What’s long-time Colorado Springs food journalist Matthew Schniper’s goal for his Side Dish with Schniper newsletter? “Gastro-diplomat.”

“I didn’t coin this term, but someone lent me this term,” he said.

Schniper said he likes the way that…

What’s long-time Colorado Springs food journalist Matthew Schniper’s goal for his Side Dish with Schniper newsletter? “Gastro-diplomat.”

“I didn’t coin this term, but someone lent me this term,” he said.

Schniper said he likes the way that…

Resolution-Ready: Subway’s New Year Lineup Delivers Protein Power and Bold Flavor at Unbeatable Value

Subway’s all-new Protein Pockets and Sub of the Day are packed with quality protein, hand-chopped veggies and bold sauces – each for less than $5

MIAMI, Jan. 7, 2026 /PRNewswire/ — Subway is kicking off the new year with fresh ways to save and fuel your day with big flavor, quality ingredients, and unbeatable value. Starting Jan. 8, sink into Subway’s all-new Protein Pockets, packed with more than 20g of protein, fresh veggies and fan-favorite sauces for just $3.99*. Hungry for more? Subway also unveiled a new six-inch Sub of the Day lineup for $4.99**. Whether you are trying to save, hit your protein goals or simply eat better in the new year, Subway is making it easier than ever – any time of day.

Introducing Protein Pockets: The Ultimate Grab-and-Go Solution

Protein Pockets feature a soft tortilla with a toasty wheat flavor that perfectly complements a curated selection of protein, hand-chopped vegetables and fan-favorite sauces. Each Protein Pocket piles on more than 20g of protein, making it a smart choice for protein-conscious guests and flavor seekers alike.

Protein Pockets debut with a lineup of four delicious options:

“Getting more protein in their diet is important to so many people. But all too often that protein is expensive or fried. With Subway’s new Protein Pockets, they can get over 20 grams of protein for $3.99* without sacrificing taste.” said Dave Skena, Chief Marketing Officer, North America. “And with our new Sub of the Day lineup, our featured 6” subs are only $4.99**. In 2026, folks can eat freshly made, delicious food at a great value every time they come to Subway.”

Sub of the Day: A Daily Deal on Subway Classics

Alongside Protein Pockets, Subway is upgrading its value menu with the all-new Sub of the Day. Guests can enjoy a different six-inch sub every day of the week for just $4.99**, or make it a meal with a drink, chips or cookies for $2 more. From Meatball Monday to Spicy Italian Sunday, start a new ritual with fresh flavor and everyday value, all week long.

The rotating lineup includes:

Value Built In: Sub Club Loyalty Rewards

Subway’s new Sub Club loyalty program launched in December and has already been a win for guests and franchisees alike. With Sub Club, every fourth footlong is free*** – delivering daily value, convenience and a seamless digital experience that keeps millions of guests coming back.

To learn more about Protein Pockets, Sub of the Day or join Sub Club to start earning rewards today, visit the Subway app or Subway.com.

*At participating U.S. restaurants. Prices higher in AK & HI. Check your app for pricing and participating stores. Add-ons addt’l. Addt’l fees apply on delivery orders. Plus tax. Cannot combine with other offers. Limited time.

**At participating U.S. restaurants. Prices higher in AK & HI. Check your app for pricing and participating stores. Meal includes a 6″ Sub of the Day, chips or 2 regular cookies, and a 20oz fountain drink. Add-ons and bottled beverages addt’l. Fountain drinks not available on delivery orders. Addt’l fees apply on delivery orders. Plus tax. 1 per order. Cannot combine with other offers. Limited time.

***Must be a Sub Club Member to qualify for this offer. Free Footlong will appear in account within 24 hours of qualifying purchase. Add-ons additional. Limitations apply. All fees apply on Subway® delivery orders. Sub Club available at participating restaurants and not on third-party delivery, catering, or purchases of gift cards. See subway.com for more details about Sub Club.

About Subway® Restaurants

As the global sandwich leader, Subway serves freshly made sandwiches at a great value to millions of guests around the world in nearly 37,000 restaurants every day. Subway restaurants are owned and operated by a network of thousands of dedicated Subway franchisees who are passionate about consistently delivering a high-quality, convenient guest experience and contributing positively to their local communities.

Subway® is a globally registered trademark of Subway IP LLC or one of its affiliates. © 2026 Subway.

![]()

SOURCE Subway Restaurants

The International Space Station is one of the most remarkable achievements of the modern age. It is the largest, most complex, most expensive, and most durable spacecraft ever built.

