Nvidia on Wednesday evening delivered better-than-expected quarterly results, with a guide that should impress even those with the highest of expectations. Revenue in the company’s fiscal 2026 third quarter grew 62% year over year to $57.01 billion, outpacing the $54.92 billion the Street was looking for, according to estimates compiled by data provider LSEG. Adjusted earnings per share for the three months ending Oct. 26 increased 67% to $1.30, also exceeding the consensus estimate of $1.25, per LSEG data. NVDA YTD mountain Nvidia YTD Talk about a strong showing. In addition to solid beats on the top and bottom lines, management guided current quarter sales to a level not only above consensus estimates but also above the so-called whisper number that was floating around. For those unfamiliar with the term, the estimates that most market watchers and participants, like the Club, cite come from sources like LSEG, FactSet, or Bloomberg – all market data platforms. These estimates are compiled from sell-side analysts, who work at the banks and firms that sell research. The whisper number, however, is what the buy-side – those who run money, like hedge funds, asset management firms, pension funds, and so on – is believed to be looking for. It sometimes happens that a stock can beat the consensus estimate and miss the whisper number, resulting in a stock move lower. Beating the whisper number, however, is an important feat as it means the company is doing even better than the ones running money and risking it on the company, expected – a very bullish sign. Nvidia shares jumped 5% in after-hours trading to $196, a step in the right direction back toward their record-high close of $207 on Oct. 29 and back toward a $5 trillion market cap. We’re reiterating our hold-equivalent 2 rating but bumping up our Nvidia price target to $230 per share from $225. Bottom line Management not only has visibility on just about 100% of the revenue the Street is modeling for next year, but appears to have indicated on the call that the $500 billion number CEO Jensen Huang called out in October is already growing. Helping to drive the growth, Huang explained that the world is currently undergoing three computing transitions simultaneously. First, Huang said there has been a shift from CPU-based general computing to GPU-based accelerated computing. (CPUs are central processing units, long seen as the brains and workhouses of traditional computers. GPUs are graphics processing units, which have become the heart and soul of AI workloads because they can complete many calculations at the same time. That parallel processing is a key advantage over CPUs.) Second, he said that AI is at a “tipping point,” transforming existing applications and enabling new ones. “For existing applications, generative AI is replacing classical machine learning in search ranking, recommender systems, ad targeting, click through prediction, to content moderation. The very foundations of hyperscale infrastructure.” Third, he said, is so-called agentic AI systems “capable of reasoning, planning, and using tools.” (Agentic AI is a type of system that can complete tasks without human supervision — for example, instead of just looking up a flight, it could book it for the user.) Why we own it Nvidia’s high-performance graphics processing units (GPUs) are the key driver behind the AI revolution, powering the accelerated data centers being rapidly built around the world. But Nvidia is more than just a hardware story. Through its Nvidia AI Enterprise service, Nvidia is building out its software business. Competitors : Advanced Micro Devices and Intel Most recent buy : Aug 31, 2022 Initiation : March 2019 At the center of it all is Nvidia. Huang said, “As you consider infrastructure investments, consider these three fundamental dynamics. Each will contribute to infrastructure growth in the coming years. Nvidia’s chosen because our singular architecture enables all three transitions, and thus so, for any form and modality of AI across all industries, across every phase of AI, across all of the diverse computing needs in the cloud, and also from cloud to enterprise to robots – one architecture.” Commentary Coming into the earnings print, we highlighted five questions posed by Ben Reitzes of Melius Research that we hoped Huang would address. The CEO and other company executives answered four of them. The first question from Reitzes was whether the capital expenditure growth could continue through the end of the decade. While time will tell, we said that it was largely going to depend on end market demand, which itself depends on the ability of Nvidia’s customers to monetize the spend. As far as demand goes, Huang got straight to the point on the earnings release, stating “Blackwell sales are off the charts, and cloud GPUs are sold out,” adding that “compute demand keeps accelerating and compounding across training and inference — each growing exponentially.” (Blackwell is the current chip platform from Nvidia) Another question Reitzes raised was: What will Nvidia do with all its free cash flow? Buybacks are clearly still in play, with the company exiting the