- AI Ignites the Return of Bezos the Inventor The Wall Street Journal

- Jeff Bezos Creates A.I. Start-Up Where He Will Be Co-Chief Executive The New York Times

- Bezos is back in startup mode, Amazon gets weird again, and the great old-car tech retrofit debate GeekWire

- AI Insider’s Week in Review: Bezos Joins Project Prometheus, OpenAI’s Pressures, TikTok’s Content Controls & Nvidia’s Record Q3, Plus the Latest Funding Rounds AI Insider

- Who is Vik Bajaj, who shares CEO title with Jeff Bezos in $6.2 billion AI startup Project Prometheus Times of India

Category: 3. Business

-

AI Ignites the Return of Bezos the Inventor – The Wall Street Journal

-

X rolls out location tool, unmasks fake Gaza influencer network

Social media platform X (formerly Twitter) has quietly introduced a feature in recent days that publicly displays key background information about user accounts. The tool adds a small button on profile pages that reveals the country or region where an account is based, how many times the user has changed their handle, when the account was created and where the app was originally installed, making previously hidden information accessible to all users.

A platform long known for allowing people to craft alternate identities and adopt personas from across the world abruptly lifted the curtain — and a sprawling ecosystem of fabricated accounts was exposed.

Fake ‘Gaza influencers’ uncovered

Nikita Bier, X’s head of product, signaled in October that the company planned to roll out the feature. At the time, it appeared to be a routine anti-spam update. Once the feature went live and users began clicking the “About this account” button, however, the scope of the fraud became clear.

Users discovered a network of accounts posing as Palestinians in Gaza who claimed to be reporting under bombardment and sharing emotional personal stories. Many were not based in Gaza at all. Some accounts shut down almost immediately after their listed locations were exposed.

One account that described its owner as a witness in Rafah “living under airstrikes” was shown to be posting from Afghanistan. A supposed nurse in Khan Younis turned out to be based in Pakistan. A man claiming to be a father of six in a displacement camp was based in Bangladesh. A “poet from Deir al-Balah writing by candlelight” was located in Russia.

The revelations went far beyond a few isolated cases. Entire bot farms appeared to be operating for months. Users posing as “North Gaza survivors” were actually in Pakistan. Self-described “Rafah residents” were in Indonesia. Accounts claiming to be members of Hamas’s Nukhba unit uploaded videos from Malaysia. Even fake profiles presenting themselves as IDF soldiers — “officers,” “snipers” and “reservists” supposedly operating in Gaza — were traced to London.

Some users continued to insist they were in Gaza despite the contradiction with their displayed location. In one prominent case, a user named Moatasem Al-Daloul posted a video of himself walking through what he said were destroyed homes in the Gaza Strip. It was not immediately possible to verify whether the video was authentic or had been filmed against an artificial background. Grok, X’s built-in artificial intelligence assistant, indicated that the platform’s displayed geographic data was accurate.

A push for transparency

The new feature allows users to choose whether to show their country or a more general region, similar to an option long available on Instagram. On X, however, the information is more prominent and cannot be hidden once enabled.

According to foreign media reports, code analysts have found evidence that X is preparing another tool that would alert users when an account attempts to disguise its true location with a VPN. If implemented, it could make remaining forms of manipulation on the platform far more difficult.

The changes raise broader questions about the future of online discourse. What happens when anonymity erodes and accounts that positioned themselves as eyewitnesses to conflict are revealed to be young people around the world with no connection to the events they describe? And what does this mean for social networks and their influence on political and social narratives shaping the lives of hundreds of millions of people?

Continue Reading

-

Why Are Analyst Forecasts for Blue Bird (BLBD) Shaping Investor Expectations Ahead of Earnings Day?

-

Blue Bird is preparing to report its quarterly earnings after the bell on November 24, 2025, with analysts forecasting earnings per share of $1.00 and steady revenue growth, reflecting strong performance within the school bus and heavy transportation equipment sector.

-

Recent positive analyst commentary and resilient financial metrics have fueled optimism among investors ahead of the earnings announcement, with many expecting the company to maintain its leadership position in revenue growth and profitability.

-

We’ll examine how analyst confidence and heightened anticipation for Blue Bird’s earnings announcement could influence its investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer’s.

