- AI hallucinations haunt users more than job losses Financial Times

- Who’s most optimistic about AI — and who isn’t, according to Anthropic CNBC

- What 81,000 people want and don’t want from AI, Anthropic study Euronews.com

- AI’s role in creative pursuits isn’t a priority for users NewsBytes

- Anthropic Releases Findings from Global User Study on AI Expectations and Concerns MLQ.ai

Category: 3. Business

-

AI hallucinations haunt users more than job losses – Financial Times

-

As War Disrupts the Gulf, India’s Growth Story Faces New Risks – The New York Times

- As War Disrupts the Gulf, India’s Growth Story Faces New Risks The New York Times

- Iran war: Gas shortage risks pushing India towards polluting fuels BBC

- Strait of Hormuz disruption could hit Indias LPG supplies, refined product markets more severe than crude oil markets: Report Zee News

- The Great Indian Energy Paradox The New Indian Express

- India’s crude imports took a big hit due to the West Asia Crisis: Systematix Research ANI News

Continue Reading

-

15th Five-Year Plan will create broader market opportunities for multinational corporations

15th Five-Year Plan will create broader market opportunities for multinational corporations

BEIJING, March 21 — During the 15th Five-Year Plan period (2026-2030), China will unswervingly expand high-level opening up and promote high-quality development, which will create wider market opportunities for multinational corporations, Chinese Vice Premier He Lifeng said in Beijing on Saturday.

He, also a member of the Political Bureau of the Communist Party of China Central Committee, made the remarks when meeting with senior representatives of well-known multinational corporations including HSBC, UBS, Louis Dreyfus, Siemens Healthineers, Schneider Electric, Rio Tinto, Prudential, Investor AB, Standard Chartered, Suzano and TCP Group.

He noted that China’s economy is making progress while maintaining overall stability, and pushing forward with innovation-led and high-quality development, adding that China welcomes multinational corporations to increase investment in China and continuously deepen mutually beneficial cooperation.

Representatives of the multinational corporations expressed confidence in China’s economy and stated their readiness to further explore the Chinese market and continue to expand investment in China.

Continue Reading

-

Business investment in the era of digital transformation

Business investment has been disappointingly weak across the OECD since the Global Financial Crisis (GFC), which has contributed to slow potential growth and stagnating living standards, particularly in large parts of Europe (Draghi 2024, Andre and Gal 2024). Some of this weakness may be explained by subdued demand and elevated uncertainty (Dlugosch et al. 2025).

Yet one component has been anything but sluggish: investment in digital assets, such as hardware, software, and databases. In our new paper (Gal et al. 2026), we use detailed national accounts data by asset type and sector for 32 OECD countries (1995–2023) to document striking differences in the investment dynamics across digital and non-digital assets. In addition, we find an important divergence across countries, with the US and a few other countries from the Baltics and Central and Eastern Europe showing relatively strong performance.

Digital investment has pulled ahead of other asset classes

Across the OECD, real investment in digital assets has risen strongly for two decades and was notably resilient during both the GFC and the Covid-19 shock (Figure 1). Since 2007, average real digital investment across OECD economies increased by over 130%. Within this broad category, ICT hardware roughly doubled while software and databases almost tripled. In contrast, real business investment in non-digital tangible assets has barely grown since the GFC, with volumes only slightly above their 2007 level. With the rising importance and rapid diffusion of artificial intelligence and related technologies (Filippucci et al. 2024), digital assets are likely to matter even more (Carpinelli et al. 2026).

Figure 1 Digital investment has outpaced other investment types across the OECD, most strongly in the US

Note: Aggregates are GDP-PPP weighted; Ireland excluded due to a 2015 series break.

Source: OECD National Accounts Database and OECD calculations, see details in Gal et al (2026).Digital investment is rising in all major OECD regions, but the slope differs sharply. The contrast is strongest in the US, where both ICT hardware, and software and data investment accelerate markedly after the mid-2010s, reaching 3-4 times higher volumes by 2023 than in 2007. Western European economies (EU-15 in Figure 1) also expanded digital investment, but at a slower pace, with only a 1.5–2-fold increase over the same period. Japan lags further behind. A plausible interpretation is that the mid-2010s acceleration coincided with the commercialisation of cloud computing and the broader diffusion of data-intensive and AI-enabled applications, which raised demand for software, data management, and computing capacity.

Nearly all of the US outperformance in investments is due to digital assets

A decomposition of business investment growth by asset type shows that digital assets account for almost the entire gap between US business investment growth and that of the rest of the OECD over the past decade (Figure 2, Panel A). From 2014–2023, US business investment grew about 2 percentage points faster per year than the rest of the OECD, and almost all of that gap reflects faster digital investment. Robustness checks suggest this is not driven by price-measurement choices or by a shift from buying to renting digital services.

