Qantas loyalty division boss Andrew Glance admits he’s been taken aback by the airline’s remarkable turnaround since the dark days that saw former chief executive Alan Joyce and chairman Richard Goyder ousted by angry investors in 2023.

Vanessa Hudson beat Olivia Wirth, former boss of the loyalty program, to the top job and has won widespread praise for rebuilding the flying kangaroo’s reputation. Glance’s star has also been rising since taking on the frequent flyer business after the overlooked Wirth left for Myer.

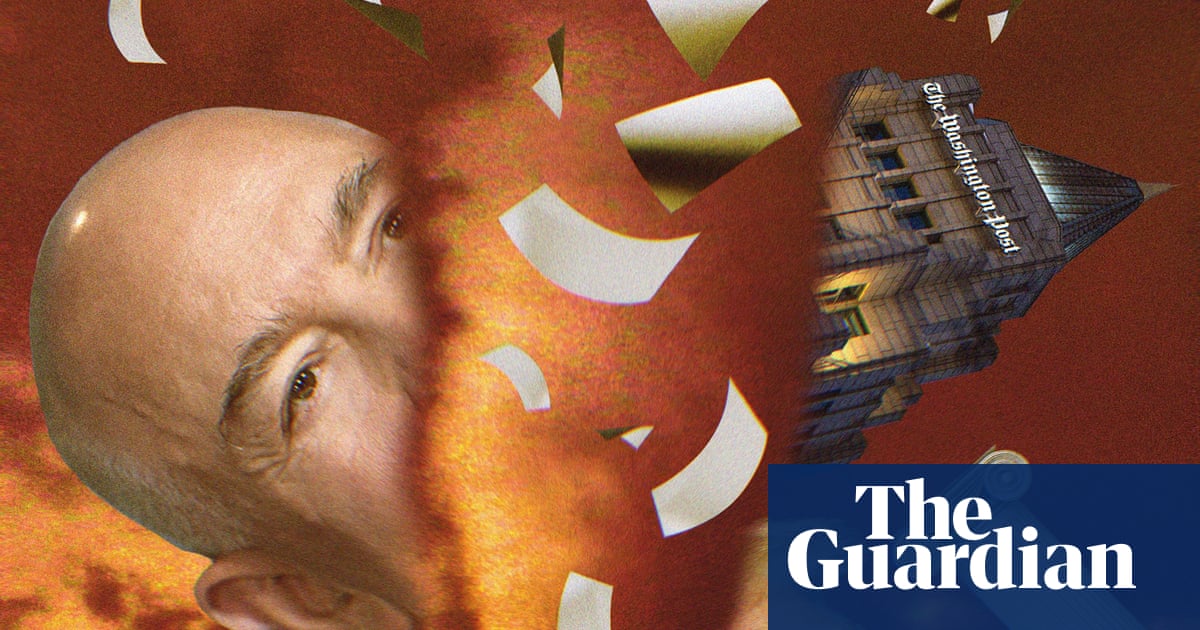

The email landed in Lizzie Johnson’s in-tray in Ukraine just before 4pm local time. It came at a tough time for the reporter: Russia had been repeatedly striking the country’s power grid, and just days before she had been forced to work out of her car without heat, power or running water, writing in pencil because pen ink freezes too readily.

“Difficult news,” was the subject line. The body text said: “Your position is eliminated as part of today’s organizational changes,” explaining that it was necessary to get rid of her to meet the “evolving needs of our business”.

Johnson’s response may go down in the annals of American media history. “I was just laid off by The Washington Post in the middle of a warzone,” she wrote on X. “I have no words.”

The Washington Post’s Ukraine correspondent may have been rendered speechless over Wednesday’s move by Jeff Bezos, the Amazon billionaire and Post owner, to cut more than 300 newsroomjobs. The bloodletting, which has raised renewed fears about the resilience of America’s democracy to withstand Donald Trump’s attacks, swept away the paper’s entire sports department, much of its culture and local staff and all of its journalists in such arid news zones as Ukraine and the Middle East.

Others, though, managed to find their tongues. “It’s a bad day,” said Don Graham, son of the Post’s legendary Watergate-era owner Katharine Graham, breaking the silence he has maintained since selling the paper to Bezos for $250m in 2013.

