The audio version of this article is generated by AI-based technology. Mispronunciations can occur. We are working with our partners to continually review and improve the results.

The Newfoundland and Labrador government is warning of multiple scams circulating leading up to the holidays.

Since Dec. 4, the province has put out two public advisories warning the public of scammers trying to obtain personal information.

The first scam involves a text message appearing to be from MyGovNL and instructs the recipient to click a link to a fake website where they will be prompted to provide personal information.

Mike Goosney, the minister responsible for the Office of the Chief Information Officer, said the government would never ask someone for information by clicking on a link.

“It can grab the information from your personal data [and] oftentimes it’ll link into your financial accounts or to get passwords,” he told CBC Radio’s Newfoundland Morning.

“And then it’s basically an open book for hackers to be able [to] do the harm, which is a lot of times financial.”

He says the text can appear legitimate and once scammers receive personal information, it can allow them to access financial accounts.

“It’s just so disheartening to think that someone could work all their life and with the click of a button, someone could take it away from them,” Goosney said.

The province says if someone receives a scam text message, they should forward it to 7726 to alert their cellular provider.

They should then delete the message, block the number and report it to local law enforcement and the Canadian Anti-Fraud Centre at 1-888-495-8501.

The second scam the province is warning of is a telephone call claiming to be on the behalf of Premier Tony Wakeham, asking for personal information in exchange for a senior’s bonus.

Mike Goosney, minister responsible for the Office of the Chief Information Officer, says the government is working to track text and phone call scams. (Darrell Roberts/CBC)

Goosney says the scammers are looking to prey on seniors’ vulnerability

“It is very much alarming if you don’t feel it’s something or if you do feel it’s something that’s too good to be true, to delete right away. And you know, let authorities know.”

If anyone receives such a phone call, the province is asking them to immediately hang up without providing any information, and then report it to the RNC or RCMP.

Reports to the RNC can be made online or by calling 709-729-8000, and reports to the RCMP can be made by contacting the local detachment or calling 1-800-709-7267.

Goosney says the government is working to track these scams, and that they are working on providing more education about scams to the public.

Download ourfree CBC News appto sign up for push alerts for CBC Newfoundland and Labrador. Sign up for ourdaily headlines newsletter here. Clickhere to visit our landing page.

Boxing Day sales have seen a muted start as shoppers continued to shun bricks-and-mortar stores in favour of online.

By 3pm, visits to UK high streets were down 1.5% on 2024, while shopping centres saw a 0.6% fall, according to data from MRI Software.

MRI’s footfall data showed retail parks saw 6.7% more people visiting compared with last year, but the rise has so far not been big enough to see an overall or significant bump in visitors.

Barclays expects shoppers to spend £3.6bn in the sales, down from the £4.6bn they forecast for the sales in 2024, with fewer people planning to bargain hunt than last year. The amount spent online is also predicted to fall.

Although people are still going out shopping, the figures indicate the Boxing Day sales are not the big event they once were.

The Barclays consumer spend report suggests those who plan to shop have upped their budgets by £17 compared with last year, but overall people are forecast to spend less this year than last year on Boxing Day sales.

Karen Johnson, head of retail at Barclays, said shoppers have been cost-conscious through the year and that behaviour is likely to extend into the Boxing Day sales.

‘Subdued atmosphere’

But one shopper from Glasgow said she preferred the more subdued Boxing Day atmosphere.

“Everybody’s taking it at their own pace, it’s a more enjoyable experience shopping on Boxing Day, I think,” she told the BBC.

Although the festive period is an opportunity for many retailers to make up for quiet periods of the year, several major brands closed their stores on Boxing Day, including Next, John Lewis, Poundland, Wickes and Iceland.

Another shopper in Glasgow said that he comes out every year only because it was his family’s tradition.

“It’s definitely a lot quieter than usual,” he noticed, “though Lush did have a big, massive queue this year.”

Diane Wehrle, chief executive of Rendle Intelligence and Insights, said 2025 had been a challenging year for many people.

“In the run up to Christmas, consumers have really pulled back on spending because they were very nervous, particularly pre-Budget in November,” she told the BBC.

Chancellor Rachel Reeves’ announced in her last budget up to £26bn in tax rises in 2029-30, which will bring the UK’s tax take to an all-time high of 38% of national income in 2030-31, according to the OBR.

It means a further squeeze on household budgets as inflation – the rate at which prices rise – remains stubbornly high, though it has fallen from peaks seen in recent years.

For employers, higher minimum wage costs and National Insurance contributions announced last year mean they’re footing higher costs in an economy with sluggish growth.

Separate festive spending data from Visa showed that in the run-up to Christmas, spending was only marginally up overall, with spending on electronics up 8.4% compared with the same period last year.

Official retail spending data from the Office for National Statistics for November also indicated many shoppers resisted the lure of Black Friday discounts and the start of Christmas sales campaigns.

But Ms Wehrle said the extension of pre-Christmas discounting and boom in online shopping meant Boxing Day sales “have really become less important” over the last few years.

Northern Canada has been gripped by an intense and prolonged cold spell, with temperatures hovering between -20C and -40C for weeks. On Tuesday, Braeburn in the Yukon recorded -55.7C, its coldest December temperature since 1975.

