Qaasid News

Download Our App

Latest News from Pakistan

New nonstop flights from Austin coming in 2026

December 29, 2025

Andy Zaltzman: ‘Aristophanes is total comedy: political satire, slapstick and dick jokes’ | Stage

December 29, 2025

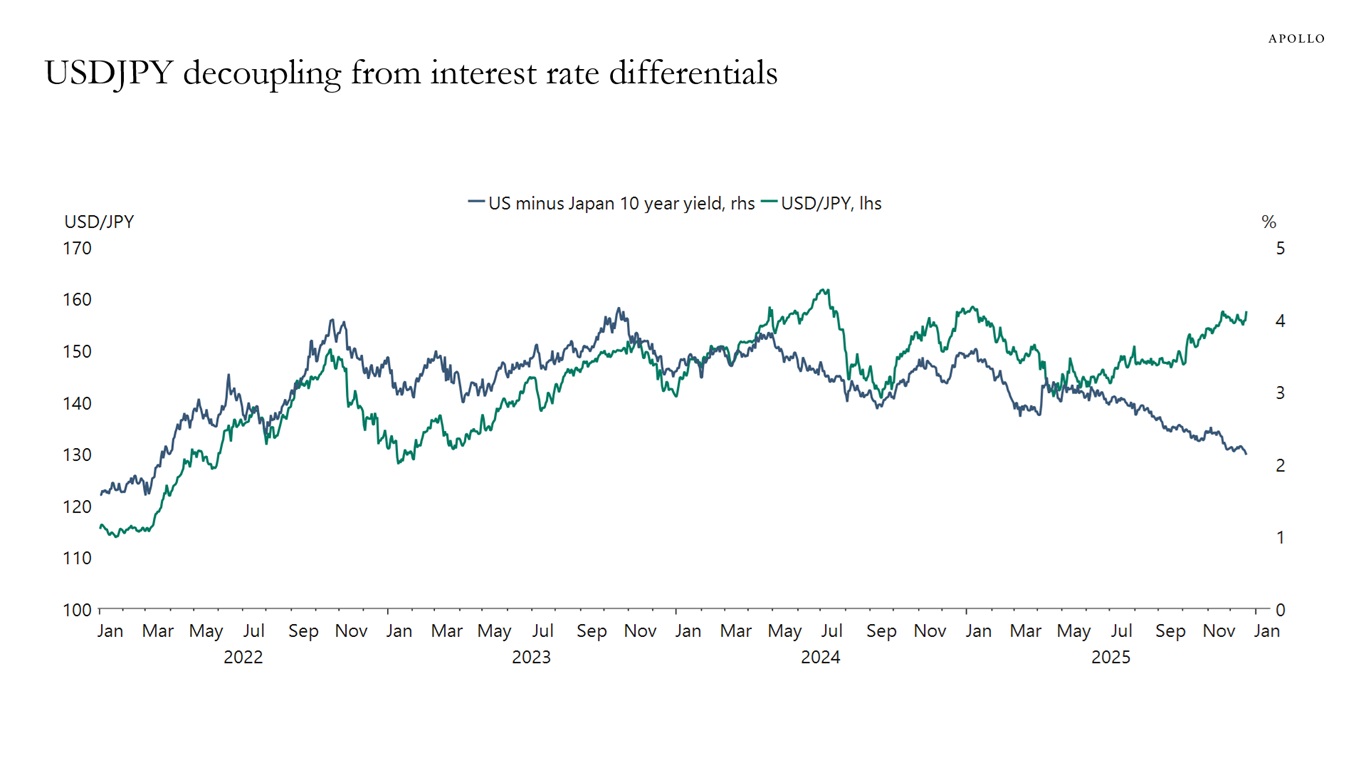

Yen Much Weaker Than Interest Rate Differentials Would Have Predicted

December 29, 2025

Hidden causes of depression you may not know

December 29, 2025

Statement by HRVP Kallas and Commissioner Kos on Kosovo parliamentary elections – European Commission

December 29, 2025

Hormone therapy has “no impact” on dementia risk, study finds

December 29, 2025

Wild things we learned about Earth in 2025

December 29, 2025

South Asia’s Dairy Intolerance Could Help Explain Our Ability to Drink Milk : ScienceAlert

December 29, 2025

Podcast tours are all the rage: Inside the big business of live shows

December 29, 2025

Even ‘Avatar: Fire and Ash’ can’t lift 2025 box office out of pandemic-crisis doldrums

December 29, 2025