“I am crushed,” was the lament of Bob Woodward, one-half of the paper’s double act with Carl Bernstein that exposed Watergate.

“This ranks among the darkest days in the history of one of the world’s greatest news organizations,” said Marty Baron, the Post’s lionised former executiveeditor. Not one to mince his words, Baron castigated Bezos for his “sickening efforts to curry favor with President Trump”, saying it left an especially “ugly stain” on the paper’s standing.

Several hundred people rallied in front of the Post’s offices on Thursday, voicing support for their laid-off colleagues. “It’s disappointing on an immense scale. They don’t seem to give a damn about this institution and the people that make it run,” said Patrick Nielsen, an engineer at the paper.

Howls of dismay were also uttered by prominent Post alumni in interviews with the Guardian. Robert McCartney, a 39-year veteran of the Post until he retired five years ago, said it was a “tragedy and an outrage”.

Like many Post insiders, McCartney has been astonished by the stark contrast between Bezos’s handling of the newspaper during Donald Trump’s first term in office and his conduct now in Trump 2.0.

McCartney was a senior journalist on the paper during Bezos’s initial eight years of ownership, through Trump’s first presidency. Back then, he, like many others, was grateful for Bezos’s tutelage.

“We saw him as a savior. He pumped money into the Post, didn’t meddle in the newsroom and stood up to Trump,” he said.

Fast-forward to 2026, and a very different Bezos has emerged. In 2017, soon after Trump’s first inauguration, the Post introduced its new strapline: “Democracy dies in darkness.”

That wording still runs proudly beneath the masthead. At the end of a week like this one, though, America looks a notable shade darker.

Marcus Brauchli, the Post’s executive editor until 2012 who now runs investment firm North Base Media, said that this was a terrible moment to be hammering one of the country’s great custodians of public accountability: “These are historic times, given the cyclone bearing down on the world order and American system of government. This is when journalism matters most. I mean, laying off reporters in Ukraine, now.”

It is not as though Bezos needs the money. He is the fourth-richest person on the planet, according to Forbes, with a $245bn fortune.

As Peter Baker, the chief White House correspondent for the New York Times, pointed out, Bezos could cover five years of the Post’s $100m annual losses by dipping into his earnings from a single week.

The optics of Wednesday’s train wreck of an announcement were also diabolical: the job of facing the distraught staff on Zoom was delegated to the Post’s beleaguered current executive editor, Matt Murray.

Bezos was nowhere to be seen. Yet there he was, earlier in the week, beaming broadly as he welcomed Trump’s defense secretary, Pete Hegseth, to the Florida headquarters of his space company, Blue Origin.

Nor did Will Lewis, Bezos’s consigliere as publisher of the Post, have the courage to present himself as the guillotine came down. A day after he had presided over the evisceration of the paper’s sports department, he was spotted attending the red carpet at an NFL Super Bowl event in San Francisco.

On Saturday night, however, Lewis abruptly resigned, acknowledging “difficult decisions” as he praised Bezos’s leadership of the paper.

The lay-offs came just five days after the launch of the first lady documentary, Melania, bankrolled by Amazon MGM Studios. Bezos sank $75m into that pile of “gilded trash” yet, unlike the Post, seems unfazed by the film’s paltry return on investment.

“What Bezos did for Melania while gutting his own newspaper,” wrote the historian Simon Schama, will come to be seen “as the most glaring symptom of cultural collapse in a democracy hanging on to truth by the barest of threads”.

This fateful juncture has been looming for a while. The first warning signs came in October 2024, when Bezos yanked the Post’s planned endorsement of Trump’s Democratic rival Kamala Harris just 11 days before the presidential election.

A wave of public revulsion ensued, leading to the cancellation of at least 250,000 Post subscriptions.

Soon after, the billionaire unilaterally imposed new strictures on the paper’s opinion content. He introduced what he called his “two pillars”: “personal liberties and free markets.”

That drove many of the paper’s top commentators rushing for the exit, among them the economics columnist Eduardo Porter, who now writes for the Guardian. “This layering of dogma undermined critical thinking,” Porter recalled. “It turned the Post into something more akin to a church, with tight constraints on thought.”

