- From Traffic Volume to Experience Value, ZTE AIR RAN & AIR CORE Redefine the Paradigm of Network Monetization ZTE

- As an AI-Native Phone Pioneer, nubia Reshapes the Paradigm of Human-Device Interaction at MWC Barcelona 2026 Morningstar

- ZTE debuts 5G-A broadband CPE with Wi-Fi 8 Telecompaper

- ZTE Showcases Full-Stack AI Innovations at MWC Barcelona 2026, Creating an Intelligent Future Developing Telecoms

- China Unicom, ZTE launch UniMAX for 5G-A+AI convergence theregister.com

Category: 3. Business

-

From Traffic Volume to Experience Value, ZTE AIR RAN & AIR CORE Redefine the Paradigm of Network Monetization – ZTE

-

Iran war: Oil prices jump above $100 for first time in four years – BBC

- Iran war: Oil prices jump above $100 for first time in four years BBC

- Oil soars past $100 a barrel as Iran war rages Al Jazeera

- Asia markets tumble as oil nears $120; marks largest one day gain in almost 40 years CNBC

- War-driven energy insecurity Dawn

- Dollar jumps as Middle East war sends oil above $100 a barrel Reuters

Continue Reading

-

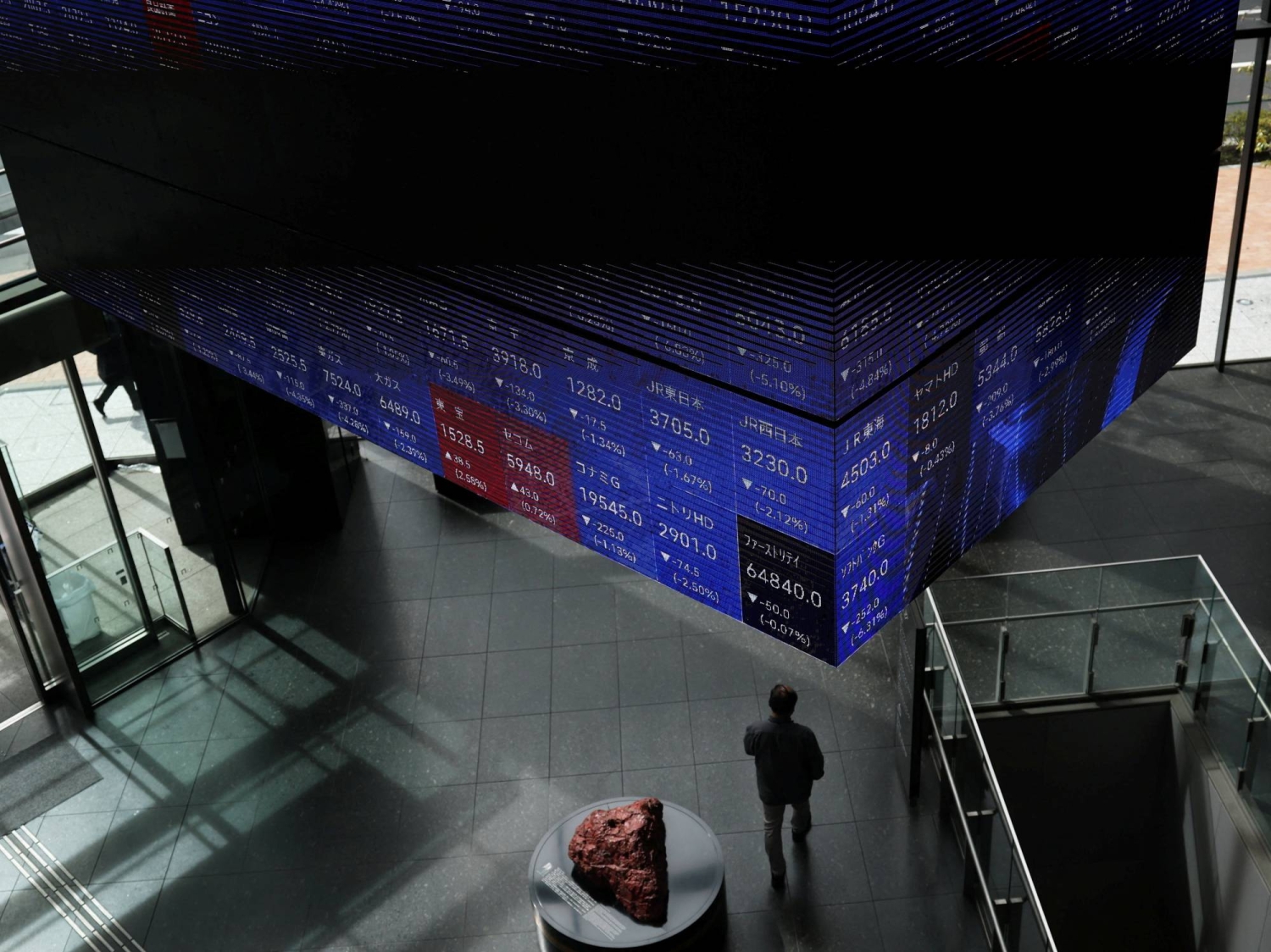

Nikkei 225 declines more than 6% as oil breaks $100 a barrel

Tokyo stocks sank at the market open Monday as oil prices soared, with the Nikkei 225 stock average dropping over 6% in the first half hour of trading.

Crude oil prices briefly hit $110 a barrel in New York trading shortly before trading opened in Tokyo on Monday, as the war in the Middle East dragged on and the threat to world oil supplies became increasingly urgent.

An unexpectedly weak jobs report issued by the United States on Friday also took a toll on the equity markets.

The U.S. lost 92,000 jobs in February, data from the Bureau of Labor Statistics showed, adding to concerns that the U.S. economy might face a double whammy in light of the ongoing war in the Middle East.

In trading Monday, the Nikkei 225 fell to 51,983.84 at 9:25 a.m. The index was near 60,000 at the end of February.

