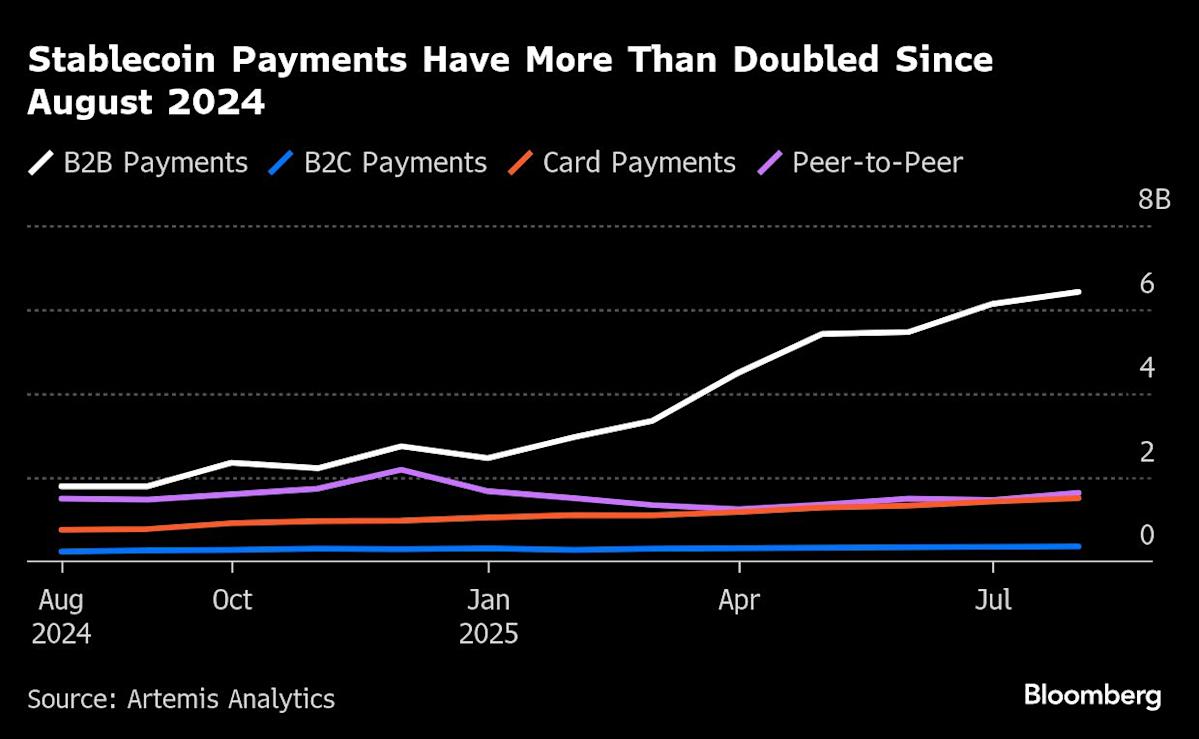

(Bloomberg) — Consumers and businesses are using stablecoins – digital tokens pegged to the dollar – to make real-world purchases and payments at an accelerating pace since the July passage of the first US legislation to regulate that niche of the cryptocurrency sector.

Over $10 billion was moved through stablecoins in August for goods, services, and transfers, up from $6 billion in February and more than double the volume from August 2024, according to a report from Artemis, a blockchain data provider. At this pace, stablecoin payments could reach $122 billion over a full year, Artemis researchers said.

Most Read from Bloomberg

This growth follows President Donald Trump’s signing of the Genius Act into law on July 18, which established federal regulations for stablecoin issuers and requires them to back their tokens with highly liquid assets such as Treasury bills.

While stablecoin payments are growing rapidly, they remain tiny compared to traditional systems. At a $122 billion annual pace, stablecoin payments represent a small fraction of conventional payment volumes. Still, this gives stablecoin advocates optimism about the instrument’s growth prospects.

“If you look at stablecoin supply on a certain trend, and then right after Genius passed, the trend does inflect even more,” said Andrew Van Aken, data scientist at Artemis, noting the report’s illustration of an increase in the growth rate of stablecoin supply. “We certainly think it has had an incremental impact.”

