne PDJH. Development of a semi‐automated method for tumour budding assessment in colorectal cancer and comparison with manual methods. Histopathology. 2022;80(3):485–500. doi:10.1111/his.14574

27. Patel BB, Yu Y, Du J, et al. Age-related increase in colorectal cancer stem cells in macroscopically normal mucosa of patients with adenomas: a risk factor for colon cancer. Biochem Biophys Res Commun. 2009;378(3):344–347. doi:10.1016/j.bbrc.2008.10.179

Continue Reading

-

TU Delft leading in deep-tech and life sciences spin-offs

TU Delft is the frontrunner in the Netherlands when it comes to value creation by academic spin-offs in deep tech and the life sciences, according to the European University Spinout Report 2025. TU Delft ranks 15th. This isn’t cause for complacency, says Ronald Gelderblom of Delft Enterprises. “To take the next step in the Netherlands, we need structural funding.”

In short:

- TU Delft is the highest-ranked Dutch university in the European University Spinout Report 2025, but emphasises that further growth is only possible with structural funding for valorisation.

- TU Delft fosters entrepreneurship through a broad ecosystem, including YES!Delft, Impact Studio, field labs, startup vouchers, entrepreneurship education and strong patent support to bring new technologies to market.

- The Netherlands is standardising spin-off conditions, with Delft Enterprises playing an important role in developing the new national deal terms.

The list is topped by the University of Oxford, followed by Cambridge and ETH Zurich. Other Dutch universities appear at positions 27 (University of Amsterdam), 28 (TU Eindhoven), 35 (Leiden), and 40 (Vrije Universiteit Amsterdam). In total, Europe’s deep tech and life sciences start-ups have a combined value of 398 billion dollars. Together, they have created 167,000 jobs across more than 7,300 start-ups.

Semiconductors and quantum technology

The report shows that the United Kingdom, Switzerland, France and Germany lead the way in value creation. Relative to their size, Belgium, the Netherlands and the Scandinavian countries create “significant value”, according to the report. The Netherlands is particularly strong in semiconductors, quantum technology, photonics and health.

The more than 300 Dutch spin-offs have raised a total of 2.7 billion dollars from investors since 2020 and are now worth over 13.4 billion dollars in total: more than three times as much as in 2019. The report highlights TU Delft, the University of Amsterdam, TU Eindhoven, Leiden University, VU Amsterdam, the University of Twente and TNO as top institutions.

Encouraging entrepreneurship

TU Delft runs numerous programmes to encourage entrepreneurship among students and researchers, ensuring that promising new technologies can be turned into societal applications: YES!Delft, Impact Studio, field labs, start-up vouchers and entrepreneurship education.

A central role is also played by the Patents department of the Innovation & Impact Centre, which helps scientists protect new inventions through patents. These patents often form the basis of academic spin-offs.

Delft Enterprises

Through Delft Enterprises, TU Delft itself participates in and invests in spin-offs. It currently has around 70 companies in its portfolio.

The findings of the report are interesting because they focus, among other things, on spin-offs that have raised money from investors (VC-backed spin-offs). “That is an interesting parameter because it says something not just about the number of spin-offs, but also about their quality,” says managing director Ronald Gelderblom. “In other words: are they attractive enough for venture capital to come on board? That is often the first validation.”

No cause for complacency

“That we are the highest-ranked Dutch university in this study is no cause for complacency,” Gelderblom continues. “We constantly consider how we can increase the number of successful spin-offs, often together with colleagues from other universities. In Delft we have built a relatively extensive innovation ecosystem, but part of it is funded through short-term project grants. To take the next step in the Netherlands, structural funding of the core task of valorisation is needed.”

Uniform deal terms

One of the recommendations of the report is to standardise the conditions for spin-offs. The Netherlands is ahead in this respect. Last week, Dutch universities announced a new national standard for the so-called deal terms. Delft Enterprises has played an important role in developing these over the past few years.

This article was first published on 3 December by TU Delft.

Continue Reading

-

LR exchanges contracts for the sale of 70 Fenchurch Street

Lloyd’s Register (LR) has exchanged contracts for the sale of 70 Fenchurch Street, EC3, to Henderson Park, the international real estate investment manager.

