A car bomb has killed a senior Russian general in Moscow as officials report “slow progress” in ceasefire talks with the United States on how to end the war in Ukraine.

Top negotiators from both Russia and Ukraine were in Miami over the weekend…

A car bomb has killed a senior Russian general in Moscow as officials report “slow progress” in ceasefire talks with the United States on how to end the war in Ukraine.

Top negotiators from both Russia and Ukraine were in Miami over the weekend…

The Federal Insurance Deposit Corp. (FDIC) has issued a notice of proposed rulemaking to establish standards by which FDIC-supervised insured depository institutions may apply to establish a subsidiary to issue stablecoins. Because the U.S. banking agencies are likely to promulgate substantially similar processes, all regulated depository institutions should consider encouraging the FDIC and other agencies to hew closely to the statutory considerations for granting such authority.

Key Takeaways

Background

The GENIUS Act establishes a federal regulatory framework for the issuance of “payment stablecoins,” defined generally as digital assets designed to maintain a stable value for use in payment or settlement. The statute limits authority to issue stablecoins in the U.S. to permitted payment stablecoin issues (PPSIs) and assigns oversight responsibility to federal financial regulators, including the FDIC for subsidiaries of FDIC-supervised institutions for which the FDIC is the primary federal payment stablecoin regulator.

On December 16, 2025, the FDIC approved an NPRM that will implement statutory provisions under the GENIUS Act requiring the FDIC to establish an application process and framework for FDIC-supervised insured depository institutions (IDI) to obtain the approval required for the issuance of payment stablecoins through their subsidiaries.

Overview of the Proposed Rule

Eligible Applicants

The proposed rule applies to state-chartered, FDIC-supervised IDIs, including state-chartered banks that are not members of the Federal Reserve System and state-chartered saving associations, that seek to issue payment stablecoins through a subsidiary. An approved subsidiary that receives FDIC approval under the rule becomes a PPSI subject to supervision of the FDIC and may issue payment stablecoins.

Evaluation Standards

In seeking to support the responsible growth and use of digital assets, the FDIC will evaluate applications under safety and soundness criteria specified in the GENIUS Act, including considerations of financial condition, governance, risk management, and compliance capabilities. The proposed rule does not establish additional prudential standards, such as quantitative capital or liquidity requirements, which will be addressed in forthcoming rulemakings, although it would require a discussion of the proposed capital and liquidity structure of the PPSI subsidiary in any application.

Application Requirements

The proposed rule requires applicants to submit an application providing the information necessary for the FDIC to evaluate safety and soundness factors described in the GENIUS Act:

The FDIC’s objective is to evaluate applications against statutory safety and soundness factors while minimizing regulatory burden where possible. Accordingly, the FDIC has not proposed safety and soundness factors beyond those listed in the GENIUS Act but has requested comment on whether any such factors should be added. Because the statute and proposed rule permit the FDIC to reject an application only if the activities of the applicant would be unsafe or unsound under the listed factors, any expansion of the relevant factors would be very significant to applicants.

Review Process and Timelines

The proposed rule establishes defined review timelines:

Denial, Hearing, and Appeal Rights

If the FDIC proposes to deny an application, the applicant will have the right to request a hearing within 30 days of receiving notice. The proposed rule outlines procedures for such hearings and requires the FDIC to issue a final determination within 60 days after the hearing.

Safe Harbor Provisions

The proposed rule provides for a temporary safe harbor for applications submitted to the FDIC before the GENIUS Act becomes effective by allowing applicants to request a waiver of certain requirements of the GENIUS Act lasting up to 12 months. The FDIC may grant such waivers on a case-by-case basis.

Considerations and Next Steps

Institutions evaluating or planning stablecoin initiatives should consider the following.

Key open questions include how the FDIC will apply and evaluate safety and soundness standards in practice, how the framework under this proposed rule will interact with oversight by other federal financial regulators, whether consortiums of banks and other potential types of investors may have partial ownership of a PPSI that is organized as a subsidiary of an FDIC-supervised institution, and how future rulemakings under the GENIUS Act will shape the broader regulatory environment for stablecoin issuance.

Across the globe, most finance teams are just beginning their journey with AI. Most organizations in North America and Japan are still testing or experimenting with AI in specific areas. However, in France, a significant number are already expanding AI implementation across several finance functions, progressing more quickly and confidently than others.

Across all three regions, most finance teams are still in the early stages of AI adoption.