To be a shareholder in Blue Bird, you need to believe in the ongoing shift toward cleaner transportation, policy-driven funding for electric vehicles, and efficient bus manufacturing. The company’s latest news reflects strong analyst confidence, but these positive signals may not materially change the fact that near-term performance remains highly sensitive to changes in government incentive programs, potential reductions or delays in funding could still impact results significantly.

Among recent developments, Blue Bird’s announcement of a $100 million buyback program, active through 2028, stands out as particularly relevant. While this move reinforces the management’s conviction in the company’s long-term value, the upcoming earnings announcement and any updates on public funding remain the main catalysts and risk factors shaping the outlook in the short run.

But on the other hand, if funding priorities shift or incentive programs are scaled back, investors should be aware of …

Read the full narrative on Blue Bird (it’s free!)

Blue Bird’s narrative projects $1.6 billion revenue and $152.3 million earnings by 2028. This requires 4.0% yearly revenue growth and a $36.4 million earnings increase from $115.9 million today.

Uncover how Blue Bird’s forecasts yield a $62.38 fair value, a 16% upside to its current price.

BLBD Community Fair Values as at Nov 2025 Three private investors in the Simply Wall St Community estimate Blue Bird’s fair value between US$62.38 and US$94.57 per share. While many are focused on long-term growth from policy incentives, you can explore a full spectrum of opinion about what drives this company’s opportunity and risk right now.

Explore 3 other fair value estimates on Blue Bird – why the stock might be worth just $62.38!

Continue Reading

-

-

Exploring Mercedes-Benz (XTRA:MBG) Valuation After Recent Share Price Gains

Mercedes-Benz Group (XTRA:MBG) shares closed at €57.02, with returns over the past month showing a 7% gain. Investors watching the automaker may be weighing recent performance against longer-term growth, including an 18% total return over the past year.

See our latest analysis for Mercedes-Benz Group.

With a recent 7% 1-month share price return, Mercedes-Benz Group is showing signs of positive momentum after a steady stretch. This is supported by an 18.5% total shareholder return over the past year, suggesting that many investors see long-term growth potential building for the storied automaker.

If the auto sector’s momentum has your attention, there are plenty of opportunities to discover among global peers. See the full list for free.

But with shares trading roughly 22% below estimated intrinsic value and still trailing analyst targets, investors may wonder whether the market is overlooking Mercedes-Benz Group’s potential or if future growth is already reflected in today’s price.

The latest consensus narrative points to Mercedes-Benz Group trading below its estimated fair value, with analysts expecting modest upside beyond the current price. This sets the stage for a forward-looking view shaped by emerging industry catalysts and premium segment opportunities.

Expansion into electric vehicles, digital platforms, and advanced in-car technologies is expected to support premium pricing, recurring revenues, and long-term earnings growth. Operational efficiency, supply chain optimization, and sustainability initiatives aim to strengthen cost resilience, net margins, and adaptability to shifting industry dynamics.

Read the complete narrative.

Curious about the hidden logic behind that valuation? Find out which bold revenue, margin, and growth forecasts analysts are betting on to justify their price target. The real story is in the details analysts used to shape this fair value. Explore the full breakdown and see what sets this forecast apart.

Result: Fair Value of €60.96 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, persistent trade tensions and weaker Chinese demand remain key risks that could quickly shift the current outlook for Mercedes-Benz Group.

Find out about the key risks to this Mercedes-Benz Group narrative.

If you have a different perspective or want to dig deeper into the numbers, you can shape your own outlook and narrative in just a few minutes. Do it your way

A great starting point for your Mercedes-Benz Group research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Continue Reading

-

What OpenAI Did When ChatGPT Users Lost Touch With Reality – The New York Times

- What OpenAI Did When ChatGPT Users Lost Touch With Reality The New York Times

- ‘A world-saving mission’: Ontario man alleges ChatGPT drove him to psychosis CTV News

- Making Chatbots Safe For Suicidal Patients Psychiatric Times

- Suspicious Minds Podcast vocal.media

- AI-induced psychosis: the danger of humans and machines hallucinating together The Conversation