Artemis

Business-to-business transfers make up the most of stablecoin payments at $6.4 billion monthly – nearly two-thirds of the total and up 113% since February, the report said. This marks the first time business payments have exceeded peer-to-peer consumer transactions, which held steady at $1.6 billion monthly, according to Artemis.

Companies are using stablecoins to bypass traditional international banking delays. Businesses are “fed up with this very cumbersome send deposit here to this bank, which then sends another bank, which sends another bank,” Van Aken said.

With an average business stablecoin payment of $250,000, Van Aken said larger purchases are where speed matters most. Companies can use stablecoin to avoid the delays of routing payments through multiple correspondent banks in the traditional system, he said.

Banks have taken notice. Zelle, the bank-owned service that facilitates consumer money movement, plans to expand its services internationally. Zelle will rely on stablecoins to enable cross-border money movement, according to a statement Friday from its parent company.

Van Aken added that the ability of stablecoin users to earn yield and facilitate faster transfers of capital gives it an added advantage, which, in turn, could mean that stablecoins could continue to see added adoption.

“As stable coins prove to be better money, that will only accelerate people’s trust in it and continue the growth,” Van Aken said.

The most gifted runners not only go faster and with a smoother gait. They also need less recovery time. The phase of the current bull market that pushed off the blocks six months ago is proving elite at refreshing itself with the briefest of respites before continuing forward to the next mile marker. The S & P 500 fell a maximum of 2.98% using intraday prices, nearly all of that in one day on Oct. 10, after President Donald Trump rhetorically re-escalated the U.S-China trade confrontation. The index then spent the next nine trading days inside that single-day range until it broke to a fresh high this past Friday, briefly surpassing 6,800, after an unthreatening CPI report removed one possible impediment to the two more Federal Reserve rate cuts expected by year’s end. The main reason the CPI report released the indexes higher is that it simply passed, making Big Tech earnings next week the next known swing factor and allowing the old favorites of the AI trade to reassert leadership. .SPX 3M mountain S & P 500, 3 months This column last week suggested that “an ideal scenario for the remainder of the year would have the recent choppiness last a bit longer to qualify as a proper scare, skimming the froth off the speculative stuff and resetting expectations in a way that rebuilds investors’ capacity to be surprised to the upside.” As of now, it appears no genuine scare was needed, unless we count the couple of days last week when gold, crowded momentum plays and unserious meme stocks were liquidated in a slightly sloppy but ultimately benign rotation. Evercore ISI equity strategist Julian Emanuel makes the case that the manic surge-and-swoon act in gold and connected high-velocity speculative stuff need not dictate the broader market path: “As was the case in early 2021 when the peak in meme stocks, SPACs and profitless tech created brief instability in markets generally, gold’s selloff has been accompanied by selloffs in other speculative themes from quantum computing to lithium to uranium. Yet as it was in 2021, where the S & P 500 rallied an additional 23% from the meme-stock fizzle to the capital markets fueled peak a year later, rumors of speculation’s demise in 2025 are greatly exaggerated.” This is well-observed, though the obliteration of the frothiest market themes from their early 2021 peak was far more damaging than anything seen so far this month. Tireless retail buying And anything resembling the demise of the speculative fervor is hard to locate. Citadel Securities equity trading-flow guru Scott Rubner on Friday extolled the persistent aggression in somewhat valuation-insensitive small-investor activity, noting that 22% of trading volume now comes from retail accounts – the most since (yup) February 2021 – and retail has been a net buyer of stocks 23 of the past 27 weeks. And, truly, what would deter such excitable, tireless buying among non-professionals when AI hype is being invoked by so many adjacent industries and marginal companies, when Robinhood is blurring the line between investing and gambling with sports-prediction contracts in their app, when whole subsectors (rare minerals, quantum computing) get pumped to the stratosphere on the mere hint of the Trump administration possibly taking a stake, in a dynamic I call “too rigged to fail?” Yet for all the fun and games, the genuine fundament of corporate value – real profits – are coming through nicely to substantiate generally elevated valuations. Companies so far are beating forecasts at around an 80% rate, better than the norm. Stocks aren’t universally being rewarded for it, but it moves the chains on forward earnings-growth forecasts. Of course, total S & P 