quarter with $62.2 billion remaining of its share repurchase authorization, even as the company has already returned $37 billion to shareholders this year, through its fiscal third quarter via dividends and buybacks. On the call, Huang said that in addition to buybacks, which will continue, the cash is going to be used to fund further growth and make strategic investments. Nvidia has been on a tear, making “strategic investment” after “strategic investment” – from committing to a $100 billion multiyear investment and partnership with ChatGPT creator OpenAI to taking stakes in rival Claude creator Anthropic, Intel, and neocloud provider CoreWeave. A third question from Reitzes dealt with the need for clarity on the $500 billion of orders for Blackwell and the next generation Rubin that Huang mentioned last month at the company’s GTC conference. On the call, CFO Colette Kress said, “We currently have visibility to a half trillion dollars in Blackwell and Rubin revenue, from the start of this year through the end of calendar year 2026.” Now, Nvidia’s fiscal year is a bit off; it’s almost a year ahead and ends in January. But if we assume that Nvidia does $212.8 billion in its current 2026 fiscal year – about what has thus far been reported, plus the $65 billion from the guidance for the current quarter – that leaves just over $287 billion to be realized in most of its fiscal year 2027, which again extends about one month past the end of calendar year 2026. We know it’s confusing, but suffice it to say, Nvidia already has visibility on nearly 100% of the sales Wall Street is looking for, with time still to go to generate even more orders as enterprise, consumer, and perhaps most exciting, sovereign adoption ramps up. In fact, based on commentary on the call, it seems there have already been announcements for new orders not included in that $500 billion figure, with Kress saying that the deal announced with the Kingdom of Saudi Arabia for 400,000 to 600,000 more GPUs over the three years is new, as is the recently announced deal with Anthropic. “So, there’s definitely an opportunity for us to have more on top of the $500 billion that we announced,” Kress stated. As for Reitzes’ question on margins, they’re clearly going to hold in for the near-term, with management guiding the current quarter to a level above expectations. “Looking ahead to fiscal year 2027, input costs are on the rise, but we are working to hold gross margins in the mid-70s,” Kress said. That’s precisely what the Steet was looking for. The one Reitzes question that Huang did not expand on was about remarks the CEO made earlier this month to the Financial Times, saying “China is going to win the AI race.” At the time, Huang softened that language in a statement, saying “China is nanoseconds behind America in AI,” adding it is vital the U.S. wins by “racing ahead.” While this particular line of inquiry was not mentioned on the call, Huang did say, “While we were disappointed in the current state that prevents us from shipping more competitive data center compute products to China, we are committed to continued engagement with the U.S. and China governments and will continue to advocate for America’s ability to compete around the world.” Nvidia has said for a while now that its forward guidance includes zero sales from China. Segment results Data center , the biggest of Nvidia’s five operating segments, saw revenue increase 66% year over year to a better-than-expected $51.22 billion in fiscal 2026 Q3, and a stunning 25% sequentially. Within the data center unit, compute revenue rose 56% to $43 billion, and networking revenue gained 162% to $8.2 billion. Gaming saw revenue jump 30% to $4.27 billion, but it did miss estimates of $4.41 billion. Professional Visualization revenue jumped 56% and was driven by the company’s recently released DGX Spark, a Grace Blackwell-based AI supercomputer small enough to fit on your desk, and Blackwell sales growth. On the call, Kress said, “Pro visualization has evolved into computers for engineers and developers, whether for graphics or for AI.” Automotive revenue was up 32% year over year as the industry continues to adopt Nvidia’s autonomous solutions. That number was, however, short of expectations. The OEM & Other segment saw revenue up 79%. This unit at Nvidia covers partnerships with original equipment manufacturers, licensing, and other things not accounted for in the other segments. Guidance Looking ahead to the current fiscal 2026 fourth quarter, management’s outlook was largely better than expected. Revenue of $65 billion, plus or minus 2%, was ahead of not only the $61.66 billion LSEG consensus estimate, but also the $64 billion whisper number that was being floated around Wall Street ahead of the release. Adjusted gross margins are expected to be 75%, plus or minus 50 basis points, better than the 74.1% estimate compiled by FactSet. Expectations for adjusted operating expenses in the fiscal fourth quarter of $5 billion are about in line with expectations. (Jim Cramer’s Charitable Trust is long NVDA. See here for a full list of the stocks.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.