Continue Reading

-

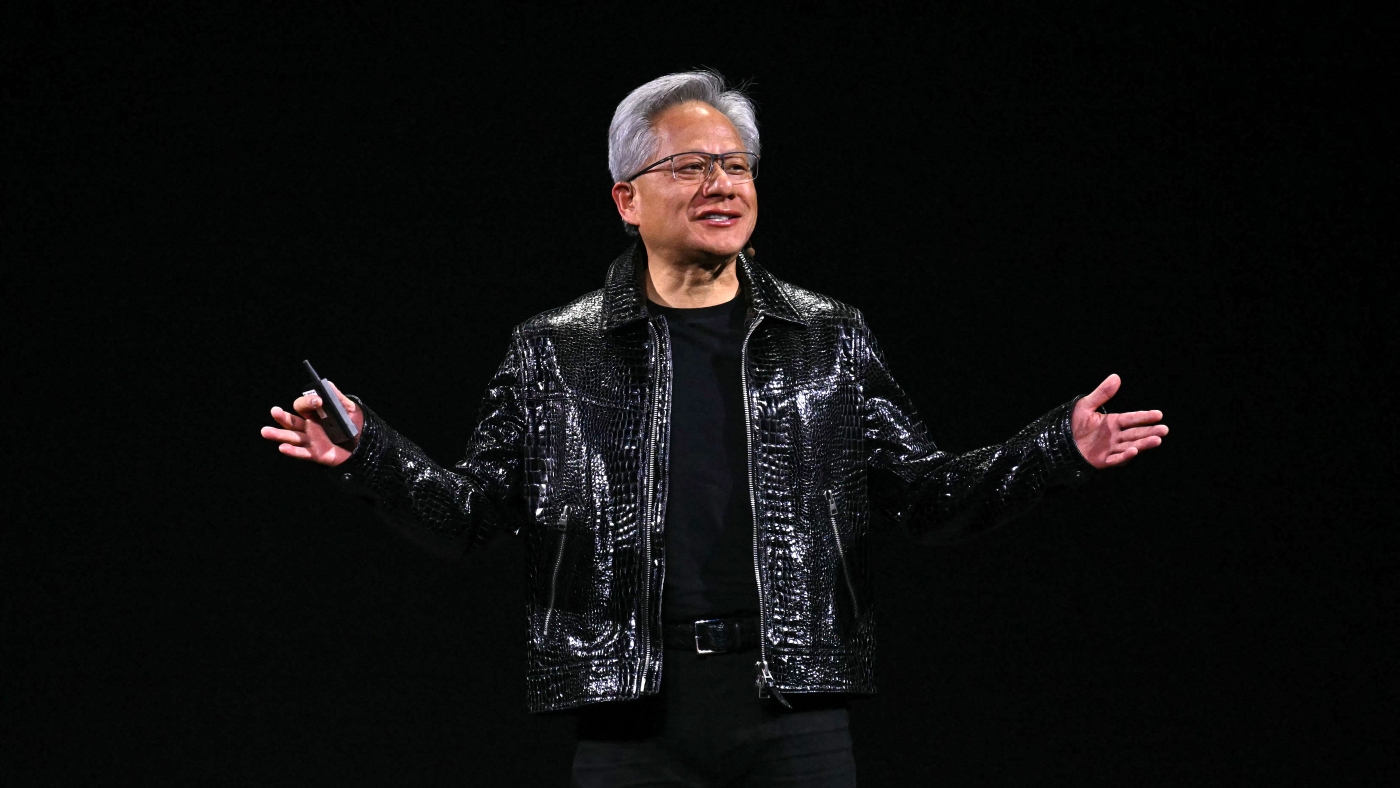

What concerns are there about an AI bubble? : NPR

Nvidia CEO Jensen Huang delivers a keynote address at the Consumer Electronics Show (CES) in Las Vegas in January.

Patrick T. Fallon/AFP via Getty Images

hide captiontoggle caption

Patrick T. Fallon/AFP via Getty Images

Perhaps nobody embodies artificial intelligence mania quite like Jensen Huang, the chief executive of chip behemoth Nvidia, which has seen its value spike 300% in the last two years.

A frothy time for Huang, to be sure, which makes it all the more understandable why his first statement to investors on a recent earnings call was an attempt to deflate bubble fears.

“There’s been a lot of talk about an AI bubble,” he told shareholders. “From our vantage point, we see something very different.”

Take in the AI bubble discourse and something becomes clear: Those who have the most to gain from artificial intelligence spending never slowing are proclaiming that critics who fret about an over-hyped investment frenzy have it all wrong.