500 earnings for 2025 are now looking as if they’ll come in below where consensus pegged them at the start of the year. On Dec. 31, the full-year estimate was $274, which fell to $264 by July and is now up to $268. That’s a 2% decline over a ten-month stretch in which the S & P 500 index is up 15.5%. So, yes, the market is more expensive now, but there’s always next year. Consensus for 2026 is tracking above $304, which is now becoming the denominator for all investor valuation assumptions and return projections. This is what bull markets do, they roll forward their optimism until forced to rethink it. Was the little wobble in popular momentum stocks enough to soften up expectations to receive good news on tech results with enthusiasm? John Flood, Head of Americas Equities Sales Trading at Goldman Sachs, says yes, in a trading-desk note: “This week’s painful drawdown in momentum…has only added to the already significant wall of worry out there. As a result, the sentiment/positioning setup into the heart of mega-cap tech earnings is the friendliest I have seen in quite some time. If no foot faults from MAGMA (Microsoft, Amazon, Google, Meta, Apple) next week (we are not expecting any) I am bracing for another leg higher at the index level led by super-cap tech.” Year-end upside again? Just a few reasons it’s tough for bears to find a meal in a year like this, especially as we get deeper into the fall. Everyone knows most years have an upward bias in the final two months of the year, even more so when the first ten months have been strong. Granted it’s hard to make a specific case for why this year will fall into the 20% of instances when year-end seasonality failed, yet it’s worth noting that the seasonal signals have been glitchy this year. We were supposed to be up handily into April, but the S & P had a 15% year-to-date drawdown by April 8. The chart below, from Renaissance Macro Research, plots the forward-three-month S & P 500 return for each date, based on decades of market history. Last week we hit what’s supposed to be the best entry point for three-month-forward gains. But note that almost exactly three months ago was meant to be the worst moment to buy (in late July) and since then the index is up 6%. Two weeks ago, the president’s social-media growling about higher China tariffs exposed a node of complacency among investors, who as a group had turned their focus away from the trade-policy flux. Rationally so, in a sense, given the incentives all around to be sure that things settle into a manageable arrangement. Alongside a few corporate-credit hiccups and overbought speculative sectors, the risk-off reaction briefly overwhelmed the market’s usual capacity to absorb shocks through rotation. If forced to identify another node of complacency it might be investors’ comfort level with the underlying sturdiness of the economy. The conventional wisdom sees meager job growth as largely a result of immigration restrictions and demographics, disconnected from still-healthy GDP-tracking models that capture urgent capex levels and free spending by the affluent. It’s a plausible and defensible stance. And it’s true that overall (unofficial) consumption data and corporate commentary are not raising any alarms. Still, the market is no longer sending as emphatic a message about the pace of growth as it was several weeks ago, even. Equal-weighted consumer discretionary stocks are no longer outperforming. Industrials are better but have stalled on a relative basis. Veteran strategist Jim Paulsen of Paulsen Perspectives says, “A good proxy for U.S. economic surprises may be the relative performance of S & P cyclical sectors. Cyclicals have continued underperforming badly since Oct 1!” Warren Pies, founder of 3Fourteen Research, points out, “During this October wobble, homebuilders and other key cyclical areas of the market have lagged. Simultaneously, the AI trade has powered higher. Against the backdrop of falling yields, these intra-market moves point to nascent growth concerns.” Accumulated anecdotes could include an uptick in corporate layoff news, weak S & P PMI manufacturing sentiment, mortgage-application volumes not responding much to lower rates. There’s a good chance the market is cushioned against a growth scare by AI, by the Fed’s dovish turn and by the projected stimulative effects of the new tax law fattening tax refunds early next year. And maybe no news can remain good news for now in the absence of government data, and then perhaps the Street will give the data a Mulligan once it comes given the shutdown distortions. This low-volatility ascent since April quite resembles the imperturbable rally through all of 2017. That run required a steep acceleration higher into January 2018 accompanied by euphoric investor expectations for policy-driven growth, reaching serious excesses well beyond present conditions before breaking hard into a flash correction. None of this is enough to withhold the benefit of the doubt from the bulls for now, of course. But such issues can serve as a study guide for when the tape goes in search of an excuse to administer its next test.