Meanwhile, Mayo and Dawson endured 16 consecutive nights below -40C, with Mayo plunging to -50.4C on Monday. Whitehorse also recorded 10 nights when temperatures dropped below -30C.

The deep freeze spread farther south over the festive period. On Christmas Day, overnight temperatures in Edmonton fell below -28C, while Boxing Day was expected to bring lows of at least -20C across many regions, including Edmonton, Montreal, Ottawa and Quebec.

The severe cold is forecast to persist into the new year. Officials have warned that the Yukon could face electricity outages in the coming days, as the territory’s power grid comes under strain from record-high energy demand.

The prolonged chill has been caused by the polar vortex remaining anchored over Canada for much of December, allowing bitter Arctic air to spill south. Next week, the cold air mass is expected to retreat north gradually, enabling milder Pacific air to move across the US and into parts of southern Canada.

In stark contrast, parts of the US experienced their warmest Christmas Day on record as temperatures soared about 15-30C above the seasonal average. In many areas, conditions felt more typical of April or May than late December.

Several states set Christmas Day temperature records. In Oklahoma, Oklahoma City hit 25C on Tuesday, surpassing the previous peak of 22C set in 1982. Cities including Austin and Dallas, in Texas, and Charlotte, North Carolina, were also among those that recorded temperatures above 25C.

Above-average warmth is expected to continue through Boxing Day and the days ahead, with unseasonable heat forecast to sweep into the south-eastern states later in the week.

The warmth has been fuelled by a strong upper-level ridge extending from the desert south-west towards the north and east, creating a heat-dome effect. This pattern establishes a broad area of high pressure across much of the continent, trapping warm air near the surface. As air sinks through the atmosphere, it compresses and heats further, allowing unusually warm temperatures to build.

A stock market boom in artificial intelligence companies has added more than half a trillion dollars to the wealth of America’s tech barons in the past year, data shows.

The top 10 US founders and bosses of some of the world’s largest technology companies saw their finances swell to nearly $2.5tn, up from $1.9tn, in the year to Christmas Eve, according to figures from Bloomberg.

Elon Musk, already the world’s richest man, has again proved to be one of biggest winners as the AI gold-rush has pushed US stock markets to record highs.

Musk’s net worth increased by nearly 50% year-on-year to $645bn. The tycoon, whose business interests include xAI, an artificial intelligence company, became the first person to have a net-worth of more than $500bn in October this year. He could become the world’s first trillionaire if he hits targets set by Tesla, the electric car company he runs.

Musk sits ahead of Google co-founder Larry Page and Amazon founder Jeff Bezos in the overall rankings of the world’s wealthiest billionaires. Page is estimated to be worth $270bn, and Bezos $255bn.

The growing concentration of wealth among an ultra elite has fuelled debate about how best to rebalance economies, with some calling for more effective wealth taxes.

The chief executive of the chipmaker Nvidia, Jensen Huang, was also one of the biggest gainers. The value of his investments, equity and other assets rose $41.8bn, taking his personal fortune to $159bn. This puts him ninth in the overall Bloomberg Billionaire Index, and eighth among the top 10 US tech billionaires, according to a separate report from the Financial Times.

Huang sold nearly $1bn worth of shares this year, cashing in on Nvidia’s soaring stock price. Its relatively advanced computer chips are a critical component in building the more powerful processing capability required by AI. It became the world’s first $5tn company in October, larger than the economic output of some of the world’s biggest economies, such as Japan or India.

List of Silicon Valley’s wealthiest billionaires

The wealth of Page and Sergey Brin, the co-founders of Google, swelled by around $102bn and $92bn respectively, as investors bet on the company’s AI progress, including its own in-house efforts to build new chips, known as a Tensor Processing Unit.

Such has been the surge in AI investments in recent years that the Bank of England has warned of a “sudden correction” in global markets if investor confidence proves misplaced.

“On a number of measures, equity market valuations appear stretched, particularly for technology companies focused on artificial intelligence,” top policymakers at the central bank said in October.

This means that stock markets are “particularly exposed should expectations around the impact of AI become less optimistic”, they said.

While technology is the dominant industry among gainers in the billionaire rankings, there are other familiar names, too. Bernard Arnault, the French chair of the LVMH luxury goods company, which makes the likes of Louis Vuitton bags and Dom Perignon champagne, saw his wealth rise by $28.5bn over the past year. The 76-year-old controls around half of LVMH and analysts have turned more positive on the stock in recent months, with strong spending by wealthy North American consumers.

The Spaniard Amancio Ortega, who holds 59% of Inditex, the parent company of the high street clothing retailer Zara, and seven other brands, was among the biggest gainers, adding $34.3bn to his fortune, which sits at $136bn. This was boosted by a record dividend of €3.1bn from the retail group.

Quick Guide

Contact us about this story

Show

The best public interest journalism relies on first-hand accounts from people in the know.

If you have something to share on this subject, you can contact us confidentially using the following methods.

Secure Messaging in the Guardian app

The Guardian app has a tool to send tips about stories. Messages are end to end encrypted and concealed within the routine activity that every Guardian mobile app performs. This prevents an observer from knowing that you are communicating with us at all, let alone what is being said.