Category: 3. Business

-

Myanmar’s Tourism Industry: Recent Developments, Prospects and Challenges Ahead – ASEAN+3 Macroeconomic Research Office

Myanmar’s tourism industry experienced unprecedented growth between 2011 and 2019, fueled by policy reforms, foreign investment, and international interest. The sector received significant foreign investment and saw rapid hotel expansions during this period. The upward trajectory was interrupted by the COVID-19 pandemic in 2020, followed by geopolitical challenges and natural disasters. The analytical note is intended to provide a historical context of Myanmar’s tourism developments since opening-up in 2011, while offering a narrative on the outlook ahead. This comes at a juncture where the tourism industry has rapidly evolved into a crucial pillar of Myanmar’s economy and a key driver of its social and economic development.

Continue Reading

-

Should US Growers Look to Africa as the Next Big Market? Understanding Africa’s Soy Import Demand

Introduction

The Soybean Innovation Lab (SIL) introduces readers to the question whether Sub Saharan Africa (SSA) presents a new market opportunity for US soybean growers. Over the next three weeks SIL and farmdoc will deliver three articles on the topic of Africa as a potential export market for US soybeans. The African market presents a very complex landscape. While it is large, diverse, and growing rapidly, there exists great uncertainty, significant business risks, and demand for soybean and associated products are just beginning to emerge.

This first article in the series focused on the larger food and oil trends dominating the African continent (see farmdoc daily from November 13, 2025). Today’s article delves into the import flows of soybean, oil, and meal into Africa. The third article will wrap up the series by outlining four specific country examples – Egypt, Ghana, Nigeria, and Tanzania – touching on their imports of soy and soy products, logistics infrastructure, and existing policies on genetically modified soybean imports. The third and final article will also include a relevant literature review on the subject of soy trade and Africa.

Soy Import Demand in SSA

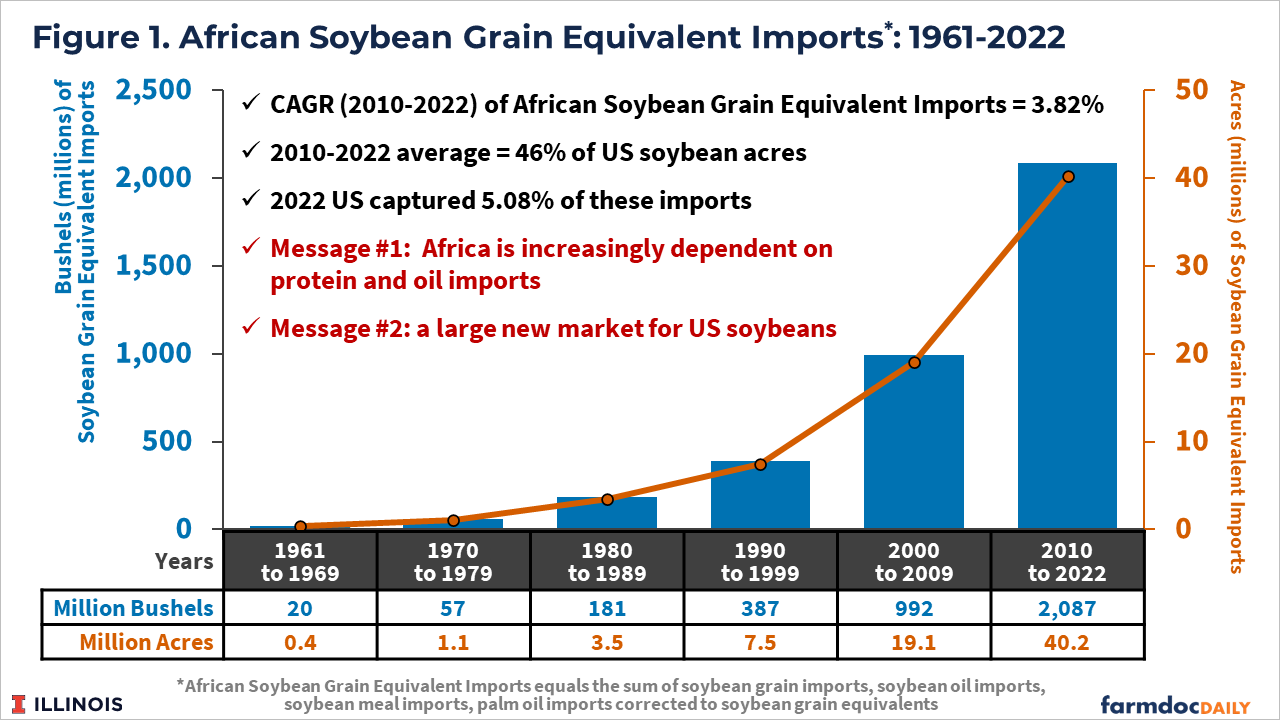

Is SSA soy import demand significant, or at least potentially significant? The answer is yes. Soy product demand is potentially very significant. Using the soybean equivalent import metric, Africa imported a soybean equivalent of 2.1 billion bushels on average per year for the period 2010-2022. That equals the production of about 40 million acres, about 47% of US plantings (see Figure 1). Most of that value results from palm oil imports (64%). Soybean oil, meal, and grain imports amount to 21%, 8%, and 7%, respectively.