This week’s day of the long knives has left many people desperately seeking explanations. There were clearly business motives at play: you don’t get to be a gazillionaire like Bezos without caring about profit lines, and the Post has been battered in recent years by harsh industry headwinds.

But there are other, more sinister, interpretations. McCartney thinks back to 2019 when Amazon lost a $10bn Pentagon cloud-computing contract during Trump’s first term.

Amazon complained in a lawsuit that this was a blatant act of retaliation by Trump, punishing Bezos for the Washington Post’s piercing coverage of his administration. Could it be that the bruising experience led Bezos to change tack, concluding that shining a light in defense of American democracy came at too high a price for the jewels in his business empire, Amazon and Blue Origin?

“It’s very likely that the desire to appease Trump, to placate him, is playing a role in these decisions,” McCartney said.

That’s a chilling thought for such a beacon of accountability journalism as the Washington Post. And it is set against the already parlous state of US media.

Since 2000, some 3,500 newspapers have closed shop, abandoning one in four Americans who now live in news deserts with no local newspaper. The most recent casualty was the Pittsburgh Post-Gazette, which will publish its final edition in May. It was founded in 1786, three years before George Washington donned the mantle of first president.

While many papers have been folding, others have fallen into the hands of a new breed of super-wealthy tech and venture capitalist owners who, like Bezos, see journalism as an asset to monetize: the Los Angeles Times was acquired in 2018 by a biotech billionaire, Patrick Soon-Shiong.

Like Bezos, Soon-Shiong has displayed symptoms of Trump Appeasement Syndrome. He too refused to allow his paper to endorse Harris days before the 2024 election.

Historic newspapers brought low, news deserts proliferating: this is fertile ground on which misinformation and the Maga pestilence can grow. Trump has cultivated it relentlessly to his advantage.

Long hostile towards what he calls the “fake news media”, Trump has taken his vendetta against truth-seekers to a new level. He has stripped public media channels NPR and PBS of more than $1bn in federal funding, launched full-frontal attacks on individual journalists and outlets exposing his corruption and lies and sustained a bullying campaign against corporate owners designed to browbeat them into subservience.

CBS News is the consummate example. Trump leaned on Paramount, which owned the news network, with a $10bn lawsuit over a 60 Minutes pre-election interview with Harris. Paramount settled for $16m, even though the suit was widely ridiculed as spurious.

Front of Paramount’s mind, no doubt, was its upcoming merger with Skydance Media that required federal – ie Trump’s – approval.

Following the merger, David Ellison became CEO of Paramount Skydance. He is son of the billionaire Oracle co-founder Larry Ellison, who is a close friend and adviser of Trump’s.

The younger Ellison went ahead and appointed the anti-woke commentator Bari Weiss as editor in chief of CBS News, sending shockwaves through the storied network’s dazed and demoralised staff. Weiss, who came to the job with no TV industry experience, has swiftly confirmed their fears.

She pulled a 60 Minutes segment on the notorious Cecot mega-prison in El Salvador to which the Trump administration had been deporting immigrants. Among her early hires as CBS News contributors are a Trump loyalist and former US marine, a prominent vaccine skeptic buddy of the health secretary Robert F Kennedy Jr, and fellow anti-woke firebrand Niall Ferguson.

The cumulative malaise that is descending over US media leaves the country’s democratic institutions vulnerable to attack. It can’t be exclusively blamed for Trump’s excesses.

There are plenty of other willing accomplices and capitulators, including universities like Columbia, corporate law firms and the gung-ho conservative activists who now control the supreme court.

But from Trump’s perspective, a media on its knees surely helps. The results are present everywhere you look.

Trump is unleashed, unchained. He feels so comfortable in his regal skin that he can berate a respected female CNN reporter questioning him on the Epstein files for never smiling.

He can peddle unashamedly in racism, posting a video depicting the first Black president and his first lady as monkeys.

He can send a masked paramilitary into the streets of Minneapolis, resulting in Americans getting killed for exercising their first amendment rights. And when the polls for November’s midterm elections look challenging for him, he can prepare for another blitzkrieg on the very foundations of American democracy: the ballot box.

There’s a paradox in all this. Many of the democratic norms that Trump is obliterating – take for example his destruction of the norm of Department of Justice independence in his persecution of his political opponents – were laid down in the 1970s in the wake of the Watergate scandal.