“I don’t think this is the beginning of a bust cycle,” White House AI czar and venture capitalist David Sacks said on his podcast All-In. “I think that we’re in a boom. We’re in an investment super-cycle.”

White House AI adviser David Sacks speaks onstage during The Bitcoin Conference at The Venetian Las Vegas in January.

Ian Maule/AFP via Getty Images

hide captiontoggle caption

Ian Maule/AFP via Getty Images

“The idea that we’re going to have a demand problem five years from now, to me, seems quite absurd,” said prominent Silicon Valley investor Ben Horowitz, adding: “if you look at demand and supply and what’s going on and multiples against growth, it doesn’t look like a bubble at all to me.”

Appearing on CNBC, JPMorgan Chase executive Mary Callahan Erdoes said calling the amount of money rushing into AI right now a bubble is “a crazy concept,” declaring that “we are on the precipice of a major, major revolution in a way that companies operate.”

Yet a look under the hood of what’s really going on right now in the AI industry is enough to deliver serious doubt, said Paul Kedrosky, a venture capitalist who is now a research fellow at MIT’s Institute for the Digital Economy.

He said there is a startling amount of capital pouring into a “revolution” that remains mostly speculative.

“The technology is very useful, but the pace at which it is improving has more or less ground to a halt,” Kedrosky said. “So the notion that the revolution continues with the same drum beat playing for the next five years is sadly mistaken.”

The huge infusion of cash

The gusher of money is rushing in at a rate that is stunning to financial experts.

Take OpenAI, the ChatGPT maker that set off the AI race in late 2022. Its CEO Sam Altman has said the company is making $20 billion in revenue a year, and it plans to spend $1.4 trillion on data centers over the next eight years. That growth, of course, would rely on ever-ballooning sales from more and more people and businesses purchasing its AI services.

There is reason to be skeptical. A growing body of research indicates most firms are not seeing chatbots affect their bottom lines, and just 3% of people pay for AI, according to one analysis.

“These models are being hyped up, and we’re investing more than we should,” said Daron Acemoglu, an economist at MIT, who was awarded the 2024 Nobel Memorial Prize in Economic Sciences.

“I have no doubt that there will be AI technologies that will come out in the next ten years that will add real value and add to productivity, but much of what we hear from the industry now is exaggeration,” he said.

Nonetheless, Amazon, Google, Meta and Microsoft are set to collectively sink around $400 billion on AI this year, mostly for funding data centers. Some of the companies are set to devote about 50% of their current cash flow to data center construction.

Or to put it another way: every iPhone user on earth would have to pay more than $250 to pay for that amount of spending. “That’s not going to happen,” Kedrosky said.

To avoid burning up too much of its cash on hand, big Silicon Valley companies, like Meta and Oracle, are tapping private equity and debt to finance the industry’s data center building spree.

Paving the AI future with debt and other risky financing

One assessment, from Goldman Sachs analysts, found that hyperscaler companies — tech firms that have massive cloud and computing capacities — have taken on $121 billion in debt over the past year, a more than 300% uptick from the industry’s typical debt load.

Analyst Gil Luria of the D.A. Davidson investment firm, who has been tracking Big Tech’s data center boom, said some of the financial maneuvers Silicon Valley is making are structured to keep the appearance of debt off of balance sheets, using what’s known as “special purpose vehicles.”

An aerial view of a 33 megawatt data center with closed-loop cooling system in Vernon, California.

Mario Tama/Getty Images

hide captiontoggle caption

Mario Tama/Getty Images

The tech firm makes an investment in the data center, outside investors put up most of the cash, then the special purpose vehicle borrows money to buy the chips that are inside the data centers. The tech company gets the benefit of the increased computing capacity but it doesn’t weigh down the company’s balance sheet with debt.

For example, a special purpose vehicle was recently funded by Wall Street firm Blue Owl Capital and Meta for a data center in Louisiana.

The design of the deal is complicated but it goes something like this: Blue Owl took out a loan for $27 billion for the data center. That debt is backed up by Meta’s payments for leasing the facility. Meta essentially has a mortgage on the data center. Meta owns 20% of the entity but gets all of the computing power the data center generates. Because of the financial structure of the deal, the $27 billion loan never shows up on Meta’s balance sheet. If the AI bubble bursts and the data center goes dark, Meta will be on the hook to make a multi-billion-dollar payment to Blue Owl for the value of the data center.

Such financial arrangements, according to Luria, have something of a checkered past.

