AILSA CHANG, HOST:

There’s an iconic brewery in Pakistan that’s been operating for generations, even though it’s illegal for the country’s Muslim majority to drink. It’s called Murree Brewery. And this year, the brewery…

AILSA CHANG, HOST:

There’s an iconic brewery in Pakistan that’s been operating for generations, even though it’s illegal for the country’s Muslim majority to drink. It’s called Murree Brewery. And this year, the brewery…

A Pakistani brewery founded in the 19th century is exporting beer again for the first time in decades, despite alcohol being illegal for the country’s Muslim majority.

AILSA CHANG, HOST:

…

Distinct psychiatric disorders have more in common biologically than previously believed, according to the largest and most detailed analysis to date of how genes influence mental illness.

The study, led by University of Colorado Boulder and…

The U.S. agricultural export scenario has experienced a transformation in 2025, with diversification of export destinations emerging as an important factor for both the corn and soybean markets. Analysis of USDA export data through October 2025, shows distinct patterns of market evolution with implications for U.S. crop producers and the agricultural economy. While these two major commodities have followed different trajectories, with corn exports expanding and soybean exports contracting, both demonstrate the strategic value of diversified market portfolios rather than keeping a high dependence on a single market.

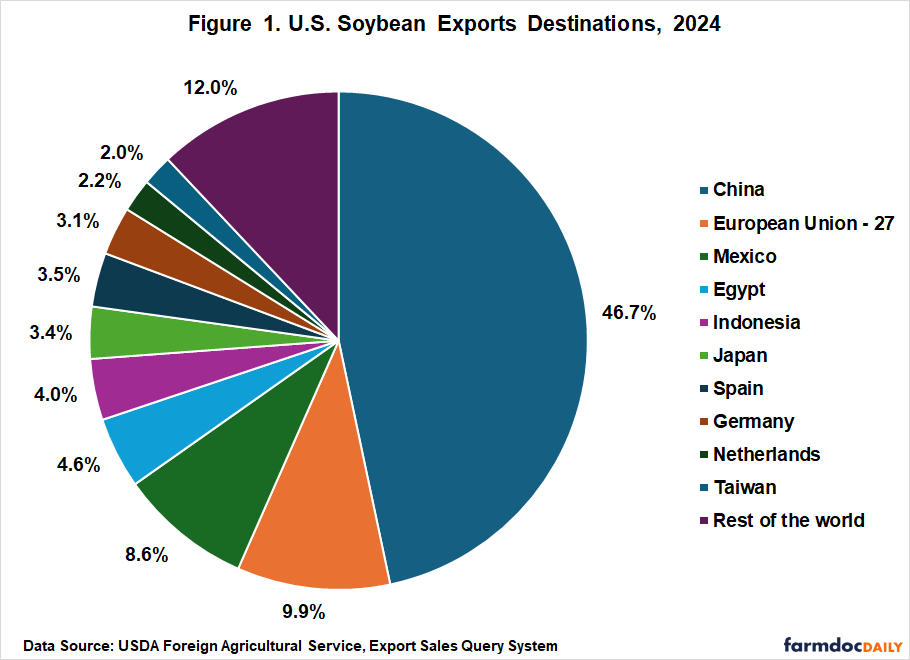

The biggest change in U.S. soybean exports between 2024 and 2025 has been the diversification of destination markets. While 2025 soybean export totals are tracking below 2024 levels, and given historical seasonal patterns, are unlikely to reach last year’s volumes even with November and December data, the diversification has helped moderate what could have been a far more severe reduction. In 2024, China accounted for 46.7% of U.S. soybean exports. The European Union held the second position at 9.9%, followed by Mexico at 8.6% (see Figure 1).

The 2025 export profile demonstrates a restructuring of U.S. soybean export markets. China’s share declined dramatically to 18.7%, a reduction of 28 percentage points, while the “Rest of the world” category surged to 21.6%, becoming the largest category (see Figure 2). The European Union increased its share to 12.9%, and Mexico expanded to 12.6%. Additional gains came from include Egypt (10.2%), Japan (5.4%), and Indonesia (5.0%).

This shift has proven important as overall U.S. export volumes have declined in 2025, with China reducing its import volumes substantially due to the second round of the trade war (see Colussi & Langemeier, 2025). This heavy reliance on China created vulnerability to market disruptions and policy changes in that single destination.

Total U.S. soybean exports are projected to total 44.50 million metric tons in 2025, representing 38% of total soybean production and a decrease of 13% compared to 2024 (WASDE-USDA, 2025). While some months in 2025 show lower volumes when compared to 2024, the magnitude of decline has been moderated by gains in alternative markets. October 2025 stands out as the month with the largest year-over-year difference, coinciding with the peak of the soybean harvest and zero purchases by Chinese buyers until then (see Figure 3).

If China reduced its purchases to the same absolute level observed in 2025, but the U.S. market structure remained as concentrated as in 2024, the overall decline would have been catastrophic. Instead, the expansion into Southeast Asia, North Africa, Europe, and Latin America absorbed a substantial portion of the displacement, transforming what could have been a market crisis into a manageable contraction.

The U.S. corn export market presents a contrasting but equally instructive story. Despite reductions in purchases from traditional top markets such as Mexico, Japan, and Colombia, overall export volumes in 2025 have already exceeded 2024 levels, even with data only through early November. This result demonstrates that diversification can not only cushion declines but also drive growth when market conditions are favorable.