Each study participant voluntarily provided informed consent. The criteria for inclusion were as follows: (i) 18 to 80 years of age with positive diagnosis of PTC using paraffin-embedded biopsy samples; (ii) no prior thyroidectomy; (iii)…

A recent large-scale study has revealed new insights into the structural changes of the retina in multiple sclerosis (MS) patients, highlighting potential biomarkers for disease monitoring and severity assessment. Researchers analyzed optical…

Customers visit a Roborock store at a shopping mall in Seoul, South Korea, Oct. 12, 2025. (Xinhua/Yao Qilin)

BEIJING, Oct. 25 (Xinhua) — At a large shopping mall in Seoul, South Korea, a Chinese brand’s robot vacuum cleaner attracted bustling crowds. A Roborock robot vacuum cleaner, equipped with a robotic arm, precisely picked up a sock, rotated, and threw it into a box, drawing cheers from the audience.

According to data from a U.S. research firm, Roborock holds over 50 percent market share in South Korea’s robot vacuum cleaner market, firmly securing the top position, with a dominance market share exceeding 70 percent in the high-end market.

People watch the demonstration of a robot vacuum cleaner at a shopping mall in Seoul, South Korea, Oct. 12, 2025.(Xinhua/Yao Qilin)A costumer uses a robot vacuum cleaner at his home in Seoul, South Korea, Oct. 13, 2025. (Xinhua/Yao Qilin)People walk by a billboard of Roborock at a subway station in Seoul, South Korea, Oct. 13, 2025. (Xinhua/Yao Qilin)Customers visit a Roborock store at a shopping mall in Seoul, South Korea, Oct. 12, 2025. (Xinhua/Yao Qilin)A costumer uses a robot vacuum cleaner at his home in Seoul, South Korea, Oct. 13, 2025. (Xinhua/Yao Qilin)

Beyond South Korea, Roborock is rapidly expanding across other Asia-Pacific markets. In Japan, during a promotion on Amazon Japan, several Roborock products ranked among the most popular robot vacuum cleaners. In Australia, its products also made it into the top ten best-selling robot vacuum cleaner list.

This photo taken on Oct. 16, 2025 shows an advertisement of Roborock at a home appliance store in Tokyo, Japan. (Xinhua/Jia Haocheng)This photo taken on Oct. 16, 2025 shows advertisements of Roborock at a home appliance store in Tokyo, Japan. (Xinhua/Jia Haocheng)This photo taken on Oct. 19, 2025 shows billboards of Roborock at Sydney Airport in Sydney, Australia.(Roborock/Handout via Xinhua)A shop assistant introduces Chinese brand robot vacuum cleaners to a customer at a home appliance store in downtown Sydney, Australia, Oct. 13, 2025. (Xinhua/Ma Ping)

Over 2,000 kilometers away from South Korea, in Huizhou City of south China’s Guangdong Province, Roborock’s smart manufacturing facility operates at high efficiency, with robot vacuum cleaners continuously distributed worldwide.

From workshops in China to living rooms across Asia-Pacific, Chinese brands for robot vacuum cleaners have gained popularity among foreign customers.

A staff member searches for information at a warehouse of Roborock in Huizhou, south China’s Guangdong Province, Oct. 10, 2025. (Xinhua/Deng Hua)A staff member transports robot vacuum cleaner products in Huizhou, south China’s Guangdong Province, Oct. 10, 2025. (Xinhua/Deng Hua)A staff member works at a workshop of Roborock in Huizhou, south China’s Guangdong Province, Oct. 10, 2025.(Xinhua/Deng Hua)Staff members work on a robot vacuum cleaner assembly line at a workshop of Roborock in Huizhou, south China’s Guangdong Province, Oct. 10, 2025. (Xinhua/Deng Hua)An aerial drone photo taken on Oct. 10, 2025 shows logistics trucks waiting for loading and delivery at a Roborock facility in Huizhou, south China’s Guangdong Province.(Xinhua/Deng Hua)■

Say hello to ionocaloric cooling. It’s a new way to lower temperatures with the potential to replace existing methods of chilling things with a process that is safer and better for the planet.

