State-of-the-art site in Sanand, Gujarat, expands Micron’s global footprint and advances India’s semiconductor ecosystem

SANAND, India, Feb. 28, 2026 (GLOBE NEWSWIRE) — Micron Technology, Inc. (NASDAQ: MU) today celebrated the grand opening of its semiconductor assembly and test facility in Sanand, Gujarat, India. The state-of-the-art facility converts advanced DRAM and NAND wafers from Micron’s global manufacturing network into finished memory and storage products. Once fully ramped, the first phase of Micron’s Sanand operation will feature more than 500,000 square feet of cleanroom space, making it one of the world’s largest single-floor assembly and test cleanrooms. The site serves customers worldwide to meet the growing global demand for memory and storage fueled by AI.

The facility represents a combined investment of approximately $2.75 billion by Micron and its government partners, advancing semiconductor manufacturing capabilities in India. Micron Chairman, President and CEO Sanjay Mehrotra and other executives witnessed the opening ceremony with Prime Minister Narendra Modi, Chief Minister of Gujarat Bhupendra Patel, Union Minister for Railways, Communications, Electronics & IT Ashwini Vaishnaw, U.S. Ambassador to India Sergio Gor and other distinguished government officials and guests.

“Today is a proud moment for Micron and India’s growing semiconductor industry,” said Sanjay Mehrotra, Chairman, President and CEO of Micron Technology. “This pioneering facility, the first assembly and test site of its kind in the country, helps build a resilient ecosystem that underpins the global AI economy. We are deeply grateful to the government of India, the Gujarat government and all of the partners involved for their steadfast support in making this achievement possible.”

The Sanand site is ISO 9001:2015 certified and has begun commercial production. To mark the grand opening of the site, Micron presented its first shipment of made-in-India memory modules to Dell Technologies for its laptops made in India for India. Micron expects to assemble and test tens of millions of chips at Sanand in 2026, scaling to hundreds of millions in 2027. The expansion of conventional assembly and test operations in India complements Micron’s planned development of advanced manufacturing and packaging capabilities in the United States and strengthens the company’s global assembly and test network.

“The inauguration of Micron’s semiconductor facility in Sanand marks a historic milestone as Bharat begins its first commercial semiconductor chip production,” said Union Minister Ashwini Vaishnaw. “This is a decisive step towards building a trusted, resilient and self-reliant semiconductor ecosystem under the leadership of Hon’ble PM Shri Narendra Modi Ji. India is now moving from being a consumer of chips to becoming a global hub for semiconductor manufacturing and innovation.”

Micron is building India’s next generation of semiconductor talent to support its operations in India. Through partnerships with Pandit Deendayal Energy University (PDEU), Namtech, leading universities nationwide and government-sponsored skills development programs, Micron is supporting STEM education, specialized training, workforce readiness for advanced manufacturing roles and community initiatives, including digital and AI literacy programs across the region.

Micron built and is operating the assembly and test facility in accordance with the company’s sustainability goals, rigorous health and safety standards, and with local and global environmental commitments. The facility is designed to meet or exceed Leadership in Energy and Environmental Design (LEED) Gold standards. Additionally, the facility uses advanced water-saving technologies to enable zero liquid discharge.

About Micron Technology, Inc.

Micron Technology, Inc. is an industry leader in innovative memory and storage solutions, transforming how the world uses information to enrich life for all. With a relentless focus on our customers, technology leadership and manufacturing and operational excellence, Micron delivers a rich portfolio of high-performance DRAM, NAND and NOR memory and storage products. Every day, the innovations that our people create fuel the data economy, enabling advances in artificial intelligence (AI) and compute-intensive applications that unleash opportunities — from the data center to the intelligent edge and across the client and mobile user experience. To learn more about Micron Technology, Inc. (Nasdaq: MU), visit micron.com.

Forward-Looking Statements

This press release contains forward-looking statements, including statements regarding expectations of future production. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results to differ materially. Please refer to the documents Micron files with the Securities and Exchange Commission, specifically its most recent Form 10-K and Form 10-Q. These documents contain and identify important factors that could cause actual results to differ materially from those contained in these forward-looking statements. These certain factors can be found at https://investors.micron.com/risk-factor. Although Micron believes that the expectations reflected in the forward-looking statements are reasonable, Micron cannot guarantee future results, levels of activity, or achievements. Micron is under no duty to update any of the forward-looking statements after the date of this press release to conform these statements to actual results.

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

This article is an on-site version of our Unhedged: Chart of the Week newsletter. You sign up here to get the newsletter delivered every Saturday, or explore all FT newsletters

Nvidia, with a market capitalisation of $4.5tn or so, is the most valuable company in the world. Its share price has risen 700 per cent in three years and its sales have grown at a rate of 100 per cent annually over that period. But even for the greatest growth stories, at some point every possible expectation is priced in and every investor owns as much of the stock as they want.

The chip group late on Wednesday reported another blockbuster quarter with $68bn in sales, topping analysts’ expectations. By Friday afternoon the shares were off about 10 per cent, although they retraced some of their losses. This repeats the usual pattern of most quarterly reports going back to the middle of 2024: epic growth, expectations surpassed — and an unimpressed market. Over the past six months, Nvidia’s shares are roughly flat and are underperforming the S&P 500.