Figure 2 Digital investment accounts for almost 90 % of the gap in business investment growth between the US and other OECD countries over the past decade

Note: Average annual real business investment growth (2014–23). Panel B shows the US–OECD (ex-US) growth gap split by asset type; digital is split into ICT and non-ICT sectors. OECD aggregates are GDP-PPP weighted.

Source: OECD National Accounts Database and OECD calculations, see details in Gal et al (2026).When decomposing the ‘investment-growth gap’ between US and the rest of the OECD, we find that stronger growth in digital investment explains nearly 90% of the outperformance of the US. Moreover, most of this gap reflects higher digital investment outside the tech sector in the US – consistent with an economy-wide broader diffusion of digital technologies there. Splitting the digital component of the gap into ICT sectors versus the rest of the economy, we find that only about 40% of the digital-investment gap comes from the ICT-producing and ICT-service sectors themselves (Figure 2, Panel B).

Digging deeper, in our firm level analysis we find that the so-called ‘Magnificent 7’ Big Tech companies accounted for a quarter of total digital investment in the US – a significant but not a dominant share. Both sector- and firm-level evidence points to the prevalence of digital intensity in the US. This in turn suggests that economy-wide differences in the incentives and capabilities to invest in, adopt, and scale-up digital technologies play an important role.

Digital capital is diverging across countries

Investment is a flow; what shapes productive capacity is the resulting capital stock. Digital assets – think of computers and software – depreciate rapidly, at a rate of more than 25% per year compared to 5-20% for non-digital assets such as buildings and machinery (OECD, 2025). Therefore, strong gross investment is required to build and maintain a sizable ‘digital capital’ base. Despite faster depreciation, digital capital accumulation has indeed outpaced that of most other assets, given the rapid rise of digital investment. However, this accumulation has been very uneven across countries.

Figure 3 contrasts the cross-country dynamics of total capital per worker (Panel A) with digital capital per worker (Panel B). Total capital shows a familiar convergence pattern: economies with lower initial capital per worker tend to grow faster, catching up over time. Digital capital does not. The United States starts from a high level and continues to accumulate quickly, pulling further ahead. Moreover, countries with smaller initial digital capital bases often record slower subsequent digital capital growth (e.g. Germany, Canada), implying ‘falling behind’ dynamics rather than catch-up in terms of digital capital. As digital capital becomes increasingly central to productivity growth – a plausible scenario given the diffusion of AI, cloud computing, and data-intensive business processes – divergence in digital capital per worker could translate into more persistent divergence in productivity and incomes.

Figure 3 Lack of convergence in digital capital stocks per worker

a) Growth over the past ten years and initial levels: total capital per worker

b) Growth over the past ten years and initial levels: digital capital per worker

Note: Capital–labour ratios are calculated using the working-age population, defined as individuals aged 16–64. Capital stock is converted into USD using GDP-based purchasing power parities (PPPs), as no specific PPPs for capital stocks exist.

Source: OECD National Accounts Database and OECD calculations.What role for government policies?

A few policy areas stand out as likely candidates to explain cross-country differences in investment performance, especially through stronger potential impacts on digital investments.

Access to finance

A large part of digital assets are intangible (software and databases) and have limited collateral value, yet frequently require sizable upfront spending and rapid replacement. That combination can make digital investment particularly sensitive to financing conditions and to the structure of capital markets. Policies that deepen equity financing, support venture capital, and more improve the financing environment have been shown to be effective regarding intangibles (Demmou and Franco 2021).

Labour markets and complementary intangibles

Digital assets are productive only when complemented with a range of intangibles such as skills, organisational capital, data governance, and (often) R&D (Pisu et al 2021, Sorbe et al. 2019). Cross-country differences in digital investment are likely to reflect differences in these complements. Policies that raise digital skills, reduce adoption costs and do not penalise experimentation with new technologies through excessive labour regulation can encourage technology diffusion through new investments across firms and sectors.

Scale, competition, and market fragmentation

Digital technologies tend to feature high fixed costs and scale economies (McMahon et al. 2024). Barriers to scaling up – including across borders – and weak competitive pressure can reduce incentives to undertake large, risky digital investments. These factors seem particularly relevant in explaining the US-EU investment performance gap, given the more unified US internal market (Cerdeiro and Rotunno 2026).

