Three-time WNBA champion Candace Parker headlines the 2026 Women’s Basketball Hall of Fame class, which celebrates a powerhouse lineup of players, coaches, and pioneers who transformed the sport.

Announced on Thursday (30 October), the class…

Three-time WNBA champion Candace Parker headlines the 2026 Women’s Basketball Hall of Fame class, which celebrates a powerhouse lineup of players, coaches, and pioneers who transformed the sport.

Announced on Thursday (30 October), the class…

The title track of Everybody Scream provides a suitably striking opening for Florence + the Machine’s sixth album. A sinister organ and a choir of voices harmonise in the style of a horror theme, replaced in short order by the sound of…

Extreme weather events – such as catastrophic floods or prolonged heatwaves – are increasing in frequency and intensity (IPCC 2021). This has sharpened the focus of policymakers ahead of COP30 on the economic resilience of developing and advanced economies. While there is a growing consensus that these events cause serious macroeconomic losses (Krebel et al. 2025), accurately quantifying them remains difficult (Aerts et al. 2024).

For advanced economies, evidence of strong and significant negative effects has been more challenging to document, especially in studies using cross-country data (Botzen et al. 2019, Klomp and Valckx 2014). There is growing recognition that the highly localised nature of weather shocks calls for studying their impacts at a subnational level (Goujon et al. 2024, Dell et al. 2014), and that combining granular data across countries and event types is essential to fully capture their macroeconomic effects.

Against this background, in new work (Costa and Hooley 2025), we use regional data for over 1,600 regions across 31 OECD countries from 2000 to 2018 to assess the economic consequences of extreme weather events in advanced economies, including how impacts propagate beyond the original event location via spillovers.

The most severe events reduce GDP in a region directly affected by a disaster by up to 2.2% relative to trend, with losses of around 1.7% persisting after five years (Figure 1). But not all disasters matter equally. The most severe events – defined as affecting at least 0.1% of a region’s population – generate disproportionately larger output losses than more moderate disasters, while minor disasters show no measurable GDP impact. Such non-linearity has also been documented by others (Felbermayr and Gröschl 2014) and is likely due to capacity constraints – technical and organisational limits that bind only in big disasters (Hallegatte et al. 2007). Small shocks are absorbed; large ones overwhelm.

Figure 1 Change in the level of real GDP following severe disasters (percent)

Labour markets are a key adjustment channel: employment declines in line with GDP and affected regions see net outward migration. Mobility is an important coping mechanism for households, but it can also deepen local output losses by eroding demand and depleting human capital.

Severe disasters also put downward pressure on prices: the GDP deflator declines to about 1% below trend in the medium term. Demand shortfalls dominate any supply-side inflationary pressures from damaged capital, disrupted production and labour market dislocations.

These are net effects on output and prices, so they already incorporate offsetting forces such as reconstruction spending, insurance payouts, and government relief transfers. The persistence of large losses shows that such support, while helpful, is, on average, insufficient to return the economy to its pre-disaster path.

The economic damage does not stop at regional borders. We identify material negative spillovers: a severe disaster occurring within 100 km of a region leads to a further 0.5% decline in GDP – roughly a quarter of the direct effect. These spillover channels are likely to reflect several factors, including disrupted supply chains, reduced demand from nearby affected areas, and population displacement.

Combining direct and spillover effects and aggregating across OECD countries, severe disasters in our sample reduced GDP by over 0.3% per year on average, with spillovers contributing roughly half of the total loss (Figure 2).

Figure 2 Average annual impact of severe disasters on OECD GDP during 2006-2018 (percent)

The capacity of regions to withstand and recover from disasters varies significantly. Fiscal space matters: regions in countries with lower debt-to-GDP recover more quickly, as governments can deploy effective post-disaster support without requiring offsetting austerity measures that could exacerbate the economic downturn (Canova and Pappa 2021). Economic diversification and labour mobility also enhance resilience: diversified economies can shift activity to less-affected sectors, and higher mobility speeds up reallocation and limits persistent unemployment (Beyer and Smets 2015).

Sectoral patterns also differ sharply. Industrial output falls by more than twice as much as output in services after a severe disaster – unsurprising given industry’s reliance on fixed capital and networked supply chains – but it tends to rebound faster in the medium term as supply chains are restored and reconstruction spending ramps up.

Quantifying the potential economic losses caused by natural disasters is crucial for effective planning and decision-making. Our estimates – showing large, non-linear, and persistent costs even in advanced economies – call for climate damage projections to explicitly incorporate extreme-event impacts. The task is challenging, however, and while recent work has begun to incorporate temperature and precipitation volatility into climate damage functions, the most extreme ‘tail’ events are unlikely to be captured (Aerts et al. 2024).

The scale of losses also underscores the urgency of adaptation efforts in advanced economies, including investment in adaptive infrastructure – flood barriers, water storage, resilient transport and power – alongside credible post-disaster plans and deeper insurance markets (OECD 2024).