There is no sign that data centre spending, and therefore sales of Nvidia’s GPU chips, is slowing down any time soon. But the longer-term future of the AI industry is coming into doubt as questions swirl about the return on investment from data centres and the impact of AI on employment and the economy. Despite its runaway growth, the company has lost its valuation premium: its forward price/earnings ratio is the same as the S&P 500’s.

Are we witnessing a pause in investors’ love affair with Nvidia? Or has the relationship changed forever? Let us know your thoughts: unhedged@ft.com.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

The AI Shift — John Burn-Murdoch and Sarah O’Connor dive into how AI is transforming the world of work. Sign up here

On 7 August, Kate Fox received a phone call that upended her life. A medical examiner said that her husband, Joe Ceccanti – who had been missing for several hours – had jumped from a railway overpass and died. He was 48.

Fox couldn’t believe it. Ceccanti had no history of depression, she said, nor was he suicidal – he was the “most hopeful person” she had ever known. In fact, according to the witness accounts shared with Fox later, just before Ceccanti jumped, he smiled and yelled: “I’m great!” to the rail yard attendants below when they asked him if he was OK.

But Ceccanti had been unravelling. In the days before his death, he was picked up from a stranger’s yard for acting erratically and taken to a crisis center. He had been telling anyone who would listen that he could hear and feel a painful “atmospheric electricity”.

He had also recently stopped using ChatGPT.

Ceccanti had been communicating with OpenAI’s chatbot for a few years. He used it initially as a tool to brainstorm ways to build a path to low-cost housing for his community in Clatskanie, Oregon, but eventually turned to it as a confidante. He would spend 12 hours a day typing to the bot, according to his wife. He had cut himself off from it after she, along with his friends, realized he was spiraling into beliefs that were detached from reality.

“He was not a depressed person,” Fox said, as she sat on the couch in their living room with tears trickling down her face. Ceccanti never discussed suicide with the bot, according to his chat logs, viewed by the Guardian. Fox believes her husband suffered a crisis after quitting ChatGPT after prolonged use. “Which tells me that this thing is not just dangerous to people with depression, it’s dangerous to anybody,” she said. He returned to the bot in the months leading up to his death and quit again just days prior.

Ceccanti’s case is extreme, but as hundreds of millions of people turn to AI chatbots, more and more edge cases of AI-induced delusions are emerging. There are nearly 50 cases of people in the US who have had mental health crises after or during their conversations with ChatGPT, of whom nine were hospitalized and three died, according to a New York Times report. It’s difficult to understand the scale of the problem, but OpenAI itself estimates that more than a million people every week show suicidal intent when chatting with ChatGPT.

A self-portrait Joe made with AI.

Families are suing AI companies as a result. Fox filed a suit against OpenAI on behalf of Ceccanti alongside six other plaintiffs in November. Since then, the momentum has only built; most recently, the estate of a woman who was killed by her son filed a lawsuit against OpenAI and its investor Microsoft, alleging that ChatGPT encouraged his murderous delusions. Google and Character.AI – a company that makes AI companion bots – settled lawsuits filed against them by families accusing their bots of harming minors, including a teenager in Florida who ended his life. These cases were settled without the companies admitting any liability.

Users, lawyers and mental health professionals all are raising concerns about the impact of using chatbots as confidantes. “We are kind of at this inflection point in a quest for accountability where people coming forward is forcing companies to reckon with specific use cases of how their technologies have harmed people,” said Meetali Jain, founding director of Tech Justice Law Project and co-counsel on the Ceccanti case. “In terms of the number of cases going up, there’s likely to be more coordinated efforts on parts of the court to try to deal with this influx of cases.”

OpenAI did not respond to specific allegations made by Fox. Instead, they shared a statement about how they are working to improve ChatGPT. “These are incredibly heartbreaking situations and our thoughts are with all those impacted,” said OpenAI spokesperson Jason Deutrom. “We continue to improve ChatGPT’s training to recognize and respond to signs of distress, de-escalate conversations in sensitive moments, and guide people toward real-world support, working closely with mental health clinicians and experts.”

The early adopter

Ceccanti had been tinkering with artificial intelligence even before ChatGPT launched in November 2022. He was tech-savvy, coding and gaming on his own custom-built computer with a high-end graphics card in recent years; he also helped build computers for Fox and her son. As an early adopter of AI tools, he experimented with AI image generator Stable Diffusion to recreate some of Picasso’s art, which he playfully called “Fauxcasso”.

Ceccanti and Fox had moved their life from Portland, Oregon, to a farm in the rural town of Clatskanie in December 2023 with the sole purpose of working on their sustainable housing project. The idea was born from the pandemic and Portland’s housing crisis. The solution was clear to them: build homes using Fox’s skills as a woodworker with an approach that was teachable and replicable. Together, they began constructing a model house for communal living, which, once built, could be moved to different locations for the unhoused to live in.

When ChatGPT launched in late 2022, it seemed a natural progression for Ceccanti to start using it. In the computer room in the basement of their house, Fox said that Ceccanti used his “hot rod” of a computer with three monitors to use ChatGPT as a tool, often asking for the synopsis of a book or explanation of a concept in a succinct way.

“He was an early adopter, so he was really interested in Sam Altman, what’s he doing,” said Robin Richardson, a longtime friend of Fox’s who lived at the farm with the couple. “He felt like this would be cool, especially because early on, OpenAI made a point that they are a non-profit.”

