While stuttering was believed to have purely psychological causes up until about 30 years ago, scientists today attribute it to a variety of factors capable of contributing to its development. For instance, several genes have been…

Blog

-

Study links skin conditions to worse outcomes in mental health patients

Scientists have discovered that mental health patients who have skin conditions may be more at risk of worse outcomes, including suicidality and depression. This work, which may aid in identifying at-risk patients and personalising…

Continue Reading

-

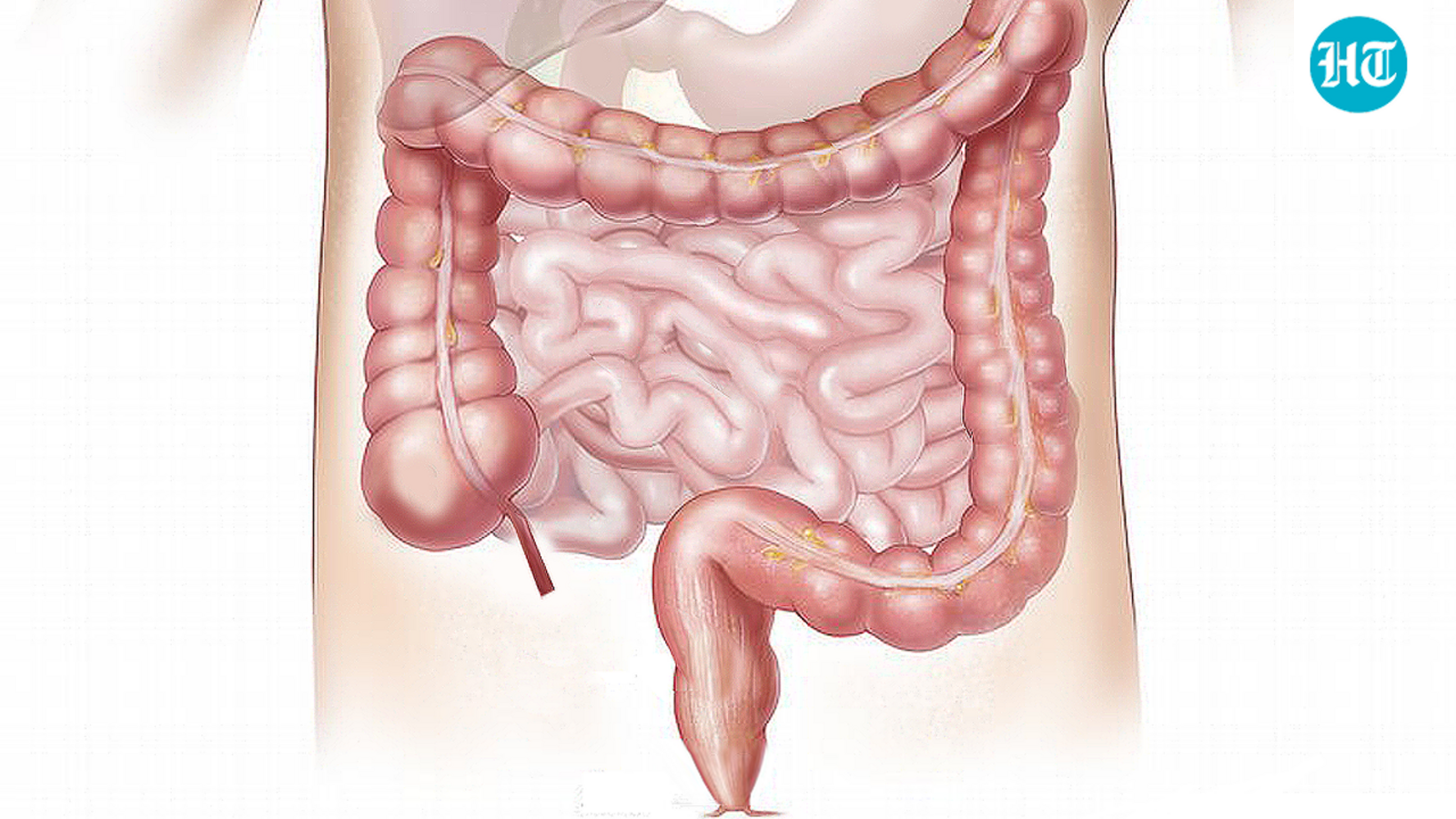

AIIMS gastroenterologist links feeling like you ‘can’t finish’ during bowel movements to colon cancer; shares 8 signs

Colon cancer often develops quietly, showing no clear symptoms in its early stages – which is why it’s often detected late. However, the body does send out subtle warning signs that should never be ignored. Recognising these early indicators…

Continue Reading

-

Researchers develop AI system to decode the human immune system

Researchers explore the human immune system by looking at the active components, namely the various genes and cells involved. But there is a broad range of these, and observations necessarily produce vast amounts of data. For the…

Continue Reading

-

New gene therapy reverses symptoms of SYNGAP1-related disorders in mice

In an exciting scientific first, researchers at the Allen Institute successfully designed a new gene therapy that reversed symptoms related to SYNGAP1-related disorders (SRD) in mice. These are a class of brain disorders that can…

