- Buffett’s Berkshire Cash Hits $382 Billion, Earnings Soar Bloomberg

- Berkshire Hathaway’s cash reserves reach a record $381.67 billion Bitget

- AP Business SummaryBrief at 1:28 p.m. EDT The Joplin Globe

- Legendary investor Warren Buffett marks 3 straight years as a net seller of stocks with a new CEO about to take charge at Berkshire Yahoo Finance

- Berkshire Hathaway Q3 results: Profit jumps 17% to $30.8 bn as Buffett readies exit; Greg Abel set to tak The Times of India

Category: 3. Business

-

Buffett’s Berkshire Cash Hits $382 Billion, Earnings Soar – Bloomberg

-

Old cars meet new in Pall Mall

More than 130 cars have been admired on London’s Pall Mall as St James’s Motoring Spectacle returned to the capital.

Organised by the Royal Automobile Club with the permission of Westminster City Council, the event is seen as the curtain-raiser to the following day’s London to Brighton Car Run.

The St James’s Spectacle showcased vehicles from the birth of motoring to the most recent hypercars.

About 75 pre-1905 vehicles took part – and they, with hundreds of others, will join Sunday’s run to Brighton.

Pedal power was also celebrated, with a collection spanning veteran bicycles and early motorcycles through to modern electric bikes.

Continue Reading

-

How S&P’s New Index Could Be a Game Changer for Your Crypto Investments

One of the main raps against cryptocurrency has been that it is not a “mainstream” investment asset. However, the recent announcement of a new crypto-related index created by S&P Dow Jones Indices is just the latest in a string of headlines pushing crypto toward wide-stream acceptance.

Read More: I Asked ChatGPT To Explain Crypto Like I’m 12 — Here’s What It Said

Find Out: 9 Low-Effort Ways To Make Passive Income (You Can Start This Week)

Here’s a look at what’s going to be in the index, how it might boost crypto in general, and whether or not it might be a fit for your portfolio.

According to S&P Global, the creator of the new S&P Digital Markets 50 Index, “The index is designed to track a wide range of companies and digital assets connected to the crypto ecosystem, combining cryptocurrencies and publicly traded crypto-linked equities into one index.”

What this means is that unlike some other indexes that merely track specific cryptocurrencies, this index is meant to encompass the entire crypto ecosystem. In addition to individual coins and tokens, the S&P Digital Markets 50 Index will include stocks of companies that are somehow related to crypto. Specifically, the index “will include 35 companies involved in digital asset operations, infrastructure providers, financial services, blockchain applications and supporting technologies, but will also be combined with 15 cryptocurrencies selected from the S&P Cryptocurrency Broad Digital Market Index.”

Note that at the present time, the S&P Digital Markets 50 is just an index, not an investable exchange-traded fund (ETF). However, later this year, fintech firm Dinari plans to offer investible “dShares” based on the index in conjunction with S&P Global. Additionally, as The Motley Fool noted, this index could lead to the introduction of new ETFs or mutual funds.

Check Out: 3 Reasons Bitcoin Is ‘Digital Gold,’ Says Investing Expert

Anything that is seen to legitimize and bring cryptocurrency into the mainstream is seen as a good thing for the overall crypto market. When investors feel more confident that crypto isn’t simply the wild west of the investment world, they’ll be more likely to invest themselves. An increase in the number of investors could both drive crypto prices higher and reduce volatility in the sector.

Investing in a crypto-based index can provide two additional major benefits.

First, it allows investors access to a relatively diversified portfolio with a single purchase. Although not a wholly diversified portfolio, as all of the investments will consist of crypto and crypto-related securities, you’d be owning 50 different investments instead of putting all your money into just one.

Continue Reading

-

Berkshire Hathaway’s profits rise 17% as Buffett prepares to step down

OMAHA, Neb. — The profits of Warren Buffett’s company improved 17% thanks to a relatively mild hurricane season and more paper investment gains this year as Berkshire Hathaway continues to prepare for the legendary 95-year-old investor to relinquish the CEO title in January.

But last month’s $9.7 billion investment in OxyChem won’t do much to diminish the $381.7 billion cash pile that Berkshire was sitting on at the end of September even though it is the biggest deal the company has made in years.

The biggest thing on most investors’ minds right now is that Buffett Vice Chair Greg Abel is set to succeed him as CEO in January, although Buffett will remain chairman at Berkshire. The Class A stock is well off its peak of $812,855, set just before Buffett surprised shareholders at the annual meeting in May by announcing he will step back. It closed Friday at $715,740, but Berkshire still didn’t buy back any of its own stock in the quarter, which suggests Buffett thinks it is still overvalued.