The transaction follows the organisation’s relocation to its newly refurbished headquarters at 71 Fenchurch Street, London, now officially renamed the Lloyd’s Register Building.

70 Fenchurch Street, commissioned by LR and completed in 2000, was designed by Rogers Stirk Harbour + Partners (RSHP). The building has won multiple architectural awards and served as LR’s global headquarters for more than two decades.

LR has now consolidated its London workforce into the adjacent Grade II* listed building at 71 Fenchurch Street, originally opened in 1901 and recently modernised to support hybrid working and collaboration. The restoration preserves the historic character of the site while creating a more efficient, digitally enabled workspace for LR and Lloyd’s Register Foundation.

Nick Brown, Chief Executive Officer of Lloyd’s Register, said: “The sale of 70 Fenchurch Street and our move into the refurbished Lloyd’s Register Building mark an important step in aligning our estate with the needs of a modern, global organisation. This enables us to focus investment on our people, our digital capabilities and the services that support our clients across the maritime industry.”

Henderson Park and YardNine, a central London’s office developer, plan to reposition 70 Fenchurch Street as prime, Grade A workspace. RSHP and Arup, both involved in the original development, have been appointed to advise on the refurbishment.

LR was advised on the sale by CBRE and Herbert Smith Freehills Kramer.

Continue Reading

-

Fitch Rates Level 3's First Lien Senior Unsecured Notes Offering 'CCC-'/'RR6' – Fitch Ratings

- Fitch Rates Level 3’s First Lien Senior Unsecured Notes Offering ‘CCC-‘/’RR6’ Fitch Ratings

- Lumen Technologies Subsidiary To Offer $750 Mln Senior Notes Nasdaq

- Lumen Technologies says Level 3 Financing to offer $750 million senior notes due 2036 marketscreener.com

- Lumen Technologies, Inc. Announces Offering of Senior Notes Due 2036 and Concurrent Tender Offers and Consent Solicitations Business Wire

- Lumen Technologies to offer $750M notes, launches tender offers for outstanding notes MSN

Continue Reading

-

Iron ore heads towards a softer year | articles

The ongoing pricing standoff, which began two months ago between BHP and China’s state-backed CMRG (China Minerals Resources Group), has added to uncertainty in the iron ore market. The standoff is part of China’s strategic push to exert greater influence over iron ore pricing and to increase the use of the yuan in contract settlements, reducing reliance on the US dollar.

CMRG was created by Beijing three years ago to shift leverage from major iron ore producers toward China, the world’s largest iron ore buyer.

Beijing has recently expanded its embargo on some BHP cargoes, ordering steel mills and traders to stop buying “jingbao fines”, a low-grade of iron ore that represents a small part of the miner’s exports to China. The ban follows an earlier halt on BHP’s “jimblebar fines”, a Pilbara iron ore grade and one of BHP’s most popular export types.

While the dispute is likely a negotiating tactic rather than a structural break, it heightens near-term volatility by disrupting trade flows and undermining confidence in China’s procurement approach. If unresolved, the impasse could drive a rerouting of some trade flows and force BHP to discount cargoes into alternative markets. For now, BHP has kept its full-year 2026 production guidance unchanged at 258-269 million tonnes.

Continue Reading

-

Commodities Outlook 2026: Energy cools as metals heat up | reports

We entered 2025 with a relatively bearish view of the commodities complex, while expecting gold to be the standout. And that was a pretty good call, especially when you look at oil and European natural gas. The oil market has been largely unfazed by geopolitical events and sanction uncertainty, which has seen it trade lower.

A number of agri commodities have also come under pressure, including cocoa, sugar, wheat and corn, on the back of more comfortable supply conditions. That said, wheat and corn have clawed their way back from the lows seen this year, with trade tensions easing between the US and China.

Base metal markets have performed well. While tariffs had been a downward concern, this uncertainty was more than offset by distortions seen in trade flows, with the market concerned about how trade policy will evolve. This has been particularly apparent in the copper market. The broad weakness in the US dollar would have provided further support to the metals complex.