Our evidence of negative spillovers furthermore carries a clear policy message: climate adaptation cannot narrowly focus on the location of a potential hazard. When around half of the economic damage from natural disasters occurs in regions that are not directly hit, such a strategy would leave major costs unaddressed.

This points to several complementary priorities:

Strengthening resilience to spillover effects – alongside broader adaptation efforts – is critical to cushion the economic and social impacts of extreme weather and to prevent disasters from widening regional inequalities.

Aerts, S, L Stracca and A Trzcinska (2024), “Measuring economic losses caused by climate change,” VoxEU.org, 2 October.

Beyer, R and F Smets (2015), “Labour market adjustments and migration in Europe and the United States: how different?”, Economic Policy 30(84): 643–682.

Botzen, W, O Deschenes and M Sanders (2019), “The Economic Impacts of Natural Disasters: A Review of Models and Empirical Studies”, Review of Environmental Economics and Policy 13(2).

Canova, F and E Pappa (2021), “Costly Disasters & the Role of Fiscal Policy: Evidence from US States”, Fellowship Initiative Paper No 151, DG ECFIN, European Commission.

Costa, H and J Hooley (2025), “The macroeconomic implications of extreme weather events”, OECD Economics Department Working Paper No 1837.

Costa, H et al. (2024), “The heat is on: Heat stress, productivity and adaptation among firms”, OECD Economics Department Working Paper No 1828.

Dell, M, B Jones and B Olken (2014), “What Do We Learn from the Weather? The New Climate-Economy Literature”, Journal of Economic Literature 52(3): 740–98.

Felbermayr, G and J Gröschl (2014), “Naturally negative: the growth effects of natural disasters”, Journal of Development Economics 111: 92–106.

Goujon, M, O Santoni and L Wagner (2024), “Global exposure to climate change at a subnational jurisdiction level”, World Development Sustainability 5, 100168.

Hallegatte, S, J Hourcade and P Dumas (2007), “Why economic dynamics matter in assessing climate change damages: Illustration on extreme events”, Ecological Economics 62(2): 330-340.

Hsiang, S and A Jina (2014), “The causal effect of environmental catastrophe on long-run economic growth: Evidence from 6,700 cyclones”, NBER Working Paper 20352.

IPCC (2023), “Climate Change 2023: Synthesis Report”, Contribution of Working Groups I, II and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, IPCC, Geneva, Switzerland, pp. 35-115,

Klomp, J and K Valckx (2014), “Natural disasters and economic growth: A meta-analysis”, Global Environmental Change 26: 183-195,

Krebel, L, D Kyriakopoulou and J Talbot (2025), “The implications of severe weather events for the economy and monetary policy,” VoxEU.org, 7 February.

OECD (2024), “Accelerating climate adaptation: A framework for assessing and addressing adaptation needs and priorities”, OECD Economic Policy Paper No. 35.

Rosvold, E and H Buhaug (2021), “GDIS, a global dataset of geocoded disaster locations”, Scientific Data 8(61).

The Pakistan Vanaspati Manufacturers Association (PVMA) has urged the government to ensure the immediate payment of Rs6.5 billion owed by the Utility Stores Corporation (USC) to ghee and cooking oil manufacturers.

According to the association, the dues have been pending for over a year despite repeated reminders, causing financial strain for the industry.

In a statement, PVMA Chairman Sheikh Umer Rehan said that ghee and cooking oil mills across the country had already supplied products worth Rs6.5 billion to USC, but the non-payment of dues created a serious liquidity crisis for the manufacturers.

“Industrialists are facing capital shortages in meeting operational expenses and the import of raw materials, disrupting production processes,” he said and cautioned that if the issue was not resolved promptly, the sustainability of the entire industry could be at risk.

The association chairman emphasised that the issue was not only an industrial concern but also the one that would affect the credibility of the government. He noted that the association had been raising the matter with the Ministry of Finance, the Ministry of Industries and the Ministry of Commerce for the past one year, yet no practical action had been taken. “The continued delay in payments has eroded business confidence and fueled uncertainty in the economy,” he added.

Umer Rehan appealed to Finance Minister Muhammad Aurangzeb and Adviser to the Prime Minister on Industries and Production Haroon Akhtar Khan to take personal notice of the issue, initiate an inquiry and ensure swift disbursement of the outstanding amount.

He stressed that the ghee and cooking oil industry plays a vital role in ensuring the country’s food security and employment continuity, adding that it was the government’s responsibility to make timely payments to support the sector’s stability and contribution to economic growth.

Iron, one of Earth’s most common and unassuming metals, has just surprised scientists.