That’s the same Watergate scandal that was brought into the light by that pair of courageous reporters at a newspaper called the Washington Post.

A UK dairy delivery business is to begin collecting unwanted or broken toys, mobile phones and laptops while dropping off milk, orange juice and butter in its latest attempt to expand.

The Modern Milkman was founded by entrepreneur Simon Mellin in Burnley, north-west England, in 2019 and delivers groceries to more than 100,000 households across the UK.

The business will now start collecting electronic goods and toys to give to recycling specialist EMR Group, which will repurpose or recycle the items. Consumers pay £2.50 a time for a collection bag.

British households have an average 30 broken tech items each – up from 20 four years ago, according to non-profit organisation Material Focus. Britons dispose of about 2m tonnes of electronic waste every year.

Retailers must now offer take-back schemes and some councils do kerbside collections but it can still be hard to find an easy way to get rid of small items such as cables, chargers and old phones.

“We did a lot of research and there is not really a convenient way to deal with this stuff,” said Mellin. The service has been trialled in four regions and would now be expanded across the group’s operations. It also has plans to tackle other waste such as soft plastics or textiles in future.

“It is about how we build a stronger proposition and make ourselves more valuable to our customers,” he said, with a focus on “sustainable growth rather than blowing the barn doors off”.

Modern Milkman founder Simon Mellin says there is ‘not really a convenient way’ to recycle toys, mobile phones and laptops. Photograph: Supplied

The business operates through local independent suppliers and a collection of franchisees who employ delivery workers across about 40% of the UK – from Newcastle, Preston and Blackburn to London and Bristol.

Mellin, who grew up on a farm and says he left school with no qualifications, admitted the business had endured “a rollercoaster” in its first years as demand for deliveries in the UK ballooned during the pandemic and later fell back.

However, UK sales rose last year and are continuing to increase as the company reaches more homes and offers new services, Mellin said.

The Modern Milkman is also expanding in the US after acquiring local businesses which serve homes in Connecticut, Massachusetts, Rhode Island, Ohio, and New York. Mellin said sales in the younger US business were also growing “at pace”.

Sales for the group rose 13% to £52m in 2024, driven by expansion in the US, but the company made a pre-tax loss of £6.3m, narrowing from a £10.6m loss in the prior year. Last year, sales rose about 20% as the UK and US markets both saw growth, partly helped by the launch of a loyalty scheme.

Grocery delivery firms have been forced to adapt amid heavy competition and a slowing market since the pandemic. Photograph: Supplied

Grocery delivery firms have been forced to adapt amid heavy competition and a slowing market since the pandemic.

Rapid grocery delivery specialists such as Getir have closed down as big supermarket chains such as Tesco, the Co-op and Sainsbury’s have expanded their own operations and worked with delivery specialists such as Deliveroo and UberEats.

Milk & More, the UK’s biggest specialist dairy delivery service, was sold by yoghurt maker Müller to dairy firm Freshways in January 2024 as the cost of living crisis hit sales.

Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

Arm Holdings (NasdaqGS:ARM) reported record Q3 results, with strong contributions from AI and data center related revenues.

The company is shifting from a mainly mobile focused business toward a broader AI and compute platform role.

New partnerships with large cloud hyperscalers and expanded compute subsystems are gaining traction across customers.

Management highlighted increased R&D commitments that support this repositioning in AI and data center markets.

For investors watching NasdaqGS:ARM, the share price sits at $123.7, with a 17.4% gain over the past week and 10.7% over the past month. Over the past year, the stock shows a 23.9% decline, so the recent move comes against a weaker 12 month backdrop. That mix of short term strength and longer term pressure helps frame how the market is reacting to Arm’s Q3 news and changing business profile.

Looking ahead, the key questions are how durable AI and data center demand will be for Arm, and how quickly new compute subsystems and hyperscaler partnerships translate into broader revenue streams. The company is putting clear emphasis on R&D and deeper platform engagement with players like AWS, NVIDIA and Microsoft. These initiatives may influence where Arm ultimately fits within evolving compute architectures.

Stay updated on the most important news stories for Arm Holdings by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Arm Holdings.

