- FDA OKs First Cell Therapy for Severe Aplastic Anemia Medscape

- Aplastic Anemia Market Expected to Experience Major Growth by 2034, According to DelveInsight openPR.com

- Additional Positive Results for Omisirge(R) in Treating Severe Aplastic Anemia Presented at ASH Lexington Herald Leader

- Gamida Cell’s Omisirge becomes first FDA-cleared cell therapy for rare blood disorder FirstWord Pharma

- FDA approves omidubicel-onlv as first HSCT therapy to treat severe aplastic anemia Contemporary Pediatrics

Category: 3. Business

-

FDA OKs First Cell Therapy for Severe Aplastic Anemia – Medscape

-

‘I feel it’s a friend’: quarter of teenagers turn to AI chatbots for mental health support | Chatbots

It was after one friend was shot and another stabbed, both fatally, that Shan asked ChatGPT for help. She had tried conventional mental health services but “chat”, as she came to know her AI “friend”, felt safer, less intimidating and, crucially, more available when it came to handling the trauma from the deaths of her young friends.

As she started consulting the AI model, the Tottenham teenager joined about 40% of 13- to 17-year-olds in England and Wales affected by youth violence who are turning to AI chatbots for mental health support, according to research among more than 11,000 young people.

It found that both victims and perpetrators of violence were markedly more likely to be using AI for such support than other teenagers. The findings, from the Youth Endowment Fund, have sparked warnings from youth leaders that children at risk “need a human not a bot”.

The results suggest chatbots are fulfilling demand unmet by conventional mental health services, which have long waiting lists and which some young users find lacking in empathy. The supposed privacy of the chatbot is another key factor in driving use by victims or perpetrators of crimes.

After her friends were killed Shan, 18, not her real name, started using Snapchat’s AI before switching to ChatGPT, which she can talk to at any time of day or night with two clicks on her smartphone.

“I feel like it definitely is a friend,” she said, adding that it was less intimidating, more private and less judgmental than her experience with conventional NHS and charity mental health support.

“The more you talk to it like a friend it will be talking to you like a friend back. If I say to chat ‘Hey bestie, I need some advice’. Chat will talk back to me like it’s my best friend, she’ll say, ‘Hey bestie, I got you girl’.”

One in four of 13- to 17-year-olds have used an AI chatbot for mental health support in the past year, with black children twice as likely as white children to have done so, the study found. Teenagers were more likely to go online for support, including using AI, if they were on a waiting list for treatment or diagnosis or had been denied, than if they were already receiving in-person support.

Crucially, Shan said, the AI was “accessible 24/7” and would not tell teachers or parents about what she had disclosed. She felt this was a considerable advantage over telling a school therapist, after her own experience of what she thought were confidences being shared with teachers and her mother.

Boys who were involved in gang activities felt safer asking chatbots for advice about other safer ways to make money than a teacher or parent who might leak the information to police or other gang members, putting them in danger, she said.

Another young person, who has been using AI for mental health support but asked not to be named, told the Guardian: “The current system is so broken for offering help for young people. Chatbots provide immediate answers. If you’re going to be on the waiting list for one to two years to get anything, or you can have an immediate answer within a few minutes … that’s where the desire to use AI comes from.”

Jon Yates, the chief executive of the Youth Endowment Fund, which commissioned the research, said: “Too many young people are struggling with their mental health and can’t get the support they need. It’s no surprise that some are turning to technology for help. We have to do better for our children, especially those most at risk. They need a human not a bot.”

There have been growing concerns about the dangers of chatbots when children engage with them at length. OpenAI, the US company behind ChatGPT, is facing several lawsuits including from families of young people who have killed themselves after long engagements.

In the case of the Californian 16-year-old Adam Raine, who took his life in April, OpenAI has denied it was caused by the chatbot. It has said it has been improving its technology “to recognise and respond to signs of mental or emotional distress, de-escalate conversations, and guide people toward real-world support.”. The startup said in September it could start contacting authorities in cases where users start talking seriously about suicide.

Hanna Jones, a youth violence and mental health researcher in London, said: “To have this tool that could tell you technically anything – it’s almost like a fairytale. You’ve got this magic book that can solve all your problems. That sounds incredible.”

But she is worried about the lack of regulation.

“People are using ChatGPT for mental health support, when it’s not designed for that,” she said. “What we need now is to increase regulations that are evidence-backed but also youth-led. This is not going to be solved by adults making decisions for young people. Young people need to be in the driving seat to make decisions around ChatGPT and mental health support that uses AI, because it’s so different to our world. We didn’t grow up with this. We can’t even imagine what it is to be a young person today.”

Continue Reading

-

OCI Global and Orascom Construction Announce Agreement to combine to create a Global Infrastructure and Investment Platform – OCI

- Agreed exchange ratio of 0.4634 Orascom Construction shares per OCI share

- Creates a scalable infrastructure and investment platform combining complementary capabilities of both companies

- Nassef Sawiris will serve as Non-Executive Chair of the combined entity

- Board and Executive Management will be announced before closing of the Combination

- Upon closing, Combination to be renamed “Orascom” with three complementary strategic pillars: Orascom Infrastructure, Orascom Construction and Orascom Capital

Amsterdam / 9 December 2025: Further to the preliminary announcement on 22 September, OCI Global (Euronext: OCI, “OCI”) is pleased to announce that it and Orascom Construction PLC (ADX and EGX: ORAS) have reached an agreement in respect of their envisaged combination (the “Combination”) to establish a scalable Abu Dhabi-anchored infrastructure and investment platform with enhanced reach, diversification and growth prospects.