The yen weakened to about ¥158.4 to the dollar.

Continue Reading

-

Stock market today: Live updates

Traders work on the floor of the New York Stock Exchange on March 5, 2026.

Spencer Platt | Getty Images

Stock futures were plunging to start the week’s trading as U.S. oil prices topped $100 a barrel amid the U.S.-Iran conflict, raising fears higher energy prices could dramatically slow the U.S. economy. The Dow Jones Industrial Average is coming off its biggest weekly slide in nearly a year.

Futures tied to the Dow fell 848 points, or 1.79%. S&P 500 futures lost 1.7% and Nasdaq 100 futures dropped 1.9%.

West Texas Intermediate crude jumped 18% to above $107 a barrel, its first time above the $100 level since July 2022, when investors were reacting to the aftermath of Russia’s invasion of Ukraine. International benchmark Brent crude added 16% to above $108 a barrel. U.S. oil prices began the year below $60 a barrel.

Oil futures jumped on Sunday night after major Middle East producers slashed their output due to the continued closure of the key Strait of Hormuz passageway. Kuwait announced cuts but did not say by how much, while Iraq has reportedly seen its production fall 70%.

The $100 oil level was seen by many on Wall Street as a breaking point for the economy unless the war is resolved quickly and prices retreat.

Trump posted Sunday evening that a gain in “short term oil prices” was a “very small price to pay” for destroying Iran’s nuclear threat.

The war showed little signs of easing despite Trump’s claim it was “already won” with Iran naming Ayatollah Khamenei’s son, Mojtaba, as its new supreme leader, according to reports.

Sunday’s moves follow a rough week on Wall Street as the U.S.-Iran war sent crude prices spiking. U.S. crude soared more than 35% last week, marking its biggest weekly gain since the futures contract began trading in 1983.