Of course, precious metals have been the standout, with gold repeatedly hitting record highs throughout the year. Uncertainty over trade policy also led to distortions in the gold market. While heightened geopolitical risks, falling real yields, and a weaker USD all proved supportive of gold investment demand, central banks continue to make strong purchases, a trend that has been clear since the freezing of Russian assets following the Russia/Ukraine war.

For 2026, we remain bearish towards energy markets, with the global oil market set to be in large surplus, following OPEC+ rapidly ramping up output as it shifts policy, while demand growth remains modest. There is plenty of uncertainty about Russian oil supply following US sanctions, but as we move through 2026, markets will get a clearer picture of the full impact. For now, we believe the impact will be limited in the medium to long term. However, there is potential for greater volatility, given that OPEC’s spare production capacity has shrunk as the group has increased output.

While there are some short-term upside risks for the European gas market, it’s set to become better supplied, despite the region’s plans to phase out Russian gas and LNG. The start-up of LNG export capacity, particularly from the US, will leave global LNG markets and the European gas market increasingly more comfortable. However, the ramp-up of US LNG exports risks leaving the US gas market tighter.

Developments related to Russia-Ukraine peace talks will also be important to watch in 2026, with any progress towards ending the war likely to put further pressure on energy markets.

Most base metals are likely to remain well supported next year. Uncertainty over US refined copper tariffs will likely continue to see strong refined copper flows to the US, tightening up the ex-US market. And this coincides with a persistently tight copper concentrate market. For aluminium, the market is focused on China approaching its production cap, along with several producers elsewhere considering closures due to high power prices. We believe the aluminium market will be tight in 2026. For nickel, we expect little change amid persistent surpluses, keeping prices under pressure. We expect iron ore to trade lower with Chinese demand still a concern and supply growing, helped by the start of the 120mtpa Simandou mine.

We expect gold prices to remain strong and yet reach new heights. With the Fed set to cut rates and the USD likely to remain under pressure, this should be constructive for investment demand, while central banks are likely to continue adding to their reserves.

While agri commodities have seen some downward pressure this year due to strong supply and trade tensions, we believe the corn, wheat, and soybean markets are set to tighten next season, suggesting the potential for some upside in prices. However, much will depend on US trade policy with China, while for soybeans, US biofuel policy is also important.

The sugar market is set for a large surplus, driven by another strong crop from CS Brazil, while India is poised for a large recovery in output. This should keep sugar prices under pressure. The cocoa market is set for another surplus in 2025/26, suggesting prices are likely to continue trending lower from elevated levels. Finally, we also expect some moderation in the coffee market, with Brazil set to see a strong 2026/27 crop, but there are risks to this view.

Continue Reading

-

EPHA and public health community urge EU countries to uphold 2035 phase-out of internal combustion engines

Air pollution from petrol and diesel vehicles remains one of Europe’s most harmful public-health threats. Emissions from internal combustion engines are major sources of nitrogen dioxide (NO₂) and fine particulate matter (PM2.5). These are pollutants with no safe exposure level, as well as well-established links to heart disease, stroke, lung cancer, asthma, COPD, diabetes, dementia, pregnancy complications, and impaired development in children. Across Europe, air pollution contributes to more than 300,000 premature deaths every year, with the heaviest burden falling on children, older people, those with chronic conditions, and socio-economically disadvantaged communities.

To protect public health, the EU committed to ending the sale of new petrol and diesel cars and vans by 2035. This phase-out is a vital measure to reduce toxic air pollution, strengthen health system resilience, and advance a fairer, cleaner, and healthier Europe. Recent signals from parts of the automotive industry and some Member States suggest that the 2035 commitment may be weakened or delayed.

For this reason, EPHA joins organisations representing over 85,000 health and medical professionals in issuing an open letter urging national governments to stand firm. Rolling back the phase-out would prolong Europe’s dependence on fossil fuels, increase avoidable illness, and undermine citizens’ right to clean air.

Phasing out combustion engines will mean fewer premature deaths, healthier children, reduced healthcare costs, and a more sustainable and competitive European economy. The transition can – and must – be done equitably, minimising negative effects on employment, in cooperation between governments, industry, and citizens.

Continue Reading