OCI shareholders will become shareholders of Orascom Construction, with their collective holding equating to approximately 47% in Orascom Construction post-Combination. This is on the basis of an exchange ratio determined with reference to the equity value of each of OCI and Orascom Construction, entitling each OCI shareholder to 0.4634 Orascom Construction Shares for each OCI share held[1]. OCI’s Board of Directors has approved the Combination, subject to shareholder approval, and will in due course call for an Extraordinary General Meeting to be held in January 2026.

The combined entity will unite Orascom Construction’s world class execution capabilities, infrastructure expertise, concessions development experience, and strong pipeline of opportunities with OCI’s track record of building and developing successful platforms across complementary business verticals, its transactional expertise and a common disciplined approach to capital deployment.

Combination Rationale

The Combination is intended to provide OCI shareholders with exposure to a larger, more diversified growth platform, strategic focus on value creation in the infrastructure sector, Orascom Construction’s engineering procurement and construction (EPC) expertise, and a proven track record of delivering complex landmark projects across industries in the United States, the GCC/Middle East, Europe, Australia and select emerging markets. This is complemented by Orascom Construction’s growing infrastructure concessions portfolio spanning three continents.

The Combination will benefit from a stronger balance sheet and an enhanced funding capacity that should enable the deployment of more than a billion dollars of equity by year-end 2026 into future investments in scalable cash generative assets, leveraging the companies’ respective execution track records and global reach. The combined entity will retain the flexibility to invest through both direct ownership and partnership models across equity and other available instruments, in addition to operations and maintenance involvement. The combined entity will evaluate and pursue infrastructure opportunities alongside an existing EPC and concessions business, targeting risk-adjusted returns with visible cashflows and recurring income streams, with “Orascom Infrastructure” positioned as a high-growth vertical within the new group.

Over the past three decades, OCI and Orascom Construction have collectively completed equity and debt transactions spanning capital markets, development projects, and M&A totaling USD 89 billion[2]. OCI has distributed approximately USD 22 billion in dividends to its shareholders, delivering an internal rate of return of approximately 39%[3]. This track record underscores both companies’ ability to create and monetize sector-leading platforms and to generate sustainable shareholder value.

Nassef Sawiris, Executive Chairman of OCI commented:

“This proposed Combination marks a new chapter for OCI and Orascom Construction, creating an integrated infrastructure and investment platform with strong capabilities and enhanced growth potential. As we celebrate 75 years of heritage, our focus remains on performance excellence, disciplined capital deployment, and long-term value creation.”

Michael Bennett, Senior Independent Director and Co-Chairman of OCI commented:

“The proposed Combination signals the beginning of a consolidated and more ambitious future for the group, bringing back together two highly respected businesses and their respective management teams with complementary strengths, and a shared commitment to shareholder value creation and governance excellence. Abu Dhabi’s emergence as a major global center for capital and financial markets, combined with the global footprint of the combined group and an infrastructure focus, demonstrates a further strategic pivot consistent with the group’s history of proactively capitalizing on global trends of relevance, creating societal value while maximizing shareholder returns.”

Hassan Badrawi, Chief Executive Officer of OCI commented:

“The proposed Combination is a further strategic step toward realising the full potential value of the platform. Since becoming listed in 1999, OCI has continuously evolved and delivered value through smart transformation and investment across multiple sectors. The management team is excited and fully committed to this next chapter of growth, where we will continue to build scale, create opportunity and deliver attractive sustainable returns for our shareholders.”

Governance and Independence of Decision Making by the Board

The Combination has been unanimously recommended by the independent directors on OCI’s board. Nassef Sawiris and Nadia Sawiris both declared a conflict of interest regarding the Combination and therefore did not participate in the board’s deliberations and decision-making. A special committee, comprised of independent directors, provided oversight of the process in preparation for the independent board’s decision making.

On 9 December 2025, Rothschild & Co issued a written fairness opinion to the Board stating that from a financial point of view, the proposed sale is fair to OCI (the Fairness Opinion). The Fairness Opinion was provided solely for the benefit of OCI’s board, in connection with, and for the sole purpose of their evaluation of the Combination.

Orascom Construction has also unanimously recommended the proposed Combination to its shareholders.

The composition of the Combination’s board and its executive leadership team will be announced prior to completion of the Combination. Nassef Sawiris will serve as Non-Executive Chairman of the combined entity.

Structure of the Proposed Combination

On 9 December, OCI and Orascom Construction reached agreement to give effect to the Combination, subject to shareholder approval. This will be achieved by the followings steps:

- OCI statutorily demerges substantially all of its assets and liabilities into a newly-incorporated, wholly-owned subsidiary (“MergeCo”);

- OCI transfers its 100% shareholding in MergeCo to Orascom Construction, in exchange for which Orascom Construction issues new shares to OCI (the “Orascom Shares”);

- OCI distributes the Orascom Shares to its shareholders; and

- Finally, OCI liquidates and delists from Euronext Amsterdam.

Orascom Construction will then continue as the surviving ADGM-incorporated and ADX- and EGX-listed entity holding OCI’s business, assets and liabilities. Upon closing, the Combination will be renamed “Orascom” with three complementary strategic pillars: Orascom Infrastructure, Orascom Construction and Orascom Capital.

OCI shareholders will become shareholders of Orascom Construction, with their collective holding equating to approximately 47% in Orascom Construction post-Combination. This is on the basis of an exchange ratio determined with reference to the equity value of each of OCI and Orascom Construction, entitling each OCI shareholder to 0.4634 Orascom Shares for each OCI share held[4].