Digital investment has become the bright spot in an otherwise subdued business investment environment. It has also been a leading factor driving cross-country differences and in particular the growing digital capital gap between the US and the rest of the OECD. A better understanding of the reasons and policy levers is critical, given that investment in new technologies is a key driver of sustained stronger productivity growth and, in turn, rising living standards.

References

André, C and P Gal (2024), “Reviving productivity growth: A review of policies”, OECD Economics Department Working Paper No. 1822.

Carpinelli, L, F Natoli and M Taboga (2026), “From AI investment to GDP growth: An ecosystem view”, VoxEU.org.

Cerdeiro, D A and L Rotunno (2026), “EU barriers to scaling up: The case of fragmented product markets”, VoxEU.org.

Demmou, L and G Franco (2021), “Mind the financing gap: Enhancing the contribution of intangible assets to productivity”, OECD Economics Department Working Paper No. 1681.

Dlugosch, D, M Glanville, J Hooley, F Ozturk and B Westmore (2025), “Understanding the weakness in business investment”, OECD Economics Department Working Paper 1836.

Draghi, M (2024), The Future of European Competitiveness – A Competitiveness Strategy for Europe.

Gal, P, J Hooley, F Ozturk and F Unsal (2026), “Business investment in the face of the digital transformation: Initial evidence”, OECD Economics Department Working Paper No. 1859.

McMahon, M, S calligaris, E Doyle and S Kinsella (2021), “Scale, market power and competition in a digital world: Is bigger better?”, OECD Science, Technology and Industry Working Paper No. 2021/01.

OECD (2025), “Annual capital formation by economic activity and Fixed assets by economic activity and by asset”, National Accounts Database.

Pisu, M, C von Rüden, H Hwang and G Nicoletti (2021), “Spurring growth and closing gaps through digitalisation in a post-COVID world: Policies to LIFT all boats”, OECD Economic Policy Paper No. 30.

Schoefer, B (2025), “Eurosclerosis at 40: Labor Market Institutions, Dyanamism, and European Competitiveness”, NBER Working Paper No. 33975.

Sorbe, S, P Gal, G Nicoletti and C Timiliotis (2019), “Digital Dividend: Policies to Harness the Productivity Potential of Digital Technologies”, OECD Economic Policy Paper No. 26.

Continue Reading

-

Thousands of people are selling their identities to train AI – but at what cost? | AI (artificial intelligence)

One morning last year, Jacobus Louw set out on his daily neighborhood walk to feed the seagulls he finds along the way. Except this time, he recorded several videos of his feet and the view as he walked on the pavement. The video earned him $14, about 10 times the country’s minimum wage, or for Louw, a 27-year-old based in Cape Town, South Africa, half a week’s worth of groceries.

The video was for an “Urban Navigation” task Louw found on Kled AI, an app that pays contributors for uploading their data, such as videos and photos, to train artificial intelligence models. In a couple of weeks, Louw made $50 by uploading pictures and videos of his everyday life.

Thousands of miles away in Ranchi, India, Sahil Tigga, a 22-year-old student, regularly earns money by letting Silencio, which crowdsources audio data for AI training, access his phone’s microphone to capture ambient city noise, such as inside a restaurant or traffic at a busy junction. He also uploads recordings of his voice. Sahil travels to capture unique settings, like hotel lobbies not yet documented on Silencio’s map. He earns over $100 a month doing this, enough to cover all his food expenses.

And in Chicago, Ramelio Hill, an 18-year-old welding apprentice, made a couple hundred dollars by selling his private phone chats with friends and family to Neon Mobile, a conversational AI training platform that pays $0.50 per minute. For Hill, the calculation was simple: he figured tech companies already capture so much of his private data, so he might as well get a cut of the profit.

These gig AI trainers – who upload everything from scenes around them to photos, videos and audio of themselves – are at the frontlines of a new global data gold rush. As Silicon Valley’s hunger for high-quality, human-grade data outpaces what can be scraped from the open internet, a thriving industry of data marketplaces has emerged to bridge the gap. From Cape Town to Chicago, thousands of people are now micro-licensing their biometric identities and intimate data to train the next generation of AI.

But this new gig economy comes with trade-offs. In exchange for a few dollars, its trainers are fueling an industry that may eventually render their skills obsolete, while leaving some of them vulnerable to a future of deepfakes, identity theft and digital exploitation that they are only just beginning to understand.

Keeping the AI wheel spinning

AI’s language models, such as ChatGPT and Gemini, demand vast troves of learning material to improve, but they’re facing a data drought. The most used training sources, such as C4, RefinedWeb and Dolma, which account for a quarter of the highest-quality datasets on the web, are now restricting generative AI companies from training models with their data. Researchers estimate AI companies will run out of fresh high-quality text to train on as soon as 2026. While some labs have resorted to feeding back the synthetic data their AI generates, such a recursive process can lead models to produce error-filled slop that causes their collapse.

