A doctor who pleaded guilty to illegally supplying ketamine to Matthew Perry in the weeks before the star’s death has been jailed for two-and-a-half years.

Salvador Plasencia, who operated an urgent-care clinic outside Los Angeles,…

A doctor who pleaded guilty to illegally supplying ketamine to Matthew Perry in the weeks before the star’s death has been jailed for two-and-a-half years.

Salvador Plasencia, who operated an urgent-care clinic outside Los Angeles,…

BEVERLY HILLS, CALIFORNIA – DECEMBER 03: Jennifer Lopez attends The Hollywood Reporter’s annual Women in Entertainment Gala at The Beverly Hills Hotel on December 03, 2025 in Beverly Hills, California. (Photo by Amy Sussman/Getty Images)

Getty…

Boeing Elects Bradley D. Tilden to Board of Directors

– Tilden, former chairman, president and CEO of Alaska Air Group, will join Safety and Finance committees

ARLINGTON, Va., Dec. 3, 2025 /PRNewswire/ — The Boeing Company (NYSE: BA) today announced that its Board of Directors has elected Bradley D. Tilden as its newest member, effective Dec. 3, 2025. Tilden will join the Aerospace Safety and Finance committees.

Tilden, 64, previously served as chairman, president and CEO of Alaska Air Group, Inc., the parent company of Alaska Airlines and Hawaiian Airlines, as well as regional airline Horizon Air.

“Brad brings a distinct customer perspective, proven leadership in the airline industry, and more than three decades of aviation experience,” said Boeing Board Chair Steve Mollenkopf. “His experience in safety management systems and financial expertise will be invaluable to our Board as we continue to make progress in the company’s recovery.”

In his 31-year tenure at Alaska Air Group, Tilden held several senior leadership roles, including CFO and then president of Alaska Airlines. Beginning in 2012, he began serving as President and CEO of Alaska Air Group, and was named executive chairman in 2021.

The 12th member of the board, Tilden will be the 10th new director added since 2019, as part of the board’s refreshment efforts. These directors collectively bring significant experience in aerospace, safety, engineering, manufacturing, cyber, artificial intelligence, software, risk oversight, audit, supply chain management, sustainability and finance, as well as the perspective of customers, suppliers and pilots.

A leading global aerospace company and top U.S. exporter, Boeing develops, manufactures and services commercial airplanes, defense products and space systems for customers in more than 150 countries. Our U.S. and global workforce and supplier base drive innovation, economic opportunity, sustainability and community impact. Boeing is committed to fostering a culture based on our core values of safety, quality and integrity.

Contact

Boeing Media Relations

media@boeing.com

SOURCE Boeing

Electric vehicles are not travelling as far as their manufacturers promise, with independent road tests showing all models analysed have failed to meet their advertised range.

One popular small car produced the worst EV result to date in the latest tests, pulling up more than 120km short of the distance printed on its sticker. At the other end of the scale, Tesla’s latest Model Y SUV was only a few kilometres short of its claim.

The Australian Automobile Association released the findings on Thursday with another four electric car road trials held as part of its $14m Real-World Testing Program.

Sign up: AU Breaking News email

The results add to a previous round of electric vehicle examinations, in which all five models failed to meet their promised range, and after tests of 131 internal combustion and hybrid vehicles found that 76% consumed more fuel than advertised.

The association tests vehicles on a 93km track in and around Geelong, Victoria, on urban and rural roads, as well as motorways.

US car maker Tesla emerged with the best result from all electric car tests to date. Its Model Y SUV fell 16km short of its claimed range of 466km on a single charge.

By contrast, the MG4 electric hatchback produced the worst result so far, missing its 405km goal by 124km – a shortfall of 31%.

The Kia EV3 missed its mark by 11% or 67km, and the Smart #1 electric car stopped short by 13% or 53km.

Comparing the real-world range of electric cars to their laboratory results would be vital for motorists, association managing director Michael Bradley said, as it would help them reach decisions and set expectations.

“These results give consumers an independent indication of real-world battery range, which means they now know which cars perform as advertised and which do not,” he said.

after newsletter promotion

“Giving consumers improved information about real-world driving range means buyers can worry less about running out of charge and make the switch to EVs with confidence.”

The association’s vehicle-testing program, funded by the federal government and launched in 2023, has tested 140 vehicles out of a target of 200, and has found most consume more energy or fuel than promised.

The Australian testing program was introduced following a 2015 Volkswagen scandal in which the European automaker was discovered using software to alter vehicle emissions during laboratory tests.

