Explore this week’s Macro Trends insights from Macrobond with the first installment below.

The US government remains in shutdown, leaving markets with very limited access to official economic data. Still, there is broad expectation that the Fed will move ahead with a rate cut this week:

- Data Blackout: With official releases paused, investors rely on alternative data sources to gauge the state of the US economy.

- New Fed Voice: Recently appointed Fed member Stephen Miran has argued for significant rate cuts, potentially pushing the Committee toward a more dovish stance.

- Bull Steepening: As the Fed shifts toward easing, short-term yields have dropped faster than long-term rates. How should investors position for this new dynamic?

Markets brace for a Fed rate cut as the US data blackout leaves investors searching for signals.

Diverging Views on the Path of Rates

Insights:

Markets are fully pricing a 25 bp rate cut, with attention shifting to forward guidance rather than the decision itself.

The Fed’s dot plot still signals a gradual easing path, while Fed funds futures expect a faster decline toward ~3% by 2026. That divergence will drive the market reaction.

The Miran Effect

Insights:

Stephen Miran was sworn in as a member of the Federal Reserve Board of Governors on September 16, 2025.

With Miran joining the FOMC, the dot plot took on a new shape — as he stood out as the only member projecting a Fed funds rate below 3%, signaling significant cuts.

The new Fed governor will likely attract extra attention, especially as discussions around Powell’s eventual successor gain momentum.

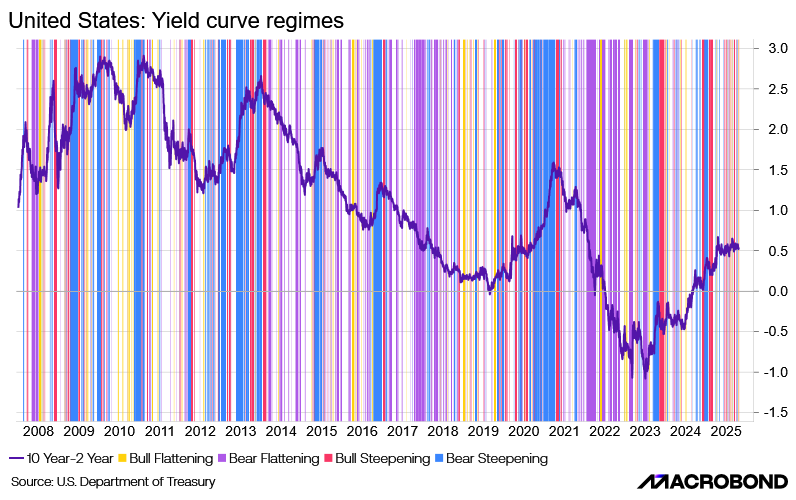

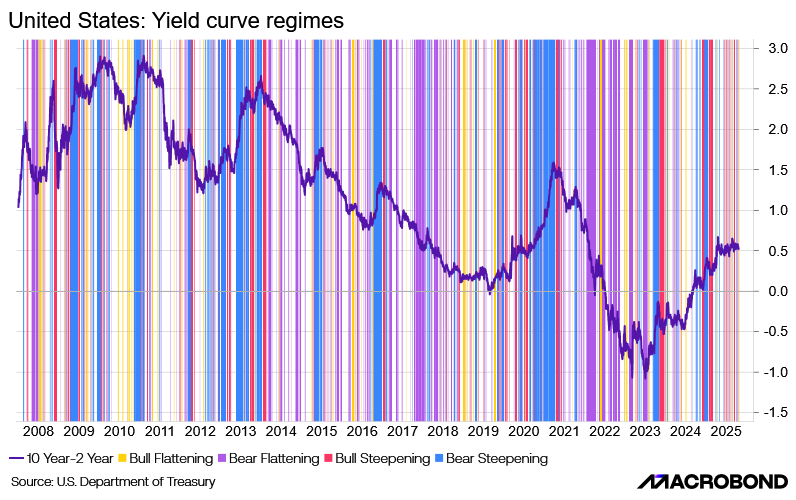

Bull or Bear Steepener?

Insights:

The Federal Reserve is in a rate-cutting cycle, while Trump’s fiscal policies are pushing longer-term yields higher through expectations of larger deficits and increased Treasury issuance. This mix of monetary easing and fiscal expansion is steepening the yield curve.

A key debate now is whether the steepening will be bearish or bullish:

- A bear steepener if long-term yields rise faster due to inflation and fiscal concerns

- A bull steepener if short-term rates fall more sharply as markets price in deeper Fed cuts