Gig AI trainers, who upload everything from scenes around them to photos, videos, and audio of themselves, are at the frontlines of a new global data gold rush. Photograph: Arun Sankar/AFP via Getty Images This is where apps such as Kled AI and Silencio step in. On these kinds of data marketplaces, millions are monetizing their identities to feed and train AI. Beyond Kled AI, Silencio and Neon Mobile, there are many options for AI trainers: Luel AI, backed by famed startup incubator Y-Combinator, sources multilingual conversations for about $0.15 a minute. ElevenLabs allows you to digitally clone your voice and let anyone use it for a base fee of $0.02 a minute.

Gig AI training is a new emerging category of work, and it will grow substantially, said Bouke Klein Teeselink, an economics professor at King’s College London.

AI companies know that paying people to license their data helps avoid the risk of copyright disputes they could face if they relied entirely on content scraped from the web, Tesselink said. These companies also need high-quality data in order to model new, improved behaviours in their systems, said Veniamin Veselovsky, an AI researcher. “Human data, for now, is the gold standard to sample from outside of the distribution of the model,” Veselovsky added.

The humans fueling the machines, particularly those in developing countries, often need the money and have few other options for earning it. For many gig AI trainers, doing this work is a pragmatic response to economic disparity. In countries with high unemployment and devalued currencies, earning US currency is often more stable and rewarding than local jobs. Some of them struggle to secure entry-level jobs, and do AI training out of necessity. Even in wealthier nations, the rising cost of living has turned selling oneself into a logical financial pivot.

However, the pitfalls of gig AI training can be invisible. On some AI marketplaces, data trainers grant irrevocable, royalty-free licenses that allow companies to create “derivative works”, meaning a 20-minute voice recording today could power an AI customer service bot for the next few years, with the trainer never seeing another cent. Plus, due to the lack of transparency in these marketplaces, a user’s face could end up in a facial recognition database or a predatory advertisement half a world away, with virtually no legal recourse.

Louw, the AI trainer in Cape Town, is aware of the privacy trade-offs. And though the income is erratic and not sufficient to cover his full monthly expenses, he is willing to accept these conditions to earn money. He struggled with a nervous disorder for years and couldn’t secure a job, but money earned on AI marketplaces, including Kled AI, allowed him to save up for a $500 spa training course to become a masseur.

“As a South African, being paid in USD is more worth it than people think,” Louw said.

Mark Graham, a professor of internet geography at the University of Oxford and author of Feeding the Machine, acknowledged that for individuals in developing countries, the money can be meaningful in the short term, but warned that “structurally this work is precarious, non-progressive and effectively a dead end”.

AI marketplaces rely on a “race to the bottom in wages”, added Graham, and a “temporary demand for human data”. Once this demand shifts, “workers are left with no protections, no transferable skills, and no safety net”.

The only winner that emerges, Graham said, are “the platforms in the global north [that] capture all the enduring value”.

Cape Town, South Africa. Photograph: Peter Titmuss/Universal Images Group/Getty Images Carte blanche permissions

Hill, the Chicago-based AI trainer, had conflicting feelings about selling his private phone calls to Neon Mobile. For about 11 hours of calls, he earned $200, but he said the app would frequently go offline and fail to release overdue payments. “Neon was always shady to me, but I kept using it to get some extra, easy money for bills and other miscellaneous expenses,” said Hill.

Now he’s reconsidering how easy that money was. In September, just weeks after it had launched, Neon Mobile went offline after TechCrunch discovered a security flaw that allowed anyone to access the phone numbers, call recordings and transcripts of users. Hill said Neon Mobile never informed him about this, and now he’s worried how his voice may be misused on the internet.

What Jennifer King, a data privacy researcher at the Stanford Institute for Human-Centered Artificial Intelligence, finds concerning is that AI marketplaces are unclear about how and where users’ data will be deployed. Without negotiating or knowing their rights, she added, “consumers run a risk of their data being repurposed in ways that they don’t like or didn’t understand or anticipate, and they’ll have little recourse if so”.

When AI trainers share their data on Neon Mobile and Kled AI, they’re granting a carte blanche license (worldwide, exclusive, irrevocable, transferable and royalty-free) to sell, use, publicly display and store their likeness – and even create derivative works of them.