Typical refrigeration systems transport heat away…

Intuitive Machines (LUNR) has drawn fresh attention as investors weigh the impact of new US export curbs on tech to China. At the same time, the company is advancing its IM-3 lunar mission and securing NASA contracts.

See our latest analysis for Intuitive Machines.

Intuitive Machines stock has whipped through a period of volatility, recently clawing back gains with a 28% share price return over the past month despite ongoing US-China export tensions and scrutiny following past missions. Although year-to-date share price return remains in negative territory, the strong one-year total shareholder return of 60% suggests that long-term momentum is still firmly alive for patient investors.

If space tech’s recent rally has sparked your curiosity, you can see what’s happening across the entire sector with our aerospace and defense discovery screener using the following link: See the full list for free.

Given its recent contract wins, strong analyst sentiment, and a price still about 20 percent below consensus targets, are investors overlooking an undervalued space innovator? Or is future growth already built into the current share price?

With Intuitive Machines closing at $12.81 and the most widely followed narrative placing fair value at $15.43, this perspective sets a higher bar than the current market price. This hints at room for re-rating if assumptions hold.

Strategic vertical integration of satellite and lander manufacturing, along with proprietary advancements from the KinetX acquisition, enhances cost efficiencies, IP control, and technological differentiation. These factors support higher net margins and competitive pricing power as the company scales recurrent service contracts across civil, defense, and commercial markets.

Read the complete narrative.

Want to see what assumptions drive this bullish view? The narrative’s fair value hinges on powerful expansion bets, bold profit transformation, and sky-high valuation multiples rarely seen outside tech’s heavyweights. Curious which projections could justify such optimism? Discover the numbers on the next page.

Result: Fair Value of $15.43 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, persistent losses and heavy reliance on large government contracts could quickly dampen the bullish outlook if execution or funding falls short.

Find out about the key risks to this Intuitive Machines narrative.

While Intuitive Machines looks attractive when compared to its fair value estimate, a look at its price-to-sales ratio tells a different story. The company is trading at 6.7 times its sales, which is much higher than the US Aerospace & Defense industry average of 3.2 and the peer average of 2.7. The market’s fair ratio, based on regression analysis, stands at just 1.4 times sales. This large gap suggests considerable valuation risk if the company fails to maintain its growth edge. Which view should investors trust?

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGM:LUNR PS Ratio as at Oct 2025

If you think there’s another angle to the Intuitive Machines story or want to dig into the numbers yourself, you can shape your own take on the company in just a few minutes. Do it your way.

A great starting point for your Intuitive Machines research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Seize your chance to get ahead by uncovering opportunities that others might miss. Simply Wall Street’s screeners give you unique insights to sharpen your investment strategy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LUNR.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Eni (BIT:ENI) reported earnings growth of 4% per year and revenue growth of 3.8% per year, both trailing the broader Italian market’s expectations of 9.7% earnings and 5% revenue growth. The company’s net profit margin shrank to 2.6% from 4.1% a year earlier. With profitability improving over the last five years and high-quality earnings, investors are weighing the premium Price-To-Earnings Ratio of 21.1x (above industry and peer averages) against a market price that still sits below the discounted cash flow fair value.

See our full analysis for Eni.

Next, we will see how these headline figures stack up against the prevailing narratives that investors follow—and where the data might surprise.

See what the community is saying about Eni

BIT:ENI Earnings & Revenue History as at Oct 2025

Analysts forecast that Eni’s profit margin will rise from 2.6% today to 5.8% in three years, even as revenue is projected to decrease by 0.7% per year over the same period.