In 2024, Mexico dominated U.S. corn exports with a 38% share, followed by Japan at 20% and Colombia at 12%. The European Union and South Korea accounted for 12% and 5%, respectively (see Figure 4). This distribution reflected relatively stable, long-standing trade relationships, mainly with Mexico under the United States-Mexico-Canada Agreement (USMCA).

The 2025 export pattern shows Mexico’s share declining to 29%, Japan’s to 18%, and Colombia’s to 9%. However, these reductions in market share, and in some cases absolute volumes, were more than offset by gains in other markets. The “Rest of the world” category increased from 12% to 15%, while the European Union expanded to 6% (see Figure 5).

Total U.S. corn exports are projected to reach 78 million metric tons in 2025, representing 18% of total corn production and an increase of 8% compared to 2024 (WASDE-USDA, 2025). Monthly export comparisons illustrate the growth trajectory. Without complete data for November and December 2025, corn exports have already surpassed 2024 levels in most months.

May 2025 showed particularly strong performance, with approximately 8.5 million metric tons exported, compared to 6 million in May 2024. October 2025 reached approximately 8 million metric tons versus 4.5 million in October 2024. These gains reflect strong demand across a more diversified export market, combined with a record U.S. corn crop exceeding 426 million metric tons (USDA-WASDE, 2025).

The contrasting trajectories of corn and soybean exports in 2025 reinforce the dual nature of market diversification as both a defensive and offensive strategy. For soybeans, diversification has functioned primarily as a buffer, mitigating the impact of reduced Chinese demand and preventing a potential market collapse. The insight is not that diversification prevented a decline in total volumes, but rather that it prevented a collapse that would have occurred had the market remained as concentrated as it was in 2024.

For corn, diversification has served as an engine of growth, enabling total volumes to expand despite weakness in traditional markets. The expansion across different markets suggests that U.S. corn has captured market share through competitive pricing and reliable supply. By establishing stronger commercial relationships with diverse markets, U.S. exporters have laid the groundwork for future growth that is less dependent on any single buyer.

In both cases, corn and soybean markets, diversification has improved outcomes relative to what would have occurred under concentrated market structures. For soybeans, this means a manageable decline rather than a crisis. For corn, this means robust growth rather than modest gains. However, building market presence in new destinations requires time, investment in relationships, adaptation to local preferences and standards, and often infrastructure development.

Wheat markets were already expecting a big global crop, but recent production updates have pushed supply even higher.

Australia’s production estimate has been lifted from around 33 million tonnes to roughly 35.6 million tonnes. Canada, helped by timely rain late in the season, is now on track for a record 40 million tonne harvest, and Argentina is forecasting a crop of 27.7 million tonnes, about 50 per cent larger than this time last year, and sending record volumes to ports.

“Farmers are delivering record amounts of wheat to the market, to local ports, and it is causing a weakening in prices,” Voznesenski said.

Argentinian wheat is landing on global markets at noticeably cheaper levels.

“If you look at the price on a ship, it is now noticeably lower than all the global prices, including here in Australia,” Voznesenski said.

Because Argentina and Australia harvest around the same time, their export offers often compete directly, especially in Asia.

“Argentina is willing to sell in Asia for a lower price. We don’t really have an option, we have to compete from a price perspective and that means our prices have to weaken as well,” he said.

There are positive signs in export data, with stronger buying from Asia and the Middle East.

“You look at Canadian, US, Russian and Ukrainian exports – they’ve all been quite strong, meaning someone’s buying this wheat,” Voznesenski said.

Even so, the sheer volume of grain this season is keeping prices from lifting.

“Yes. Demand is picking up. That’s a positive as always, but there’s just simply too much wheat around,” he said.

While today’s price story is mostly about abundant supply, Voznesenski is watching two key risks that could jolt the market next year.

1. Tension in the Black Sea

Shipping disruptions have resurfaced, with attacks on cargo vessels pushing up war-risk insurance premiums.

“If those tensions keep rising, that could cause prices to go higher,” he said.

2. Spring weather across the Northern Hemisphere

Crops across Europe, the US, Russia and Ukraine will emerge from snow cover in March and April.

“If it is very dry, when the crops come out of the ground into dry conditions, it could cause notably higher prices,” Voznesenski said.

He says an escalation in the conflict between Russia and Ukraine would also shift the market.

A single supply shock – geopolitical or weather-related – could flip the current trend of low prices.

For now, Australian wheat prices are responding to strong production at home and abroad, along with more competitive offers from Argentina. But Voznesenski says the story doesn’t end there.

“Overall, there’s a lot of supply but demand is picking up and all it takes is a supply side issue for markets to change direction,” he said.

Some major importers are also rethinking their approach to food security. Egypt, for example, plans to plant more wheat next year, a shift Voznesenski says is worth keeping an eye on.

“Large importers focusing a bit more on food self-sufficiency,” he said.

COLUMBIA, S.C. – South Carolina (7-3) heads to The Upstate for the annual SC Education Lottery Palmetto Series matchup with in-state rival Clemson (8-3) on Tuesday night. The Gamecocks will be playing their first and only true road matchup…

SAVE $30: As of Dec. 15, the Amazon Fire TV Stick 4K Select is back down to its $9.99 Black Friday price when you use the coupon code HOLFTV4K at checkout. That’s $30 or 75% off its…

Holding approximately 2,500 billion tons of sequestered carbon, soil is one of Earth’s largest carbon sinks — second only to the ocean. But even though soil is all around us, scientists are only just beginning to…