Kled AI’s founder, Avi Patel, said his company’s data agreements limit use to AI training and research purposes. “The entire business depends on user trust. If contributors believe their data could be misused, the platform stops working.” He said his company vets businesses before selling datasets, to avoid working with those with “questionable intent”, such as pornography, and “government bodies” that they believe could use the data in ways that conflict with that trust.

Neon Mobile did not respond to a request for comment.

According to Enrico Bonadio, a law professor at City St George’s, University of London, the terms of these agreements permit the platforms, as well as its clients, to do “almost anything with that material, forever, with no further payment and no realistic way for the contributor to withdraw consent or meaningfully renegotiate”.

More troubling risks include trainers’ data being used for deepfakes and impersonation. Even though data marketplaces claim to strip the data of any identification, like name and location, before selling it, biometric patterns are, by nature, hard to anonymise in a robust sense, added Bonadio.

Seller’s regret

Even when AI trainers are able to negotiate more nuanced protections for how their data will be used, they can still feel regret. When Adam Coy, an actor from New York, sold his likeness in 2024 for $1,000 to Captions, an AI-powered video editor that’s now called Mirage, his agreement ensured his identity wouldn’t be used for any political means or for selling alcohol, tobacco or pornography, and that the license would expire in a year.

Captions did not respond to a request for comment.

Not long after, Adam’s friends started forwarding him videos they’d found online featuring his face and voice garnering millions of views. In one of these videos, an Instagram reel, Adam’s AI replica claims to be a “vagina doctor” and promotes unproven medical supplements for pregnant and postpartum women.

“It felt embarrassing to explain it to people,” Coy said.

“The comments are strange to read because they comment on my physical appearance, but it’s not really me,” Coy added. “My feeling [while deciding to sell my likeness] was that most models were going to be scraping the internet for data and likeness [anyway], so may as well be paid for it.”

Coy said he hasn’t signed up for any AI data gigs since. He’d only consider it, he said, if a company offered major compensation.