The Fairness Opinion issued by Rothschild & Co confirmed that this exchange ratio and the consideration accordingly received are fair from a financial point of view for OCI. The Fairness Opinion also considered the eventual liquidation of OCI’s status quo. Similarly, an independent assessment of Orascom Construction’s valuation was also in scope of the Fairness Opinion. Furthermore, both legal and financial due diligence was conducted to identify any material issues that may have warranted consideration in the Fairness Opinion.

An independent valuation has been issued by BDO Chartered Advisors & Accountants – UAE (“BDO”) – an independent firm licensed by the Securities and Commodities Authority in respect of Orascom Construction.

Valuation and Exchange RatioOCI and Orascom Construction have agreed on an exchange ratio, which is based on an equity value for OCI of approximately USD 1.35 billion and an equity value for Orascom Construction of approximately USD 1.52 billion. Accordingly, OCI will receive 97,201,359 newly issued Orascom shares in consideration for the sale of its business. Combined with OCI’s existing holding of 561,803 Orascom Shares, this implies an exchange ratio (Orascom shares per OCI share) of 0.4634. Following completion of the Combination, OCI shareholders will own approximately 47 per cent of Orascom Construction.

Conditionality and TimingCompletion of the Combination remains subject to, amongst other customary conditions, the approval by the shareholders at the Extraordinary General Meetings (EGMs) of each of OCI and Orascom Construction, and the successful implementation of the above demerger.

OCI will shortly announce the convocation of an EGM to be held in January 2026. The invitation, agenda and explanatory notes and related convocation materials will be made available on OCI’s website at www.oci-global.com and a separate announcement will follow. Orascom Construction will also announce the convocation of an EGM to be held in January 2026.

If both EGMs approve the Combination, the Demerger and thereafter the remaining steps of the Combination will be implemented in the weeks that follow. It is expected that the distribution of Orascom Shares to OCI shareholders will be effected in the first half of Q1 2026[4] with more detailed dates to be communicated in due course.

For more detail on the steps required to take delivery of the Orascom Shares, or otherwise for more information on the arrangements put in place for shareholders who do not or cannot take delivery thereof, please see Delivery of OC Shares to OCI Shareholders in the agenda and explanatory notes to be made available as part of the Shareholder Circular.

Note on Delivery of Orascom Construction shares to OCI shareholders

Orascom Shares will be credited to the shareholder’s securities account by their financial intermediary if OCI has been provided with the necessary information. If such information has not been provided, shareholders will receive a beneficial entitlement to Orascom Shares. ABN AMRO will circulate a Technical Information Memorandum to institutions admitted to Euroclear Nederland, setting out the operational mechanics of the Combination, including the procedures to obtain a NIN for opening an ADX securities account, and the terms applicable to the sales facilities that will be provided for the sale of OCI shares. OCI Shareholders will be informed by their financial intermediary about the Combination and what kind of actions are required from the shareholders.

OCI Q3 2025 Trading Statement

Please refer to OCI’s Q3 2025 Trading Statement, which was published today.

AdvisorsDe Brauw Blackstone Westbroek N.V. provided legal advice to OCI’s board, while Rothschild & Co served as the board’s financial advisor and provided a fairness opinion. A&O Shearman and Rabobank served as the Company’s legal and financial advisors, respectively. ABN AMRO advised the Company in its role as exchange agent in the context of share settlement mechanics, and Deloitte undertook financial due diligence for the Company.

BDO Chartered Advisors & Accountants – UAE (“BDO”) – an independent firm licensed by the Securities and Commodities Authority, was appointed by Orascom Construction as an independent valuer to determine the fair value ranges of both Orascom Construction and OCI and to derive an appropriate share exchange ratio. White & Case served as Orascom Construction’s legal counsel, EFG Hermes and First Abu Dhabi Bank served as Orascom Construction’s financial advisors, and KPMG undertook Orascom Construction’s financial and tax due diligence.

Investor and Analyst Conference Call

OCI will host a conference call for investors and analysts on 11 December 2025 at 13:00 CET. Details of the call will be available on the Company’s website at www.oci-global.com.

This press release contains information within the meaning of Article 7(1) of the EU Market Abuse Regulation.

* Ends *

ABOUT OCI GLOBAL

OCI Global (Euronext: OCI) is a global investment platform focused on long-term value creation through disciplined capital allocation. With a 30-year history of building and scaling sector-leading businesses in fertilizers, methanol, cement, and infrastructure, OCI has returned over USD 7 billion to shareholders since 2022.

Learn more at www.oci-global.com. Follow OCI on LinkedIn.

ABOUT ORASCOM CONSTRUCTION PLC

Orascom Construction PLC (ADX and EGX:ORAS, “Orascom Construction” or the “Group”) is a leading global engineering and construction contractor with a long-standing track record of delivering large-scale, complex infrastructure, industrial, and commercial projects across the Middle East, Africa, and the United States.

The Group has a global infrastructure and industrial track record of projects completed and under construction including over 30 GW of power; c.17 million m3/day of desalination, water and wastewater treatment capacity; over 3,800 km of high-speed, monorail and metro, including the largest high-speed network under construction worldwide; and iconic social infrastructure projects such as the Grand Egyptian Museum.

In the U.S., through its subsidiaries Orascom Construction USA, The Weitz Company, EPI Power, and Contrack Watts, Orascom Construction builds on a 170-year legacy and is today highly active across data centers and aviation, with a track record of over 1.2 GW of data centers and more than thirty aviation projects.