The Dow slid around 3% last week, its worst weekly decline since President Donald Trump’s initial tariff announcement roiled markets in early April 2025. The broad S&P 500 shed 2%, while the Nasdaq Composite ended the week 1.2% lower.

“Markets are clearly jittery as the impact, and duration, of the war in the Mideast are very uncertain, with a potentially wide range of outcomes for economies and important market influences,” BlackRock CIO Rick Rieder wrote to clients on Friday. “These events are creating some extreme movements in areas of the markets as market participants are clearly looking to reduce overweight positions or hedge embedded risk.”

There’s no economic data of note slated for Monday, but investors will follow releases on inflation, employment and gross domestic product due throughout the week. Investors will monitor Hewlett Packard Enterprise earnings after the bell on Monday, followed by Kohl’s, Oracle, Dollar General and Dick’s Sporting Goods later in the week.

— CNBC’s Spencer Kimball contributed to this report.

Continue Reading

-

OpenAI robotics leader resigns over concerns about Pentagon AI deal : NPR

OpenAI CEO Sam Altman speaks in Washington, D.C., on July 22, 2025.

Mandel Ngan/AFP via Getty Images

hide captiontoggle caption

Mandel Ngan/AFP via Getty Images

A senior member of OpenAI’s robotics team has resigned, citing concerns about how the company moved forward with a recently announced partnership with the U.S. Department of Defense.

Caitlin Kalinowski, who served as a member of technical staff focused on robotics and hardware, posted on social media that she had stepped down on “principle” after the company revealed plans to make its AI systems available inside secure Defense Department computing systems.

The agreement is part of a broader push by the U.S. government to incorporate advanced AI tools into national security work, a trend that has sparked debate across the tech industry about oversight and acceptable uses.

In public posts explaining her decision, Kalinowski wrote: “I resigned from OpenAI. I care deeply about the Robotics team and the work we built together. This wasn’t an easy call.”

She said policy guardrails around certain AI uses were not sufficiently defined before OpenAI announced an agreement with the Pentagon. “AI has an important role in national security,” Kalinowski wrote. “But surveillance of Americans without judicial oversight and lethal autonomy without human authorization are lines that deserved more deliberation than they got.”

Kalinowski also emphasized that her concerns were more about the process rather than specific executives inside the company, saying she had “deep respect for Sam and the team, and I’m proud of what we built together,” referring to OpenAI chief executive Sam Altman.

A spokesperson for OpenAI told NPR the company believes the agreement with the Pentagon “creates a workable path for responsible national security uses of AI while making clear our red lines: no domestic surveillance and no autonomous weapons.”

It continued, saying the company recognized “people have strong views about these issues and we will continue to engage in discussion with employees, government, civil society and communities around the world.”

Kalinowski’s resignation comes amid heightened competition among leading developers of artificial intelligence to supply technology to the U.S. government. In recent weeks, federal agencies have turned to OpenAI and Google for AI systems as tensions increased with a rival firm, Anthropic, over the military use of its models.

Anthropic’s CEO spoke out against allowing the company’s software to be used for applications such as domestic mass surveillance or autonomous weapons, a stance that led to clashes with defense officials — including Secretary of Defense Pete Hegseth — who said the department needs flexibility to deploy commercial AI tools in all “lawful” operations.

Within OpenAI, Kalinowski’s role focused on building out the company’s robotics organization as it scaled. She wrote on her LinkedIn profile that this included hiring to support the company’s expansion into AI efforts tied to physical infrastructure and machinery.

Kalinowski signaled she plans to continue working in the same field. “I’m taking a little time, but I remain very focused on building responsible physical AI,” she wrote.

Continue Reading

-

Could AI-powered property management transform hotel stays?

Investing.com — Artificial intelligence could soon reshape how hotel stays are designed and managed, enabling highly personalized experiences for guests while opening new revenue opportunities for hotel operators, according to a report by Bernstein.