Continue Reading

-

India seals £350m missile purchase deal with UK – Dawn

- India seals £350m missile purchase deal with UK Dawn

- UK signs $468m deal to supply India with missiles Dawn

- Starmer hails India trade deal as ‘launchpad’ after meeting Modi BBC

- Modi, Starmer tout India-UK trade deal as new Indian investment…

Continue Reading

-

Southward Impact Excavated Magma Ocean at Moon’s Biggest Crater: Study

Roughly 4.3 billion years ago, when our Solar System was still in its infancy, a giant asteroid slammed into the far side of the Moon, blasting an enormous crater referred to as the South Pole-Aitken basin. This impact feature is the largest…

Continue Reading

-

Revenue Surge Amid Strategic Expansion

This article first appeared on GuruFocus.

-

Revenue: $64.2 million, up 84% from $34.8 million in the fiscal first quarter of 2025.

-

Tenant Fit-Out Revenue: $26.3 million from HPC hosting business.

-

Cost of Revenues: $55.6 million, up from $22.7 million.

-

SG&A Expenses: $29.2 million, increased due to $16.6 million in stock-based compensation and $3.9 million in personnel expenses.

-

Net Loss: $27.8 million or $0.11 per share.

-

Adjusted Net Loss: $7.6 million or $0.03 per share.

-

Adjusted EBITDA: $0.5 million, compared to $6.3 million in the prior year.

-

Cash and Cash Equivalents: $114.1 million.

-

Debt: $687.3 million.

Release Date: October 09, 2025

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

-

Applied Digital Corp (NASDAQ:APLD) expanded its long-term lease agreements with CoreWeave, increasing the total contract value to approximately $11 billion.

-

The company broke ground on a new campus, Polaris Forge 2, with initial construction funding secured and plans to scale to 1 gigawatt.

-

Applied Digital Corp (NASDAQ:APLD) secured an initial $112.5 million draw from a $5 billion preferred equity facility with Macquarie Asset Management, ensuring financing alignment for future projects.

-

The company reported a significant increase in revenues for the first fiscal quarter of 2026, up 84% from the previous year.

-

Applied Digital Corp (NASDAQ:APLD) has a robust multi-gigawatt pipeline and is actively evaluating new sites across additional states and regions to meet accelerating demand.

-

The company reported a net loss of $27.8 million for the first fiscal quarter of 2026.

-

Stock-based compensation expenses increased significantly, contributing to higher SG&A costs.

-

The cloud services business is under strategic review and classified as held for sale, indicating potential divestment.

-

Interest expenses increased compared to the previous year, impacting overall financial performance.

-

The company faces challenges in scaling development and construction to meet the high demand for AI infrastructure.

Q: What are the largest remaining factors for project financing, and should we expect financing for the first $150 million or all $400 million? A: Saidal Mohmand, CFO: We expect the project financing to entail both buildings due to their size and timing. This is one of the largest CoreWeave tenant financings in the market, and we aim for a facility in line with or more optimal than competitors.

Continue Reading

-

-

A New Concept to Support Brain Recovery in

LONDON, Oct. 10, 2025 (GLOBE NEWSWIRE) — Concern over the long-term effects of head injuries in rugby and American football has inspired a new approach to athlete care. Oralift Neuro, an emerging concept at the initiation stage, explores how…

Continue Reading

-

Week Ahead Economic Preview: Week of 13 October 2025

The following is an extract from S&P Global Market

Intelligence’s latest Week Ahead Economic Preview. For the full

report, please click on the ‘Download Full Report’ link.Download Full Report

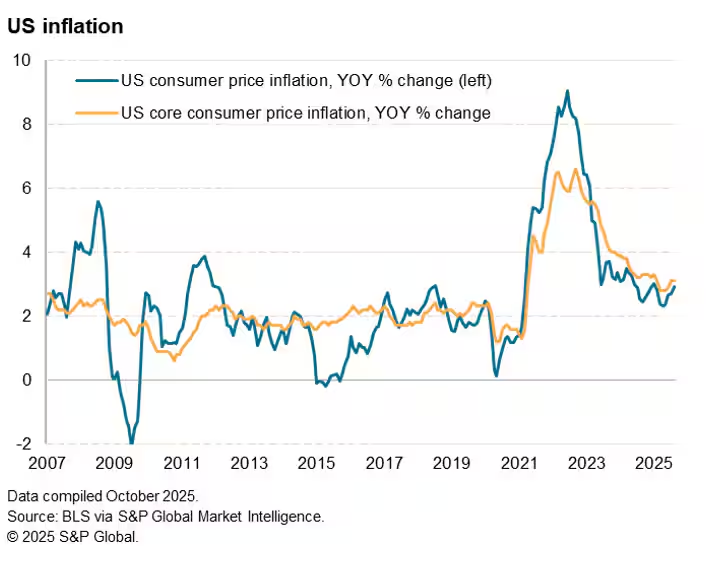

US shutdown prompts more data worries as policy clues are

soughtClues as to the path of US interest rates will hopefully be

provided from updated inflation numbers and economic activity data,

but a prolonged government shutdown would mean a lack of key US

data releases, engendering more uncertainty in the markets and

heightened growth worries. US tariff impact will, however, be

monitored via industrial production numbers for the US as well as

trade numbers out of mainland China and the eurozone. In the UK,

labour market and GDP come under scrutiny.At the time of writing, an ongoing federal government shutdown

