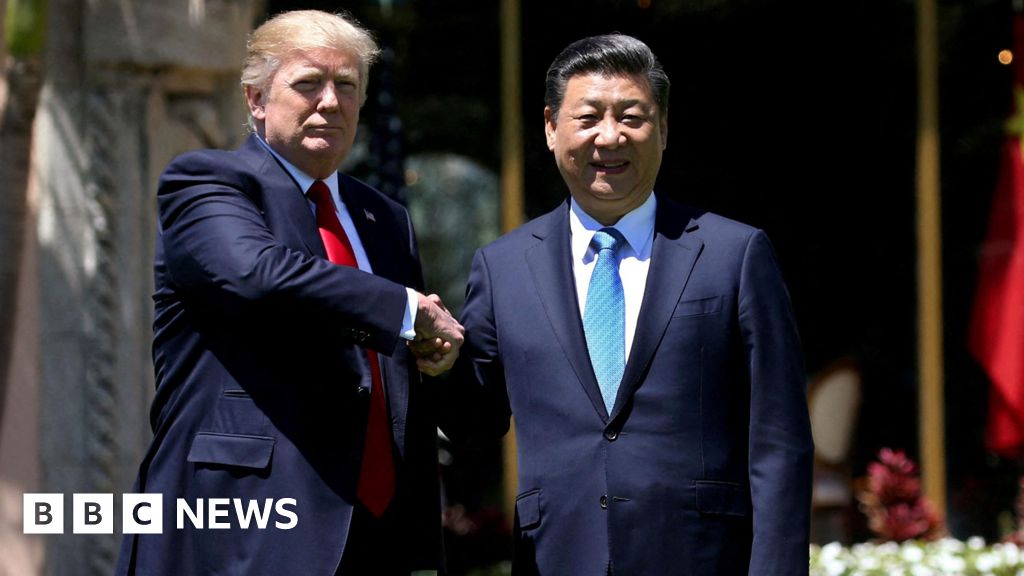

The US and China have agreed the framework of a potential trade deal that will be discussed when their respective leaders meet later this week, the US trade secretary has said.

Scott Bessent told the BBC’s US news partner CBS that this included a…

The US and China have agreed the framework of a potential trade deal that will be discussed when their respective leaders meet later this week, the US trade secretary has said.

Scott Bessent told the BBC’s US news partner CBS that this included a…

This next update is a game changer

NurPhoto via Getty Images

Whisper it quietly, but there’s a serious issue at the heart of Android. Google’s success with Pixel has exposed a disconnect with the world’s most popular OS. That’s good news…

The FIS Alpine Ski World Cup men’s season got underway on Sunday (26 October) with the giant slalom on the Rettenbach Glacier in Sölden, Austria, and Marco Odermatt wasted no time reminding the field why he remains the standard-bearer in the…

Plenty of folks have recreated the infamous Rocky scene where Sylvester Stallone memorably started the day off by necking five raw eggs.

Although consuming this yellow concoction has become something of a health trend online, a lot of people…

Atlético Madrid coach Diego Simeone was quizzed on Sunday by the media before he takes him to La Cartuja for a Monday night showdown with Real Betis. Simeone responded bluntly when he was questioned about how every bad result brings speculation…

Published on: Oct 26, 2025 07:47 pm IST

Qualys (QLYS) shares are trending slightly higher so far this month, showing around a 1% positive return over the past week. This comes at a time when the broader technology sector continues to face market volatility. Investors are keeping an eye on valuation and trends after recent pullbacks.

See our latest analysis for Qualys.

Zooming out, Qualys’s share price has slipped nearly 8% year-to-date but still posts a positive 1-year total shareholder return of around 6%. This reflects a mix of investor caution and enduring belief in its growth story. The momentum has faded recently, although its longer-term track record highlights an ability to deliver for shareholders.

Curious what else savvy investors are discovering? This could be a perfect time to broaden your research with fast growing stocks with high insider ownership

With Qualys trading below its analyst price target and fundamentals showing steady growth, the key question now is whether the stock is undervalued and offering potential upside, or if the market has already priced in future gains.

The current narrative fair value for Qualys lands at $141, which is noticeably higher than its last closing price of $128.05. This gap highlights ongoing optimism about the company’s prospects and sets the foundation for the key thinking driving this estimate.

Adoption of Qualys’ new cloud-native risk operations center (ROC) and Agentic AI platform positions the company as a leading pre-breach risk management provider. It offers unified orchestration, automation, and remediation across both Qualys and non-Qualys data. This opens incremental greenfield opportunities and should support higher ARPU and expanded TAM, leading to durable revenue and earnings growth.

Read the complete narrative.