If you don’t already have the Guardian app, download it (iOS/Android) and go to the menu. Select ‘Secure Messaging’.

SecureDrop, instant messengers, email, telephone and post

If you can safely use the Tor network without being observed or monitored, you can send messages and documents to the Guardian via our SecureDrop platform.

Finally, our guide at theguardian.com/tips lists several ways to contact us securely, and discusses the pros and cons of each.

Irwin said many farmers in the Corn Belt have been surviving on a series of ad hoc payment programs from the federal government. Next year, producers are slated to receive billions in funding from disaster relief and economic aid programs – including a $12 billion bailout package announced earlier this month that aims to offset losses from low crop prices and the trade war.

Irwin said those payments could push farmers in Illinois toward a small profit instead of a hefty loss.

But, ad hoc payments only go so far, Cowley said.

“It’s not necessarily going to help the fundamentals of, you know, what do we do with the supply of the products that we grow?” Cowley said. “And what does that mean for prices that farmers are going to be paid on the market?”

New year, same trade questions

Economists say that trade uncertainty will continue to be a challenge as farmers make decisions for their operations this year.

Irwin is watching the U.S. relationship with China, the biggest buyer of U.S. soybeans, and the weather in South America through the first quarter of 2026.

Earlier this year, China boycotted U.S. soybean purchases for months to retaliate against the Trump administration’s tariffs. The country later agreed to buy 12 million metric tons of U.S. soybeans in 2025, and 25 million metric tons for the next three years – which is closer to what the country typically buys from the U.S.

But after the first Trump administration’s trade war, China further diversified where it sourced soybeans, namely from South America. Irwin said Brazil is now the dominant soybean producer in the world.

“I think what people are probably as worried about as anything on the trade front is, how much permanent damage has this done in our trade relationship with China?” Irwin said. “Is this just going to be a repeat of the last 2017, 2018, when we permanently gave up market share to South America, principally Brazil?”

While the Trump administration has announced trade agreements with countries like Japan, Irwin said some of the details are still unclear.

“Maybe there will be some nice boosts in our agricultural exports coming out of these trade agreements. But we have to see more specifics and get down to that before we’ll really know for sure,” he said.

This is happening as tariffs themselves are in question. Currently, the U.S. Supreme Court is considering their future in a lawsuit.

For Luis Ribera, economic professor at Texas A&M University, trade in 2026 is hard to predict because it’s heavily political. He said markets don’t know how to react to tariff unpredictability.

“In my world, that’s the big question – is this the new normal? Is tariffs going to be a tool to negotiate with other countries? And looks like that’s the way it’s going to be,” Ribera said.

As other countries retaliate against U.S. tariffs and find other places to source products, some American farmers are putting harvested crops in silos. Ribera said that means farmers have to pay for storage, and they don’t know when crops can be moved.

He said the current market leaves few options for crop growers.

“Producers, they don’t have an alternative or say, ’OK, you know, soybean prices are low, well, we’re going to produce more corn, or we’re going to go into cotton, or we’re going to go into a different type of rotation crops just to take advantage of prices,” Ribera said. “I mean, all across the board commodity prices are low.”

He says the regulars over the years have become lifelong friends − more like family.

Club Paihia spokesman and committed timeshare owner Bill O’Meara. Image / Supplied

Timeshare, or “holiday ownership”, is a concept where several people own rights to a holiday property, as opposed to the property itself.

The number of owners depended on the timeshare model, with the most common being 52 owners per unit, where each owner got one week of use a year.

The number of owners was then multiplied by the number of apartments available, so, for example, a 50-room resort could have up to 52 owners a unit, resulting in a total of 2600 owners.

O’Meara says the timeshare concept came from the US and arrived in New Zealand in the early 1980s.

Owners paid an up-front purchase price for a unit title that could be tens of thousands of dollars for a new one, or a couple of thousand for something older, plus annual levies to cover maintenance fees.

Purchasers were given a certificate of title. In New Zealand, owners had legal protection under the Unit Titles Act.

O’Meara says securing your week could come down to “drawing straws”, but booking systems were professionally run under a “classification” system, much like any hotel or resort.

Back when he bought their timeshare, it was a better option than an annual overseas holiday.

“There was no way that I could have a holiday at an international holiday destination for the same money.”

He wouldn’t say what he and his wife paid for their timeshare, only that they weren’t among those who forked out up to $30,000 in the early 1980s (about $107,000 today) for a timeshare off the plans.

True believer

O’Meara is a firm believer in the merits of the timeshare concept. He holds an active role in the industry association for the timeshares in New Zealand as a member of the New Zealand Holiday Ownership Council (formerly the New Zealand Timeshare Owners Association).

He is also on the body corporate of Club Paihia, which oversees the running of the resort.

For O’Meara and his family, the merits of owning a timeshare include the “enforced getaway” to a favoured spot, in New Zealand and even overseas.

He says there’s a global network of about 500 timeshare resorts offering an exchange system, helmed by companies offering a professional management service.