Continue Reading

-

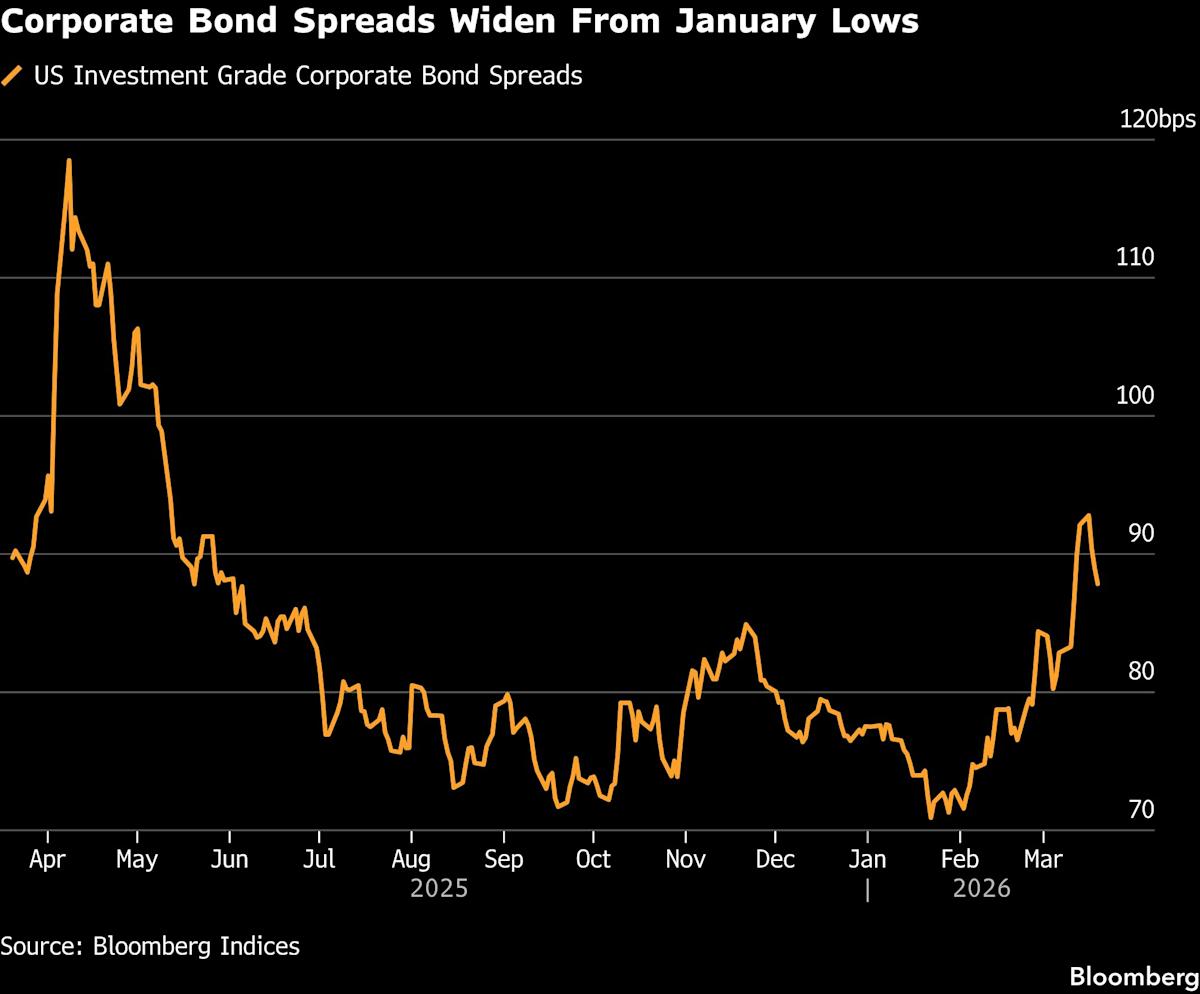

State Street, Voya Seek Shelter From Default Risk

Bloomberg Indices (Bloomberg) — As rising energy prices and growing inflation fears make corporate bonds look increasingly risky, big money managers including State Street and Voya Investment Management have been looking at buying mortgage bonds and other securitized debt instead.

Mortgage bonds often perform better than US high-grade corporate debt in “risk off” markets where investors are becoming more fearful, wrote Spencer Rogers, strategist at Goldman Sachs, in a note this week.

Most Read from Bloomberg

The debt is getting extra support now from Fannie Mae and Freddie Mac, after US President Donald Trump in January directed the companies to buy another $200 billion of the bonds. It’s worth looking at mortgage bonds that might perform better if rates fall again, Rogers wrote. For instance, purchasing specified pools designed to protect against higher prepayment speeds means investors can hang on to those cashflows for longer as rates fall.

Meanwhile, there’s ample reason to be worried about corporate debt. Crude oil futures have surged amid the US and Israeli attacks on Iran, and Iran’s retaliation on energy sites in nearby countries. West Texas Intermediate futures topped the $95-a-barrel range this week, compared with $57.42 at the end of last year. Prices in other markets are rising even more. Higher energy prices can effectively act as a tax on manufacturers and consumers, and can weigh on profits.

Higher oil prices may also make it harder for the Federal Reserve to continue cutting rates. On Wednesday, Fed Chair Jerome Powell said that central banks usually view higher energy prices as transitory, but inflation has been above the Fed’s 2% target for five years, implying that the central bank has less leeway to dismiss higher oil prices now. Bond traders are no longer pricing in any US rate cuts this year.

If rates stay higher for longer than expected, corporate profits could be hit as future borrowing costs rise. That’s at least part of the reason that US high-grade corporate bond spreads have widened by about 0.17 percentage point from their Jan. 22 lows. It may also be part of why the bonds have lost value this year on a total return basis.

Mortgage bonds, meanwhile, have gained a bit, according to Bloomberg index data. The securities look attractive from a relative value standpoint compared with corporate bonds, said Matthew Nest, global head of active fixed income at State Street Investment Management.

Continue Reading

-

Trump’s economic shocks are derailing Britain’s building plans | Phillip Inman

Donald Trump has done his best to crush the green shoots of the global, post-pandemic economic recovery – nowhere more so than in the UK.

The US president’s vandalism can be seen across the economic landscape, especially in the property sector, which has become more sensitive to international events since the spread of Covid-19 disrupted long-established supply chains and sent the cost of raw materials soaring.

What should be a strictly domestic consideration – what to build and where – has been shaped by the backwash from one geopolitical crisis after another, inducing a long period of stasis.

The latest UK industry statistics come hot on the heels of Trump’s attack on Iran.

The data provider Glenigan said last week the value of new projects had dropped by more than a third in the three months to the end of February.

Projects in the category marked “major works” – worth more than £100m – have suffered the most. Last November, with Rachel Reeves signalling a relatively benign budget, major developers were gung-ho and the number of major projects was on the rise. Not any more. Trump has slammed on the brakes.

Office building, civil engineering projects and residential housing are all affected by the slowdown.

It might seem strange to focus on how many spades are going into the ground across the UK when Trump’s epic miscalculation in the Middle East is having far-reaching effects beyond the property industry. With Iran almost certain to exact a high price by keeping oil and gas prices elevated, there could be terminal knock-on effects for liberal democracies facing yet another inflation shock.