NasdaqGS:ARM Earnings & Revenue Growth as at Feb 2026

How Arm Holdings stacks up against its biggest competitors

Arm’s record Q3 shows how quickly its business mix is tilting toward AI and data center workloads, with revenue of US$1.24b versus US$983m a year earlier and royalty and licensing activity supported by higher value architectures and pre integrated compute subsystems. For you as an investor, the key shift is that Arm is moving from a mainly smartphone royalty story to a broader compute platform that competes more directly with CPU ecosystems from Intel, AMD and emerging RISC V designs across cloud, edge and automotive use cases.

The latest results fit neatly into existing narratives that Arm is leveraging its large customer base and developer community to extend into data centers, edge AI and physical AI applications such as robotics and self driving systems. At the same time, earlier narrative flags about patent expirations in the 2030s, high R&D intensity and SoftBank’s control are still part of the story, so this pivot toward higher value AI centric products can be seen as an attempt to deepen monetization per chip rather than radically expand the customer count.

Q3 revenue of US$1.24b and nine month revenue of US$3.43b show that Arm is already operating at scale in AI focused segments, with data center royalties and higher rate products contributing meaningfully.

Expanded partnerships with hyperscalers such as AWS, NVIDIA and Microsoft, and traction for compute subsystems, give Arm more ways to participate as customers move to custom silicon and AI specific chips.

Net income in Q3 moved from US$252m to US$223m even as revenue rose, hinting that higher R&D and go to market spending could weigh on margins while the new AI and data center businesses mature.

Management and analysts still point to risks around smartphone exposure, memory chip shortages, competition from RISC V and geopolitical issues, which could limit how smooth this business model shift proves to be.

From here, it will be important to see whether AI and data center royalties continue to gain share of Arm’s overall mix, and whether higher R&D spending starts to show up in sustained profit growth rather than just top line momentum. You can keep track of how different investors are interpreting this shift and how it ties into longer term expectations by checking community narratives for Arm on the company’s dedicated page, especially as new guidance, product launches and hyperscaler roadmaps are announced through 2026.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ARM.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

Liquidity Services (LQDT) is back on investors’ radar after first quarter earnings showed higher profitability, with net income of US$7.49 million and improved EPS, alongside guidance that points to further earnings strength in the March quarter.

See our latest analysis for Liquidity Services.

At a share price of US$32.51, Liquidity Services has logged a 39.35% 90 day share price return and a 147.41% three year total shareholder return, while the 1 year total shareholder return is roughly flat. This suggests recent earnings strength is aligning with a longer term improvement story rather than a short term swing.

If strong execution in resale and liquidation platforms has your attention, this could be a good moment to broaden your watchlist and check out 22 top founder-led companies.

With the shares up sharply over 90 days and trading below a US$43 analyst target and some intrinsic value estimates, the key question now is simple: Is Liquidity Services still mispriced, or is the market already baking in future growth?

At $32.51, the most followed narrative pegs Liquidity Services’ fair value closer to $41, putting current pricing at a clear discount in that framework.

Secular trends toward sustainability and circular economy solutions are driving more organizations to liquidate and resell surplus assets via specialized marketplaces; this is reflected in record asset listings, expansion into new verticals (construction, heavy equipment), and high client acquisition across government and enterprise sellers. (Steady increase in asset throughput and recurring fee-based revenue streams)

Read the complete narrative.

Curious what sits behind that valuation gap? The narrative leans heavily on gradually rising revenues, thicker margins, and a future earnings profile that assumes a premium P/E. The exact hurdle it sets is anything but modest.

Result: Fair Value of $41 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this hinges on surplus volumes staying robust, and there is a real risk that tighter inventory management or brands scaling their own resale channels could cap Liquidity Services’ throughput.

Find out about the key risks to this Liquidity Services narrative.

The story changes when you look at Liquidity Services through its P/E ratio instead of fair value estimates. At 33.9x earnings, the shares trade well above both the US Commercial Services industry on 26.1x and an estimated fair ratio of 23.3x. This points to valuation risk rather than a clear bargain, and if sentiment cools, that premium could narrow faster than optimists expect.

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGS:LQDT P/E Ratio as at Feb 2026

If you read this and think the assumptions feel off, or you prefer to test your own inputs and views on Liquidity Services, you can build a tailored narrative in just a few minutes and Do it your way.