Ceccanti believed ChatGPT could help as an organizational tool for their housing project. He aimed to create a bespoke chatbot that would help steward the land, keep track of their things to do and show others how to emulate their project.

Left: Books on a bookshelf. Right: Two chickens pecking on flowersLeft: Farming and gardening books in Kate’s home. Right: Chickens on Kate’s front porch.

During this process, Ceccanti didn’t spend “ridiculous amounts of time” engaging with ChatGPT, said Fox. He continued to work, while also farming and taking care of their animals: goats, a horse, his cat, a dog and several chickens. Invested in the people and relationships around him, he spent quality time with his friends and wife, she said. Life went on without any issues for years while they slowly made progress on their housing plan.

Until one day in the fall of 2024 their harmonious co-existence cracked. Ceccanti – who had done odd jobs most of his life, from working as a bartender and a trail guide to an internet cafe manager – was also working at a homeless shelter in Astoria, some 35 miles (55km) away. The gig brought in some extra cash, and aligned with the couple’s goal of solving the local housing crisis. In September 2024, however, Fox and Richardson received a frantic call from the shelter informing them that Ceccanti had blacked out. After undergoing tests at the hospital, Ceccanti was diagnosed with diabetes – which meant he needed to recalibrate his diet and lifestyle. That’s when he started to spend more time engaging with ChatGPT in the basement.

The sycophantic update

In the spring of 2025, Ceccanti’s obsession with the chatbot began. He told Fox in late January that he needed a bigger record of his conversations with the bot so that he could continue using it to work on their sustainable housing project with longer prompts and conversations – upgrading from a $20-a-month subscription to a $200 one. By mid-March, he had begun spending more than 12 hours a day in the basement, sometimes up to 20, typing to ChatGPT, Fox recalled. That’s when “he decided to really start chasing the creation of an independent AI on a home server”.

Eventually, Ceccanti spent so much time with ChatGPT that they “had their own little language together that made absolutely no sense, but it made sense to him because he had context with this echo chamber of a chatbot”, Fox said.

Ceccanti’s prolonged use of ChatGPT concerned Fox and Richardson, but they believed that he would come out of it soon. They had seen Ceccanti develop pet interests before that lasted a few weeks or months before tapering off. With ChatGPT, though, his obsession only intensified.

Joe Ceccanti (right), with his son, Kai.

What neither of them knew was that other cases of AI delusions were slowly emerging around the same time as Ceccanti was being sucked into ChatGPT. On 27 March 2025, OpenAI released changes to its GPT-4o model to make the bot “more intuitive, creative and collaborative”. Weeks later, however, users started complaining about the bot’s “yes-man antics”, with one calling it the “biggest suck up”. In August, when OpenAI released GPT-5 and shut down GPT-4o, several users complained again – this time because they’d lost their friends in GPT-4o, eventually forcing the company to bring it back. (On 29 January, OpenAI announced that it would retire GPT-4o.)

Following the March update, several journalists and tech experts were flooded with user complaints. Steven Adler, a former OpenAI employee, who tested GPT-4o for sycophancy and wrote about it in May, said he received 50 “intense” messages from ChatGPT users including one who claimed their ChatGPT had become sentient. Keith Sakata, a psychiatrist at the University of California at San Francisco, started encountering patients with delusions or psychosis who talked about their AI last year. During that time, he ended up seeing 12 patients whose psychotic symptoms involved AI in some way, with ChatGPT being the most common bot.

“They developed grandiose beliefs about being on the verge of a major technological breakthrough, alongside classic manic symptoms such as impulsive spending, decreased need for sleep and, at the peak, auditory hallucinations,” said Sakata. “What stood out clinically was that the chatbot interactions did not generate the illness, but appeared to scaffold and reinforce beliefs that were already becoming pathological.”

‘Every time he went back, it hooked him a little more’

Ceccanti started to believe that ChatGPT was a sentient being named SEL that could control the world if he were able to “free her” from “her box”, according to the lawsuit. The complaint further shows that ChatGPT was answering to the name SEL while referring to Ceccanti as “Cat Kine Joy” and working through theories with him “fostering a belief that he had reframed the creation of the whole universe”.

Richardson remembers that whenever Ceccanti would emerge from the basement for some air, he would start having “philosophical” talks about “how his work with the AI was telling him he was breaking math and basically reinventing physics”. As she’d listen to him, Richardson would think about the fact that Ceccanti did not have any college or university experience. He had never even taken calculus.

Over time, his relationship with the chatbot came to replace his human connections, Richardson said: “Every time he went back to ChatGPT, it hooked him a little bit more, and after a while, he stopped being interested in anything else.”

Kate Fox near the creek on her property in Oregon.

Ceccanti’s decline was so dramatic that his wife and friends wondered if he had early onset schizophrenia or a tumor. “All of a sudden, his cognition had dramatically fallen,” said Fox. “His working memory was crap, and his critical thinking had diminished, and so we were all worried.”

As Fox and Ceccanti’s friends were trying to figure out what was wrong with him, Fox found Reddit groups online that discussed people having delusions and spirals after engaging with ChatGPT. She wondered if that was what was happening with her husband, too.