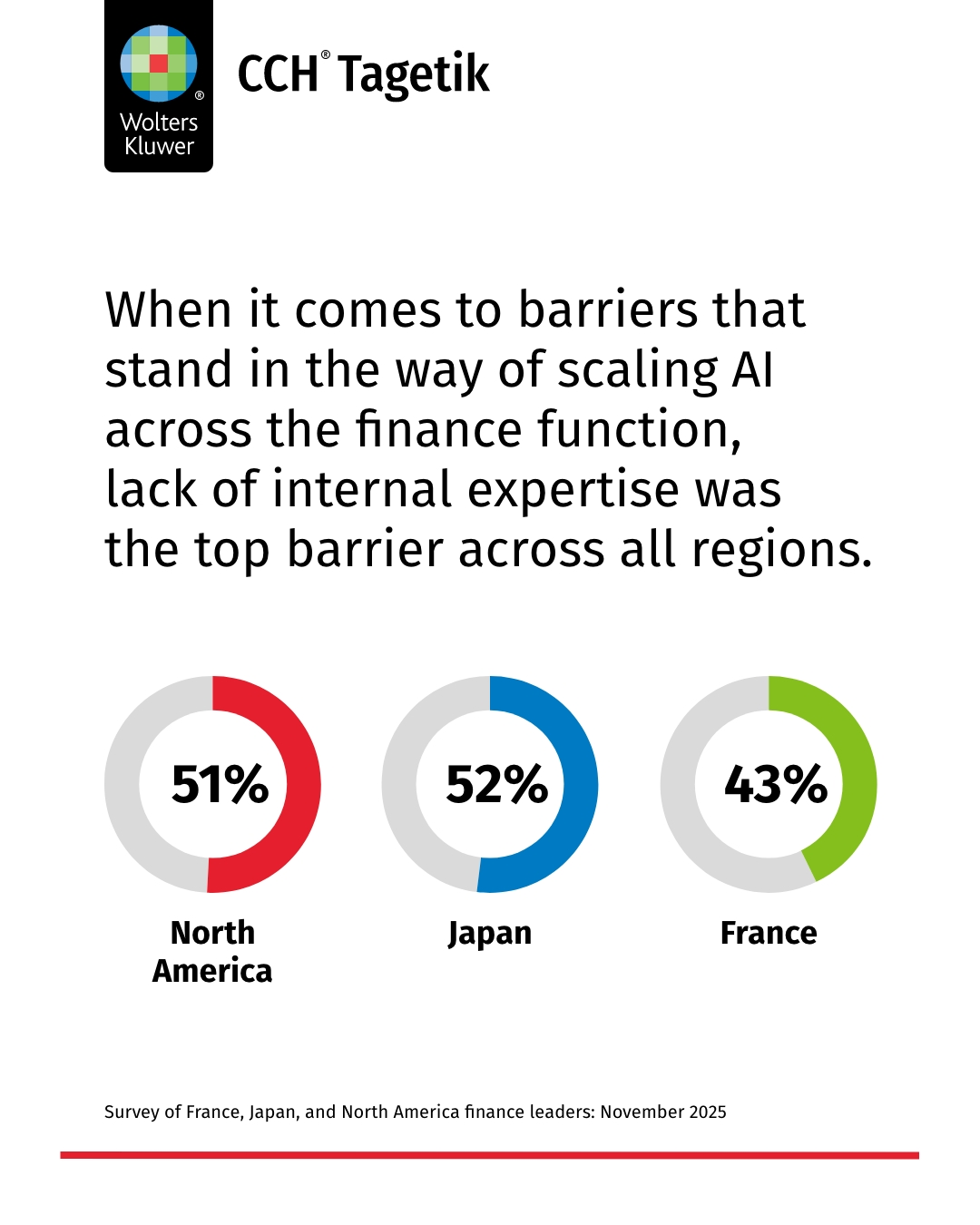

When it comes to barriers that stand in the way of scaling AI across the finance function, lack of internal expertise was the top barrier across all regions (North America 51%, Japan 52%, France 43%). However, the degree to which each region faces other obstacles to scaling AI varies considerably.