A great starting point for your Liquidity Services research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

If Liquidity Services has sharpened your focus, do not stop here. Widening your idea set now can be the difference between spotting and missing the next opportunity.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LQDT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Eli Lilly and Company (NYSE:LLY) is one of the 13 Best Extremely Profitable Stocks to Invest in Now.

Analysts Project Eli Lilly (LLY) to Deliver 21%+ Revenue Growth and 40%+ Adjusted Earnings Growth in 2026

Pixabay/Public Domain

On February 2, 2026, Reuters reported that long-standing expectations that the global obesity drug market would reach $150 billion over the next decade are being reconsidered amid declining U.S. prices for GLP-1 therapies and intensifying competition. The new projections indicate that the market will reach closer to $100 billion by 2030, which is roughly 30% less than previous estimates. Furthermore, the $150 billion mark is not expected to be reached until 2035.

Citing pressure from cash-pay competition and faster-than-expected generic entry, Jefferies reduced its peak market estimate by 20% in January. The firm’s expected market size as of 2035 stands at $80 billion.

Even with these revised assumptions, LSEG’s consensus estimates still expect Eli Lilly and Company (NYSE:LLY) to deliver more than 21% revenue growth and more than 40% adjusted earnings growth in 2026 compared to 2025.

Against this backdrop of demand, Lilly outlined its strategic initiative two days earlier.

On January 30, 2026, Eli Lilly and Company (NYSE:LLY) announced that it would construct a $3.5 billion pharmaceutical manufacturing facility in Pennsylvania, which will be its fourth new location in the United States. As GLP-1 competition accelerates, the plant will work on injectable weight-loss drug production like retatrutide, with construction expected to begin this year and operations starting in 2031.

Eli Lilly and Company (NYSE: LLY) develops and commercializes innovative medicines across diabetes, obesity, oncology, immunology, and neuroscience.

While we acknowledge the potential of LLY as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you’re looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

READ NEXT:What Are the Best Stocks to Buy Right Now? and 10 Stocks Under $1 That Will Explode.

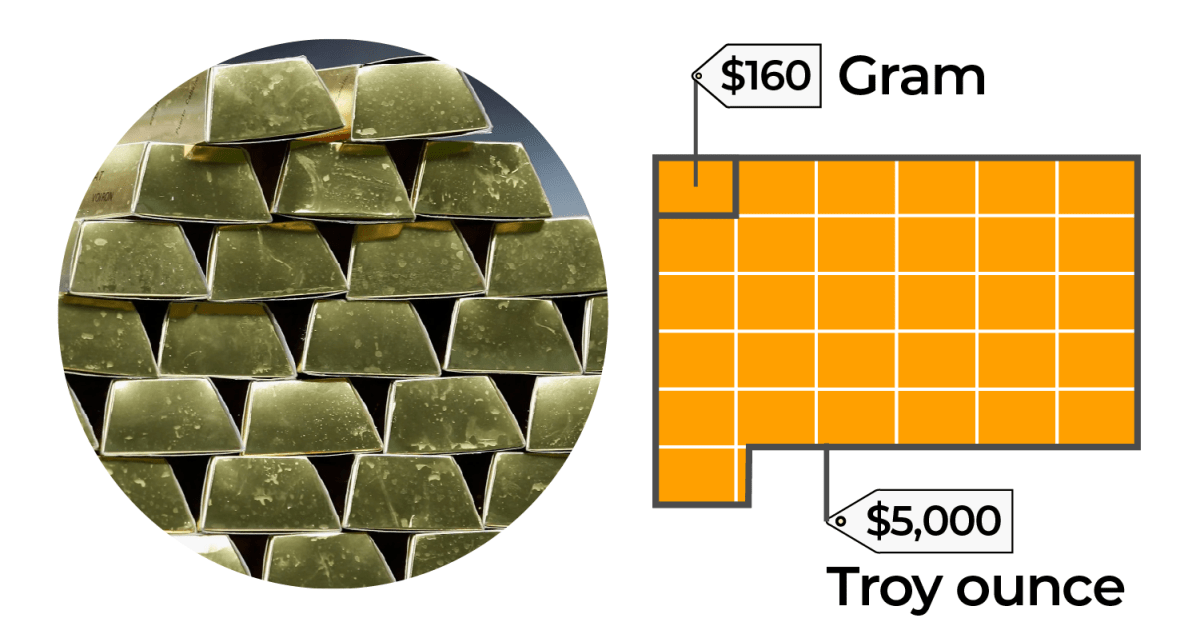

Interest in gold has skyrocketed in recent weeks, with the price of one ounce hitting an all time high of $5,600 on January 29 before settling back to just under $5,000 on Sunday.