“The term special purpose vehicle came to consciousness about 25 years ago with a little company called Enron,” said Luria, referring to the energy company that collapsed in 2001. “What’s different now is companies are not hiding it. But having said that, it’s not something we should be leaning on to build our future.”

Enormous spending hinging on returns that could be a fantasy

Silicon Valley is taking on all this new debt with the assumption that massive new revenues from AI will cover the tab. But again, there is reason for doubt.

Morgan Stanley analysts estimate that Big Tech companies will dish out about $3 trillion on AI infrastructure through 2028, with their own cash flows covering only half of that.

“If the market for artificial intelligence were even to steady in its growth, pretty quickly we will have over-built capacity, and the debt will be worthless, and the financial institutions will lose money,” Luria said.

Twenty-five years ago, the original dot-com bubble burst after, among other factors, debt financing built out fiber-optic cables for a future that had not yet arrived, said Luria, a lesson, it appears, tech companies are not worried about repeating.

“If we get to the point after spending hundreds of billions of dollars on data centers that we don’t need a few years from now, then we’re talking about another financial crisis,” he said.

Circular deals raise even more concern

Another aspect of the over-heated AI landscape that is raising eyebrows is the circular nature of investments.

Take a recent $100 billion deal between Nvidia and OpenAI.

Nvidia will pump that amount into OpenAI to bankroll data centers. OpenAI will then fill those facilities with Nvidia’s chips. Some analysts say this structure, where Nvidia is essentially subsidizing one of its biggest customers, artificially inflates actual demand for AI.

“The idea is I’m Nvidia and I want OpenAI to buy more of my chips, so I give them money to do it,” Kedrosky said. “It’s fairly common at a small scale, but it’s unusual to see it in the tens and hundreds of billions of dollars,” noting that the last time it was prevalent was during the dot-com bubble.

Open AI CEO Sam Altman speaks during Snowflake Summit 2025 at Moscone Center in June.

Justin Sullivan/Getty Images

hide captiontoggle caption

Justin Sullivan/Getty Images

Lesser-known companies are getting in on the action, too.

CoreWeave, once a crypto mining startup, pivoted to data center building to ride the AI boom. Major AI companies are turning to CoreWeave to train and run their AI models.

OpenAI has entered deals with CoreWeave worth tens of billions of dollars in which CoreWeave’s chip capacity in data centers is rented out to OpenAI in exchange for stock in CoreWeave, and OpenAI, in turn, could use that stock to pay its CoreWeave renting fees.

Nvidia, meanwhile, which also owns part of CoreWeave, has a deal guaranteeing that Nvidia will gobble up any unused data center capacity through 2032.

“The danger,” said the MIT economist Acemoglu,”is that these kinds of deals eventually reveal a house of cards.”

Some high profile investors see bubble-popping on the horizon

Some influential investors are showing signs of bubble jitters.

Tech billionaire Peter Thiel sold off his entire stake in Nvidia worth around $100 million earlier this month. That came after SoftBank sold a nearly $6 billion stake in Nvidia.

And in recent weeks, AI bubble pessimists have rallied around Michael Burry, the hedge-fund investor who made hundreds of millions of dollars betting against the housing market in 2008. He was the subject of the 2015 film The Big Short. Since then, though, he’s had a mixed reputation for market predictions, having warned about imminent collapses that never came to pass.

For what it’s worth, Burry is now betting against Nvidia, accusing the AI industry of hiding behind a bunch of fancy accounting tricks. He’s homed in the circular deals between companies.

“True end demand is ridiculously small. Almost all customers are funded by their dealers,” Burry wrote on X. He later wrote: “OpenAI is the linchpin here. Can anyone name their auditor?”

As tech companies sink billions into data centers, some executives themselves are freely admitting there looks to be some over exuberance.

OpenAI CEO Sam Altman told reporters in August: “Are we in a phase where investors as a whole are overexcited about AI? My opinion is yes. Is AI the most important thing to happen in a very long time? My opinion is also yes.”

And Google chief executive Sundar Pichai told the BBC recently that “there are elements of irrationality” in the AI market right now.

Asked how Google would fare if the bubble burst, Pichai responded: “I think no company is going to be immune, including us.”