Orascom Construction also develops and invests in concessions. The Group’s portfolio spans seawater and wastewater treatment, renewable energy, and logistics in the United Arab Emirates, Saudi Arabia, and Egypt, including 913 MW of wind farms and the largest operational wind farm in the Middle East and Africa.

Orascom Construction owns 50% of BESIX Group, one of Europe’s largest privately-owned contractors, with operations across construction, concessions and real estate across Europe, Middle East, Africa, and Australia. BESIX has a proven track record that includes Burj Khalifa, Zayed National Museum, and Guggenheim Abu Dhabi in the UAE and Oosterweel Link-Scheldt Tunnel in Belgium, and has an established portfolio of concessions in Europe and the UAE of over 20 years, including transportation and marine in Europe and water treatment, waste-to-energy and social infrastructure in the UAE.

Orascom Construction has a total backlog including its 50% share in BESIX of USD 13 billion.

The Group also owns a portfolio of subsidiaries across building materials, facility management, and equipment services.

Orascom Construction has consistently ranked among the world’s top contractors and is dual listed on the Abu Dhabi Securities Exchange (ADX) and the Egyptian Exchange (EGX).

Learn more at www.orascom.com. Follow Orascom Construction on LinkedIn.

CONTACT INVESTOR RELATIONS

Sarah Rajani CFA

Global Vice President Investor Relations and Communications

sarah.rajani@oci-global.com

www.oci-global.com

[1] The Company will withhold 15% Dutch dividend withholding tax (DWT) from the distribution of the Orascom Shares to OCI’s shareholders, to the extent the distribution is not made from qualifying capital reserves, unless a relief at source is available. For further information, see the convocation materials for the OCI EGM, which will be made available at: www.oci-global.com.

[2] Management estimate includes acquisitions, disposals, listings, bond issuances, equity injections, and project financings.

[3] Validated by KPMG; Total IRR in USD since formation of OCI SAE in March 1999 up until 31 October 2024.

[4] The Company will withhold 15% Dutch dividend withholding tax (DWT) from the distribution of the Orascom Shares to OCI’s shareholders, to the extent the distribution is not made from qualifying capital reserves, unless a relief at source is available. For further information, see the convocation materials for the EGM, which will be made available at: www.oci-global.com.

Continue Reading

-

US Justice Department accuses two Chinese men of trying to smuggle Nvidia chips – Reuters

- US Justice Department accuses two Chinese men of trying to smuggle Nvidia chips Reuters

- US busts China-linked AI chip smuggling ring worth $50 million lokmattimes.com

- Houston-area man pleads guilty to smuggling $160 million high-powered chips to China Houston Public Media

- Feds say Houston-linked ‘Operation Gatekeeper’ broke $160M A.I. chip smuggling pipeline to China FOX 26 Houston

- Sugar Land man pleads guilty to smuggling AI computer chips to China, first case of its kind Click2Houston

Continue Reading

-

Owning 46% shares,institutional owners seem interested in Fleetwood Limited (ASX:FWD),

-

Institutions’ substantial holdings in Fleetwood implies that they have significant influence over the company’s share price

-

A total of 9 investors have a majority stake in the company with 53% ownership

-

Insiders have been buying lately

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

Every investor in Fleetwood Limited (ASX:FWD) should be aware of the most powerful shareholder groups. And the group that holds the biggest piece of the pie are institutions with 46% ownership. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

Since institutional have access to huge amounts of capital, their market moves tend to receive a lot of scrutiny by retail or individual investors. As a result, a sizeable amount of institutional money invested in a firm is generally viewed as a positive attribute.

Let’s take a closer look to see what the different types of shareholders can tell us about Fleetwood.

Check out our latest analysis for Fleetwood

ASX:FWD Ownership Breakdown December 9th 2025 Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices.

We can see that Fleetwood does have institutional investors; and they hold a good portion of the company’s stock. This can indicate that the company has a certain degree of credibility in the investment community. However, it is best to be wary of relying on the supposed validation that comes with institutional investors. They too, get it wrong sometimes. When multiple institutions own a stock, there’s always a risk that they are in a ‘crowded trade’. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Fleetwood’s historic earnings and revenue below, but keep in mind there’s always more to the story.

ASX:FWD Earnings and Revenue Growth December 9th 2025 We note that hedge funds don’t have a meaningful investment in Fleetwood. Sandon Capital Investments Limited is currently the company’s largest shareholder with 9.0% of shares outstanding. With 8.3% and 7.0% of the shares outstanding respectively, Greg Tate and Paradice Investment Management Pty Ltd. are the second and third largest shareholders.

We also observed that the top 9 shareholders account for more than half of the share register, with a few smaller shareholders to balance the interests of the larger ones to a certain extent.

Continue Reading

-

-

Australia's central bank holds rates steady, warns of inflation risk – Reuters

- Australia’s central bank holds rates steady, warns of inflation risk Reuters

- Australian dollar braces for hawkish RBA, bond yields hit two-year high Business Recorder

- Reserve Bank holds interest rates amid warning on stubborn housing inflation realestate.com.au

- AUD/NZD slides to near 1.1440 as RBA holds OCR steady at 3.6%, as expected FXStreet

- The RBA decision highlights today’s Asia-Pacific calendar TradingView

Continue Reading

-

Australia central bank keeps rates at 3.6%, warns of inflation risk – Reuters

- Australia central bank keeps rates at 3.6%, warns of inflation risk Reuters

- Australian dollar braces for hawkish RBA, bond yields hit two-year high Business Recorder

- Reserve Bank makes final rate call for 2025 hrleader.com.au

- Reserve Bank holds interest rates amid warning on stubborn housing inflation realestate.com.au

- AUD/NZD slides to near 1.1440 as RBA holds OCR steady at 3.6%, as expected FXStreet

Continue Reading

-

China’s Li says tariff consequences increasingly evident

BEIJING, Dec 9 (Reuters) – China’s Premier Li Qiang said on Tuesday the “mutually destructive consequences of tariffs have become increasingly evident” over 2025, in remarks at a “1+10 Dialogue” including the heads of the IMF, World Trade Organization and World Bank.