CFRA Research analyst Cathy Seifert said she expects investors will clamor for more details from Berkshire after Abel takes over, and that calls for the company to finally pay a dividend if it can’t find better uses for all that cash will also grow louder. But with Buffett remaining chairman there may not be any immediate changes.

“The lack of discussion and disclosure — I think has a lot of the investment community frustrated,” Seifert said. Berkshire has never had public or investor relations departments, and the company skips the quarterly investor calls that nearly every public company holds. Buffett has long said he prefers to share results with every investor at the same time, on Saturdays, and give them the weekend to digest the results before the markets reopen.

Berkshire said Saturday that it earned $30.796 billion, or $21,413 per Class A share, in the quarter. That’s up from last year’s $26.251 billion, or $18,272 per A share.

But those bottom-line figures are always distorted by the current value of Berkshire’s massive investment portfolio and any stock sales, which this year added $17.3 billion to the company’s profits.

That’s why Buffett has long recommended that investors pay more attention to Berkshire’s operating earnings to get a sense of how its many operating companies are performing, including well-known insurers like Geico, BNSF railroad, several major utilities and an assortment of manufacturing and retail companies.

On that measure, Berkshire’s operating profit jumped to $13.485 billion, or $9376.15 per Class A share, thanks to a strong rebound in its insurance companies. A year ago, Berkshire reported operating earnings of $10.09 billion, or $7,023.01 per Class A share.

The four analysts surveyed by FactSet Research predicted Berkshire would report operating earnings of $8,573.50 per Class A share.

Berkshire said fewer catastrophic losses from hurricanes this year compared to when Hurricane Helene ravaged the southeast a year ago helped its insurance underwriting profit jump $1.6 billion to $2.369 billion. The bottom line was also helped by $331 million in gains on debt held in foreign currencies this year, compared to a $1.1 billion loss on those holdings a year ago.

Most of Berkshire’s other companies performed well in the quarter although profits did decline nearly 9% at its utilities to $1.489 billion.

Continue Reading

-

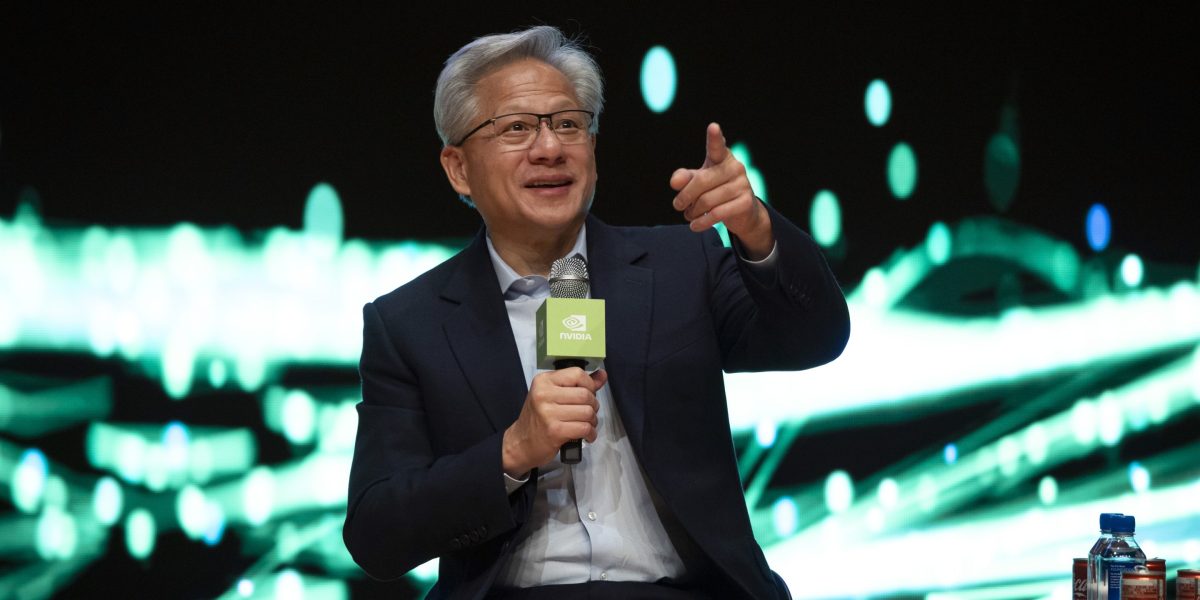

Nvidia chief still hopes to sell Blackwell chips to China

Nvidia Corp. Chief Executive Officer Jensen Huang still hopes to sell chips from the company’s Blackwell lineup to customers in China, though he has no current plans to do so, he told reporters Friday.