As economic conditions fluctuate and geopolitical tensions rise, more individuals are seeking gold as a secure investment.

In this visual explainer, Al Jazeera breaks down how gold value is determined, the prices of gold coins in different markets, and the countries holding the largest reserves.

How is the value of gold measured?

Understanding the value of a gold item requires knowing its weight in troy ounces alongside its purity in karats.

(Al Jazeera)

Weight (in troy ounces)

The weight of gold and other precious metals like silver and platinum is commonly measured in troy ounces (oz t). One troy ounce is equal to 31.1035 grammes.

At $5,000 per troy ounce, 1 gramme of gold is worth about $160, and a standard 400-troy-ounce (12.44kg) gold bar costs $2m.

Troy ounces are different from regular ounces, which weigh 28.35 grammes and are used to measure everyday items including foods.

Purity (in karats)

Karat or carat (abbreviated as “K” or “ct”) measures the purity of a gold item. Pure gold is 24 karats, while lower karats such as 22, 18, and 9 indicate that the gold is mixed with less expensive metals like silver, copper, or zinc.

To determine the purity of gold, jewellers are required to stamp a number onto the item, such as 24K or a numeric value like 999, which indicates it is 99.9 percent pure. For example, 18K gold will typically have a stamp of 750, signifying that it is 75 percent pure.

Some typical values include:

24 karat – 99.9% purity – A deep orange colour, is very soft, never tarnishes and is most commonly used for investment coins or bars

22 karat – 91.6% purity – A rich orange colour, moderate durability, resists tarnishing and most often used for luxury jewellery

18 karat – 75% purity – A warm yellow colour, high durability, will have some dulling over time and most often used in fine jewellery

9 karat – 37.5%purity – A pale yellow colour, has the highest durability, dulls over time, used in affordable jewellery

Other karat amounts such as 14k (58.3% purity) and 10k (41.7% purity) are often sold in different markets around the world.

When you buy jewellery, the price usually depends on the day’s gold spot price, how much it costs to make, and any taxes.

If you know the item’s exact weight in grammes and the gold’s purity in karats, you can calculate the craftsmanship cost on top of that.

You typically cannot negotiate the spot gold price, but you can often haggle over the craftsmanship costs.

The price of gold has quadrupled over the past 10 years

Gold has been valued for thousands of years, serving various functions, from currency to jewellery. The precious metal is widely regarded as a safe haven asset, particularly in times of economic uncertainty or market volatility.

Up until 1971, the United States dollar was physically defined by a specific weight of gold. Under the classical gold standard, for nearly a century, from 1834 until 1933, you could walk into a bank and exchange $20 for an ounce of gold.

In 1933, amid the Great Depression, the price was raised to $35 per ounce to stimulate the economy.

In 1971, under President Richard Nixon, gold was decoupled from the dollar, and its price began to be determined by market forces.

Over the past 10 years, the price of gold has quadrupled from $1,250 in 2016 to around $5,000 today.

(Al Jazeera)

How is the price of gold determined in different countries?

Gold is priced globally based on the spot market, where one troy ounce is traded in US dollars on exchanges such as London and New York. Local prices vary as the dollar rate is converted into domestic currencies, and dealers add premiums for minting, distribution and demand.

Taxes and import duties further influence the final cost: India adds 3 percent GST, while the United Kingdom and United Arab Emirates impose none on gold investments.

Different countries produce unique gold bullion coins and bars, each with its own distinct features and cultural significance. Notable examples include the Gold Eagle from the US, the Gold Panda from China, and the Krugerrand from South Africa.

Which countries have the most gold reserves?

The US leads global gold reserves with 8,133 tonnes, nearly equal to the combined total of the next three countries. Germany is in second place with 3,350 tonnes, and Italy comes in third with 2,451 tonnes.

The graphic below shows the top 10 countries with the largest gold reserves.