is set to affect US data releases in the coming week, including

consumer and producer price inflation numbers, as well as retail

sales data. The markets are expecting consumer prices to have risen

0.3% after a 0.4% rise in August, but for core inflation to hold

steady at 0.3%. Producer prices are meanwhile anticipated to have

risen 0.3% after a surprise 0.1% drop in August. Weakening price

trends will add to the odds of a further FOMC rate cut, but the

case for lower rates will also likely hinge on the activity data.

Fed-compiled industrial production data could therefore prove the

US data highlight of the week, alongside New York and Philly Fed

surveys.Trade and inflation data are meanwhile issued for mainland

China, as are industrial production and trade data for the

eurozone. The data will be scoured for clues as to the impact of US

tariffs, though to also see whether domestic factors such as

increased fiscal spending may be offsetting some of the dampening

impact of the levies.GDP data for August and the latest official labour market data

will be digested by UK economy watchers keen to gauge fiscal

implications ahead of November’s Budget. Prior data showed the

economy flatlining in July and ongoing steep job losses, the latter

largely blamed on last year’s Budget.

Recent PMI survey data have also disappointed, likewise

signalling a stagnating economy and falling employment. More weak

data could tip the scales further toward rate cuts by the Bank of

England. The Bank held rates steady at 4.0% at its last meeting,

but two of the nine policymakers voted to cut rates due to growth

concerns.S&P Global will also be publishing the Investment Manager

Index (IMI) survey, revealing how institutional US equity investor

sentiment trends have changed in October.

Last month’s survey showed heightened risk aversion amid

worries over valuations and the political environment.If released, US inflation numbers will be watched for signs

of tariff levies being passed through to end consumers. So far, the

inflation numbers have not risen as much as many analysts had

feared, but headline inflation was up to 2.9% in August with core

at 3.1%, and it remains early days in terms of the degree to which

the import levied might be expected to impact high street

prices.Key diary events

Monday 13 Oct

Americas

Canada Market Holiday

– Brazil Business Confidence (Oct)EMEA

– Germany Current Account (Aug)APAC

Japan, Thailand Market Holiday

– China (Mainland) Trade (Sep)

– India Inflation (Sep)Tuesday 14 Oct

S&P Global Investment Manager Index* (Oct)

Americas

– Canada Building Permits (Aug)EMEA

– UK BRC Retail Sales Monitor (Sep)

– Germany Inflation (Sep, final)

– UK Labour Market Report (Aug)

– France IEA Oil Market Report

– Eurozone ZEW Economic Sentiment (Oct)

– Germany ZEW Economic Sentiment (Oct)APAC

– Singapore GDP (Q3, adv)

– Australia NAB Business Confidence (Sep)

– Australia RBA Meeting Minutes (Oct)

– India WPI (Sep)

– China (Mainland) New Yuan Loans, M2, Loan Growth (Sep)Wednesday 15 Oct

Americas

– Brazil Retail Sales (Aug)

– Canada Manufacturing Sales (Aug, final)

– US Inflation (Sep)

– US NY Empire State Manufacturing Index (Oct)EMEA

– Germany Wholesale Prices (Sep)

– France Inflation (Sep, final)

– Spain Inflation (Sep, final)

– Eurozone Industrial Production (Aug)APAC

– China (Mainland) Inflation (Sep)

– Japan Industrial Production (Aug, final)

– India Unemployment (Sep)

– India Trade (Sep)Thursday 16 Oct

Americas

– Canada Housing Starts (Sep)

– US PPI (Sep)

– US Retail Sales (Sep)

– US Initial Jobless Claims

– US Philadelphia Fed Manufacturing Index (Oct)

– US Business Inventories (Aug)

– US NAHB Housing Market Index (Oct)EMEA

– UK monthly GDP, incl. Manufacturing, Services and Construction

Output (Aug)

– Italy Inflation (Sep, final)

– Eurozone Balance of Trade (Aug)

– Italy Balance of Trade (Aug)APAC

– Japan Machinery Orders (Aug)

– Australia Employment Change (Sep)Friday 17 Oct

Americas

– US Building Permits (Sep, prelim)

– US Housing Starts (Sep)

– US Industrial Production (Sep)

– US Capacity Utilization (Sep)EMEA

– Eurozone Inflation (Sep, final)APAC

– South Korea Export and Import Prices (Sep)

– South Korea Unemployment Rate (Sep)

– Singapore Non-Oil Domestic Exports (Sep)

– Malaysia Balance of Trade (Sep)

– Malaysia GDP (Q3, prelim)* Access press releases of indices produced by S&P Global

and relevant sponsors

here.Download Full Report

© 2025, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers’ Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Learn more about PMI data

Request a demo

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Continue Reading