Nevertheless, the UK economy is underpinned by an obsession with property, and the failure to get the market moving is another major blow to Reeves’s growth plans.

In many ways, Britain’s economy is principally a property market with a sideline in other services and manufacturing. The financial services sector is underpinned by property wealth and makes its money from loans tied to homes, offices and factories. Buying and selling property is a national pastime, along with the surveying, designing and maintaining it.

The UK runs a current account deficit because it buys more from abroad than it sells, and this gap is largely closed by selling assets, much of it property.

Consumer spending, too, is affected by people moving home and buying new things. More than that, spending reflects how wealthy people feel – and most of their wealth is in property.

Much of the difficulty faced by building firms, property developers and the servicing companies that facilitate deals stems from the reluctance of consumers to buy homes. Of course, affordability plays a big part in any decision, but there is also a risk in making such a large purchase even when you have the means.

In January, Trump threatened Greenland’s existence as an independent nation under Danish protection. At the time it felt like a bizarre but damaging conflict was coming to Europe courtesy of the Pentagon. In February, the US supreme court ruled Trump’s tariffs illegal, only for the president to impose a fresh set of import charges that bypassed the judgment. Then came the Iran conflict.

Much of the Glenigan survey covered this period of extreme instability, casting a cloud over the industry, as it has over manufacturing and the services sector since Trump began pushing the boundaries of presidential power.

Allan Wilen, Glenigan’s economics director, said: “We’re in a deeply worrying position where market volatility means prices are erratically fluctuating on a daily basis, dictated by the direction of international affairs. As our results show, the decline in construction activity has deepened and hopes for a recovery in the second half of the year now hang in the balance.”

It presents Reeves and local councils with a double dilemma. The first relates to the current slowdown and the loss of tax income as projects remain stuck. The second relates to the housebuilding sector and the over-reliance on the private sector to bring forward schemes.

While developers want a steady stream of work and dislike the disruption caused by Trump as much as anyone, it does provide an opportunity to turn the screw on public authorities – pushing them to drop requirements for public amenities and to target buildings at more affluent buyers.

There are growing reports from around the country of developers demanding cuts in the number of affordable homes.

For instance, British Land is in dispute with Southwark council over a tower the developer wants to make taller while cutting the number of affordable apartments from 35% to 3%. The London mayor, Sadiq Khan, has said he will adjudicate on the dispute.

It will not be the last case – just a small instance of a much larger problem. It also shows that Labour’s aversion to directly managing these housing projects, rather than trying to control them from a distance, needs to end.

Councils and mayors need to be the commissioners for all new schemes, with building firms as contractors. If the Dutch can do it, then so can the UK.

Trump is going to be around for several more years and greater self-sufficiency is going to be paramount. It is clear that if housebuilding is left to the private sector, we will be denied the homes, amenities, workspaces and landscapes we deserve. The sector will remain in the doldrums and continue to miss all government targets.

Continue Reading

-

Salesforce (CRM) Partners with NVIDIA for AI Agents in Enterprise Business Workflows

Salesforce, Inc. (NYSE:CRM) is one of the 10 Best AI Stocks to Buy for the Next 10 Years. On March 16, Salesforce, Inc. (NYSE:CRM) announced a partnership with NVIDIA Corporation (NASDAQ:NVDA) to use its Agentforce platform and NVIDIA’s Nemotron models to bring AI agents into enterprise business workflows.

This partnership connects Salesforce, Inc.’s (NYSE:CRM) Agentforce platform with NVIDIA’s Agent Toolkit, making it possible to use AI agents in both regulated and on-premises environments. This will give employees access to AI agents through Slack, while still keeping strong data governance and compliance standards in place.

Salesforce (CRM) Partners with NVIDIA for AI Agents in Enterprise Business Workflows According to the report, NVIDIA Nemotron 3 Nano has been added to Agentforce. This model features a 1 million token context window, allowing agents to process long customer histories and complex workflows. Nemotron 3 Nano uses a Mixture of Experts design, which helps lower computing costs in multi-step agent operations.

The system uses Slack as a coordination layer. Slackbot receives user requests, activates Agentforce workflows, and manages agent actions across enterprise systems. Users will be able to simply send requests in Slack, which would trigger Agentforce workflows. Data will be processed through Nemotron models and actions will be completed across connected business systems.

Salesforce, Inc. (NYSE:CRM) is a leading American AI cloud-based software company that specializes in customer relationship management (CRM) solutions. The company offers software, tools, services, and applications for sales, customer service, marketing, e-commerce, and analytics.

While we acknowledge the potential of CRM as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you’re looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

READ NEXT: 11 Best Tech Stocks Under $50 to Buy Now and 10 Best Stocks Under $20 to Buy According to Hedge Funds.