This article is an on-site version of our FirstFT newsletter. Subscribers can sign up to our Asia, Europe/Africa or Americas edition to get the newsletter delivered every weekday morning. Explore all of our newsletters here

Good morning and…

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

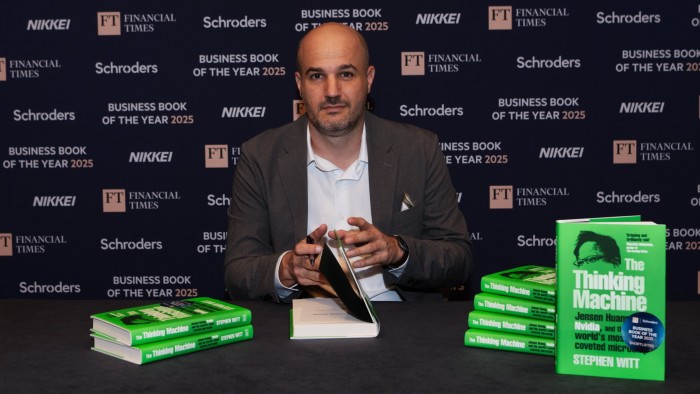

Stephen Witt’s The Thinking Machine, about the rise of Nvidia and its hard-driving leader Jensen Huang, has won the 2025 Financial Times and Schroders Business Book of the Year Award.

It is the second year in succession that the £30,000 award has gone to a book about the rapid spread of generative artificial intelligence. Last year’s winner, Supremacy by Parmy Olson, examined the rivalry between OpenAI and DeepMind.

Richard Oldfield, chief executive of asset management group Schroders, presented Witt with the prize at a dinner in London on Wednesday, mentioning how the judges praised The Thinking Machine’s “unique insights” into the success of Huang and Nvidia. In October, the chipmaker became the first company to surpass a market value of $5tn.

Roula Khalaf, FT editor and chair of judges, called the book “a fascinating account of the making of one of the most consequential companies of our times”.

Television producer and investigative journalist Witt was shortlisted for the FT award in 2015 for his book How Music Got Free, the story of how piracy and peer-to-peer sharing disrupted the recorded music industry.

The judges also praised the five other shortlisted titles, each of which is awarded £10,000, for the way in which they summed up critical issues facing business and the world, including US-China rivalry and the quest for growth and prosperity.

The award, which is also supported by FT owner Nikkei, is now in its 21st year. Previous winners include Amy Edmondson in 2023 for Right Kind of Wrong, about how to learn from failure and take better risks, and Chris Miller’s Chip War in 2022, about the global battle for semiconductor supremacy.

The other 2025 finalists were: House of Huawei by Eva Dou, which investigates the rise of the Chinese technology company and its founder; Chokepoints by Edward Fishman, about the use of economic sanctions; How Progress Ends by Carl Benedikt Frey, on what decides the destiny of civilisations; Abundance by Ezra Klein and Derek Thompson, about the growth dilemma facing the US; and Breakneck by Dan Wang, contrasting the US and its arch-rival China.

The other judges of this year’s award were Mimi Alemayehou, founder and managing partner, Semai Ventures; Daisuke Arakawa, senior managing director for global business, Nikkei; Mitchell Baker, founder, former CEO and executive chair, Mozilla; entrepreneur, angel investor and board leader Sherry Coutu; Mohamed El-Erian, professor of practice at the Wharton School, University of Pennsylvania, chief economic adviser, Allianz, and chair, Gramercy Funds Management; James Kondo, chair, International House of Japan; Adam Osborn, head of research, Asia ex Japan equities, Schroders; Randall Kroszner, economics professor at University of Chicago’s Booth School of Business; Nicolai Tangen, CEO, Norges Bank Investment Management; and Shriti Vadera, chair of Prudential and the Royal Shakespeare Company.

For more on this year’s award and previous winners, visit www.ft.com/bookaward

Maxton Hall – The World Between Us Season 2 came to a close after the 2025 Thanksgiving holiday, and one more season is on the way.

The show received a Season 3 renewal six months ahead of the premiere of Season 2. The German series set…

Eating disorders are associated with a 26% increased risk of school-age asthma and a 25% higher risk of preschool wheeze, researchers reported Tuesday in the journal Thorax. Adobe Stock/HealthDay

Women with an eating disorder are more likely to…

(Web Desk) – Australian bowler Mitchell Starc has surpassed Pakistani legend Wasim Akram’s long-held record for the most Test wickets by a left-arm fast bowler.

Akram took 414 wickets in 104 Test matches, a…