The sun might be setting on the concept of timeshare holiday accommodation, once popular among the now-boomer generation. Photo / 123rf

In New Zealand, many timeshares were managed by Australian firm Classic Holidays, which bought New Zealand‐based Monad Pacific Management Limited in 2023.

Monad managed 13 timeshare resorts across New Zealand, with about 13,000 member families under management.

The acquisition made Classic Holidays the largest timeshare management company in Australia and New Zealand.

O’Meara says owners can swap their week for another timeshare somewhere else in the world through one of the exchange companies.

“As a family, we’ve been to Hawaii every year. We would take two weeks on the Gold Coast and school holidays in the middle of winter.

“We’d get the cheapest airfare we could find to get into Coolangatta, hire a rental car from a fellow who gave us a really good deal and got to know us really well and off we go.”

O’Meara says it does, however, take a lot of planning.

“You’ve got to be on your game.”

He says little can beat a relaxing luncheon boat ride with friends to one of many bays out from Paihia, or a slow jetski ride to one of many inlets, or a kayak trip to Haruru Falls.

“We’d go up on the tide and when the tide turned, we’d come back again.”

Tide has turned

However, the tide that brought in the wave of investors in the 1980s now appears to have also turned.

In 2023, media reported there were fewer than 20 such resorts left in New Zealand.

The decision in 2025 to wind up the Bishop Selwyn timeshare resort in Paihia was one of five in as many years handled by one law firm alone.

In July, the High Court cancelled the unit plan that covered all unit titles at the Bishop Selwyn, and that freed up the entire complex to be sold.

The High Court has cancelled the unit plan that covered all unit titles at the Bishop Selwyn Resort in Paihia, and that freed up the entire complex to be sold. Image/Supplied

It followed an application to the court by the resort’s body corporate to allow its sale.

The decision wasn’t unanimous, but the majority of owners were in favour.

A survey in 2023 of the 263 unit owners showed 59.7% agreed to a wind-up of the scheme and sale of the property.

At a meeting the following year, 83% voted in favour of a motion to cancel the unit plan, although not all owners could be found.

Justice Jason McHerron said in his judgment that many owners had formed the view that the annual costs of keeping their timeshare weeks did not provide sufficient value, or they no longer had a need for their timeshare holiday accommodation.

Levies are typically in the $800-$1000 range and are paid to the body corporate to cover maintenance and any development.

Justice McHerron said about 17% of the survey respondents last stayed at the Bishop Selwyn two or three years ago and 24% at least four years ago.

He said unit owners looking to sell their interests had found there was no market for timeshare leases and where sales did happen, the vendor was unlikely to receive much, if anything.

He was satisfied it was an appropriate case for the court to exercise its discretion to make orders authorising the cancellation of the unit plan, which was approved to allow sale of the whole property.

It was envisaged a share of the proceeds would be allocated to each owner according to their respective interests in the unit plan.

Justice McHerron said a registered valuer would determine this on a percentage basis for each unit and would then be used to calculate the distribution of the sales proceeds after the costs of the sale have been paid.

The Bishop Selwyn Resort on almost 2500sq m of land in downtown Paihia had an insurance value of $20 million and was listed for sale in June 2025 for $5.6m.

Agent Ross Robertson, who recently retired, was handling it as his swansong, one-off project.

He told NZME in late October he had fielded a decent amount of interest so far, with 18-20 parties wanting to look at it.

Gone ‘out of fashion’

A partner in a Hawke’s Bay law firm, Jonathan Norman, who specialises in the timeshare field, says the dynamic of ownership is fascinating.

“For the people who do use the properties, they absolutely love them. They talk about how their family might have holidayed there for 40 years, that they had the most amazing times and want their children to have the same experience.”

Hawke’s Bay lawyer Jonathan Norman is a partner in law firm Sainsbury Logan & Williams and specialises in winding up timeshare units. Image/Supplied

Norman says there’s still a market for timeshares in some areas of the country, but the concept has largely gone out of fashion as the boomers who led the charge begin to fade out.

He says the biggest issue is most owners no longer use them, but are still paying their levies every year and getting very little back.

O’Meara says timeshares have also been at the mercy of increasing competition in the holiday accommodation sector, with the arrival of Airbnb and Bookabach.

Airlines had also become “more aggressive” through there simply being more of them, and the associated travel package deals that have flooded the market.

But many have simply done their time.

“Their life has changed. They bought in when they were 40 and they’re in their 70s now or coming up 80, and some of them are in their 90s.”

Betty is 86 and trying to sell a timeshare unit the family bought beside Lake Taupō in the early 1980s.

She’s one of several owners to have listed their timeshare at the Lakeside Villas Resort. She says it’s time to bid farewell to a place they loved and enjoyed and which her family isn’t keen to take on.

“I’m getting too old for it now. I don’t want to travel,” she says.

Betty and her late husband were drawn to the idea of timeshare ownership in the early 1980s by the promise of an annual holiday at a place they didn’t have to maintain.

It’s right on the lakefront, with walkways nearby and not far from town. Owners also have a swimming pool, spa pool, tennis court, mini golf, squash court, pool table and table tennis at the resort.

“We could just walk in and have a week in Taupō, which we quite enjoyed.”

Betty and her husband also took advantage of the international exchanges to timeshares around the world.