The Africa soybean grain import equivalent metric comprises the sum of: 1) soybean imports, 2) soybean oil imports, 3) soybean meal imports, and 4) palm oil imports all corrected to soybean grain equivalents. That is, based on current soy and palm product imports, were it grain, the metric captures how much grain would theoretically be demanded by Africa’s processors and manufacturers. The grain equivalent metric melds both current import activity and the potential to expand soybean export demand by taking market share from palm oil. The equivalent metric, when measured in bushels and acres also allows comparison with US production.

These imports grew at a compound annual growth rate (CAGR) of 3.82% between 2010 and 2022. Soybean grain imports lead the group growing at a CAGR of 8.04%, with palm oil, soybean oil, and soybean meal growing at 4.46%, 2.05%, and -0.34%, respectively.

African soybean production currently amounts to 270 million bushels or about 6% of US production and 2% of global production (see Figure 2). Global soybean output over the last ten years has grown at a CAGR of 2% while African production has grown at an annual rate of 11%. While growing rapidly, Africa will remain far from being self- sufficient in the future and require significant imports. For example, forecasts to 2050 show Africa would still only be able to supply 35% of its current soybean equivalent import demand, even assuming the current soybean production growth rate.

Finally, African soybean processors in the 1960’s had very little use for soybean, processing less than 20% of the region’s soybean crop to produce food oil (see Figure 3). Over time, processors have expanded capacity and by 2002 the industry switched from an under capacity position to overcapacity where local supplies were not sufficient to meet demand resulting in significant acceleration in the imports of soybean grain. Most recently, processors are 40-60% overcapacity relative to domestic supply and import about 200 million bushels of soybeans to keep their factories operating. Demand for soybean grain imports since 2010 has been quite fast with a compound annual growth rate of just over 8%.

Note: The Soybean Innovation Lab (SIL) at the University of Illinois is the world’s leading organization focused on establishing soybean as the feed, oil, industrial materials, and biofuels standard in Sub Sharan Africa (SSA). SIL’s strong network across 31 countries, experienced team, track record of success, and partners on the ground support clients looking to serve the fastest growing and a potentially large new soy market.

Continue Reading

-

Fujitsu launches integrated package of core system support services for food distribution industry

Fujitsu today announced the launch of a new integrated package of services for the food distribution industry aimed at helping customers build business systems inexpensively and quickly and supporting the digital transformation of the whole industry. More than 1,500 functions for building business systems will eventually be offered including management for sales, orders, inventory, and logistics, and the gradual roll out will start in December 2025 and conclude by the end of fiscal 2026.

By leveraging existing solutions and working closely with partner companies, Fujitsu will continue to enhance its capabilities, including end-to-end data integration across the entire food distribution value chain and the standardization of interfaces and master data. Fujitsu also plans to offer the service globally to support customers’ overseas expansion.

Continue Reading

-

Baker McKenzie Advises Sampoerna Group on its Divestment of Sampoerna Agro to POSCO International’s Subsidiary | Newsroom

Baker McKenzie, together with its member firms Baker McKenzie Wong & Leow in Singapore and HHP Law Firm in Indonesia, has advised Twinwood Family Holdings Limited, part of the Sampoerna Strategic Group (“Sampoerna Group”), on the divestment of its entire 65.721% stake in PT Sampoerna Agro Tbk (“SGRO”), to AGPA Pte. Ltd., a subsidiary of POSCO International Corporation (“POSCO International”; Stock Code: 047050.KS), a Korean conglomerate engaged in trading, energy, steel, and agribusiness.

The deal represents a key milestone in Sampoerna Group’s business transformation, enabling the company to seek new opportunities that are in line with current business needs and market trends. The transaction also marks a new chapter for SGRO as it embarks on the next phase of its growth under POSCO International’s management control.

Indonesia’s palm oil industry accounts for around 60% of total global production, with crude palm oil exports of about 50% of total global exports. SGRO is a leading listed company in Indonesia operating palm plantations across Sumatra and Kalimantan. It also owns a specialized palm seed subsidiary and research institute that together hold the second-largest share in the domestic palm seed market.