AI is increasingly reshaping the travel industry, particularly in how trips are discovered and planned online. However, the booking and hotel stay experience itself has changed little so far. Analysts say advances in hotel technology and AI agents could enable a new wave of hyper-personalized stays, where guests customize room features, amenities and services before arrival.

This could include options such as selecting specific room attributes like floor level or view, choosing pillow types or minibar contents, arranging spa treatments, or booking transport and dining in advance. AI agents could handle these decisions automatically based on a guest’s travel history and personal preferences, simplifying what would otherwise involve navigating hundreds of choices.

The report notes that some forms of personalization already exist in luxury hotels, where guests can choose amenities such as pillow types or pre-arranged services before arrival. But AI could expand these capabilities significantly by automating decisions and coordinating services behind the scenes.

To enable this shift, hotel technology systems will need to evolve. Current booking and property management systems typically categorize rooms by basic types rather than detailed attributes, limiting how much customization can be offered during booking. Moving to attribute-based inventory systems could allow hotels to dynamically price and manage personalized options.

Major hotel groups are already investing in updated technology stacks to support these capabilities. For example, companies such as Marriott and InterContinental Hotels Group are developing systems that allow more granular room characteristics and customization features to be integrated into the booking process.

Bernstein also noted that AI-driven personalization could strengthen hotels’ direct booking channels. Because hotels control detailed information about their inventory and services, they may choose not to share all data with online travel agencies, potentially giving direct booking platforms an advantage.

Over time, AI-powered hotel management could expand personalization beyond luxury properties, especially if automation technologies such as service robots and integrated hotel systems reduce the labor required to deliver customized services.

Continue Reading

-

UK must be prepared for a price shock from the Iran war | Heather Stewart

Donald Trump’s assault on Iran and the deadly conflict it has unleashed is grim and unprecedented – but there is a familiarity to its economic consequences: brace yourself for another price shock.

From the Covid shutdown and subsequent reopening to Russian tanks rolling into Ukraine, the global economy has been rocked by one cost surge after another.

Meanwhile, the climate crisis means more volatility in the cost of commodities whose production is vulnerable to extreme weather events – coffee, cocoa and olive oil.

The reaction to Trump’s Operation Epic Fury in the energy markets was initially relatively restrained. On Friday, though, with the critical strait of Hormuz effectively closed, and reports of production cuts in Kuwait, the dam seemed to break, pushing oil to $90 (£67) a barrel.

Oil shocks are especially painful because of the commodity’s wider uses, not least in fertiliser, and the knock-on effects for manufacturing and transport.

And poorer people are hit hardest. Recent research published by economists at the University of Massachusetts Amherst identified energy, along with food and agriculture as among the commodities that had “a disproportionate capacity to increase inequality when their prices rise”.

Where there are benefits, these are narrowly shared. Another striking recent paper showed that after the 2022 oil price surge in the US, 50% of the windfall benefit from higher prices in the sector went to the wealthiest 1% of individuals, via the stock market. The bottom 50% of people received only 1%.

As Gregor Semieniuk, the lead author, puts it: “While everybody is bearing the inflation costs of an energy price crisis, which drove inflation in 2022, the very prices that are causing this inflation are also giving extraordinary profits to mostly a small minority of very affluent shareholders.”

In the UK – unlike the US, a net oil importer, where the impact of higher prices is therefore unambiguously negative – the impact of the Middle East conflict has already added 3p to the cost of a litre of unleaded, according to the RAC.

If the jump in the cost of gas proves sustained, household energy bills could rise sharply when the next quarterly price cap takes effect in July – just as Labour was trumpeting its plans to reduce household costs. Ministers are already thinking about how they might protect consumers.

It is the latest stark reminder that hiving off the job of tackling economy-wide inflation to central banks, and letting the market sort out the rest, is becoming less and less viable in this volatile world.