What exactly propels this bullish narrative? Behind the ambitious price target are bold expectations about rising average customer spend, new platform launches and growing demand from global organizations. Want to see how much future growth, profit expansion and technology innovation must deliver in reality to make these numbers stack up? Find out what the consensus is betting on and what needs to go right by reading the full breakdown.

Result: Fair Value of $141 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, rapid AI innovation and new pricing models could disrupt Qualys’s momentum if competitors advance more quickly in development or if customer adoption trends unexpectedly shift.

Find out about the key risks to this Qualys narrative.

Palomar Holdings (PLMR) has been in the spotlight following a recent mix of cautious and optimistic signals from institutional investors. Changes in hedge fund positions, along with the completion of key reinsurance programs, have prompted renewed market attention.

See our latest analysis for Palomar Holdings.

After navigating a stretch of cautious sentiment related to reinsurance renewals and hurricane season risks, Palomar Holdings is showing more stable momentum. Its latest share price sits at $113.25, and while the short-term returns have been muted, the 1-year total shareholder return of 23.5% highlights growing long-term optimism despite recent volatility.

If you’re curious about what other companies are attracting institutional attention, now is a perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With the stock trading below analyst price targets and showing solid revenue and income growth, the question remains: Is Palomar Holdings undervalued at current levels, or are investors already pricing in future momentum?

With Palomar Holdings closing at $113.25 versus the most popular narrative fair value of $153.33, the case for upside is compelling and getting attention as analyst expectations shift.

Ongoing investment in proprietary technology, data analytics, and advanced underwriting disciplines is improving risk assessment and pricing accuracy, already reflected in strong combined ratios and low loss ratios. This should continue to enhance underwriting profitability and expand net margins over time.

Read the complete narrative.

Curious about what’s behind this bullish fair value? The narrative hangs on rapid growth projections. One key assumption could be surprisingly aggressive. There’s a crucial forward valuation embedded here that you may not expect for an insurer. Dig in to discover the foundational numbers and the future profit model that could shake up price targets.

Result: Fair Value of $153.33 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, intensifying competition and Palomar’s reliance on catastrophe-exposed property lines could quickly shift profitability and challenge the current growth narrative.

Find out about the key risks to this Palomar Holdings narrative.

While the market’s favorite narrative points to a bargain, looking at the company’s price-to-earnings ratio offers a more cautious perspective. Palomar trades at 19.6 times earnings, which is notably higher than the US Insurance industry average of 13.5 times and a peer average of 13.8 times. The fair ratio, which is what the market could eventually gravitate toward, is just 16.2 times. This substantial gap suggests that Palomar’s shares could be at risk of a pullback if expectations shift. Could these elevated multiples limit future upside?

Toyota has announced it will end Supra production next March, with 2026 being the car’s last model year. The automaker already introduced the Final Edition, which…

Aurora Innovation (AUR) shares have edged slightly higher recently, following a modest uptick of about 2% in the last day and smaller gains over the past week. Investors seem to be weighing the company’s performance during the month, as Aurora continues its work in autonomous vehicle technology.

See our latest analysis for Aurora Innovation.

Zooming out, Aurora Innovation’s 1-year share price return is still down double digits, while its three-year total shareholder return remains notably positive. After a recent stretch of modest gains, momentum is still searching for its footing as investors gauge the company’s long-term roadmap and evolving risk profile.

If Aurora’s recent moves have you reflecting on shifts across the sector, now is the perfect time to explore innovation on a broader scale through the See the full list for free.

With shares trading well below analyst price targets and impressive long-term gains in the rearview, investors now face a critical question: Is Aurora a bargain poised for growth, or is the market already factoring in its future potential?

At a price-to-book ratio of 4.8x, Aurora Innovation trades below its peer average of 5.9x based on this valuation measure. This suggests the stock is relatively more attractively priced compared to similar companies. With the last close at $5.15, this indicates the market is discounting Aurora relative to its book value more than its immediate peer group.

The price-to-book ratio compares a company’s market value to its net asset value. This metric is particularly relevant for asset-light and high-growth sectors like software and autonomous vehicles. For Aurora, this ratio reflects what investors are willing to pay for the company’s equity compared to the book value recorded on its balance sheet.

This valuation suggests investors may be skeptical about Aurora’s path to profitability or are discounting near-term challenges, despite the sector’s broader appetite for growth. However, the company’s price-to-book still remains higher than the US Software industry average of 4x. This signals the market may still be assigning a premium for its technology or future prospects relative to the average US software company, though less so compared to its closest peers.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 4.8x (UNDERVALUED compared to peers)

However, continued net losses and uncertainty around the company’s path to profitability remain challenges that could weigh on future share performance.