Asked whether Nvidia intends to sell AI accelerators from that family of products in the Asian country, the tech chief said, “I don’t know. I hope so someday.”

Huang’s comments came a day after US President Donald Trump said he didn’t discuss the prospect of Blackwell chip sales in a meeting with Chinese counterpart Xi Jinping, despite saying earlier that he would do so. US Trade Representative Jamieson Greer, asked whether Blackwell chip sales to China would be discussed more going forward, said “I don’t think that’s on the table right now.”

Huang, speaking Friday in South Korea, expressed optimism that might change. “No decisions have been made, and we’ll see how it turns out,” said Huang, 62, of Nvidia’s Blackwell export plans. “I hope it turns out well.” The Nvidia chief said earlier this week that the company hasn’t applied for Washington’s permission to sell Blackwell chips to China, permits that are required under export controls first imposed in 2022.

Read More: Trump Says Nvidia Chip Talks With Xi Didn’t Cover Blackwell

The Blackwell family of chips is Nvidia’s latest generation of artificial intelligence semiconductors and the industrial standard for developing and running large language models like OpenAI’s ChatGPT. The processors have capabilities that far surpass those of semiconductors that Washington effectively banned from export to China several years ago, as well as anything that’s currently available from Chinese competitors like Huawei Technologies Co.

Selling those products to China, as Huang hopes to do, would require a dramatic departure from the Trump administration’s stated approach to the tech competition between the world’s two largest economies. Still, the president had put it on the table. Trump said months ago that he’d be open to allowing China shipments of an unspecified, downgraded Blackwell chip. Ahead of his meeting with Xi, Trump said he’d discuss the “super duper” Blackwell accelerators with the Chinese leader — remarks that helped make Nvidia the first $5 trillion business by market value.

But while Trump and Xi did discuss Nvidia’s access to China in general, Trump said after the meeting, those talks did not touch on Blackwell chip approvals: “We’re not talking about the Blackwell,” Trump told reporters aboard Air Force One. “That just came out yesterday.”

Back in Washington, China hawks breathed a sigh of relief. Many US officials had worried that Trump, in an effort to reach a broader trade deal with Beijing, might give away what they consider to be the country’s strongest technological asset — and one with significant national security implications. Concern about Blackwell chip sales to the Asian country is one of the primary motivations behind a bipartisan congressional measure that could have major implications for Huang’s hopes for the China market.

The legislation, an earlier version of which has already passed the Senate, would require chipmakers like Nvidia to prioritize American customers before selling chips to buyers in arms-embargoed countries, including China. Hours after Trump and Xi concluded their meeting, lawmakers introduced the highly-anticipated bill to the US House of Representatives.

One congressional staffer, who requested not to be identified, described a sense of uncertainty akin to a fog of war when asked how Trump’s stance on Blackwell chips was playing on Capitol Hill.

Read More: AI Chip Export Controls Backed by House After Trump-Xi Talks

Nvidia has criticized trade restrictions as hamstringing US competitiveness and lobbied aggressively against chip export controls more broadly. “I think it’s really good for America and it’s really good for China that Nvidia could participate in the Chinese market,” Huang said Friday. Nvidia’s argument is that restricting Chinese AI developers from using American chips will only push them toward domestic alternatives.

To be sure, participating in China would also be really good for Nvidia: the world’s most valuable company wrote down billions of dollars in revenue earlier this year when Trump’s team restricted sales of a less-advanced processor called the H20. Washington later reversed course and greenlit H20 chip shipments, but Beijing has discouraged Chinese companies from using those accelerators.

Trump said Thursday that Nvidia and the Chinese government will have to keep talking about the chipmaker’s access to the Asian nation’s market, which is the world’s biggest for semiconductors. Huang, though, said the topic didn’t come up during his meeting Friday with Ren Hongbin, Chairman of the China Council for the Promotion of International Trade.

“We were just talking mostly about enjoying each other’s company,” Huang said.

Continue Reading

-

Barnsley’s Mr Kipling bakery to be powered by solar farm

Premier Foods

Premier FoodsMr Kipling cakes are produced at Carlton Bakery in Barnsley, South Yorkshire The bakery which produces Mr Kipling cakes and pies will soon be powered by the sun thanks to a £2.1m solar farm installed at the site in South Yorkshire.

The 2.2mw solar farm has been installed on 2.9 hectares (7.2 acres) of land at Premier Foods’ Carlton Bakery in Barnsley.