According to the analysts’ consensus view, margin expansion is supported by:

Growth in higher-margin businesses like biorefining and sustainable mobility, with new biorefinery projects and partnerships fueling expanded revenue streams and better return on equity.

Strategic LNG expansion and diversification, specifically new projects in Africa and Asia, add resilience to earnings and help offset declining revenue in legacy operations.

Strong margin outlook could underpin future shareholder returns. See how the consensus narrative interprets this shift in direction. 📊 Read the full Eni Consensus Narrative.

Persistent losses in Eni’s Versalis (chemicals and downstream) division, with management noting a “lack of meaningful economic recovery” in this European sector, continue to drag on group earnings and introduce ongoing margin pressure.

Analysts’ consensus view notes two main risk areas:

Legacy businesses like Versalis generate negative free cash flow, and expected only “slight improvement” in margin outlook, raising concerns about lasting drag on net profits.

Eni’s upstream expansion in regions such as Africa and Argentina boosts production potential but increases exposure to regulatory and expropriation risks, which could disrupt future revenue streams or lead to asset losses.

Eni trades at a Price-To-Earnings Ratio of 21.1x, far above the industry and peer averages (14.5x and 14.7x). Yet its share price of €15.84 remains below both consensus analyst target (€15.75) and DCF fair value (€19.76).

Analysts’ consensus view underlines:

The small 2.9% difference between the current share price and the €15.75 consensus target suggests limited immediate upside. This implies the stock is close to being fairly priced in the eyes of most analysts.

Holding a valuation premium may weigh on sentiment if Eni’s forecasted growth continues to lag the broader Italian market. However, the DCF fair value offers longer-term support for investors who see further profitability gains.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Eni on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Have a unique take on these results? Bring your perspective to life and shape your story in just a few minutes with us. Do it your way

A great starting point for your Eni research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Eni faces challenges as its forecast revenue shrinks and growth lags the Italian market. Persistent losses in key divisions also strain future prospects.

If you want steady earnings and reliable growth, use our stable growth stocks screener (2099 results) to find companies that consistently expand revenue and profits through all market cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ENI.MI.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Hexatronic Group (OM:HTRO) posted a forecasted earnings growth rate of 17.8% per year, outpacing the Swedish market, with expected revenue growth of 4.2% annually. Both figures signal momentum ahead of local peers. Over the past five years, the company has averaged an 18.3% annual earnings increase, though the latest net profit margin of 4.7% is down from last year’s 6.8%, showing some margin pressure has crept in. Even so, with Hexatronic trading at a 13.3x P/E ratio, well below its peer and industry averages and under the SEK33.3 estimated fair value, investors may see the setup as one of strength checked by caution on margins.

See our full analysis for Hexatronic Group.

Now it’s time to pit these headline numbers against the most widely held narratives. Some will match expectations, while others may surprise.

See what the community is saying about Hexatronic Group

OM:HTRO Earnings & Revenue History as at Oct 2025

Hexatronic’s decision to manufacture fiber optic cable in the US directly targets tariff increases and high freight costs, two line items that have notably squeezed margins and profitability in recent quarters.

Bears argue that these external pressures, especially rising freight expenses and persistent tariff impacts, create sustained risks for revenue margins.

The net profit margin sits at 4.7%, down sharply from the prior year’s 6.8%, highlighting that cost inflation has already eaten into profitability.

This contraction directly challenges the company’s ambition to improve regional margins through local production and operational tweaks.

Hexatronic’s Data Center business line reported record 41% sales growth and 37% EBITA growth, outpacing all other operating segments and positioning the business to capitalize on rising cloud demand.

Consensus narrative notes that these robust results, combined with efficiency gains in the Harsh Environment segment, are expected to drive profit margin improvement from 4.7% now to 5.6% in three years.

The uplift is anchored by analysts forecasting total earnings of SEK 459.8 million by 2028, compared to SEK 358.0 million today, signalling belief in the durability of cloud-driven growth.

What is surprising is that while most of Europe remains flat, success in Data Centers and targeted US investments have offset some of the headwinds from lagging regions.