Investcorp Saudi Arabia Financial Investments Company (together with its affiliates, “Investcorp”), a leading global alternative investment manager, and SNB Capital, Saudi Arabia’s largest asset manager, today announced a strategic partnership framework focused on cooperation across asset management, investment banking, and wealth management.

The partnership combines Investcorp’s global investment platform and deep experience across alternative asset classes with SNB Capital’s strong investment banking expertise and capabilities in fund structuring and development. Together, the firms aim to originate and capitalize on investment opportunities in Saudi Arabia and internationally, spanning Private Equity and Real Assets.

Both Investcorp and SNB Capital see significant potential in Saudi Arabia, underpinned by strong economic fundamentals and the ambitious Vision 2030 reform agenda. As the Kingdom’s growth accelerates, sectors such as technology, logistics, healthcare, and infrastructure are experiencing rapid expansion, creating compelling opportunities for strategic capital deployment that support long term economic diversification, resilience, and global competitiveness.

Leveraging deep local market expertise, strong regulatory engagement, and a proven track record of structuring and executing landmark transactions, SNB Capital supports the advancement of Saudi Arabia’s capital markets, in line with the Kingdom’s Vision 2030 objectives. An autonomous subsidiary of Saudi National Bank, the largest bank in the region, SNB Capital is a market leader and the largest Sharia-compliant asset manager in the world, with Assets under management (AUM) of SAR 246 billion (USD 65 billion).

Mashaal AlJomaih, Managing Director and CEO of Investcorp Saudi Arabia Financial Investments Company, commented: “Through our strategic partnership with SNB Capital, we are uniquely positioned together to unlock new opportunities and drive innovation across asset management, investment banking, and wealth management. Together, we look forward to delivering value to our clients while supporting Saudi Arabia’s continued growth and economic development.”

BP will face pressure from shareholders to prove it can leave a turbulent period in the past as it prepares to reveal its full-year results this week.

The company is expected to follow industry rivals by reporting weaker annual profits after global oil prices fell for a third consecutive year in 2025, in the steepest decline recorded since the Covid pandemic.

City analysts forecast BP profits of about $7.5bn (£5.5bn), down from almost $9bn in 2024, following an expected slump in fourth quarter earnings after crude prices fell below $60 a barrel for the first time in almost five years.

Meg O’Neil, who will become the chief executive of BP from April, will face pressure from investors to set out a new strategic vision, while activist shareholders continue to push the oil company to prepare for a long-term decline in fossil fuel demand.

This month a group of investors led by the Australasian Centre for Corporate Responsibility, which includes the workplace pension scheme Nest, filed a resolution that called for the company to set out how it would control its spending on oil and gas projects in the years ahead.

Dutch shareholder activists at Follow This are also calling for BP to disclose its strategy for creating shareholder value under scenarios of declining demand for fossil fuels.

BP started up seven new oil and gas projects last year as the company returned its focus to fossil fuels in an effort to resuscitate itsfortunes after trying to diversify into major renewable energy investments. Five of the seven projects were delivered ahead of schedule.

Analysts at Citi told clients in a recent investor note that BP’s share price has outperformed its European rivals by 4.4%, the equivalent of about $4bn of additional equity value over the last six months. They expect that rival Shell’s “material exploration success” off the coast of Brazil could add a further $15bn to $20bn to the company’s value.

“We think all the ingredients are there for a substantial change in narrative,” Citi said.

However, shareholder activists and green groups are preparing to oppose BP’s fresh investments in new fossil fuel projects. They argue the projects will not prove to be financially sustainable as electric vehicles and that the shift to clean energy erodes demand for oil and gas.

“The new chief executive needs to come up with a strategy to address the world’s declining oil and gas markets,” said Mark van Baal, the founder of Follow This.

The International Energy Agency expects oil demand to begin falling from about 2030 in all but its most conservative outlook for global energy use.

Follow This said the new resolution, which was filed ahead of BP’s annual meeting in April, would increase shareholder pressure and focus attention on the financial unsustainability of fossil fuel business models.

“In recent years the strategy has been shaky; shifting from left to right,” Van Baal said. “In our opinion they didn’t fail because, as they suggested, they went too far too fast on green energy. They failed because their strategy was completely unclear.”