Once it becomes fully operational later this month, it will power three-quarters of the factory’s energy, from cake mixers to office lighting, the company said.

Nick Brown, ESG Director at Premier Foods, said: “By generating more of our energy needs on site, we’re not only reducing our carbon footprint but making our operations even more resilient.”

He said when the bakery opened in the 1970s it was the largest purpose-built bakery in the world, and it remains the biggest bakery in the UK.

Mr Brown added: “It’s also positive that the solar farm has the capability to potentially export electricity back into the local electricity grid, when we are producing more electricity than we need.”

The solar project is expected to reduce the factory’s carbon emissions by 468 tonnes per year and deliver savings in annual energy costs, something it said will support the resilience of the business which is a key local employer.

Premier Foods

Premier FoodsThe solar farm has been installed on 2.9 hectares (7.2 acres) of land The Carlton Bakery is one of the region’s largest food production facilities, employing up to 1,000 people at peak production.

Steve Morton, Manufacturing Director and Factory General Manager at Carlton Bakery, added: “The whole team is excited to see the solar panels go live. Carlton has been part of the community for over 50 years, and over that time the site has changed a great deal – this is the next really exciting step in its story.”

Premier Foods has rolled out solar power at its other manufacturing sites, including at its Stoke-on-Trent bakery, and is investing in another project in Ashford, Kent.

Continue Reading

-

Evaluating Valuation After New Growth-Focused Leadership Appointments

Rezolve AI (NasdaqGM:RZLV) is shaking up its executive team, with Arthur Yao stepping into the dual role of Chief Operating and Financial Officer. Several new key leaders are also joining the company’s top ranks.

See our latest analysis for Rezolve AI.

Momentum has been anything but steady for Rezolve AI this year. While the 90-day share price return stands at 46.4%, driven by new executive appointments and a push to court investors at major tech conferences, the company’s 1-year total shareholder return remains negative at -4.7%. This indicates that recent optimism is only beginning to challenge a much longer period of underperformance.

If leadership shakeups and newfound momentum have you looking for more opportunities, now is a perfect time to broaden your search and discover fast growing stocks with high insider ownership

With shares still trading at less than half of analyst targets, but recent gains challenging a sluggish year, investors have to decide whether Rezolve AI is a bargain set for a turnaround or if the market has already priced in the company’s growth plans.

The SWS DCF model points to a fair value of $8.63 for Rezolve AI, suggesting the stock is trading markedly below intrinsic value with its last close at $4.29.

The DCF model estimates a company’s true worth by projecting all future cash flows and discounting them back to today’s value. For Rezolve AI, this approach is especially relevant as the company focuses on aggressive revenue growth in the burgeoning AI software space, despite ongoing losses.

This means the DCF estimate emphasizes future expansion and cash potential rather than current profitability. For investors, this model invites a deeper look at whether the revenue surge can bridge the gap toward eventual profitability in a volatile sector.

Look into how the SWS DCF model arrives at its fair value.

Result: DCF Fair value of $8.63 (UNDERVALUED)

However, persistent net losses and volatile short-term returns still loom as risks that could quickly test investor confidence in Rezolve AI’s turnaround story.

Find out about the key risks to this Rezolve AI narrative.

If you want to dig into the numbers yourself or think you have a different perspective, you can easily build your own story around Rezolve AI in just a few minutes. Do it your way

A great starting point for your Rezolve AI research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Continue Reading

-

Credit Fraud Fears Loom After BlackRock’s HPS Zeros Out Bad Loan – Bloomberg

- Credit Fraud Fears Loom After BlackRock’s HPS Zeros Out Bad Loan Bloomberg

- Explained: How an Indian-origin entrepreneur ‘borrowed’ $500 million from the world’s biggest asset manag The Times of India

- Who is Bankim Brahmbhatt? The Indian-origin man allegedly behind $500 million loan fraud in US Tribune India

- BlackRock thought it backed a telecom empire, what they got was a $500 mn ghost story Business Today

- BlackRock loses ₹4,435 crore to ‘breathtaking fraud’ by Indian-origin CEO | ‘Brahmbhatt disputes the allegations of fraud’ | Inshorts Inshorts

Continue Reading

-

Chubu Steel Plate (TSE:5461) Loss Reduction Challenges Persistent Dividend Concerns

Chubu Steel Plate (TSE:5461) continues to operate at a loss, as evidenced by its negative net profit margin, but has managed to trim its losses at an annual rate of 6.9% over the past five years. Shares currently trade at ¥1,981, which stands well below the estimated fair value of ¥14,047.73. However, the price-to-sales ratio of 1.2x remains well above both industry and peer averages of 0.4x. Investors are assessing whether the company’s progress on narrowing losses and offering perceived value will outweigh persistent concerns about unprofitability and dividend sustainability.

