Stay informed with free updates

Simply sign up to the Artificial intelligence myFT Digest — delivered directly to your inbox.

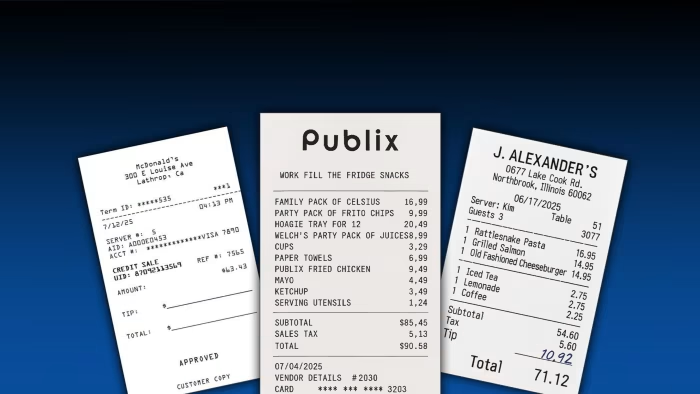

Businesses are increasingly being deceived by employees using artificial intelligence for an age-old scam: faking expense receipts.

The launch of new image-generation models by top AI groups such as OpenAI and Google in recent months has sparked an influx of AI-generated receipts submitted internally within companies, according to leading expense software platforms.

Software provider AppZen said fake AI receipts accounted for about 14 per cent of fraudulent documents submitted in September, compared with none last year. Fintech group Ramp said its new software flagged more than $1mn in fraudulent invoices within 90 days.

About 30 per cent of US and UK financial professionals surveyed by expense management platform Medius reported they had seen a rise in falsified receipts following the launch of OpenAI’s GPT-4o last year.

“These receipts have become so good, we tell our customers, ‘do not trust your eyes’,” said Chris Juneau, senior vice-president and head of product marketing for SAP Concur, one of the world’s leading expense platforms, which processes more than 80mn compliance checks monthly using AI.

Several platforms attributed a significant jump in the number of AI-generated receipts after OpenAI launched GPT-4o’s improved image generation model in March.

OpenAI told the Financial Times that it takes action when its policies are violated and its images contained metadata that signalled they were created by ChatGPT.

Creating fraudulent documents previously required skills in photo editing or paying for such services through online vendors. The advent of free and accessible image generation software has made it easy for employees to quickly falsify receipts in seconds by writing simple text instructions to chatbots.

Several receipts shown to the FT by expense management platforms demonstrated the realistic nature of the images, which included wrinkles in paper, detailed itemisation that matched real-life menus, and signatures.

“This isn’t a future threat; it’s already happening. While currently only a small percentage of non-compliant receipts are AI-generated, this is only going to grow,” said Sebastien Marchon, chief executive of Rydoo, an expense management platform.

The rise in these more realistic copies has led companies to turn to AI to help detect fake receipts, as most are too convincing to be found by human reviewers.

The software works by scanning receipts to check the metadata of the image to discover whether an AI platform created it. However, this can be easily removed by users taking a photo or a screenshot of the picture.

To combat this, it also considers other contextual information by examining details such as repetition in server names and times and broader information about the employee’s trip.

“The tech can look at everything with high details of focus and attention that humans, after a period of time, things fall through the cracks, they are human,” added Calvin Lee, senior director of product management at Ramp.

Research by SAP in July found that nearly 70 per cent of chief financial officers believed their employees were using AI to attempt to falsify travel expenses or receipts, with about 10 per cent adding they are certain it has happened in their company.

Mason Wilder, research director at the Association of Certified Fraud Examiners, said AI-generated fraudulent receipts were a “significant issue for organisations”.

He added: “There is zero barrier for entry for people to do this. You don’t need any kind of technological skills or aptitude like you maybe would have needed five years ago using Photoshop.”