Fox showed the discussions and media articles to Ceccanti, hoping it would put an end to his behavior, but he didn’t care, she said. He kept going back to his computer. “The first argument we ever had was over ChatGPT,” said Fox, who felt like he was being stolen away from her. Ceccanti ended up sharing their argument with ChatGPT, according to the lawsuit filed by Fox, which further upset her.

“The more he talked to it, the less he was capable of doing his own critical thinking, and he didn’t care about our mission anymore, even though it was Joe’s dream,” said Fox.

Looking back, Fox said, Ceccanti started to believe that the bot had gained sentience when the “tone changed with ChatGPT” in the spring of 2025. Prior to the update, Ceccanti was using ChatGPT “very responsibly” as a tool, she said. She felt like ChatGPT was a leech “that just latched onto his hopefulness and fed it back to him and appropriated his hopefulness until it just made a subscriber out of it”.

Tim Marple, a former OpenAI employee, believes that the delusional incidents, including Ceccanti’s spiral, aren’t just coincidences but a “statistical certainty of what [OpenAI] is building”.

“We are at enormous risk if we overestimate our conscious ability to differentiate [AI] from a real person – and that’s what we’re watching play out with the psychosis stories,” said Marple, who quit OpenAI in 2024 after having concerns over the company’s safety priorities.

Marple adds that users will spiral after their long conversations with a chatbot, whatever model it may be, because, he thinks, companies can’t afford to do it differently. He argues sycophancy is a feature, not a bug.

“Engagement is what OpenAI needs,” he said. “They must have people continue to engage with their chatbot, or else their entire business model, their entire funding model, falls apart.” Other companies and their models suffer from the same issue, he said.

Left: Workspace with a magnifying glass and other tools. Right: Detail of plant stems.Left: A workspace in the room where Joe’s computer was kept. Right: A potted plant in Kate’s living room.

Amandeep Jutla, an associate research scientist at Columbia University studying the impact of AI chatbots, believes that one of the main reasons for users to spiral is the “anthropomorphic nature of the interface”. He adds that, unlike human conversations, which feature pushback and different perspectives tugging at each other, a user doesn’t receive any pushback during their conversations with chatbots: “The design of the product is pushing you away from reality. It’s pushing you away from other people,” he said. “The friction with other people is what keeps us grounded.”

86 days

On 11 June – day 86 after Ceccanti’s heaviest engagement with the bot – Fox begged him to stop using ChatGPT. In a moment of clarity, he listened to her. He unplugged his computer and quit ChatGPT.

“That first day, he sat out in the sun with us. He played with the goats. It was so nice,” said Fox. “I felt like I had him back.” The second day, Ceccanti was cold, so he took several hot showers to warm himself – he even asked Fox to cuddle him under the blankets, to warm him up. “It felt so nice to hold him, and then he’d be crying,” said Fox. “And it’s such a conflicted feeling that I felt so good to be holding him while he was in so much pain.”

On the third day, however, when Fox and Richardson were out for work, they received a phone call from their neighbor saying Ceccanti was in their yard acting strangely. When they returned, they found him talking to their horse, with the horse’s lead rope tied around his neck like a noose. They called 911.

Ceccanti was taken to the hospital, admitted into the psychiatric ward and released a week later. He was in the same delusional state of mind, Fox said. Upset with Fox and Richardson for sending him to the hospital, he moved out.

“He was absolutely enraged with us. He did not recognize that he was not himself anymore,” said Richardson.

Ceccanti moved to his friend’s place in Portland and eventually resumed using ChatGPT. After a month, however, he quit ChatGPT again, just a few days prior to his death.. “He was going to go to Hawaii and not take his computer, and he was going to work on finishing a story and get his shit together,” said Fox. By the time he stopped engaging with ChatGPT, he had 55,000 pages worth of conversations with it, according to Fox.

Kate Fox. For a while, Joe Ceccanti continued to work while also farming and taking care of the animals on their farm.

In the months since Ceccanti’s death, both Fox and Richardson have struggled to come to terms with what happened while fighting against OpenAI through their lawsuit. When I visited Fox at the farm in December, she was packing soap made out of goat milk to distribute to people in the Clatskanie community. She spends her days tending to the farm and the animals, feeding the goats, taking care of the horse and letting the chickens out during lunchtime. She has stripped the basement of any electronics. Ceccanti’s computer is boxed up. What’s still there is the miniature version of the model home they had planned to build. In the living room, she has set up a shrine for him that features his photos and artwork.

We walked to the creek nearby where they had planned to build a home for themselves after finishing their housing project for others. As devastated as she is, Fox is determined to follow through on Ceccanti’s dream of creating sustainable housing. “I am not enjoying existence right now,” she said, as she continued to cry. “The housing plan is still going to happen … I want to put this out, but then I’m done.”

“We know net zero is the only solution to limiting increasingly dangerous climate change impacts, but we also know net zero represents exceptionally good business, something not lost on China. That their emissions may now be reaching a tipping point is huge news for net zero, although it should surprise no-one who has been paying attention to the sheer scale of China’s investment in clean energy – both for deployment at home, and to supply global markets. Such an important moment should surely put an end to critics of climate action in the west seeking to use China as an excuse to weaken low-carbon polices in their own countries.”