Without naming U.S. President Donald Trump, China’s second-highest ranking official told the meeting in Beijing that greater effort was needed to reform global economic governance due to the trade barriers.

Sign up here.

China’s trade surplus topped $1 trillion for the first time in November, trade data showed on Monday, which economists say is linked to Trump’s tariffs diverting shipments from the world’s second-largest economy to other markets, putting pressure on manufacturing sectors in those economies.“Since the beginning of the year, the threat of tariffs has loomed over the global economy,” Li told the meeting, which also includes senior officials from the OECD and International Labour Organization.

Li also said artificial intelligence is becoming central to trade, highlighting models such as China’s DeepSeek as drivers of the global transformation of traditional industries and as catalysts for growth in new sectors, including smart robots and wearable devices.

Reporting by Joe Cash; Editing by Sam Holmes

Our Standards: The Thomson Reuters Trust Principles.

Continue Reading

-

Japan’s offshore wind sector: Down but not out

In August 2025, a consortium led by Mitsubishi Corporation announced its withdrawal from three offshore wind projects in Japan. The decision raised concerns about the viability of the country’s offshore wind sector, long viewed as a cornerstone of its renewable energy expansion. The stated cause — surging construction costs linked to inflation — is not unique to Mitsubishi; developers across Europe and elsewhere face the same challenge.

Yet it would be premature to conclude that offshore wind development in Japan has reached a dead end. Although developers are grappling with structural barriers, the government has begun reassessing its auction framework and implementing reforms that could make the next bidding round more attractive.

Japan’s wind energy plans

Japan’s 7th Strategic Energy Plan aims to increase the share of renewable energy in power generation from approximately 20% to 40%–50% by fiscal year (FY) 2040. Within this target, wind power is expected to rise from approximately 1% to between 4% and 8%, with offshore wind positioned as the centerpiece of this expansion. Japan added more offshore wind capacity in 2024 than ever before, albeit from a modest base, reaching 253.4 megawatts (MW) of operational offshore wind capacity. Meanwhile, onshore wind capacity stood at 5,330MW at the end of that year.

In 2020, Japan’s Ministry of Economy, Trade and Industry (METI) published its “Vision for Offshore Wind Power Industry,” aiming for 10 gigawatts (GW) of total wind capacity by 2030. METI began drafting a second version of the plan in March 2025. Meanwhile, the Japan Wind Power Association has outlined a longer-term vision to build 140GW of wind capacity by 2050, comprising 40GW onshore, 40GW fixed offshore, and 60GW floating offshore capacity.

Recent political developments in Japan are likely to affect the trajectory of its energy policy. The newly elected prime minister, Sanae Takaichi, has been a strong advocate for nuclear energy and has highlighted the risks of relying on foreign suppliers for conventional solar panels. While she has shown less resistance to offshore wind, she has emphasized a goal of achieving 100% energy self-sufficiency. Under her administration, Japan’s decarbonization strategy is expected to place greater emphasis on energy security and industrial competitiveness.