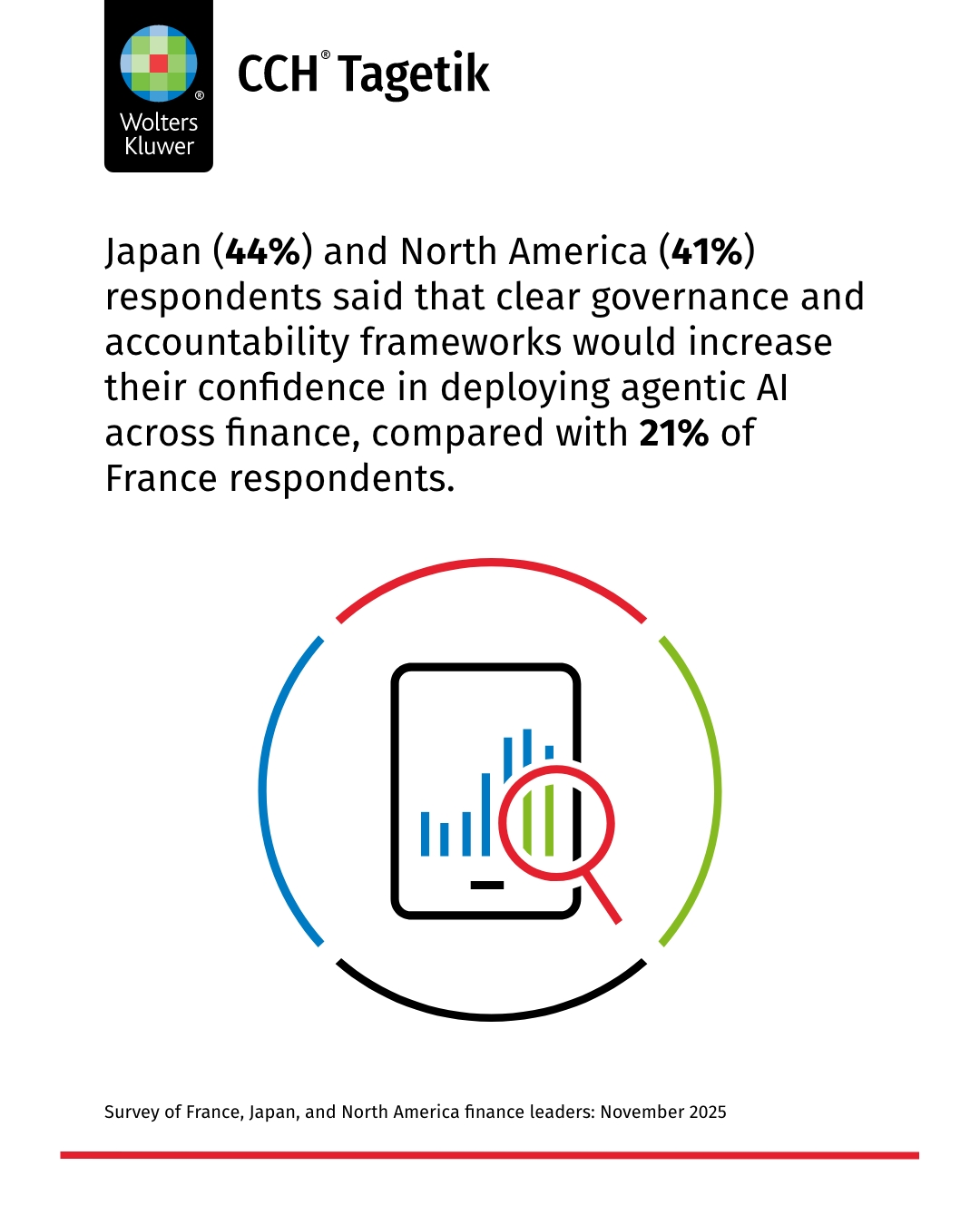

When asked what would give them the most confidence to deploy agentic AI more broadly:

North America respondents overwhelmingly said proven use cases (65%).

France respondents said that agentic AI integration with existing CPM tools (65%) would be their biggest confidence driver.

Japan (44%) and North America (41%) respondents said that clear governance and accountability frameworks would increase their confidence in deploying agentic AI across finance, with 36% of respondents in Japan also saying that stronger internal AI literacy would further boost their readiness to scale AI.

A shared vision, different journeys

As the polls from the inTouch25 events show, the story of AI in finance is not one of uniform progress, but of diverse experiences and evolving ambitions.

Finance leaders worldwide recognize AI’s transformative potential, but these findings underscore that the journey looks different across regions. At Wolters Kluwer, we are committed to working hand-in-hand with customers to overcome barriers, whether that’s integration challenges in France, ROI clarity in North America, or funding concerns in Japan.

No matter where you are on your AI journey, understanding regional differences can help you benchmark progress and anticipate challenges. With tools like CCH Tagetik Intelligent Platform, finance professionals are finding new ways to transform the Office of the CFO, with each region writing its own chapter in the global narrative of AI adoption.

Get ready for the Future Ready CFO report, the latest in a series of global survey reports from Wolters Kluwer. Future Ready reports feature informative content and actionable Business Insights that keep professionals updated on the latest trends, best practices, and regulatory changes, ensuring they are well-prepared for the future.

Launching by March 2026 Future Ready CFO will capture the voices of 1,300 CFO decision makers in North America, Europe, and Japan. It will reveal what’s next for finance leadership including technology adoption, operations and decision making. Experts will examine the seismic shift presented by AI and how these trends will redefine finance leadership.