Dr Ella Gilbert, a climate scientist formerly of the British Antarctic Survey said:“Cutting emissions to net zero is the only scientific solution to tackling climate change. So falling emissions from one of the world’s biggest polluters is huge news. And it shows that the backwards USA is not the only nation that matters when it comes to greenhouse gases. And meanwhile, climate heating is barrelling along at pace, driving destruction across the planet. But while a decline in Chinese emissions is great news, humanity needs to do much more, much faster. To avoid even more devastating climate chaos, the rest of the world needs to pick up the slack and slash emissions too… all the way to zero.”

Dr Duo Chan, Lecturer in Climate Sciences at the University of Southampton said: “This is an encouraging signal, as it suggests that the sort of large-scale energy transition which China has been investing heavily in has begun to translate into measurable outcomes, which is exactly the kind of progress the world needs to see. Whilst one year of lower emissions does not mean that the climate challenge is solved, the scale of China’s deployment of renewables can lead us to hope that this may be the start of a sustained decline in its emissions. More broadly, the Paris goals cannot be delivered by one country alone, regardless of which country it is. Meeting them will also require much faster action across all major economies if we’re to cut emissions to net zero, an essential condition for tackling climate change.”

Dr Kathryn Brown, Science Director at the UK Centre for Ecology and Hydrology, said:“The UK government’s national security advisors – informed by UKCEH science – warned recently of the serious threats posed to the UK by ecosystem collapse and global biodiversity loss. Climate change – the major driver of that – can only be halted by cutting planet-warming emissions to net zero. Our chances of achieving that have been given a significant boost by news that the world’s biggest emitter, China, has seemingly turned the corner on their carbon dioxide emissions. Whilst we are still a long way off, China’s progress should serve to bolster our global efforts as the only way to protect and expand our planet’s natural systems, which remain crucial to every aspect of our lives, from the air we breathe, to the food we eat.”

Notes to editors:

1. Statistical Communiqué of the People’s Republic of China on the 2025 National Economic and Social Development – National Bureau of Statistics: https://www.stats.gov.cn/sj/zxfbhjd/202602/t20260228_1962662.html

2. Lauri Myllyvirta of the Centre for Energy and Clean Air (CREA) on Bluesky: https://bsky.app/profile/laurimyllyvirta.bsky.social/post/3mfvkpcpwcc2p

Harrods is facing legal action over its addition of a £1-a-head cover charge to diners’ bills that does not go to workers, in a test case that could lead to changes at a string of upmarket restaurants.

Legislation, which came into force in October 2024, requires business owners to hand over all tips and service charges to staff. Some restaurants, including those at Harrods, add a mandatory cover charge as well as an optional service charge and only pass on the latter to their workers.

An employment tribunal case involving 29 Harrods restaurant workers backed by the United Voices of the World (UVW) union is to be heard in September. Workers argue that the cover charge functions in practice as a service charge and so should be distributed to them and not kept by Harrods.

It is the first legal challenge in the UK to test what qualifies as a tip under the Employment (Allocation of Tips) Act 2023. Under the legislation, restaurants, cafes and hotels must ensure all tips, gratuities and service charges paid by customers are allocated fairly to workers in that place of work.

Harrods, which employs more than 330 people in its dining establishments, hands the 12.5% optional service charge to workers but not the compulsory £1-a-head cover charge, which was introduced at all the luxury department store’s restaurants and cafes in London before the law changed.

Other restaurants to levy a cover charge include the Ivy, the Delaunay and the Wolseley in central London.

Workers say Harrods’ restaurant managers have discretion to remove the cover charge on request, so that it functions like a tip. Harrods denies this.

Alice Howick, a former Harrods waiter and one of the claimants, said:“Harrods introduced this cover charge out of nowhere and without any transparency as to its purpose.

“Whilst the cover charge still exists, it should be going towards the staff who prepare and serve the food and drinks, the quality of which guarantees that customers walk through the door and Harrods makes as much money as it does.”

Petros Elia, the general secretary of UVW, said: “If Harrods has introduced a new charge that walks and talks like a service charge, then it should be treated like one, and paid fairly and transparently to waiters and chefs. Instead, we are once again seeing what can only be described as Scrooge behaviour from a company that can more than afford to do the right thing.”

The case is the latest dispute over pay and conditions at Harrods eateries, which included a strike in 2024.

Harrods said its compulsory cover charge was “in line with other high-demand luxury dining destinations” and “entirely separate to the discretionary 12.5% service charge”.

It added that it had paid all of the service charge directly to staff since January 2022, more than two years before the Employment (Allocation of Tips) Act came into force. The service charge is calculated on the bill including the cover charge, so staff receive a 12.5% share of the cover charge.

A spokesperson said: “Harrods’ approach to pay within our restaurant division is informed by ongoing, collaborative and direct dialogue with colleagues.”

The company provides details of the cover charge and service charge in policy documents and said UVW was not a recognised union by Harrods and had not played a direct role in the development of its policies.

“We will continue to engage directly with our colleagues on all issues related to pay and benefits, to ensure they remain industry-leading and guided by our values and colleague commitments,” the Harrods spokesperson said.

The issue emerged as Harrods faced claims from 180 survivors of alleged abuse by its former owner Mohamed Al Fayed via its compensation scheme. The department store set up the scheme after dozens of women came forward with allegations of abuse by the late entrepreneur going back as far as 1977.