Disclosure: None. Follow Insider Monkey on Google News.

Continue Reading

-

RBC Capital and Jefferies Keep Bullish Ratings on Microsoft (MSFT)

Microsoft Corporation (NASDAQ:MSFT) is one of the 10 Best AI Stocks to Buy for the Next 10 Years. On March 11, RBC Capital reiterated its Outperform rating on Microsoft Corporation (NASDAQ:MSFT) with a price target of $640 on the stock.

Earlier, on March 5, Jefferies also reiterated its Buy rating on Microsoft Corporation (NASDAQ:MSFT) with a price target of $675 after meeting with the company’s head of investor relations. Jefferies pointed to the company’s end-to-end platform that combines Azure and Microsoft 365 (M365), which helps bring enterprise AI spending together. Microsoft Corporation (NASDAQ:MSFT) already supports more than 450 million paid M365 users with its enterprise distribution network.

RBC Capital and Jefferies Keep Bullish Ratings on Microsoft (MSFT) Jefferies highlighted that AI is increasing the total addressable market for M365. The firm also noted that AI margins are improving faster than cloud did at a similar stage. Additionally, Jefferies pointed out that Microsoft Corporation (NASDAQ:MSFT) can make money from its infrastructure no matter which AI model or agent wins. The research firm said that the company has a model-agnostic strategy, focusing on controlling the platform where models are deployed, governed, and monetized.

According to Jefferies, Microsoft Corporation’s (NASDAQ:MSFT) full-stack AI solution, including governance, is attractive to chief information officers. The firm also highlighted that Microsoft Corporation (NASDAQ:MSFT) is trading at about 21 times its expected EPS for fiscal year 2027, which is lower than its 10-year average of 23.5 times.

Microsoft Corporation (NASDAQ:MSFT) is an American technology company that specializes in AI-powered cloud, productivity, and business solutions. The company develops and markets software, services, and hardware.

While we acknowledge the potential of MSFT as an investment, we believe certain AI stocks offer greater upside potential and carry less downside risk. If you’re looking for an extremely undervalued AI stock that also stands to benefit significantly from Trump-era tariffs and the onshoring trend, see our free report on the best short-term AI stock.

READ NEXT: 11 Best Tech Stocks Under $50 to Buy Now and 10 Best Stocks Under $20 to Buy According to Hedge Funds.

Disclosure: None. Follow Insider Monkey on Google News.

Continue Reading

-

Bill Gates Says Warren Buffett ‘Doesn’t Know Much About Cooking Or Art Or A Huge Range Of Things’ — But His Ability to Read People is ‘Magical’

Some people try to know everything. Warren Buffett made billions knowing what to ignore.

The HBO documentary “Becoming Warren Buffett” from 2017 shows how Microsoft co-founder Bill Gates went from skeptical to fully convinced — not because of what Buffett knew, but because of how he thinks.

Melinda French Gates, who was married to Bill at the time of the film, said it took persistence to make the meeting happen.

“He’s one of the smartest people we know,” she said in the film. “I was at a couple of the family dinners at the Gates house where Mary, Bill’s mom, was trying to convince him to come out to the family place at Hood Canal to meet Warren Buffett, and he was resisting because he was really busy with Microsoft. Finally he said, ‘Mom, okay, I’ll come for lunch.’”

Don’t Miss:

Gates said he showed up without much interest.

“So the two of us flew out there somewhat reluctantly,” he said. “Buying and selling stocks, which is how I thought of Warren, wasn’t a particular interest to me and didn’t seem like value added.”

That didn’t last.

“It turned out that was completely wrong,” Gates said. “We knew that day that we’d be very close friends. In fact, we just couldn’t get enough of each other.”

“Shortly after I met Bill Gates, Bill’s dad asked each of us to write down on a piece of paper one word that would best describe what had helped us the most,” Buffett said in the film. “Bill and I, without any collaboration at all, both wrote the word ‘focus.’”

For Buffett, that word drives everything.

“Focus has always been a strong part of my personality,” he said. “If I get interested in something, I get really interested. If I get interested in a new subject, I want to read about it, I want to talk about it, and I want to meet people that are involved in it.”

Gates saw the same pattern.

“We both love to work hard,” he said. “Neither of us like frivolous things.”

Trending: Skip the Regrets: The Essential Retirement Tips Experts Wish Everyone Knew Earlier.

Gates didn’t describe Buffett as well-rounded.

“He doesn’t know much about cooking or art or a huge range of things,” he said in the documentary.

Continue Reading