Even Liz Truss tacitly admitted as much, when she brought in the energy price cap in 2022 – a surprisingly statist policy for an avowed free marketeer.

With or without government action to keep a lid on utility bills, a fresh oil shock is a nightmare for central bankers everywhere, especially in the UK.

They can in theory “look through” supply-side shocks, such as rocketing energy prices, which tend to be inflationary in the short-term but ultimately depress growth and inflation, as consumers cut back spending elsewhere.

Alan Taylor, a dovish independent member of the Bank of England’s monetary policy committee, made that point in a recent speech. “Large energy shocks move faster than inflation-targeting central banks can respond,” he said, adding: “Central banks and their mandates can never fully solve every type of inflation problem, including the big shocks of recent years.”

Yet the prospect of a fresh surge in economy-wide inflation, just as it was set to return to the 2% target, is likely to prompt the divided MPC to hold off from further rate cuts.

So we may now face a grim few months in which the Bank sits on its hands, as unemployment continues to climb with young people bearing the brunt.

Recent research by Joseph Evans and Carsten Jung of the Institute for Public Policy Research highlighted the risks, in particular to workers, of running the economy “too cold for too long” – slowing it down too much to tackle inflation.

Shocks such as these are expected to keep rocking the heavily indebted and import-dependent UK economy in a world with fracturing geopolitics and a raging climate crisis.

That may eventually mean rethinking the monetary policy framework. Economists at the London School of Economics’ Grantham Research Institute have mooted “adaptive inflation targeting”, for example, which would allow for more leeway in times of repeated shocks.

However, politicians will increasingly have to look beyond monetary policy, too: acting to secure supplies of key commodities, protecting the poorest from the worst of the onslaught, and cracking down hard on the price gouging that tends to take place in these tight spots.

If the jump in the cost of gas proves sustained, household energy bills could rise sharply when the next quarterly price cap takes effect in July. Photograph: Andy Rain/EPA In the energy sector, the long-term answer is the one set out by energy secretary, Ed Miliband, in the House of Commons last Thursday, and pursued doggedly by Labour since it came to power in 2024: “Get off our dependence on fossil fuel markets, whose prices we do not control, and on to clean, homegrown power that we do control.”

That will take time, though – and it’s not only energy. Governments are increasingly having to wake up to the fact that they will have to take a closer interest in the supply chains for essentials, from food to rare earths, as the climate crisis and rising geopolitical instability make strung-out, just-in-time supply chains look increasingly fragile.

Should hostilities abate in the coming days, energy supplies could be unblocked – but for the moment, as the chancellor, Rachel Reeves, prepares to give the annual Mais lecture on Labour’s latest plans for kickstarting growth, the UK must ready itself for yet another economic shock.

Continue Reading

-

Why an Iran war inflation shock could wreck global economic recovery | Economics

An inflation shock triggered by the US-Israel attack on Iran could wreck a fragile global economic recovery that had been expected to gain momentum this year.

With oil and gas prices spiking, despite a pledge from Donald Trump to protect tankers making their way through the crucial strait of Hormuz shipping chokepoint, central bankers and economists have warned that a prolonged conflict could increase retail prices around the world and force them to rip up growth forecasts for this year.

On Friday, the International Monetary Fund managing director, Kristalina Georgieva, said a 10% increase in energy prices that persists for a year would push up global inflation by 40 basis points and slow global economic growth by 0.1-0.2%.

“The world economy has been remarkably resilient. Shock after shock, and yet growth is at 3.3%,” Georgieva told Bloomberg.

Some economists argue that a jump in the price of energy and transport costs, significant though they are for households and businesses, could prove to be a sideshow if the bombing of Iran by the US and Israel destabilises financial markets already worried about ballooning AI stocks and the impact of US import tariffs.

“It’s not like this war has started with the world in a settled place,” said Lord Jim O’Neill, the ex-chief economist of Goldman Sachs Asset Management and former government adviser.