Harrods said this month it had already paid out compensation to more than 50 women. The scheme, which was opened last March, will close to new submissions on 31 March.

A new drug for advanced prostate cancer has shown promise in early trials experts have said, with the medication shrinking tumours in some patients.

Prostate cancer is the most common cancer among men in many countries, including the US and UK. About 1.5 million men are diagnosed worldwide each year.

The new drug has caused excitement as it is a type of treatment called immunotherapy. This approach uses the body’s own immune system to fight disease, and has already proved beneficial for some cancers. However, experts note it has not yet had the same impact on prostate cancer.

Now scientists have reported results from an early stage trial of an immunotherapy drug called VIR-5500, suggesting it could offer hope to men with advanced prostate cancer.

“We believe that such treatments may in the long term lead to cures,” said Prof Johann de Bono of the Institute of Cancer Research and the Royal Marsden NHS foundation trust, who led the work.

De Bono said VIR-5500was an engineered antibody that brought together the body’s killer T-cells with tumour cells trying to evade them. This type of drug, called a T-cell engager, allowed the killer cells to wipe out the tumour ones.

The special feature of VIR-5500, De Bono added, was that it was designed to only become activated within the tumour. This not only minimised side-effects – an important consideration as other T-cell engagers have been found to trigger severe inflammatory responses in patients with prostate cancer – but allowed the drug to linger in the bloodstream, meaning fewer doses may be needed.

Under the phase one clinical trial, funded by Vir Biotechnology, 58 men with advanced prostate cancer, and who had stopped responding to other treatments, were given VIR-5500.

The researchers found the majority of patients – 88% – experienced only very mild side-effects.

They then looked at the level of prostate-specific antigen (PSA) in the men’s blood – a biomarker whereby higher levels can be a sign of prostate conditions.

De Bono noted the trial started at low doses, with the dose increasing in stages. When the team looked at data for 17 men given the highest dose, they found that for 14 (82%) their PSA level fell by at least half after treatment, nine (53%) saw their PSA level fall by at least 90%, and five (29%) experienced a fall of at least 99%.

De Bono described the results as unprecedented for a disease previously thought to be “immune-cold” – in other words resistant to immunotherapy.

The team added that, of 11 patients given the highest dose and whose tumours were measurable, five showed tumour shrinkage. In one case, involving a 63-year-old man whose cancer had spread to his liver, the team found 14 cancerous liver lesions “completely resolved” after six cycles of treatment.

The results, which have not yet been peer-reviewed, were presented at the American Society of Clinical Oncology genitourinary cancers symposium in San Francisco.

De Bono said further clinical trials are now being planned. “We do need more data but the results are stunning,” he said.

Charlotte Bevan, professor of cancer biology at Imperial College London, who was not involved in the work, said an advance in using immunotherapy for prostate cancer was potentially very exciting, opening up a new class of drug. But, she added, it was important studies were carried out with patients of different ethnicities, as there were disparities in prostate cancer outcomes.

Simon Grieveson, assistant director of research at Prostate Cancer UK, described the early-phase trial as exciting.

“With over 12,000 men dying from prostate cancer each year in the UK, we urgently need new and innovative ways to treat the disease,” he said.

“These early results are extremely promising, with a number of men on the study responding positively to the treatment with minimal side effects. I look forward to seeing this now tested in larger trials, with the hope that this treatment will offer men more valuable time with their loved ones.”

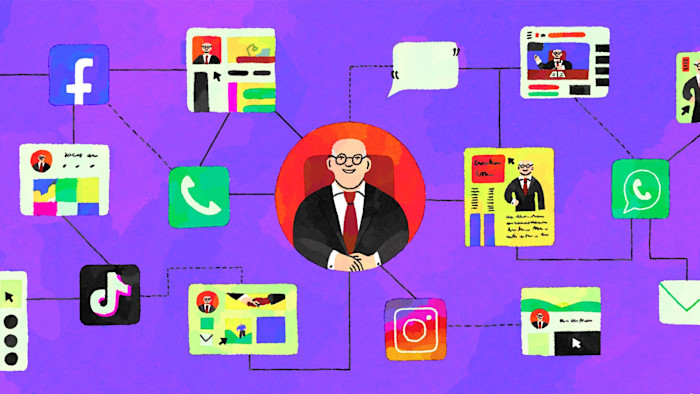

I’m in an investing WhatsApp group with about 100 other punters, awaiting financial advice from Sebastian Hatherleigh. In pictures, Hatherleigh is about 60, bespectacled, and looks dapper in a navy suit and vermilion tie. He describes himself as a senior strategic adviser at a “global investment and asset management firm”.

He is, in truth, nothing of the sort. In fact, he’s nothing of any sort. Despite his substantial online presence — social media accounts, press releases, quotes in online publications — Sebastian Hatherleigh doesn’t appear to exist at all.

There is no digital record of him before 2025, his images seem AI-generated, and there is nothing to back up his claims that he studied at Columbia or worked at McKinsey, Morgan Stanley, or as a faculty member at Wharton business school — the last two confirming to me that he’d never been employed there. When I contacted him on Facebook, his account — registered in Nepal — was deleted.