“We went overseas to England and Canada and Australia and I thought that was marvellous.”

Norman says the sale on a timeshare can often come down to a vendor paying the buyer’s legal costs.

“So, you know, it’s pretty grim for people. They’ve paid all the levies and that’s the best they can get out of it.”

Betty is offering the lease plus one fixed week and one floating week at the studio unit at Lakeside Villas Resort for a total of $600.

The annual $545 levy is paid, but will renew in 2026 when the body corporate sets the fees for the year.

“I shouldn’t imagine it’ll be much more,” Betty says.

When she spoke with NZME in October, she’d had interest from one person, but refused their $50 offer.

“I would virtually be giving it to them and they get a holiday this year.”

Norman says a lot of them are now on fixed incomes and worried about passing it down to their children because a timeshare lease does form part of your estate.

Thomas Attwood is among those to have inherited a timeshare at the Bishop Selwyn and the headaches he says came with it.

The Bishop Selwyn Resort in downtown Paihia had an insurance value of $20m and was listed for sale in June 2025 for $5.6m. There is a good market for these properties as either motels or other types of accommodation, lawyers and agents say.

“The timeshare was our dad’s and when he passed away it was sort of handed over to us.”

Attwood remembers his parents used it regularly “in the early days when all the timeshare was in vogue”.

They initially owned one in Taupō, but that was wound up, so they transferred ownership to one in Tūrangi, but that, too, was wound up.

Attwood says they owned a timeshare at Bishop Selwyn for about 15 years and used it yearly for a family holiday break.

But, it’s an added burden he doesn’t need.

“Dad was retired, so managing all this side stuff was no problem for him.”

That includes the expert organisation it takes to book an extra time at a timeshare outside the allocated week.

“He’d be on the website like a hawk. He was used to the mechanisms and the way the timeshare stuff worked, but for families inheriting it’s kind of, ‘Oh yeah we look on the thing [website] but it’s all been booked out’.

“I think you probably have to be like my dad and know how to work the timeshare system, so it does end up kind of being a burden,” Attwood says.

He compares timeshare ownership to what it’s probably like owning a villa or unit in a retirement home.

“You know you’re looked after and all that sort of stuff and you can live with other elderly people and go to the golf course or the bowling green, but you’re still paying maybe $150 a week [in levies] on something you might have paid thousands for up front.”

Different legal structures surround retirement home ownership, such as freehold, leasehold or a licence to occupy.

Entry costs are typical, which may include a deferred management fee and monthly fees for maintenance, insurance and communal services.

Norman says while there are challenges to selling a timeshare unit, where the market lies is in the bricks and mortar.

“There is a good market for these properties as either motels or other types of accommodation.

“They’ve generally been really well maintained and kept to a pretty good standard, albeit dated as products of the 80s and 90s.”

Tracy Neal is a Nelson-based Open Justice reporter at NZME. She was previously RNZ’s regional reporter in Nelson-Marlborough and has covered general news, including court and local government for the Nelson Mail.

Another coastal charity swim in Dorset was cancelled because of concerns about water conditions on Thursday.

The Weymouth and Portland Lions Club took the decision to end its Christmas Day Harbour Swim after the first of 10 scheduled swims.

“This was not an easy decision, but it was the right one in the interests of safety for all participants, water support teams, and spectators,” it said in a statement.

“We are grateful that both swimmers and spectators supported this decision.

“Despite the cancellation, many spectators continued to donate generously into the collection buckets, for which we are extremely thankful.”

The Federal Energy Regulatory Commission said a NorthWestern Energy subsidiary’s application to sell power from its soon-to-be-acquired Puget Sound Energy shares is “deficient” and called for more details about the deal.

The deal is controversial and contested.

However, a spokesperson for NorthWestern Energy said Wednesday the utility anticipates a green light from FERC.

“We are working with FERC to provide additional information and are confident our application will be approved,” said NorthWestern spokesperson Jo Dee Black in an email.

NorthWestern Energy announced in August 2024 it would acquire the Puget shares at the coal-fired electricity plant at Colstrip at no cost. Puget is based in Washington, where state law ends coal-fired electricity for state customers by the end of 2025.

NorthWestern said the new shares would provide a benefit to existing customers on Jan. 1, 2026, when the utility acquired them.

However, NorthWestern since created a subsidiary it said would receive all the Puget shares, and it told the Public Service Commission the shell company was outside the authority of regulators.

The Public Service Commission regulates monopoly utilities in Montana.

This fall, the NorthWestern subsidiary filed an application with the Federal Energy Regulatory Commission to sell power from the Puget shares on the wholesale market.

In a move it later reversed, the Public Service Commission demanded the feds investigate the monopoly utility for attempting to evade the law in shifting the shares to the new subsidiary; the PSC said it would proceed with its own inquiry instead.

An energy watchdog, the Montana Environmental Information Center, has protested NorthWestern’s federal application and filed to intervene in the case.

The energy nonprofit argues in part that the NorthWestern subsidiary should have secured federal authorization for the planned transfer — and its failure to do so is “fatal” to any approval request for a wholesale deal.

The MEIC also said NorthWestern has not shown that existing customers won’t be subsidizing the costs for the wholesale market deals.