There are also analysts who worry about the chaos prompted by Iran’s retaliatory bombing of Kuwait, Dubai, Saudi Arabia and, most recently, Azerbaijan, which could trigger a further re-ordering of global strategic alliances – and not to the west’s benefit.

O’Neill, a crossbench peer, said the White House appeared to have given little consideration to the geopolitical impact of its opportunistic assassination of Ayatollah Ali Khamenei and subsequent bombing campaign.

“The Gulf states will be thinking the US is an unreliable partner and be drawn towards China, India and Brazil,” he said.

O’Neill became famous more than 20 years ago for coining the term Brics to denote the emerging economies of Brazil, Russia, India, China and South Africa, which was later expanded to include Iran and Saudi Arabia among a larger grouping of 11.

Saudi Arabia, the United Arab Emirates and Kuwait are among the countries to have had important infrastructure sites – airports, oil refineries and gas plants – targeted by Iranian rockets and drones.

If Iran takes aim at some of the 450-plus desalination plants that feed the region with fresh water, then social unrest could follow.

Oil is the key

About 20% of global oil supply passes through the strait of Hormuz. Drawing on academic studies and the experience of past supply disruption, Bloomberg Economics estimates that a 1% drop in supply pushes oil prices up by about 4%.

That suggests a closure of the strait over a few months would raise prices by 80% from pre-Iran war levels, taking them to about $108 a barrel.

Oxford Economics said it expected inflation at the end of the year in the UK and eurozone would be roughly 0.5 percentage points to 0.6 percentage points higher than previously expected. UK inflation was 3% in January, while in the eurozone it was 1.9% in February.

Economic growth will be hit

In the US, forecasts have remained unchanged, with economists pencilling in growth of 2.2% this year, as the cost of higher wholesale energy prices is offset by the huge gains to the US fracking companies that will benefit from bigger profits selling their home-drilled gas.

However, US consumers have already begun to feel direct financial pain after a 17% rise in Brent crude prices that has fed into fuel station prices, which tend to rise roughly 2.5 cents for every $1 increase per barrel on global markets.

Since last Saturday, prices at the pump have jumped by 15 cents a gallon on average across the US, according to the price tracker service GasBuddy.

Long term, disruptions in the global supply chain are likely to feed back to the US and push up costs that many Americans already believe are too high. Anger over the cost of living was a major factor in Joe Biden’s defeat. Now, Trump is struggling to convince Americans that he has the situation under control.

Trump’s nominee as the incoming chair of the Federal Reserve, Kevin Warsh, is expected to change the US central bank’s response to inflation. If he follows the president’s wishes, Warsh will cut interest rates when he takes over in May, even if inflation is increasing. Last week, financial markets assigned a 97% probability to the Fed holding rates steady at its meeting later this month, monitoring how the Iran conflict develops before taking any action.

UK and Europe will suffer

According to the National Institute of Economic and Social Research, a UK thinktank, economic growth in the UK and euro area could drop by 0.2% this year if the impact of the conflict persists. In the UK, that means national income, or gross domestic product (GDP), falling from a growth rate of 1.1% estimated by the Office for Budget Responsibility to 0.9%.

The projection for the euro area by the EU Commission would be cut from 1.2% to 1%. In the context of a long period of low growth, these falls will damage investment, push up interest rates and hurt government finances.

In the UK, diesel has risen 5p since the conflict began to 147p a litre – the most expensive since August 2024 – while petrol has risen by 3p to 136p on average, the RAC said.

That will place a further squeeze on households already grappling with the rising cost of essentials, which has become a political sore spot in the lead-up to both local elections in the UK in May and the US midterms in November.

Official polling released by the Office for National Statistics last month found that 88% of adults believed the cost of living was the most important issue facing Britain.