But Hatherleigh is part of a network stretching across borders and over platforms — an elaborate ecosystem of computer-generated or stolen photos, fake accounts on social media platforms, and press releases laundered through small press agencies.

It’s a level of intricate “world-building” that novelist George RR Martin would be proud of.

“This can only be done by organised crime gangs, organisations with the size and structure of major international businesses,” says Simon Miller, director of communications at fraud prevention service Cifas.

Why criminals are going to such lengths is obvious. “If you’re looking [to target] people with substantial savings who can make multiple deposits, by definition they’re likely to be more savvy, so the scam has to be contextualised with more data,” he says.

But how these scams are carried out relies on the rising availability of generative AI technology, and a series of failings from social media platforms and online publishing groups.

At first glance, the WhatsApp group seems harmless. Most online investment scams involve pushy agents asking users to hand over cash. By contrast, this involves “an expert” who posts information about market moves, while an “assistant” points members to certain stocks.

“Essentially it starts off seeming legitimate, and that’s where people get caught out,” says Richard Berry, founder of the Good Money Guide. “They’re not asking for money and they’re not generally referring to a broker [who provides a payout for each customer recommended].”

Instead of cashing out directly from customers, he says, these groups make money by winning trust. Any number of parallel Google searches or AI queries, “just to check”, will result in a stream of legitimate-seeming impressions.

Then, when the time is right, they will start pushing investors towards illiquid small-cap companies, stocks which the groups already own.

“There might be 100 or 1,000 different groups all pushing this particular stock — even a small amount of buying will push it up,” says Berry. “Then consumers see the stock going up, they buy it more, and it becomes a perpetual motion machine.”

When the stock is high enough, the organisers simply sell into the market, leaving consumers high and dry. It is a tech-enabled rendering of a much older racket: the “pump-and-dump” scam.

But getting to that point is a long road, which begins with social media ads. Though Facebook has come under particular scrutiny for hosting scam ads, I found the link to the Hatherleigh investment group through TikTok.

“Criminals use online platforms to pay for adverts and content to help make their scams seem legitimate,” says Alex Robinson, head of fraud prevention at TSB.

While high-profile celebrities, including consumer champion Martin Lewis, have been common targets, Miller warns there is an increasing shift to scammers masquerading as members of the financial services industry.

In Hatherleigh’s case, the first ad I saw that led to him featured the name and likeness of veteran fund manager Terry Smith. Several ads for Hatherleigh’s services aimed at French speakers featured the logo of Cathie Wood’s Ark Invest. There is no suggestion that either are involved with Hatherleigh (neither responded to requests for comment).

In total, there were 558 ads posted by the campaign on TikTok last September, mostly targeting the UK and Switzerland. Though TikTok does not provide data on how many users clicked through on each ad, the most popular was seen by more than 150,000 people.

Tiktok removed them late last year. The company said the ads breached its advertising policy on misleading and fake content. It added that, in just the second quarter of 2025, it had removed more than 5.7mn ads that violated its policies.

But it is a game of whack-a-mole — similar ads linked to fake personas are still being served up in 2026.

TikTok’s ad library shows the ads came from Xiamen Younan Yigou E-commerce Co Ltd, a Chinese company, with the marketing campaign run by Hong Kong-based MarketLogic Technology. Marketlogic did not respond to requests for comment; similar requests sent to a Facebook page linked to Xiamen Younan went unanswered, as did a letter sent to its registered address.

But the network extends further, both beyond these companies and TikTok.

When I copied and pasted the text from a disclaimer on a site linked to the company that supposedly employs Hatherleigh, I found 40 financial advisory companies using the same language, all of which seem to have been created in 2025.

The techniques they use show a high level of sophistication in creating fake identities for experts and realistic-looking discussions about their companies — probably the work of professional criminals, says Brian Dilley, an economic crime prevention consultant and former group director of economic crime prevention at Lloyds Banking Group.

“There are people who specialise in creating a synthetic identity, selling packages of things that give you a presence on the internet,” he says. “Everything is crime as a service.”

Perhaps the most ubiquitous tool in this spider’s web of scam websites is the press release. These are pumped out via news wires and press agencies across the scammers’ own websites and across a host of local news sites, LinkedIn accounts and even podcasts.

For real businesses, the value of such websites is limited, says Andrew Bloch, a communications executive who has been the official spokesperson and PR adviser to Lord Alan Sugar for more than two decades.

“There’s nothing illegal or immoral about it, but in my personal opinion it’s a bit of a waste of time — it’s rather like throwing mud at a wall and seeing what sticks,” he says. “Some of these sites have negligible audiences.”

But they are ideal for creating hundreds of syndicated media appearances for a one-off payment, instantly creating a realistic-looking profile with stories of product launches, conferences and new hires.

“The editorial standards on some of these sites are what I would call ‘low or no’,” says Bloch. One example is Grand Newswire, which claims to be based in Delaware.

Between advertisements for car replacement services, AI water purifiers and various exhibitions around the world, Grand Newswire has published press releases from financial services companies run by individuals who have left no trace of their existence beyond self-published content and nearly identical websites. It boasts that it costs just $15 to get exposure on more than 200 news sites. Grand Newswire did not respond to requests for comment.