Continue Reading

-

Independent Non-Executive Director of Bridgepoint Group Picks Up 100% More Stock

Investors who take an interest in Bridgepoint Group plc (LON:BPT) should definitely note that the Independent Non-Executive Director, Cyrus Russi Taraporevala, recently paid UK£2.84 per share to buy UK£284k worth of the stock. That certainly has us anticipating the best, especially since they thusly increased their own holding by 100%, potentially signalling some real optimism.

AI is about to change healthcare. These 20 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10bn in marketcap – there is still time to get in early.

Notably, that recent purchase by Cyrus Russi Taraporevala is the biggest insider purchase of Bridgepoint Group shares that we’ve seen in the last year. That means that an insider was happy to buy shares at above the current price of UK£2.72. Their view may have changed since then, but at least it shows they felt optimistic at the time. To us, it’s very important to consider the price insiders pay for shares. Generally speaking, it catches our eye when an insider has purchased shares at above current prices, as it suggests they believed the shares were worth buying, even at a higher price. The only individual insider to buy over the last year was Cyrus Russi Taraporevala.

The chart below shows insider transactions (by companies and individuals) over the last year. If you click on the chart, you can see all the individual transactions, including the share price, individual, and the date!

Check out our latest analysis for Bridgepoint Group

LSE:BPT Insider Trading Volume November 23rd 2025 Bridgepoint Group is not the only stock insiders are buying. So take a peek at this free list of under-the-radar companies with insider buying.

Another way to test the alignment between the leaders of a company and other shareholders is to look at how many shares they own. Usually, the higher the insider ownership, the more likely it is that insiders will be incentivised to build the company for the long term. Based on our data, Bridgepoint Group insiders have about 0.1% of the stock, worth approximately UK£2.3m. We do note, however, it is possible insiders have an indirect interest through a private company or other corporate structure. We prefer to see high levels of insider ownership.

It is good to see the recent insider purchase. And the longer term insider transactions also give us confidence. While the overall levels of insider ownership are below what we’d like to see, the history of transactions imply that Bridgepoint Group insiders are reasonably well aligned, and optimistic for the future. So these insider transactions can help us build a thesis about the stock, but it’s also worthwhile knowing the risks facing this company. Our analysis shows 3 warning signs for Bridgepoint Group (1 is significant!) and we strongly recommend you look at these before investing.

Continue Reading

-

Exploring Valuation as Shares Edge Up Despite Sector Uncertainty

Oceaneering International (OII) has caught some attention lately as its stock edged higher, gaining about 3% in the latest session. This uptick comes even as the broader energy sector presented mixed signals for investors.

See our latest analysis for Oceaneering International.

Oceaneering International’s recent share price gain builds on a gradually improving short-term trend, but momentum is still muted compared to last year’s performance. While the stock is up 3.29% in the last session, the one-year total shareholder return sits at -19.58%. This reminds investors of some lingering caution, even after impressive multi-year gains.

If you’re keeping an eye on shifts in energy sector momentum, now is the perfect chance to broaden your search and discover fast growing stocks with high insider ownership

With shares staging a modest rebound, the question now is whether Oceaneering International remains undervalued with more upside ahead, or if investors have already factored in future growth prospects at current levels.

At $24.15 per share, Oceaneering International trades just above the consensus narrative fair value of $22.38, suggesting that the market anticipates robust operational progress and stable growth prospects.

The company’s high dependency on cyclical offshore oil and gas spending, evident in bookings and utilization guidance, makes its revenues and earnings vulnerable to potential sharp downturns if energy prices fall or if capital expenditure plans of major clients decline, as indicated by flat book-to-bill ratios and conservative utilization outlooks.

Read the complete narrative.

What hidden numbers are driving analyst models this time? The narrative is based on detailed assumptions about future revenue streams, margin pressures, and strategic pivots that could change profits more rapidly than many anticipate. Want to know what financial forecasts are influencing this price target? Find out what could surprise investors by reading the full breakdown.

Result: Fair Value of $22.38 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, continued growth in aerospace and defense contracts, or persistent strength in high-margin robotics, could boost earnings beyond current expectations.

Find out about the key risks to this Oceaneering International narrative.

While the market sees Oceaneering International as slightly overvalued based on analyst price targets, our DCF model presents a very different story. The SWS DCF model estimates fair value at $51.12, which is more than double the current share price. This suggests considerable undervaluation. Could analysts be overlooking hidden future cash flows?