In its own filing, the NorthWestern subsidiary argues the feds should reject the argument that the transfer of the Puget shares needs federal approval in part because the utility says the value of the shares doesn’t hit a financial threshold for approval — $10 million.

The MEIC disagrees; the nonprofit said just because the cost of the shares was $0 doesn’t mean the value of the asset is $0.

It said NorthWestern itself has estimated annual revenues of nearly $30 million from the asset and said it would cost $700 million to build an equivalent plant.

Wednesday, NorthWestern did not have an estimate of the value of the shares immediately available, but in a filing, it argues the nonprofit isn’t using an appropriate measure to value them.

The value is one request from the Federal Energy Regulatory Commission.

In the letter calling for additional information, FERC said the NorthWestern subsidiary must provide the original cost of the shares being transferred, undepreciated, in its filing.

The feds also called for details about the transfer within NorthWestern, including ownership arrangements, timing of arrangements, and rights or veto powers to any parties that are “disproportionate” to the deal.

“For example, do any of the owners hold special share classes with different rights that do not match their economic interest?” the letter said.

The letter called for specific information about the timing and structure of the transfer of shares from Puget to NorthWestern, and the timing of the transfer of the ownership interest between NorthWestern and the subsidiary, NorthWestern Colstrip 370Pu LLC.

The letter gives the NorthWestern subsidiary 30 days to provide the additional information.

In the meantime, NorthWestern spokesperson Black said the acquisition from Puget will be complete on Jan. 1, 2026. NorthWestern did not address what its plans are for the shares while the case is pending.

The NorthWestern subsidiary entered into a 21-month contract with Mercuria Energy America LLC and filed for FERC approval of the contract.

Note: This article was written by University of Illinois Agricultural and Consumer Economics M.S. student Yu-Chi Wang and edited by Joe Janzen. It is one of several excellent articles written by graduate students in Prof. Janzen’s ACE 527 class in advanced agricultural price analysis this fall.

Soybean oil and palm oil are the two most widely available vegetable oils in the world and are substitutes in many products, including as feedstocks in the production of biofuels. For many years, soybean oil and palm oil prices moved together, but since 2020, the close co-movement between soybean oil and palm oil prices has weakened. Prices now diverge more often and for longer periods. This change suggests that the types of supply and demand shocks hitting these markets has shifted. We suggest these shocks are becoming less global and more regional or national; aggregate vegetable oil supply and demand still matter, but these now interact with region-specific disruptions, particularly those related to biofuels policy, that affect one oil more than the other.

The goal of this article is to document how the price relationship between soybean oil and palm oil has changed and what this change means for future price dynamics. We first describe the global roles of soybean and palm oils and the different production systems behind them. We use monthly and daily prices to show how their historical co-movement has broken down since 2020. We then draw on several recent market episodes to explain soybean-palm price divergences and end with implications for U.S. soybean oil and future biofuel policy.