See our full analysis for Chubu Steel Plate.

The next section puts these earnings figures side by side with the most widely held market narratives, highlighting where the data supports the stories and where it raises new questions.

Curious how numbers become stories that shape markets? Explore Community Narratives

TSE:5461 Revenue & Expenses Breakdown as at Nov 2025 -

Chubu Steel Plate has managed to narrow its losses at a rate of 6.9% per year over the last five years, directly addressing the company’s long-standing unprofitability.

-

The prevailing market view notes this steady pace of improvement could gradually restore investor confidence if it holds.

-

However, with no return to positive net margins in sight, the central debate is whether the ongoing reductions can meaningfully close the gap before sector headwinds offset these advances.

-

Investors watching the loss reduction trend will want evidence of a real pivot toward profitability, not just smaller annual deficits.

-

-

The EDGAR summary lists dividend sustainability as the main risk, raising questions about how long dividends can be supported while the business stays unprofitable.

-

The prevailing market view points out that ongoing losses put dividend coverage under pressure.

-

With no near-term sign of a profit turnaround, bulls hoping for consistent payouts could be caught off guard if reductions or suspensions become necessary.

-

This makes the dividend picture a key test case for management’s balancing of investor promises versus financial reality.

-

-

The current share price of ¥1,981 trades at a deep discount to the DCF fair value estimate of ¥14,047.73, but at a price-to-sales ratio of 1.2x, it still commands a premium compared to the 0.4x peer and industry averages.

-

Prevailing market analysis highlights this valuation tension:

-

Some investors may see the wide gap to fair value as a tempting entry point for an eventual turnaround, especially if the loss reduction trend accelerates.

-

Others note the company’s high price-to-sales multiple compared to peers sets a high bar, suggesting further downside unless profitability improves materially.

-

Continue Reading

-

-

The Bull Case For Block (SQ) Could Change Following ARK Invest’s $30.9M Share Purchase and Bitcoin Push

-

Earlier this week, ARK Invest purchased over US$30.9 million worth of Block Inc. shares across three exchange-traded funds, including ARKK, ARKW, and ARKF, highlighting continued interest among institutional investors.

-

This investment comes as Block accelerates its rollout of integrated bitcoin solutions for merchants, further cementing its role at the intersection of digital payments and cryptocurrency adoption.

-

We’ll explore how ARK Invest’s expanded position in Block underscores confidence in the company’s advancing crypto and payments ecosystem.

The latest GPUs need a type of rare earth metal called Terbium and there are only 37 companies in the world exploring or producing it. Find the list for free.

To own Block shares, you need to believe in the long-term relevance of its two-sided payments and banking ecosystem, built around Cash App and Square, especially as digital finance and bitcoin adoption expand. ARK Invest’s sizable US$30.9 million purchase showcases institutional optimism but does not materially change the core risk: Block’s earnings remain highly sensitive to bitcoin-related revenue fluctuations and ongoing competitive threats in peer-to-peer payments, which may be amplified or mitigated in the near term by broader crypto trends.

The most relevant recent announcement is the rollout of Square’s new integrated bitcoin payments solution for merchants, making it easier for businesses to seamlessly accept, hold, and convert bitcoin through Square’s point-of-sale system. This initiative directly aligns with Block’s push to deepen cryptocurrency integration, one of its central growth catalysts, by strengthening its merchant platform and reinforcing its role as a bridge between digital asset adoption and real-world payments.

But while interest in bitcoin solutions is growing, investors should pay careful attention to the risk that…

Read the full narrative on Block (it’s free!)

Block’s outlook anticipates $32.8 billion in revenue and $2.4 billion in earnings by 2028. This is based on a projected 11.3% annual revenue growth rate, but earnings are forecast to decrease by $0.6 billion from the current $3.0 billion.

Uncover how Block’s forecasts yield a $88.40 fair value, a 16% upside to its current price.

XYZ Community Fair Values as at Nov 2025 Seventeen members of the Simply Wall St Community estimate Block’s fair value between US$60.37 and US$104, showing a wide range of outlooks. With Block’s ongoing integration of bitcoin payments for merchants, this diversity hints at how opinions can differ around the business’s exposure to crypto volatility, open these alternative perspectives to understand what could drive future results.

Continue Reading

-