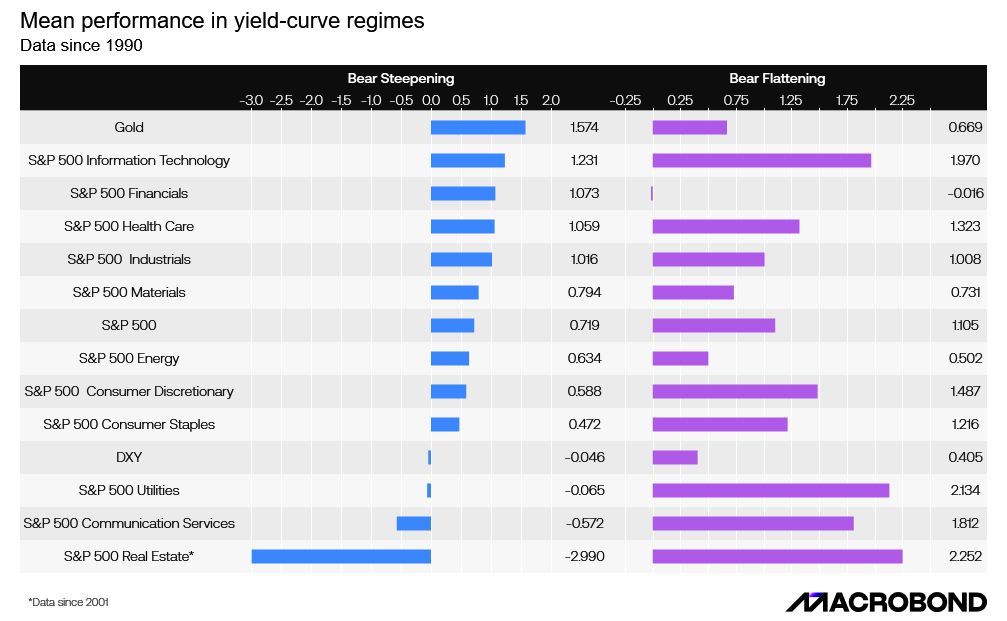

Average Asset Performance Across Yield Curve Regimes

Insights:

The direction this steepening takes will be crucial for market positioning, as equity valuations and fixed-income returns tend to react very differently under bear versus bull steepening regimes.

In this chart, you can see the historical performance of various equity sectors, fixed income, and gold across these different yield-curve environments.

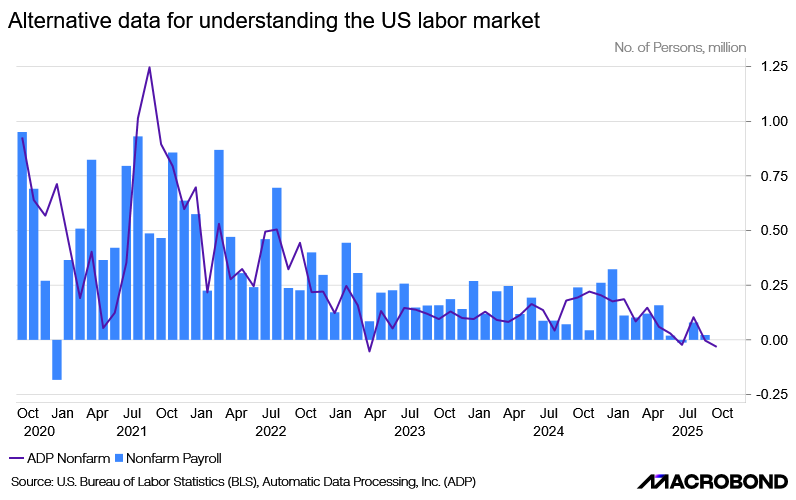

Alternative Data Takes the Lead on U.S. Labor Trends

Insights

With the U.S. government shutdown halting operations at the Bureau of Labor Statistics (BLS), official labor market data — including the monthly Nonfarm Payrolls report — will not be released. This data blackout leaves policymakers and markets without one of their most important economic indicators. In the absence of BLS data, attention will turn to ADP’s private-sector employment report as a key alternative gauge of labor market momentum ahead of the Fed’s upcoming policy decisions.

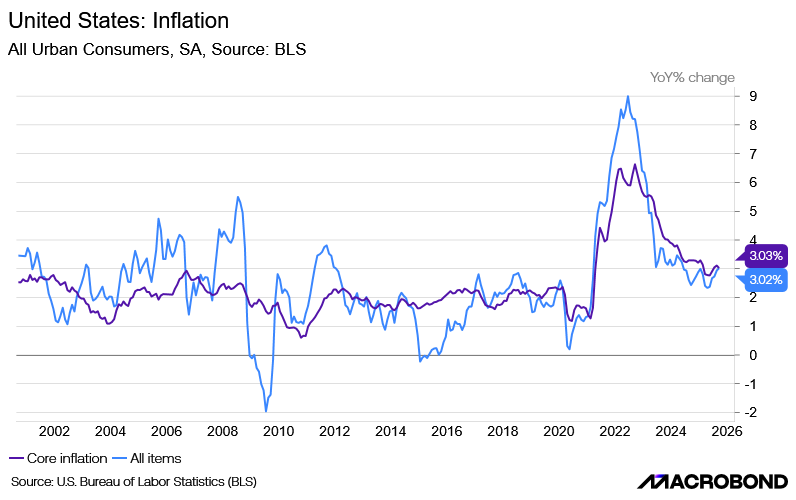

Inflation Holds Firm Amid Policy Uncertainty

Insights

Last Friday, despite the ongoing government shutdown, markets received fresh economic data — the Consumer Price Index (CPI) for September.

The report showed that inflation remains stubbornly high at 3 percent, reinforcing concerns that price pressures are proving more persistent than the Federal Reserve had hoped.

This resilience in inflation is likely to weigh on the Fed’s upcoming policy discussions, as it complicates the path toward potential rate cuts and raises questions about how long restrictive monetary conditions will need to stay in place.