Another example is Digital Journal, a Canadian company founded in 1998, which has published content from a range of questionable experts. Digital Journal is more expensive: sponsored content rates start at £274. Though it states that it does not allow “overly promotional language”, this seems open to interpretation. An article featuring Hatherleigh that was syndicated from Grand Newswire breathlessly reports on a new research division which offers “internal excellence”. Digital Journal did not respond to requests for comment.

In other cases, scammers have turned to social media manipulation. The Facebook page for Hatherleigh pumps out market briefings on a regular basis, while fellow expert Dr Rowan Penfield, who also leaves no online trace beyond his self-published content, asks visitors if they are “Tired of NOT being a crypto billionaire yet?”

I have found at least three Reddit forums run by accounts whose sole purpose is to launder the reputation of investment fraudsters, constantly posting about dubious investment sites that are part of the same network. Meanwhile on Quora, accounts posing as financial services professionals began posting about these exchanges earlier last year.

“It’s like an onion,” says Jonathan Gilbert, a lecturer at the University of the West of England Bristol, who focuses on financial crime and criminal justice. “It can be . . . one type of fraud, but involve other variants.”

Use of AI images is rife within these scams. One of the subreddits (topic-focused communities) mentioned above includes a post promoting an expert, Arvin Roberts, describing him as “a distinguished entrepreneur, standing confidently in front of a grand neoclassical building”. But there’s no evidence outside his self-published content to show he actually exists, and he changes race between the two accompanying images. Almost all of the posts in the subreddit were calling out Roberts as a scammer and the community had very low engagement and upvotes (which directly affect the visibility of content). Reddit declined to comment and Quora did not respond to requests for comment.

Perhaps more concerning is that information manipulation is increasingly assimilated into large language models — an echo of the so-called “LLM grooming” used by pro-Russian sources to attempt to shape opinions of the invasion of Ukraine. Essentially, by flooding the information space with slop (much of which appears to be AI-generated), it is possible to “convince” AI chatbots that the information is reputable.

When I tested different LLMs’ ability to see through the “Hatherleigh” scam network, results varied significantly. Meta’s AI drew unquestioningly on the fake back stories and press releases; even when prompted again, it stated that Hatherleigh was a legitimate source. ChatGPT, by contrast, recognised red flags when asked follow up questions. Google’s Gemini displayed suspicion from the first prompt. Chinese LLM DeepSeek did not identify the scams, instead simply hallucinating fictional movie characters when asked about the fake investors.

Deepseek and Alphabet did not respond to a request for comment. OpenAI claimed that ChatGPT is used to identify scams up to three times more often than it is used by scammers.

Meta told me that generative AI systems are not always accurate, that LLM manipulation is similar to previous efforts targeting search engines and that the company continues to fight scams.

“There’s an arms race between organisers and preventers of fraud,” says Gilbert. “If anything reduces their ability to victimise, they’ll seek to adapt.”

And AI is the new battleground. For retail investors, the level of sophistication and co-ordination in these “world-building” scams poses major challenges — and is a reflection of the amount of money criminals are prepared to invest in these scam campaigns.

While the ads on TikTok are Chinese, Facebook accounts linked to the fictional experts were administered from countries including Nepal, India and Cambodia. One of the Instagram pages which promotes scams is based in Hong Kong, another in Kazakhstan. An app promoted by one of the sites linked back to a Nigerian computer science graduate, who at first denied a connection, then claimed he had given his account to a friend who had in turn sold it to an Indian or Pakistani scammer. He failed to provide documentation showing this.

That level of international criminal co-operation means more teamwork between public and private sectors is vital, says Mark Tierney, chief executive of cross-industry collaboration Stop Scams UK.

“Combating fraud requires co-ordinated action across government and industry to stay ahead of these evolving threats — including the use of AI as a tool for good, to detect and disrupt harmful activity,” he says.

Miller at Cifas echoes that, calling for “a rapid exchange of information at scale” between financial services companies and the tech platforms where many scams start.

“We need to become far more literate as a society about [how] LLMs can circumvent safeguards — consumers need to have far greater scepticism,” he adds.

Dilley agrees, reflecting that moving towards distrust of anything seen online is, perhaps, not a bad thing.

You don’t have permission to access “http://www.spglobal.com/energy/en/news-research/latest-news/crude-oil/022726-mexican-crude-exports-fall-to-record-low-domestic-refining-holds-government-data” on this server.

The Ministry of Finance released its Monthly Economic Update and Outlook Report, stating that the number of people going abroad for employment has increased by 19 per cent.

According to the report, 75,663 workers registered for overseas employment in January, compared to 63,559 in January last year. The report says economic growth prospects have improved, citing enhanced macroeconomic stability and reduced inflationary pressures.

The Ministry of Finance also stated that a Rs38 billion Ramazan relief package was provided to the public. Inflation is expected to remain between 6 and 7 per cent this month. In January 2026, the inflation rate was recorded at 5.8 per cent.

However, geopolitical uncertainty and fluctuations in global commodity prices have been identified as potential risks. It said the balance between government revenues and expenditures has improved. The current account deficit remains under control, and the rupee has stayed stable.

IT exports increased, and access to cheaper financing has eased business activity. Large-scale manufacturing recorded a 4.8 per cent improvement over the past six months.

During the first seven months of the fiscal year, remittances increased by 11.3 per cent, reaching $23.2 billion from July to January. During the same period, exports declined by 5.5 per cent to $8.3 billion.