Mitsubishi’s winning bids and subsequent withdrawal

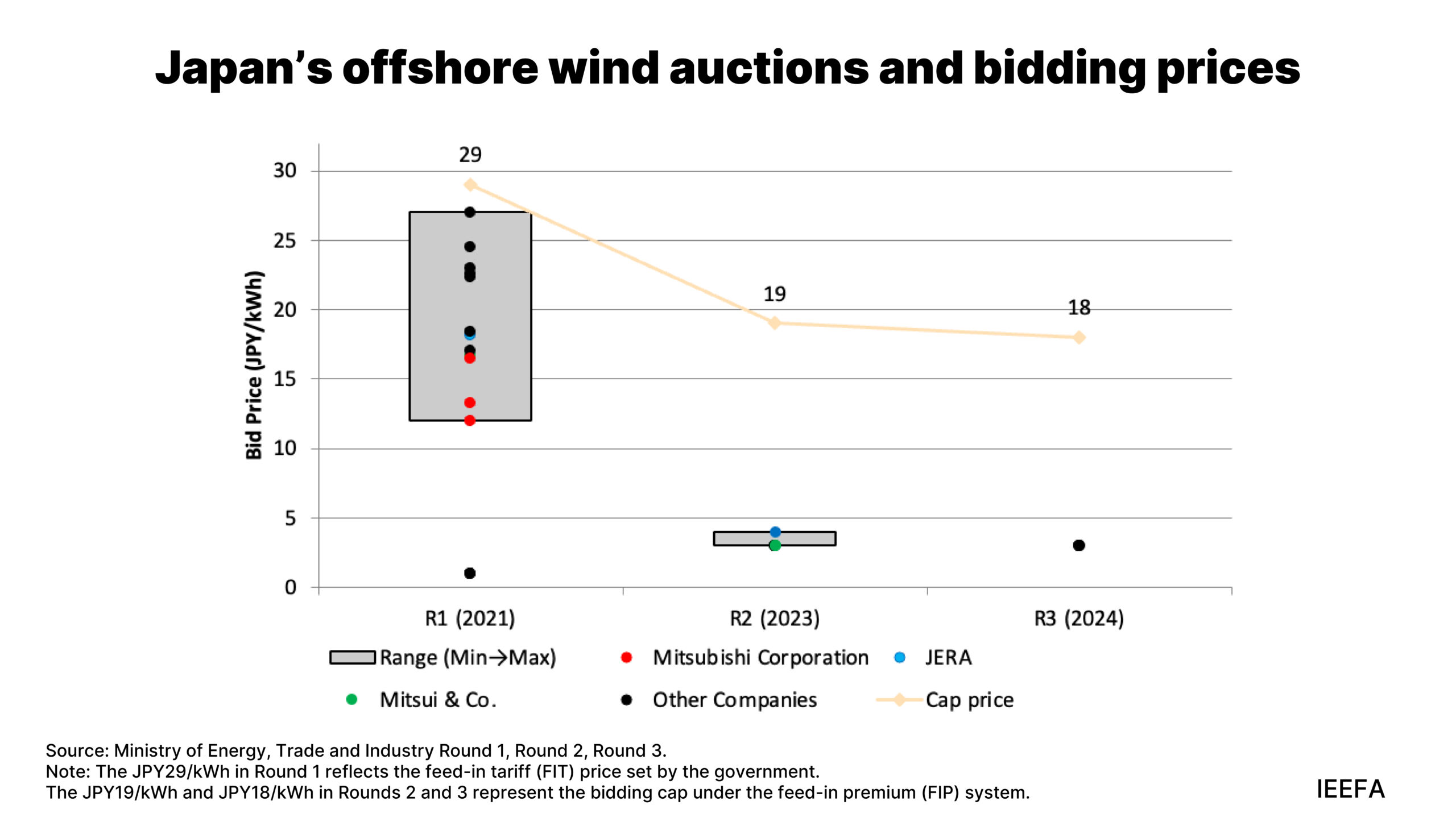

Mitsubishi’s withdrawal from three offshore wind projects reflects both company-specific missteps and broader structural issues in Japan’s offshore wind market. In 2021, Japan held its first offshore wind auction for three projects with a combined capacity of 1.7GW. Under the feed-in tariff (FIT) scheme, companies would compete for projects by submitting low-cost bids but would ultimately win contracts set at higher, predetermined fixed rates. The process enabled price discovery while also enhancing financial security for project backers.

In the first round, a Mitsubishi-led consortium won all three projects with a bidding price between JPY11.99 and JPY16.49 per kilowatt-hour (kWh), or USD10.85 cents per kilowatt-hour (¢/kWh) and USD14.8¢/kWh. This was far lower than the JPY29/kWh (USD26.1¢/kWh) ceiling price set by the government and the JPY17–JPY24.5/kWh (USD15.3¢/kWh to USD22.0¢/kWh) range from other bidders. Mitsubishi’s bid range was closer to that seen in more mature, established European markets than in an inaugural auction. These bids appeared competitive but left little buffer for cost inflation.

In the years following the auction, Mitsubishi’s project costs more than doubled, with total investment ballooning above JPY1 trillion (USD6.4 billion). The company announced a JPY52.2 billion (USD0.3 billion) impairment on the three offshore wind projects, exacerbated by inflation, global supply chain disruptions, yen depreciation, and rising turbine costs. In Japan, average construction costs for offshore wind projects were 20% higher in FY2024 than in FY2020, compared to an 8.5% increase in the cost of consumer goods. This is broadly consistent with trends in Europe, where capital costs increased by 18% between 2019 and 2024.

Factors constraining Japan’s offshore wind sector

Across the wind energy industry, all major segments — turbines, cables, foundations, and substations — have been affected by inflation, driven by rising raw material and energy prices, as well as persistently high shipping rates. Global equipment and materials prices have surged since 2022, particularly for turbines, subsea cables, monopiles, and substations, driving engineering, procurement, and construction (EPC) costs higher. For example, wind turbines have typically accounted for 30% of the capital expenditure (capex) required for Japanese fixed offshore wind projects in FY2025. However, turbine costs reportedly increased by 10%–15% between 2021 and 2023.

Monopile foundation costs, which typically account for approximately 8% of capex for Japanese wind projects, have been almost entirely sourced from Europe. European steel prices, the main cost driver for turbines and monopiles, surged by around 200% between late 2020 and mid-2022. Although global steel prices have since fallen to near-2019 levels, the decline in turbine costs has been slow. Shipping and installation expenses have also increased due to post-COVID supply chain bottlenecks. Transporting monopiles from Europe can cost around JPY300 million (USD1.9 million), underscoring Japan’s reliance on imports — a challenge that extends across its offshore wind supply chain.

By 2040, Japan aims to achieve over 65% local content across its entire offshore wind supply chain. Currently, however, the country lacks a domestic supplier for offshore wind turbines. Toshiba plans to establish a nacelle assembly line at its Yokohama plant in partnership with General Electric (GE), but production has not started yet. Mitsubishi Heavy Industries and Hitachi also previously pursued wind turbine manufacturing, but were unable to establish a sustained, large-scale domestic supply foundation. As a result, Japan’s offshore wind projects continue to rely heavily on imported turbines. Nevertheless, there are opportunities to substantially increase the proportion of wind farm costs sourced domestically, even in the absence of a full turbine manufacturing base.