The cross-border deal team was led by Principals Theodore Heng (M&A) and Bee Chun Boo (M&A), with the support of Senior Associate Alexa Jiang, Associate Gerald Lim and Trainee Willy Wai in Singapore as well as Partner Daniel Pardede (M&A), Associate Partner Bimo Harimahesa (M&A), Senior Associate Bratara Damanik and Associate Naztasha Cesty (Capital Markets) in Jakarta.

The core team was further supported by multidisciplinary experts across Singapore, Indonesia, Seoul and Dubai, including: Principals Shih Hui Lee (Tax Advisor) and Emmanuel Chua (Dispute Resolution); Partners Iqbal Darmawan (Capital Markets), Seong Hoon Yi (M&A) and Stephanie Samuell (M&A); Senior Associates Santri Satria and Shawn Joo; and Associates Ernest Low, Sharon Tay, Novrita Nadila Humaira, Devinka Adira, Samuel Evan Hardy, Jose Guardiola and Pricilla Patricia.

With more than 2,700 deal practitioners in over 40 jurisdictions, Baker McKenzie is a transactional powerhouse. The Firm has the broadest M&A footprint of any law firm globally, with more than 1,300 locally qualified and globally experienced M&A lawyers. The team excels at advising clients on their most complex, cross-border M&A matters and has advised on more than USD 600 billion in M&A transactions in the last five years (Refinitiv; 2020-2024).

Continue Reading

-

Asian chip names rally as Nvidia forecasts hotter-than-expected sales after earnings beat

A 300mm wafer on display at the booth of Taiwan Semiconductor Manufacturing Company during the 2023 World Semiconductor Conference at Nanjing International Expo Center on July 19, 2023, in Nanjing, China.

Vcg | Visual China Group | Getty Images

Asian chip stocks rallied in early trading Thursday after American AI chip darling Nvidia beat Wall Street expectations and issued stronger-than-expected guidance for the fourth quarter.

South Korea’s SK Hynix rallied around 4%. The memory chip maker is Nvidia’s top supplier of high-bandwidth memory used in AI applications.

Samsung Electronics, which also supplies Nvidia with memory, was also up nearly 4%. The company has been working to catch up to SK Hynix in high-bandwidth memory to land more contracts with Nvidia.

In Tokyo, Renesas Electronics, a key Nvidia supplier, was trading up about 4%. Tokyo Electron, which provides essential chipmaking equipment to foundries that manufacture Nvidia’s chips, was trading up 5.87%. Another Japanese chip equipment maker, Lasertec, was up about 6%.

Japanese tech conglomerate SoftBank skyrocketed nearly 7%, though the firm recently offloaded its shares of Nvidia. Softbank owns the majority of British semiconductor company Arm, which supplies Nvidia with chip architecture and designs.

SoftBank is also involved in a number of AI ventures that use Nvidia’s technology, including the $500 billion Stargate project for data centers in the U.S.

Nvidia’s sales and outlook are closely watched by the technology industry as a sign of the health of the AI boom, and its strong earnings could ease recent fears regarding an AI bubble.

“There’s been a lot of talk about an AI bubble,” Nvidia CEO Jensen Huang told investors on an earnings call. “From our vantage point, we see something very different.”

Continue Reading

-

JGB Yields May Rise Amid Fiscal Policy Concerns – The Wall Street Journal

- JGB Yields May Rise Amid Fiscal Policy Concerns The Wall Street Journal

- Benchmark JGB yields touch 17-year high on spending concerns Business Recorder

- Japan’s borrowing costs at highest in decades on fears of public spending surge Financial Times

- Market Euphoria Ends for Takaichi as Yen and Bonds Sink Bloomberg.com

- Japan’s $127 billion stimulus plan to include payouts to children, Asahi reports By Reuters Investing.com

Continue Reading

-

Victoria to force agents to publish property reserve prices in crackdown on underquoting | Real estate

Real estate agents in Victoria will be legally required to reveal a property’s reserve price a week before auction, under nation-first laws to crack down on underquoting.

The Allan government on Thursday announced the major reform that would be introduced to parliament next year.

Under the changes, agents must publish the owner’s reserve price at least seven days before auction day or a fixed-date sale. Real estate agents that fail to disclose within the timeframe will be unable to proceed to auction or sale.