A recent poll by YouGov showed that roughly 42% of Americans believe the state of the US economy is poor, marking the highest level since September 2024. That has been compounded by anger over Trump’s tariff regime, with most Americans saying Trump’s tariffs have resulted in them having to pay more for goods and services, according to a separate YouGov poll.

Emphasising the vulnerability across Europe to higher imported gas and oil prices, three European Central Bank (ECB) policymakers warned on Thursday that eurozone inflation would probably rise, and growth sag, if the conflict in the Middle East becomes drawn out and sucks in more countries.

The ECB’s vice-president Luis de Guindos, and the central bank governors of Germany and Finland, all said it was too early to draw conclusions but warned that a prolonged, wider war may push up inflation, both present and expected.

De Guindos said: “The baseline (is) that this is going to be short-lived. If it is longer, then there is a risk that inflation expectations will change.”

The interest rate conundrum

In the UK, Bank of England ratesetter Alan Taylor said on Monday that central banks should reject raising interest rates to tackle an energy price shock that was imported from the Middle East and over which UK policymakers had little control.

Taylor is more concerned that high borrowing costs will make a difficult situation worse, hitting investment and pushing up unemployment from already high levels.

Taylor is likely to be in a minority after central bankers delayed interest rate rises in the wake of Russia’s invasion of Ukraine. Most central bank staff have since concluded that treating the situation as temporary was a mistake and they should have reacted more quickly to rising oil, gas and food costs.

Michael Saunders, senior economic adviser at Oxford Economics and a former central bank official, said he expected the Bank to hold rates at 3.75% at its next meeting and possibly for the remainder of this year if the conflict continued. In the days before the war erupted, financial markets expected at least two quarter-point cuts this year, to 3.25%.

UK mortgage lenders have already begun to increase the interest rate on home loans in a further blow to the living standards of hard-pressed households who cannot catch a break.

Continue Reading

-

UBS sees rising opportunity for analog semis in AI data center power

Investing.com – Analog semiconductor makers are poised to benefit from the rapid buildout of artificial intelligence data centers, as the growing power demands of advanced computing infrastructure drive higher demand for chips that manage and regulate electricity, according to UBS.

Unlike digital processors such as GPUs that perform computing tasks, analog and power semiconductors manage how electricity flows through data center systems.

These components are essential at multiple stages of the power chain, including converting grid electricity into usable power for servers and stabilizing voltage for GPUs and other computing hardware.

The importance of these chips is rising as AI workloads dramatically increase electricity consumption inside data centers. New AI server racks require far more power than traditional computing infrastructure, pushing operators to adopt more advanced power management architectures.

The bank said power semiconductors, which convert and control electricity across servers and infrastructure, are becoming increasingly important as AI data centers consume significantly more power than traditional facilities.

UBS expects the market for AI data center power semiconductors to expand sharply over the next few years, estimating total addressable market growth from about $1.5 billion in 2025 to roughly $2.5 billion in 2026. The market could reach around $3.8 billion by 2028 as AI infrastructure continues to scale.

A key driver of this growth is the rising power density of AI server racks. As more GPUs are packed into data center systems, the electricity required per rack is expected to surge from roughly 40 kilowatts in 2023 to as much as 1 megawatt by 2028, significantly increasing the amount of power management hardware required.

This shift is also prompting architectural changes in data center design, including a move toward 800-volt direct current power systems, which improve efficiency but require more advanced semiconductor components.

UBS said power supply units and voltage regulator modules currently account for roughly 70% of power semiconductor demand in AI servers, as these components are critical for converting grid electricity and delivering stable power to GPUs.

Among companies exposed to the trend, UBS highlighted Infineon and Texas Instruments as leading suppliers in the segment, with Analog Devices, Renesas, ON Semiconductor and STMicroelectronics also increasing their presence in AI data center power systems.

However, the bank cautioned that growth could moderate later in the decade if the pace of new data center capacity additions slows or if the industry experiences some degree of over-ordering across the supply chain.

Continue Reading