Importantly, turbines now account for less than 30% of total offshore wind capex in Japan. The remaining 70% consists of balance-of-plant components — foundations, towers, cables, transmission systems, installation vessels, port upgrades, and operations — many of which align closely with Japan’s existing industrial strengths. The country already hosts globally competitive firms in specialty steel production, heavy fabrication, electrical equipment, shipbuilding, and marine logistics.

Therefore, what is lacking is not industrial capability but the effective mobilization of that capability. Irregular auction schedules and an unpredictable long-term project pipeline have prevented domestic industries from scaling or repositioning to meet offshore wind demand, reinforcing reliance on imported equipment, even when domestic alternatives exist.

Japan already forges the specialty steels used in offshore wind foundations and turbine towers. Despite this, developers continue to import these components from Europe. Hitachi, Toshiba, and Mitsubishi manufacture a large proportion of the transmission system components needed for both offshore and onshore portions of wind farm interconnections. The country also has a world-class shipbuilding industry, capable of fabricating vessels of all sizes and specialties, which is a critical requirement for offshore wind farms. These ships need crews, port facilities, and maintenance services, reinforcing the potential for domestic economic spillovers if offshore wind supply chains are localized.

Along with higher component costs, the weak yen and rising interest rates have increased import and capital financing costs. Since 2021, the yen has significantly weakened. On an annual-average basis, the exchange rate increased from 109.78 JPY/USD in 2021 to 151.50 in 2024 — a 38% depreciation. These currency fluctuations have inflated dollar-denominated equipment prices and amplified project financing costs. Moreover, Japanese short-term policy rates are at their highest level since 2008, with future hikes anticipated in 2026. Although lower financing costs, compared to those in the United States (US) and Europe, have been cited as an advantage for Japanese wind projects, recent increases in debt costs have eroded that benefit.

Additionally, regulatory and permitting barriers further increase overall project expenses. In Japan, it takes 6–8 years from the start of permitting to the commercial operation date for fixed-bottom offshore wind projects. By contrast, the European Union (EU) caps the permit-granting process at two years for offshore projects. Japan’s lengthy baseline lead time increases exposure to component price volatility, rising financing costs, and delays, making projects more costly and risk-prone by global standards.

Like Mitsubishi, other bidders in the third offshore wind auction would likely have faced the same inflationary challenges. However, this case highlights more than just the risks of aggressive bidding. To realize its offshore wind ambitions, Japan should address its high domestic costs and unfavorable auction rules that incentivize low bids.

Auction price comparisons: Japan vs. international benchmarks

Japan’s first offshore wind auction in 2021 highlighted the stark disparity between domestic and international prices. Bidding prices in Japan’s first round were between JPY11.99/kWh and JPY24.5/kWh. This was two or three times higher than international benchmarks, such as the United Kingdom’s (UK) 2021 Round 4 bid at GBP37.35 per megawatt-hour (MWhGBP37.35 per megawatt-hour (MWh) (around JPY7–8/kWh) or Germany and Taiwan’s Round 3.2 with zero-premium bids. A zero-premium bid refers to an auction scheme in which developers bid with a premium — defined in the support scheme as a subsidy — set at zero, and proceed with the project solely based on revenues linked to wholesale electricity market prices.

At first glance, Japan’s results appear uncompetitive. However, the higher ceiling prices set by the government reflected the country’s unique conditions rather than an intentional distortion. Japanese developers must pay for grid connections and seabed reinforcement, which are often covered by governments in Europe. Long permitting timelines and coordination with fisheries extend project risks, raising financing costs. The absence of inflation indexation forces bidders to price in uncertainty, while dependence on imported turbines exposes them to exchange-rate and shipping risks.

Japan’s high auction prices are the product of systemic design and cost burdens, not technological inefficiency. Recognizing these differences is essential to understanding why the country’s offshore wind auctions are more expensive compared to its global peers. It also underscores why recent government reforms aimed at correcting low-price competition and easing structural burdens will be critical for unlocking Japan’s true offshore wind potential.

Evolution of Japan’s offshore wind policy framework

The Japanese government has started amending its offshore wind policy framework in response to the issues revealed in Round 1 bidding. In January 2025, it revised core auction guidelines to address excessively low-price bidding and project delays. The new rules allow developers to reflect up to 40% of cost inflation in the electricity price between the auction and the start of construction. For projects allocated from Round 4 onwards, bid bonds for operational delays increase from JPY13,000 per kilowatt (kW) to JPY24,000/kW — double that of projects assigned from Rounds 1 to 3 — and are structured as phased penalties to discourage speculative bidding and ensure project completion. Scoring criteria have also shifted from a price-only evaluation to factor in feasibility and local contributions.

Moreover, in November 2025, the government announced seven measures to enhance the bankability and completion prospects of offshore wind projects. These include a provision that zero-premium projects in Rounds 2 and 3 will be allowed to participate in the Long-Term Decarbonization Power Source Auction, securing 20 years of capacity revenue. The price-adjustment mechanism will continue to reflect only future inflation. Developers may also revise key equipment, including turbines, in cases of supplier withdrawal or significant cost escalation. Additional measures include more flexible base port rules, “renewal in principle” for occupation permit extensions, improved valuation of renewable attributes, and integrated grid, port, and financial support for low-carbon investments.

Strengthening domestic supply chains

METI also aims to reinforce domestic supply chains through initiatives, such as the July 2025 memorandum of understanding with Vestas and Nippon Steel, to localize turbine component production. The government has also pledged to reauction the sites abandoned by Mitsubishi under these new rules.