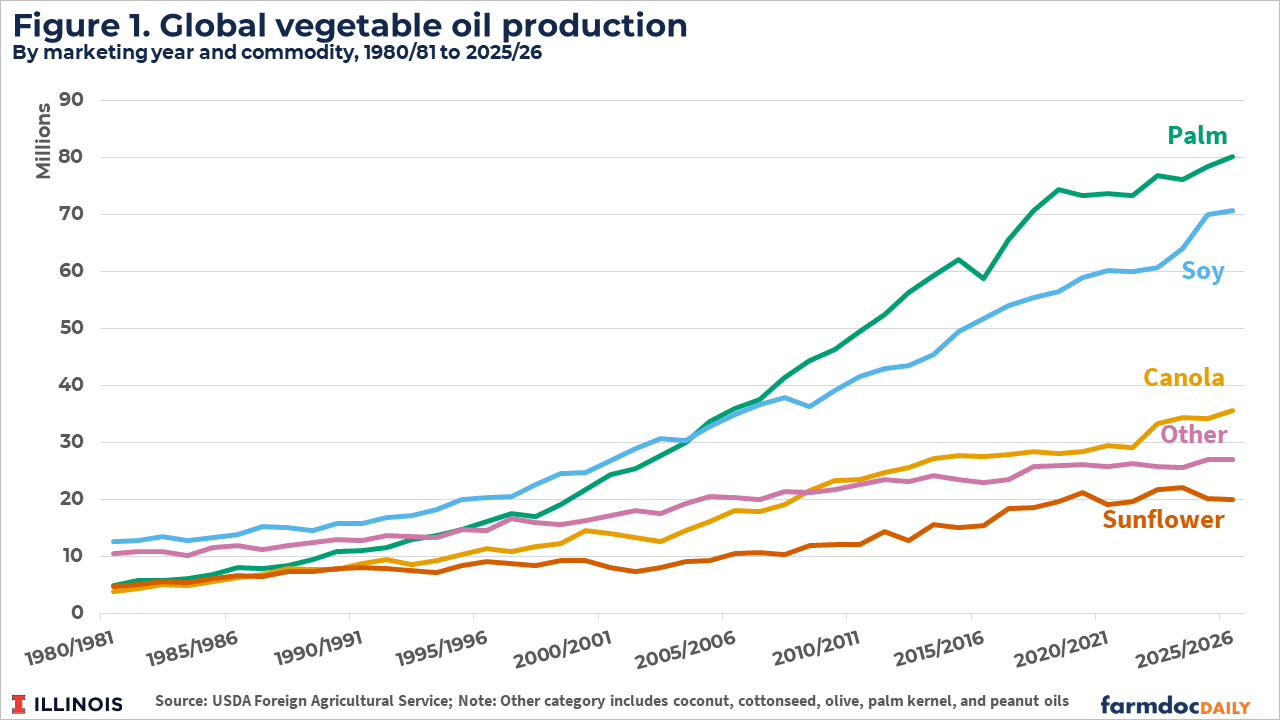

Overview of Global Vegetable Oil Production

Soybean oil and palm oil are the two leading vegetable oils in the world, a position they have held since the 1980s when palm oil surpassed production of canola and sunflower oils. Figure 1 plots changes in the production of leading vegetable oils over time. Soybean oil was long the world’s largest vegetable oil, but global production of palm oil began to exceed soybean oil beginning in the 2004/2005 marketing year. Together, they account for more than 60s% of global edible oil supply. Other vegetable oils such as canola, sunflower, and others play an important but mainly supporting role in meeting global demand.

The location of soybean and palm production and the process for extracting oil are important differences between the two commodities. Palm oil production is heavily concentrated in Indonesia and Malaysia, where output expanded rapidly in the 2000s. Palm oil refining, logistics, and trade are strongly geographically clustered. Soybean oil production is less concentrated than palm oil but focused in large agricultural exporting countries such as the United States, Brazil, and Argentina and major soybean importers, principally China. Major exporting nations typically have varying forms of biofuels mandates that incentivize domestic demand for soybean or palm oil as a feedstock and these mandates typically target domestically produced feedstock. Structural differences in location and policy may help explain why the two oil markets may not always respond in the same way to changes in demand.

Historical Price Relationships

To the extent that vegetable oils are substitutable and trade costs like transportation, tariffs, and others are low, soybean and palm prices should move closely together. To document this connection over a long time period, we analyze monthly benchmark prices tracked by the World Bank’s so-called ‘Pink Sheets’. These prices represent vegetable oils delivered to ports in Northwest Europe so they account for location differences. Figure 2 shows historic prices for both soybean and palm oil since 2000. While soybean oil has typically been valued at a slight premium to palm oil, prices have typically moved closely together over this period. Increases in prices correspond to increases in the other. Episodes like the 2008 price spike that affected many agricultural and energy prices are common to both series and the gap between prices has remained fairly stable over time. Despite substantial changes in price levels, the difference or ratio between soybean and palm oil prices was generally stable, at least until about the year 2020.

After 2020, soybean and palm oil prices begin to diverge more often and for longer periods. Before and after the 2022 price spike that coincides with another broad increase in agricultural and energy prices, prices for soybean oil surged well above palm oil prices. In other cases, soybean and palm oil prices appear to move in opposite directions. In late 2024, palm oil futures prices actually exceeded soybean prices for the first time since the 1990s. While some common dynamics remain part of price behavior after 2020, Figure 2 suggests more volatility in the underlying economic forces driving vegetable oil supply and demand. These patterns indicate that the close and predictable price relationship seen before 2020 has fundamentally changed.

To assess soybean and palm oil price dynamics since 2020 in greater detail, we look at daily futures price data. Daily data provide a more granular look at the timing of particular price movements. To make prices comparable across markets, soybean oil and palm oil prices must be adjusted, as they trade on different exchanges and are quoted in different units and currencies. Soybean oil prices are taken from Chicago Board of Trade (CBOT) front-month futures and are quoted in U.S. cents per pound. Crude palm oil prices are taken from Bursa Malaysia Derivatives (BMD) front-month futures and are quoted in Malaysian ringgit per metric ton. To place both series on a common basis, soybean oil prices are expressed per ton, while palm oil prices are converted from Malaysian ringgit to U.S. dollars using the daily MYR–USD exchange rate from the Federal Reserve Bank of St. Louis.

Figure 3 shows daily nearby soybean oil and palm oil futures prices from January 2020 to November 2025, both in levels and in terms of the price ratio of soybean to palm oil. Prices diverge beginning in early 2021. The price ratio returns to near parity during the early 2022 commodity price spike, but there is a second sharp divergence as prices for both commodities fell off of early 2022 highs. In mid 2023, prices diverge again with soybean oil prices jumping sharply. The price ratio reaches parity in mid-2024, after which palm oil prices exceed soybean oil prices for a time. Soybean oil prices have been slightly above palm oil prices for much of the past year. Overall, this period features more volatility in the price ratio and longer and sharper divergences in price than seen in past periods.

Why did the Soybean Oil-Palm Oil Price Relationship Break Down?

To understand price divergences shown in Figure 3, we consider narrative explanations coincidental to observed price movement. We highlight three episodes where soybean prices diverged from palm oil prices.