Continue Reading

-

Assessing Valuation Following Recent Share Price Volatility

Dave (DAVE) shares have experienced some notable ups and downs over the past month, catching the attention of investors watching the stock’s performance. Recent price shifts prompt a closer look at how the company is positioned in today’s market.

See our latest analysis for Dave.

Dave’s recent 6.7% jump in share price came after weeks of choppy trading, including a noticeable slide earlier in the month. Even with this volatility, momentum remains strong, as shown by its impressive year-to-date share price return of 125.56% and a truly staggering total shareholder return of 1,383.84% over the past three years.

If you’re open to finding other remarkable growth stories in today’s market, now is the perfect moment to broaden your perspective and discover fast growing stocks with high insider ownership

But with Dave’s current share price still trading well below analysts’ targets, the key question remains: does this signal an undervalued opportunity, or has the market already factored in the company’s growth prospects?

With Dave’s last closing price standing well below its most popular narrative’s fair value, debate is swirling on what’s truly fueling this perceived upside. As analysts weigh enthusiasm against new profitability forecasts, one insight stands out as a defining catalyst.

Enhanced monetization from fee structure changes, including a successful rollout of a $3 monthly subscription fee (with no measurable negative impact on retention), offers meaningful ARPU and LTV uplift, further supported by secular demand for transparent, low-fee banking alternatives. This directly supports revenue growth and margin expansion.

Read the complete narrative.

Want to know what’s behind this big valuation gap? The narrative pivots on bold fee strategies, new margin targets, and revenue projections that defy industry norms. Ready to see the financial leap that drives this astounding fair value?

Result: Fair Value of $285 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are still questions about tightening regulations on fee-based models. There is also the possibility that shifting consumer preferences could dampen demand.

Find out about the key risks to this Dave narrative.

If you see things differently or want to conduct your own research, it only takes a few minutes to build your own perspective. Do it your way

A great starting point for your Dave research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Continue Reading

-

A Look At The Intrinsic Value Of iomart Group plc (LON:IOM)

-

Using the 2 Stage Free Cash Flow to Equity, iomart Group fair value estimate is UK£0.28

-

Current share price of UK£0.26 suggests iomart Group is potentially trading close to its fair value

-

Analyst price target for IOM is UK£0.53, which is 87% above our fair value estimate

Today we will run through one way of estimating the intrinsic value of iomart Group plc (LON:IOM) by taking the expected future cash flows and discounting them to their present value. One way to achieve this is by employing the Discounted Cash Flow (DCF) model. There’s really not all that much to it, even though it might appear quite complex.

Companies can be valued in a lot of ways, so we would point out that a DCF is not perfect for every situation. If you want to learn more about discounted cash flow, the rationale behind this calculation can be read in detail in the Simply Wall St analysis model.

AI is about to change healthcare. These 20 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10bn in marketcap – there is still time to get in early.

We are going to use a two-stage DCF model, which, as the name states, takes into account two stages of growth. The first stage is generally a higher growth period which levels off heading towards the terminal value, captured in the second ‘steady growth’ period. To begin with, we have to get estimates of the next ten years of cash flows. Where possible we use analyst estimates, but when these aren’t available we extrapolate the previous free cash flow (FCF) from the last estimate or reported value. We assume companies with shrinking free cash flow will slow their rate of shrinkage, and that companies with growing free cash flow will see their growth rate slow, over this period. We do this to reflect that growth tends to slow more in the early years than it does in later years.

A DCF is all about the idea that a dollar in the future is less valuable than a dollar today, so we discount the value of these future cash flows to their estimated value in today’s dollars:

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

Levered FCF (£, Millions)

UK£200.0k

UK£3.30m

UK£6.40m

UK£5.20m

UK£4.56m

UK£4.21m

UK£4.02m

UK£3.93m

UK£3.90m

UK£3.92m

Growth Rate Estimate Source

Analyst x2

Analyst x2

Analyst x1

Est @ -18.80%

Est @ -12.26%

Est @ -7.69%

Est @ -4.48%

Est @ -2.24%

Est @ -0.67%

Est @ 0.43%

Present Value (£, Millions) Discounted @ 13%

UK£0.2

UK£2.6

UK£4.4

UK£3.2

UK£2.5

UK£2.0

UK£1.7

UK£1.5

UK£1.3

UK£1.1

(“Est” = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = UK£20mContinue Reading

-