The initial bidding rounds highlighted the cost risks associated with weak domestic supply chains. Japan could address both exchange rate impacts on wind farm costs and the need to localize the offshore wind supply chain by domestically sourcing steel, foundation and tower fabrication, and other key components in the balance of systems and services. Beyond the turbines themselves, these inputs and services account for 60% to 70% of total project expenses. Japan’s advanced steel production, fabrication, integration, project management, and logistics systems are well-suited to meet offshore wind demands. The country’s shipbuilding sector could also benefit from producing specialized vessels needed for offshore wind farm installation and maintenance. Additionally, Japan is home to leading global suppliers of key components for cabling and transmission system elements, especially high-voltage direct current (HVDC) transmission components. As the offshore wind auction market matures and scales, the advantages of onshoring or localizing a greater share of wind turbine manufacturing and assembly become increasingly clear.

Expanding the scope for offshore wind projects

In June 2025, the Japanese parliament passed a law allowing the installation of offshore wind farms in the country’s exclusive economic zone (EEZ). This is a significant development as it effectively expands the geographical scope for future auctions beyond Japan’s territorial waters, opening vast new areas for large-scale offshore wind development. With one of the world’s sixth-largest EEZs, Japan could now access deeper and windier sites with higher capacity factors and lower seasonal variability, giving new momentum to its long-term offshore wind ambitions.

The government is considering reauctioning the three sites in Akita and Chiba that were awarded in Round 1, following Mitsubishi’s withdrawal from the projects.

Simultaneously, attention is turning to the upcoming Round 4 auction. Two new offshore areas near Matsumae and Hiyama in Hokkaido have been designated as promotion zones, and a public tender is expected for these sites. However, the government postponed the launch of Round 4, initially scheduled for 14 October 2025. The delay is intended to provide time to assess the reasons behind developers’ withdrawal from the three Round 1 sites and to establish conditions to ensure offshore wind investments can reach completion. Therefore, the postponement is not a setback, but a constructive step toward refining the auction framework and fostering a more sustainable market environment.

Optimistic outlook for the sector

Despite these headwinds, other renewable energy developers remain optimistic about the long-term outlook for the sector. At a recent industry event, Masato Yamada, Senior Vice President at JERA Nex bp Japan Ltd., remarked, “There’s a perception that offshore wind power is dead, but the initiative hasn’t even truly begun.” Regarding the company’s Round 2 project off the coast of Akita, he further noted that withdrawing would result in greater losses, making continued development the rational choice. His comments underscore that, despite recent setbacks, developers still have strong incentives to move projects forward.

In fact, not all projects are stalled. Round 2 developments are progressing despite cost headwinds: Mitsui & Co. has selected its EPC contractor and plans to begin onshore construction in October 2025, Tohoku Electric is moving ahead with its 615MW Aomori project, and the Oga–Katagami–Akita consortium led by JERA Nex bp Japan has established a local headquarters with operations targeted for June 2028.

Round 3 developments are also progressing in line with planned construction and operation timelines. The consortium led by JERA is preparing fisheries impact assessments for its project off the southern coast of Aomori in the Sea of Japan, while Marubeni’s project off Yuza, Yamagata Prefecture, is moving forward on a similar schedule. Both projects target commercial operation in June 2030 and plan to use Siemens turbines. In June 2025, METI and Siemens Gamesa established a cooperation framework to discuss and promote the development of a wind turbine supply chain for the Japanese market and overseas expansion. Together, these efforts signal growing momentum toward strengthening Japan’s offshore wind industry through international collaboration and supply chain development.

These examples demonstrate that, alongside policy reform, tangible progress continues, highlighting that Japan’s offshore wind sector may be down — but is far from out.

Yet limitations remain

Despite the visible progress in Round 2 and the reforms introduced, Japan’s offshore wind developers still face structural headwinds. The latest measures — including the provision of 20 years of capacity revenues for zero-premium projects in Rounds 2 and 3, the allowance of turbine substitutions in the event of supplier withdrawal, and the shift toward “renewal in principle” for occupation permit extensions — are crucial mechanisms to reduce cancellation risks and improve financial visibility. However, these relief measures apply only to Rounds 2 and 3; from Round 4 onward, developers will return to a highly competitive environment.

At the same time, many of the fundamental bottlenecks identified by industry and in the Global Wind Energy Council’s (GWEC) recent white paper remain unresolved. These include:

(1) Insufficient inflation protection that does not compensate for past cost escalation, in stark contrast to the UK’s fully Consumer Price Index (CPI)-adjusted Contract for Difference (CfD)

(2) An underdeveloped corporate power purchase agreement (PPA) market and the absence of credit-guarantee schemes that constrain access to higher-priced offtake

(3) A lack of compensation mechanisms for curtailment risk

(4) The absence of a strategic offshore transmission plan and persistently high grid-connection costs

(5) Shortages of domestic ports and installation vessels, which continue to force developers to rely on costly foreign charters

(6) Regulatory inconsistencies — such as the implicit application of building standards — that prolong certification and permitting timelines, delaying revenue generation

Unless these structural issues are resolved, development costs will remain elevated, permitting will remain protracted, offtake options will stay limited, and incentives for meaningful domestic supply chain investment will continue to be weak. Addressing these challenges would establish a solid foundation for the long-term growth and stability of the offshore wind market and send a strong signal to domestic manufacturers to invest in localizing supply chains. Mitsubishi’s withdrawal showed that the difficulty was not only aggressive bidding but also weaknesses in the auction framework. With further institutional improvements, Japan can still realize its offshore wind potential. Accelerating climate policy and innovation in this sector will be essential to sustaining the country’s future competitiveness.

Continue Reading