Illegal underquoting is an industry tactic used by some agents who advertise a property for less than the estimated selling price or the owner’s asking price. They do this to draw buyers in and drum up competition.

Sign up: AU Breaking News email

Victoria’s consumer affairs minister, Nick Staikos, said the government wanted to ensure the housing market to be fair.

“Underquoting isn’t fair and it’s young Victorians and families paying the price,” he said in a statement.

Last year, a Guardian Australia analysis of property sales data showed underquoting (here defined as any sale where the final price exceeds 10% of the pre-sale price guide) is more prevalent in Sydney (20% of sales) and Perth (18%), and least prevalent in Canberra, Hobart and Darwin.

The analysis found the mismatch between the price guide on property ads and the final sale price was worse for houses than townhouses or apartments and is much more likely when the property is being sold at auction than at private sale.

Under the changes, real estate agents would be required to update all marketing materials to reflect the reserve price and stop using any previous advertising that does not contain the reserve price.

The proposed laws come after the Victorian government earlier this month introduced stricter guidelines for agent’s selection of comparable properties to determine a home’s price guide.

The guidelines aim to ensure agents use the most appropriate comparable local properties when determining a home’s likely price before auction, factoring in things like the dwelling’s age and any renovations.

Consumer Affairs Victoria can ask for evidence from agents showing how they chose the three most comparable properties, and penalties apply for not providing these records.

Last week, the NSW government announced new rules for real estate agents that would mandate price guides on all advertising and a statement of information offered to buyers backing up their estimated sales price – similar to Victoria’s existing system.

In NSW, agents who underquote can be fined up to $22,000 and lose their commission and fees earned from the sale of an underquoted property.

In Victoria, agents who underquote risk fines of more than $11,000 for each breach, or penalties of over $38,000 under the Estate Agents Act.

But the head of consumer research at Finder, Graham Cooke has previously told Guardian Australia these regulations often don’t work – and underquoting keeps happening.

Continue Reading

-

Assessing Morgan Stanley’s Value After Leadership Changes and a 30% Price Surge in 2025

-

Ever wondered if Morgan Stanley’s stock is the opportunity you’ve been waiting for? Let’s dig in to see what’s really driving its perceived value right now.

-

The stock recently closed at $162.29, showing a year-to-date surge of 30.1% and a gain of 26.7% over the past year, though it dipped 4.5% in the last week alone.

-

Market chatter has picked up amid sector rotation into financials, driven by renewed optimism around interest rate cuts. Recent headlines about Morgan Stanley expanding its wealth management footprint and making strategic leadership changes have also caught investors’ attention.

-

Our initial valuation score for Morgan Stanley comes in at 3 out of 6 on key metrics, meaning it appears undervalued in half of our checks. Next, we will break down how this score was calculated using different approaches, so keep reading for a smarter way to think about valuation later in the article.

Morgan Stanley delivered 26.7% returns over the last year. See how this stacks up to the rest of the Capital Markets industry.

The Excess Returns model evaluates a company’s value by measuring how much return it generates above its cost of equity on invested capital. This method focuses on long-term profitability instead of relying solely on cash flow projections. For Morgan Stanley, key metrics highlight its ability to create shareholder value above the basic cost of capital.

Morgan Stanley’s Book Value per share is $62.98, and its Stable Earnings Per Share are estimated at $11.10, based on weighted future Return on Equity estimates from 13 analysts. The Cost of Equity is calculated at $6.64 per share, resulting in an Excess Return of $4.46 per share. This indicates an Average Return on Equity of 16.30%, reflecting strong capital efficiency. In addition, the Stable Book Value is projected to reach $68.10 per share, according to future estimates from 14 analysts.

According to this model, the intrinsic value per share is estimated at $136.77. With the recent share price at $162.29, the stock appears to be 18.7% above its intrinsic value, which suggests it is currently overvalued by this approach.

Result: OVERVALUED

Our Excess Returns analysis suggests Morgan Stanley may be overvalued by 18.7%. Discover 897 undervalued stocks or create your own screener to find better value opportunities.

MS Discounted Cash Flow as at Nov 2025 Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Morgan Stanley.

The Price-to-Earnings (PE) ratio is widely recognized as a valuable yardstick for profitable companies like Morgan Stanley because it connects the company’s current share price to its annual earnings. This makes it easier to gauge whether investors are paying a fair price for each dollar of net income. For companies with steady profits, the PE ratio helps investors quickly compare relative valuation across peers and industries.

Continue Reading

-