Consensus sees growth in Data Center sales as the lever that could move earnings beyond expectations. 📊 Read the full Hexatronic Group Consensus Narrative.

With a current P/E of 13.3x compared to 36.2x for peers and 23.4x for the broader European electrical industry, Hexatronic trades at a clear discount, while its SEK 22.67 share price sits below both the analyst target (SEK 25.17) and DCF fair value (SEK 33.30).

Consensus narrative contends that this valuation gap could close if profit margins rebound and forecasts play out, but the market remains cautious amid margin compression and cash flow volatility.

Analysts’ consensus assumes minimal change in share count, projecting that future upside is driven by improved profitability, not financial engineering.

The 12.4% gap between current share price and analyst target provides a visible benchmark for upside, yet only if the company delivers on growth and cash flow improvement.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Hexatronic Group on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Got a different take on these results? Share your perspective and shape your own narrative in just a few minutes by using Do it your way.

A great starting point for your Hexatronic Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Hexatronic’s compressed profit margins and uneven cash flow reveal the challenge of sustaining growth when operational costs and external headwinds increase.

Prefer more consistent financial performance? Use stable growth stocks screener (2099 results) to discover companies with reliable revenue and earnings growth, proven to hold steady when markets take a turn.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include HTRO.ST.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Voyager Technologies (VOYG) shares climbed 4% today. The solid move comes following recent earnings numbers, which revealed double-digit annual revenue growth and improving net income. This has sparked fresh discussion about the company’s underlying valuation.

See our latest analysis for Voyager Technologies.

Voyager Technologies has seen some sharp swings this year. Today’s 3.67% 1-day share price return adds to a recent rebound. Despite upbeat earnings news and double-digit growth, momentum is still recovering after a rough 90-day stretch. The share price is down more than 21% over that period and nearly 41% year-to-date. Long-term investors will be watching to see if renewed optimism signals a turning point for the stock.

If today’s jump has you looking for your next opportunity, it might be the perfect moment to discover fast growing stocks with high insider ownership.

With impressive earnings and a steep stock discount compared to analyst price targets, the big question now is whether Voyager Technologies is truly undervalued or if the market already reflects the company’s future growth prospects.

Voyager Technologies commands a hefty price-to-sales ratio of 12.5x, putting it well above both industry and peer averages at its latest closing price of $33.35. This means investors are paying a substantial premium for every dollar of current revenue compared to other U.S. Aerospace & Defense companies.

The price-to-sales ratio compares a company’s market value to its revenue, providing perspective when profits are negative or not meaningful, as is the case for Voyager. In sectors like Aerospace & Defense, this multiple is often used to gauge the market’s expectations for future growth, especially for companies not yet generating profits.

However, such a high price-to-sales multiple may signal market optimism about Voyager Technologies’ rapid growth, but it could also reflect overexuberance. When compared to the industry average of 3.2x and a peer average of 3.1x, Voyager’s 12.5x stands out as especially expensive. At these levels, investors should recognize that a lot of future success is already baked into the share price.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Sales of 12.5x (OVERVALUED)

However, sustained net losses and an outsized price-to-sales ratio could pose challenges if growth slows or if expectations cool in the months ahead.

Find out about the key risks to this Voyager Technologies narrative.

Taking a different approach, our DCF model places Voyager Technologies’ fair value at just $16.24 per share, compared to its current price of $33.35. This suggests the stock may actually be overvalued and raises the question: is investor optimism outpacing what the business can realistically deliver?

Look into how the SWS DCF model arrives at its fair value.

VOYG Discounted Cash Flow as at Oct 2025

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Voyager Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

If you see things differently or want to dig deeper into the numbers, you can easily craft your own take on Voyager Technologies in just a few minutes. Do it your way.

A great starting point for your Voyager Technologies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Don’t let your search stop with Voyager Technologies. Exceptional companies are waiting to be found, and now is the time to look beyond the obvious winners. Use Simply Wall Street’s powerful screener to make smart investing moves that set you ahead of the curve.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include VOYG.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com