Its first modules were launched in 1998. The…

The bombshell announcement that the Trump administration no longer fully recommends a third of childhood vaccines means the US moved from leading globally on vaccination to lagging behind other high-income nations in preventing disease, experts…

When an ant pupa has a deadly, incurable infection, it sends out a signal that tells worker ants to unpack it from its…

It’s a challenge for the human brain to reckon with deep time. Visits to the Great Pyramids or Stonehenge can jog us out of present-tense bias and…

Every animal with a brain needs sleep — and even a few without a brain do, too. Humans sleep, birds sleep, whales sleep and even jellyfish sleep. Sleep is universal “even though it’s actually very risky,” said Paul-Antoine Libourel, a…

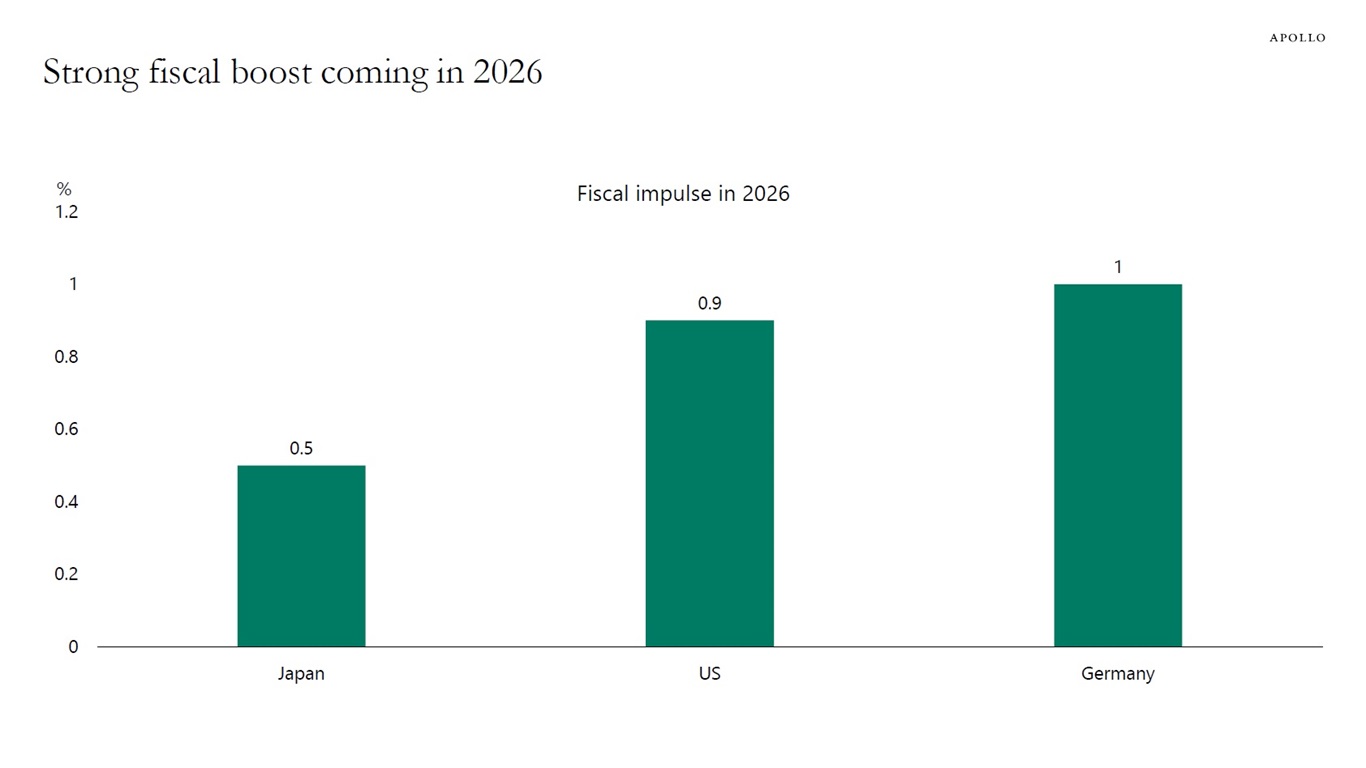

The IMF estimates that fiscal policy will boost growth by 1% in Germany and 0.5% in Japan in 2026. The CBO estimates that the One Big Beautiful Bill will boost US growth by…

Sea levels are rising faster than at any point in human history, and for every foot that waters rise, 100 million people lose their homes. At current projections, that means about 300 million people will be forced to move in the decades to come,…

Venezuela will reportedly continue supplying oil to the US beyond the initial 50m barrels announced by Donald Trump after the American military’s capture of Nicolás Maduro.

The US would remove some sanctions on Venezuela to allow sales of oil…