A Stanford-led team has discovered how to push iron into a higher-energy state than ever seen before, a feat that could reshape the future of…

Expect more Chinese epic costume dramas and Shanghai-set modern urban romance dramas in the coming years. And with both genres still at the zenith of their popularity in Asia, why change a winning formula? That seemed to be the message from a…

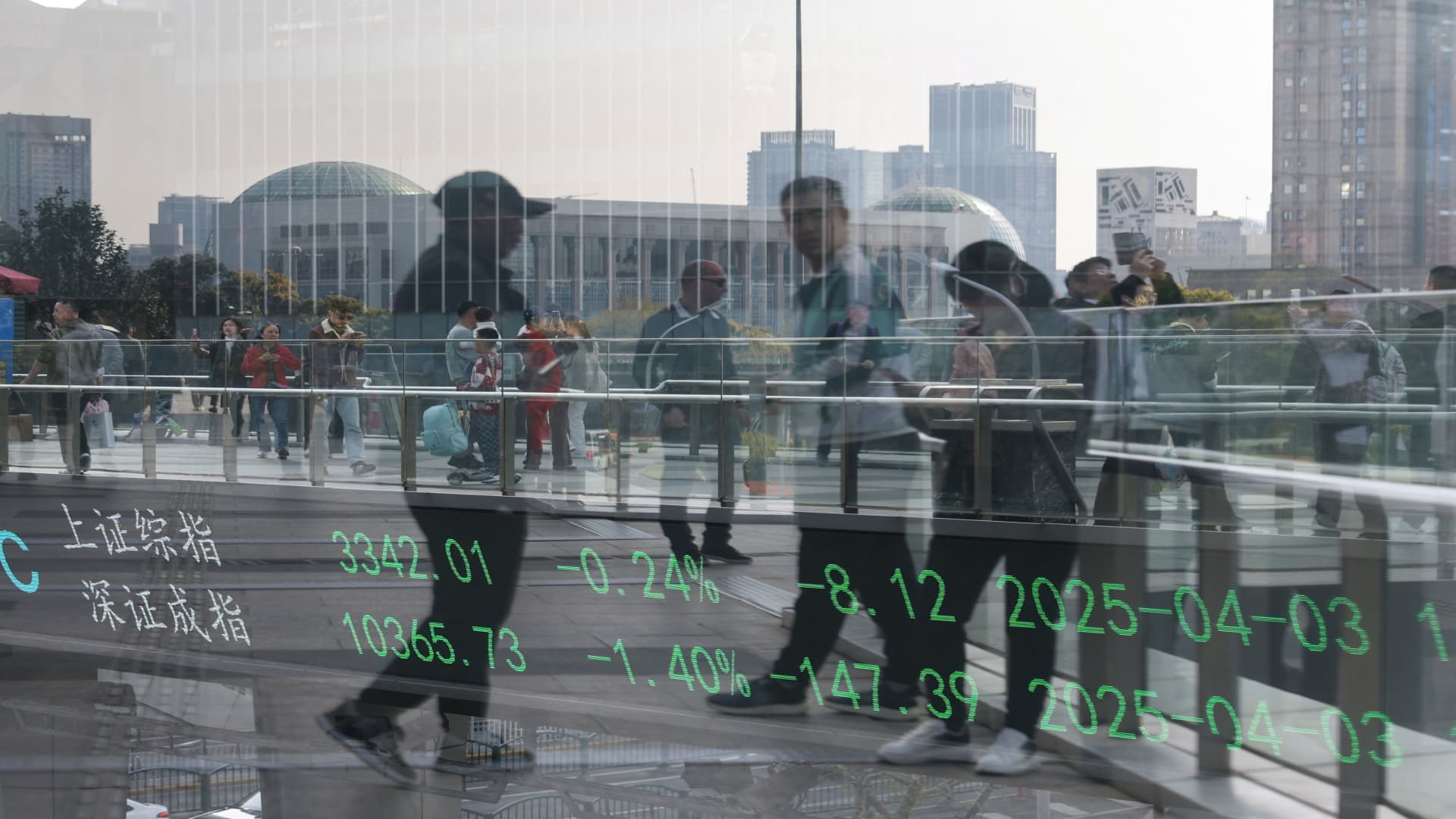

An electronic board shows Shanghai and Shenzhen stock indices as people walk on a pedestrian bridge at the Lujiazui financial district in Shanghai, China April 3, 2025.

Go Nakamura | Reuters

Asia-Pacific markets opened mostly higher Friday as…

Fathom Entertainment’s re-release of Summit/Lionsgate‘s Twilight posted $1.55M in its first day Wednesday.

The feature take on the Stephenie Meyer-penned saga started its rollout Wednesday. Today, Twilight Saga: New Moon will play,…

“The reason we have an office here is to be close to our investors,” Yao said in an interview with the Post on Thursday. “We have very important insurance companies that have already committed to our various products. To be close to clients is one thing we want to develop in Hong Kong.”

“Private wealth is also a big topic in our industry as a source of capital. Investment-wise it is very important for the secondary business,” Yao added. “So we have a lot of sellers here and we have most of the intermediaries, the investment bank side, also here. It’s also very critical for us to further expand our secondary business in the region.”

It has about 50 long-standing clients in the Greater China region. Its investors include insurance firms, sovereign wealth funds, private wealth investors and endowments.