The first occurs over calendar year 2021. Both soybean oil and palm oil prices rise sharply during this period, reflecting tight global vegetable oil supplies. However, soybean oil prices increase more than palm oil prices; at the peak of this divergence indicated in Figure 3, the soybean oil price was 68% higher than the palm oil price. This coincides with a surge in US renewable diesel capacity and production (USDA-FAS, 2024), leading to a stronger increase in demand for soybean oil as a feedstock. Although programs such as the Renewable Fuel Standard and California’s Low Carbon Fuel Standard had been in place for years, renewable diesel production rapidly increased during this period which may have helped push soybean oil prices higher.

By late 2021, this divergence begins to narrow. Palm oil prices move higher as Malaysia experiences La Niña-related adverse weather and a shortage of migrant harvest workers following COVID-19 border restrictions (McKeany-Flavell, 2022). Malaysian palm oil production, exports, and year-end stocks fall to multi-year lows, which coincides with palm oil prices reaching record or near-record levels. As palm oil prices rise more quickly, the soybean-oil premium narrows, and by late 2021 the two prices move back together, ending the first divergence episode.

The second divergence begins after both prices reach record highs in early 2022. These peaks in Figure 3 occur during a period of very tight global supplies associated with the Russia-Ukraine war and Indonesia’s temporary ban on palm oil exports. Indonesia lifted the export ban in late May 2022 and exports resumed, leading palm oil prices to fall sharply. Soybean oil, as a close substitute, also moves lower but declines more gradually. As palm oil falls more quickly, the soy-to-palm price ratio increases, peaking with soybean oil prices 113% percent (i.e. more than double) palm oil in September 2022.

Toward the end of 2022, this divergence starts to narrow. In December 2022, EPA releases proposed biofuel mandates for 2023 to 2025 that are lower than the market had anticipated. This announcement may have reduced projected renewable diesel demand for soybean oil and is followed by a sharp decline in soybean oil prices (Sterk, 2022). As soybean oil prices fall more quickly and begin to move back toward palm oil’s earlier decline, the two price series return to a more stable relationship. This marks the end of the second divergence.

The third divergence begins in mid-2023, when markets appear to become more concerned about U.S. weather and the possibility of drought reducing soybean yields. As of mid-June 2023, about half of the U.S. soybean crop is classified in drought categories and crop condition ratings are declining across much of the Corn Belt (Purdue Center for Commercial Agriculture, 2023). At the same time, short-term weather forecasts point to a continuation of dry conditions, and soybean futures move sharply higher in a way that is consistent with this combination of poor current conditions and ongoing drought risk.

Beginning around September 2023, soybean oil prices in Figure 3 start to fall sharply and continue to decline into early 2024. Clean Fuels Alliance America (2024) reports that generation of biomass-based diesel Renewable Identification Numbers (RINs) in 2023 substantially exceeded the biomass-based diesel mandate and that RIN values declined sharply as this oversupply became apparent. RINs are tradable compliance credits that fuel suppliers use to show they have met U.S. renewable fuel blending requirements. Because soybean oil is an important feedstock for biomass-based diesel, this combination of abundant credits and lower RIN values is consistent with a reduced willingness to pay high prices for soybean oil in fuel uses and may have contributed to the downward pressure on soybean oil prices during this period. As soybean oil prices fall more than palm oil prices and the relative price in Figure 3 moves back to a more normal range in mid-2024 marking the end of the third divergence.

Discussion

We show the long-standing tight connection between soybean oil and palm oil prices has changed in recent years. Since 2020, leading vegetable oil price benchmarks have diverged more often and for longer periods. Co-movement has weakened and the two markets now follow separate paths more frequently than in the past. Evidence from recent market episodes suggests that this shift reflects a new mix of shocks. Broad global demand and cost shocks still move both markets, but they now interact with more frequent policy shocks and region-specific disruptions. In this environment, even close substitutes like soybean oil and palm oil can depart from their historical pattern of co-movement.

Our analysis suggests the US soybean industry may be more insulated from global vegetable oil shocks: palm oil may not play the same role it once did in shaping soybean oil prices. Palm oil production growth has slowed as Southeast Asia’s plantations hit land limits and a larger share of trees move into older age. Expansion has largely given way to replanting, so future output gains are likely to be small even if prices stay high (Bloomberg Intelligence, 2024). A larger share of palm oil production now stays in Southeast Asia to meet domestic biodiesel and food demand. This means palm oil has less effect on global vegetable oil prices than in the past, although major changes in palm oil supply and demand may still be transmitted to global vegetable oil markets. At the same time, the US soybean industry is now more exposed to domestic biofuels policy shocks. The rising importance of soybean oil as a biofuels feedstock in US has increased the importance of domestic policy decisions, such as blending incentives and volume obligations, in driving U.S. soybean oil use and price.

Our central conclusion is that there is no longer a single global vegetable oil market signal. To an increasing degree, farmers, crushers, renewable fuels producers, and policymakers need to watch both broad global shocks and more local, product-specific shocks. That means tracking not only world demand and overall stocks, but also U.S. biofuel policy decisions, biodiesel and export rules in Indonesia and Malaysia, and weather and crop developments in South America and Southeast Asia. Managing soybean oil price risk in this new environment requires paying attention to all these moving parts, not just a single commodity price.